Navigating the New Normal: Investing in an Age of Heightened Geopolitical Risk

Geopolitical tensions in the Middle East have sparked short-term market volatility, driving oil prices higher and shifting investor focus toward inflation risks. Despite near-term uncertainty, strong economic fundamentals and AI-driven growth support

Geopolitical tensions in the Middle East have sparked short-term market volatility, driving oil prices higher and shifting investor focus toward inflation risks. Despite near-term uncertainty, strong economic fundamentals and AI-driven growth support

Ascendant Wealth Partners

March 16, 2026

Highlights

- Market Volatility: The conflict in Iran has triggered market volatility across multiple asset classes, beginning with the initial strike on Iran at the end of February

- Energy Disruptions: Oil prices have surged due to constrained supply and fractured global transport routes, specifically following the substantial closure of the Strait of Hormuz

- Bond Market Signals: The bond market is pricing in higher inflation expectations driven by rising energy costs. While U.S. Treasury yields typically decline during market shocks, interest rates have increased—suggesting that inflation is a primary concern and the immediate risk of a recession remains low

- Economic Outlook: The global economy remains on track with solid economic growth expectations for 2026. The market continues to expect robust earnings growth this year, with the build-out and adoption of Artificial Intelligence (AI) serving as a significant catalyst for GDP growth and U.S. S&P 500 earnings per share growth

- Portfolio Strategy: We believe a carefully structured, globally diversified portfolio will help navigate short-term noise related to current geopolitical conflicts. Historically, markets have shown similar weakness during such events, followed by relatively quick recoveries as tensions subside

- Risk Management: Given the economy's strong foundation, we remain fully invested and are not looking to reduce risk at this juncture. We recently introduced emerging market equity and precious metals exposure to select portfolios, where appropriate, based on our clients’ objectives and risk profile

Today’s conflict in the Middle East has introduced short-term volatility across all major markets. Oil stocks are one of the major beneficiaries, as a supply shock has occurred due to curtailed production and the closure of the Strait of Hormuz, which has halted approximately 20% of global oil transportation.

Interest rates have generally increased across the yield curve, as inflation expectations mount; the length and severity of the conflict will determine whether higher inflation is a long-term threat or a short-term development. Equity markets have also moved to a "risk-off" stance—a common reaction when geopolitical events surface.

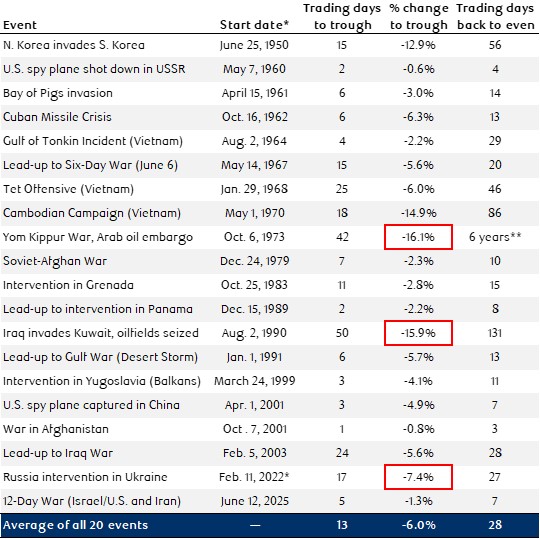

We reviewed previous geopolitical conflicts as a guide, as history can provide important insights. The following table identifies market responses to various military operations dating back to the end of World War II. In 19 of the 20 events, the U.S. equity market fully recovered its initial drawdown within a few months.

Figure 1: S&P500 Responses to Select Military Interventions and Hostilities since World War II

Red circled data indicate events impacted by crude oil price spikes.

* Dates attempt to capture any material pre-event impact; actual starting dates may differ.

** Following the Arab oil embargo, other economic and monetary factors negatively influenced the number of days to get back to even; this event is not counted in the average.

