A Different Way to Think About Investing

Most investors focus on what can go right.

Long-term success often comes from planning for what can go wrong - and building portfolios that don't rely on a single outcome.

Large pension and endowment funds take this approach. They focus on diversification, asset allocation and long-term decision making - not short-term market noise.

The same principles apply here - with an added focus on tax efficiency and how capital will ultimately be used over time.

Black and White Insights

Read the latest on markets and more from our team as well as experts and thought leaders at RBC.

Real Situations We Help With

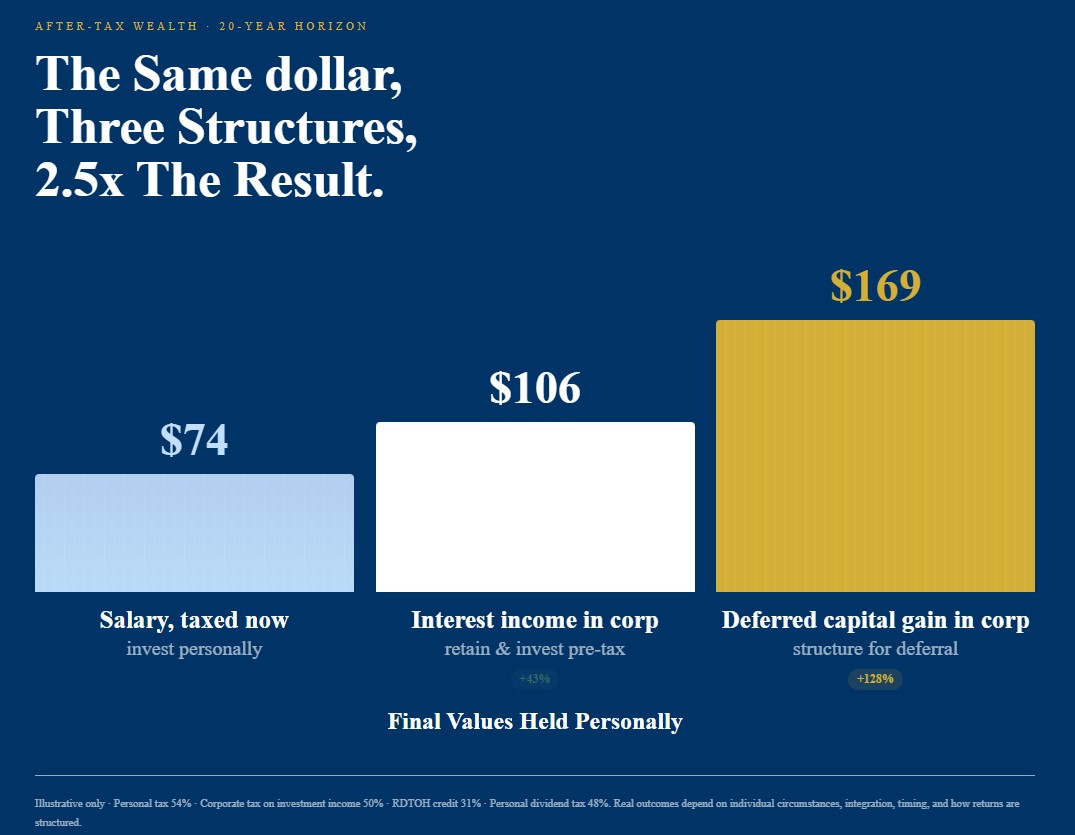

Managing Investments Inside a Corporation

Business owners often accumulate significant assets inside a corporation but aren't sure how to invest or eventually draw on those funds. The focus is balancing tax deferral today with how that capital will be used over time.

A $100 of salary or business income, invested for 20 years at a 5% return. What you keep depends less on the market than on the structure you hold it in.

Transitioning Into Retirement

Moving from saving to generating income introduces a new set of decisions - including how to structure withdrawals across accounts and maintain consistency.

Sitting on Excess Cash

After a business sale, bonus or period of uncertainty, many clients find themselves holding more cash than intended. The challenge becomes how to redeploy it thoughtfully without overreacting to short-term markets.

Portfolios That Feel Too Simplistic

Some clients come in with portfolios that are heavily concentrated or overly reliant on traditional stocks and bond allocations. They're often looking for a more diversified and structured approach.

I spent two decades managing and analyzing investments before moving into wealth management. That experience shapes how I approach portfolios today - with a focus on structure, tax efficiency and long-term decision making rather than short-term market views.

Who I Work Best With

The core investment philosophy stays consistent - the way it's applied depends on your situation.

Physicians & Incorporated Professionals

Incorporation creates flexibility - but also more decisions around what to do with excess cash, where to invest it and how to draw income over time.

We help connect corporate and personal accounts so those decisions aren't made separately.

Business Owners

Your business is often your largest asset, but its not always clear how it should connect to your personal wealth.

From retained earnings to succession planning, we help make those decisions work together over time.

Retirees & Families

The focus shifts from growth to income, preservation and predictability.

We use detailed financial projections to map out your plan, so you can spend with confidence.

What Actually Drives Long-Term Results

Most investors focus on returns. In practice, tax efficiency, diversification and disciplined decision-making tend to matter more over time.

Portfolios are built with this in mind - not just around individual investments.

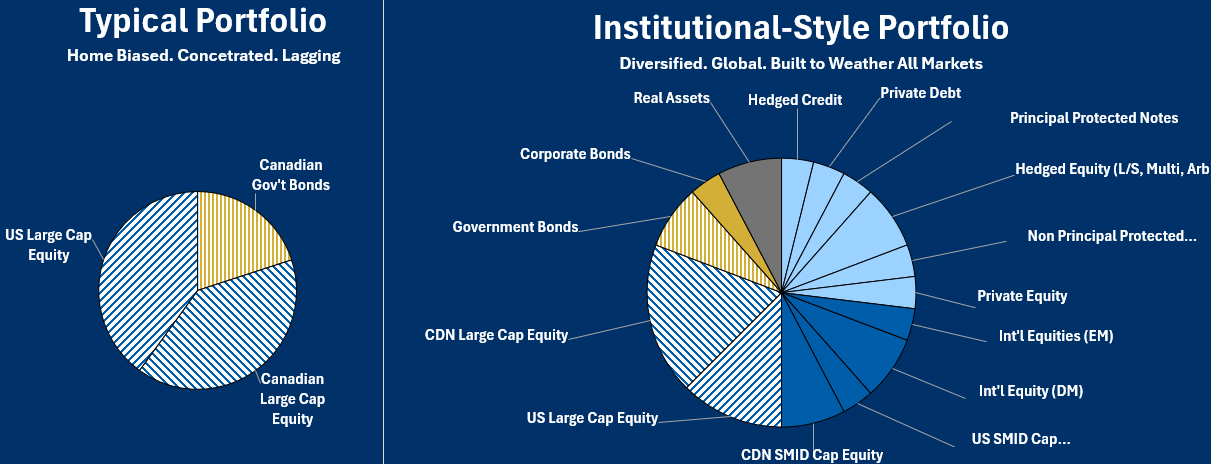

How Portfolios Are Built

Good portfolio construction is not just about picking investments. It is about structuring portfolios to capture long-term market returns while managing risk and taxes along the way.

Research has shown that a small percentage of stocks have driven the majority of long-term wealth creation. That is one reason we emphasize broad diversification and allowing winners to compound, rather than trying to constantly rotate between ideas.

We combine this with disciplined rebalancing, tax-aware strategies such as tax-loss selling, and maintaining liquidity so that periods of market volatility can be used as opportunities rather than risks.

Tax-Aware Decisions

After-tax outcomes matter more than pre-tax returns.

This includes how income is generated, when gains are realized and where investments are held. Small decisions like limiting passive income in a corporation or tax-loss selling can compound into meaningful differences over time.

Adapting to Market Conditions

If someone tells you with confidence where markets are going, it's worth questioning.

We don't try to predict markets. We prepare for them. That means building portfolios with enough diversification and liquidity to stay invested through uncertainty, and to take advantage of dislocations when they occur.

Next Generational Planning

My Story and Why it Matters to Me:

When I was 14 I started my first job as a busboy at Outback Steakhouse (which I love reminding my kids about) and was motivated to start investing in its stock. It was the perfect time before rocketing higher along with all other companies in the mid 90s. My father's Investment Advisor recommended I read the Wealthy Barber and that was the start of a long series of reading books and investing in other stocks. I want to pay it forward and teach the next generation the value (and joy) of investing!

Education for Kids and Grandkids

Teaching What School Doesn't - and make it practical.

Opening Accounts for Minors:

Ages 0-12: RBC Leo's Young Savers Account (free bank account)

Ages 14+: RBC Direct Investing Practice Account (free; $100,000 practice money for stocks/options)

Ages 16+: DS Investment Account (requires parent signatory) or in-trust account

All Ages: Mydoh app, parents can load money and set up tasks, allowances, and savings goals for up to five children.

Timeless Lessons on Money:

The best investment is understanding how money works and the best asset you can have is knowledge.

Suggested Book Themes: Compounding returns, dollar cost averaging, paying yourself first, stock picking

All-Time Favorites:

- Beating the Street (Peter Lynch)

- The Wealth Barber (David Chilton)

- The Psychology of Money (Morgan Housel)

- The Most Important Thing (Howard Marks)

- Thinking Fast and Slow (Daniel Kahneman)

Age-Appropriate:

- 10+: From Piggy Banks to Stocks (Maya Corbic)

- 13-16: A Rich Future (Noah Booth)

- 16+: Seventeen to Millionaire (Douglas Price)

How Well Do You Understand Money?

Most people understand the basics of money, but many underestimate what actually drives long-term outcomes. See how you compare.

Generational Wealth Transfer Scenarios (Tax-Efficient Strategies)

As portfolios shift from growth to income, planning how assets pass to the next generation becomes critical. When the focus becomes less about what to invest in, and more about how everything gets used over time, people get confused and lost, and that is normal. That's exactly where I come in to help you navigate the complexity and turn confusion into clarity. We explore tax-efficient transfer strategies so more wealth reaches your kids and grandkids, not the tax office. If you're thinking about how to structure wealth transfer to the next generation, I'm always happy to have a conversation

Estate Planning, In-Trust Accounts, and Insurance: Complete Protection

Building wealth is only half the battle. Protecting it and ensuring it's distributed according to your wishes requires a solid plan. We cover wills, trusts, guardianship designations, power of attorney, in-trust account strategies, life insurance, and beneficiary designations. In-trust accounts teach your children about investing while managing tax efficiently. Life insurance and clear beneficiary designations protect your family's financial future. These decisions require expert guidance to navigate successfully. Let's work together to ensure your family's future is secure.

Frequently Asked Questions

What is the best way to invest through a corporation in Canada?

The best way to invest through a corporation in Canada typically involves balancing tax deferral with how funds will eventually be withdrawn. This includes selecting tax-efficient investments, managing how income is generated, and coordinating corporate and personal planning over time.

What is the most tax-efficient way to withdraw income in retirement in Canada?

The most tax-efficient way to withdraw income in retirement in Canada usually involves combining multiple sources — such as registered accounts, dividends, and capital gains — to stay within lower tax brackets and maintain flexibility over time.

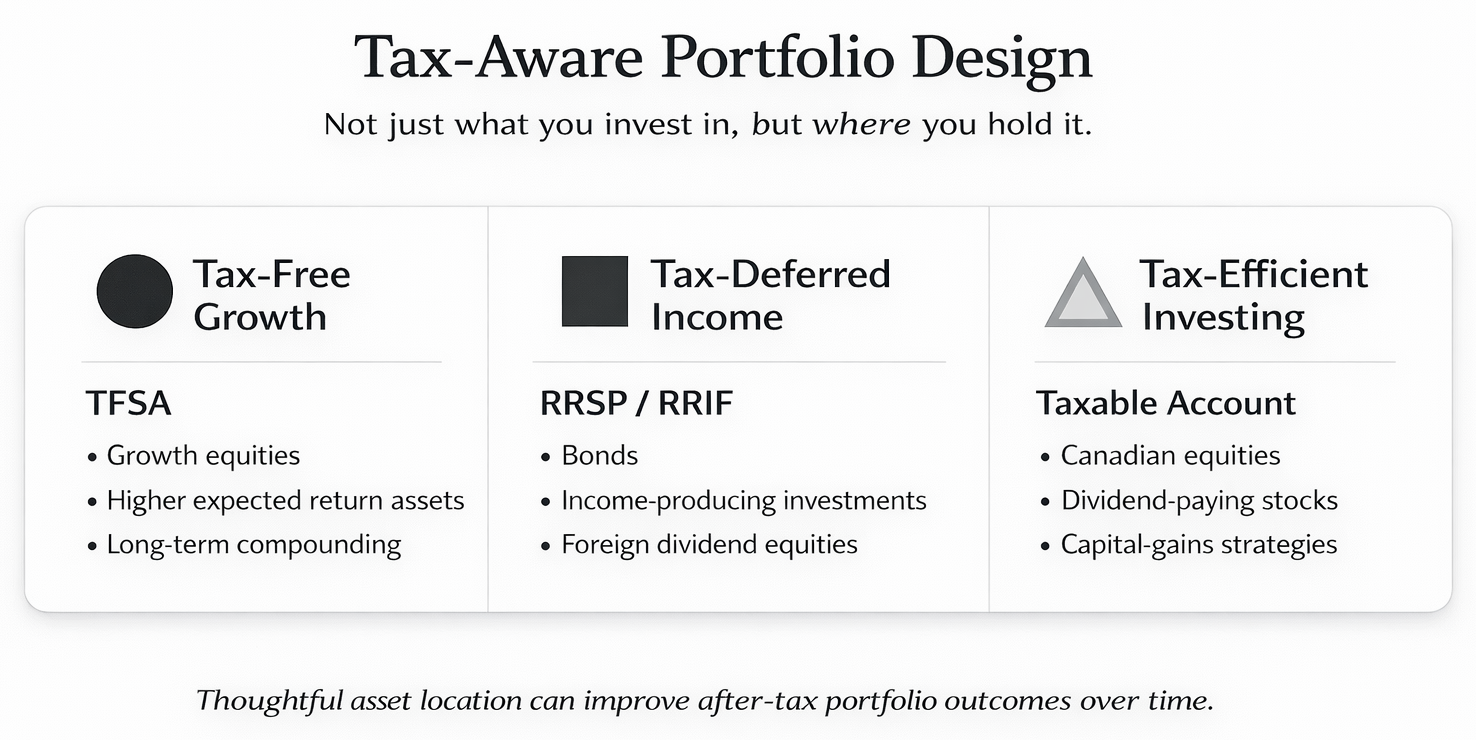

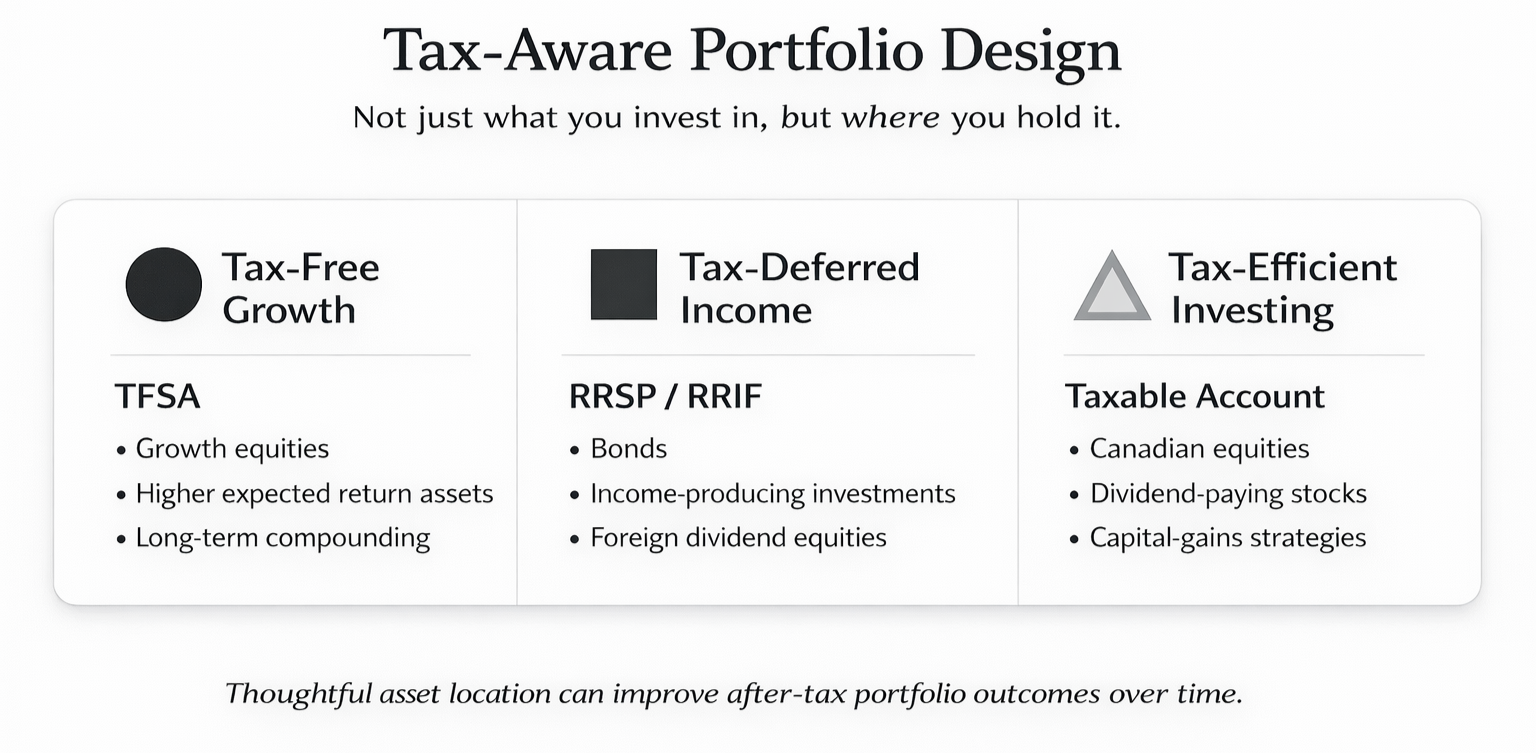

How should investments be structured across TFSA, RRSP, and taxable accounts?

Investments should be structured across TFSA, RRSP, and taxable accounts based on tax treatment and time horizon. Growth-oriented assets are often placed in tax-free accounts, while income-generating investments may be better suited for tax-deferred or taxable accounts.

Is paying a financial advisor worth it in Canada?

For many investors, the value of a financial advisor comes from tax efficiency, disciplined decision-making, and structuring income over time — not just investment performance. Avoiding costly mistakes and improving after-tax outcomes can have a meaningful long-term impact.

Should I invest personally or through a corporation in Canada?

Investing through a corporation in Canada can provide tax deferral, but it also introduces complexity when funds are withdrawn. The right approach often involves coordinating both corporate and personal investments based on income needs and long-term goals.

What are alternative investments and should I use them?

Alternative investments include assets such as private credit, infrastructure, and real assets that can provide diversification beyond traditional stocks and bonds. They may help improve portfolio resilience when used appropriately within a broader strategy.

When do structured investment strategies make sense?

Structured investment strategies can be useful in certain market environments, particularly when volatility is elevated or return expectations are more uncertain. They are typically used selectively to help define outcomes or enhance yield.

How often should a portfolio be rebalanced?

Portfolios are typically reviewed and rebalanced periodically or when allocations drift meaningfully from their intended levels. Rebalancing helps maintain the desired risk profile and encourages disciplined decision-making over time.

What matters more in investing: returns or structure?

Returns are important, but over time, tax efficiency, diversification, and disciplined decision-making often have a greater impact on overall outcomes. How investments are organized and used tends to matter more than any single return.