Source: Ascendant Wealth Partners, RBC Wealth Management, RBC Global Asset Management, National Security Archive at George Washington University, Wikipedia, U.S. Naval Institute.

While inflation risks are on the rise, we expect the economic growth outlook for 2026 to remain unfazed. Equity markets are projected to generate double-digit earnings growth, with operational efficiencies expanding margins—driven by the broader adoption of AI across various industries and sectors. Major U.S. technology hyperscalers—Amazon, Google, Meta, and Microsoft—are projected to spend U.S. $650 billion on AI-related infrastructure. These expenditures, combined with stimulus injections from developed governments and an anticipated interest rate cut by the U.S. Federal Reserve later this year, serve as tailwinds that will support economic growth.

We continue to monitor overseas events and, as with any such development, are assessing the duration, severity and economic impact of the conflict. While major economies are collaborating to release 400 million barrels of oil from global strategic reserves, this volume represents less than four days of global demand. If oil prices remain elevated, there could be a significant impact on the U.S. consumer, who accounts for approximately 70% of U.S. GDP. However, with the U.S. midterm elections approaching and affordability and inflation remaining primary concerns for Americans, we believe the U.S. administration is mindful of the need for a swift end to the conflict.

Considering the current geopolitical landscape, we are monitoring two primary scenarios and their potential market impacts:

Short Disruption Scenario: If tanker flows normalize within a few weeks and oil prices move back towards $60–$65 per barrel, economic damage would be limited. Historically, geopolitical events alone have not led to sustained equity volatility. Under these conditions, we believe equity markets would likely remain supported.

Prolonged Disruption Scenario: If the Strait of Hormuz remains closed or severely constrained for months -- causing tanker flows to remain near zero -- oil prices will stay elevated long enough to accelerate inflation and dampen growth. A sharp and persistent rise in oil prices poses a significant risk to the current business cycle. In this environment, equity markets would likely face downward pressure as growth headwinds would outweigh near-term earnings support.

Portfolio Positioning

We maintain a well-diversified portfolio and do not intend to reduce our risk exposure at this time. Nevertheless, we continue to tactically evaluate market opportunities and will adjust our positioning as conditions evolve, consistent with the framework outlined above.

The following themes outline our current outlook, including two recent additions designed to optimize the portfolio for the current environment:

- Short-Term Bonds and Floating-Rate Loans: We are focusing on these areas as they offer superior protection against inflation and rising interest rates

- Canadian Equities (Exposure to Hard Assets): We maintain a significant weight in Canadian equities that hold direct hard assets across the commodity complex. If inflation continues to trend higher, these commodities serve as an effective hedge

- Precious and Base Metals: We recently introduced positions in gold miners and silver and copper producers. Precious metals, particularly gold, provide the following portfolio benefits:

- Inflation Protection: Strong performance and real returns during periods of high inflation

- Currency Hedge: Maintaining purchasing power against currency devaluations, performing well during periods of U.S. Dollar weakness

- Safe-Haven Status: Acting as a hedge during market crises and geopolitical conflicts; demand typically increases during war or financial and political unrest

- Risk Diversification: As the traditional correlation between stocks and bonds has become increasingly positive, gold acts as a stabilizer to reduce overall portfolio risk

- Sector Opportunity: We believe Canadian miners and producers are currently under-owned by the investment community. Given their strong performance and favourable diversification characteristics, we expect active managers to increase their allocations to the Materials sector to manage benchmark risk, which should drive share price gains

- Global Diversification: While Canada remains a beneficiary, and we maintain direct exposure to U.S. large-cap and mid-cap equities—also focusing on durable AI-related technology themes—we find international and emerging market equities increasingly attractive from a relative valuation perspective

- Emerging Markets: We have recently introduced emerging market equities on a selective basis, which are gaining favour due to several structural factors:

- Attractive Valuations: Forward valuations are below 14x, compared to approximately 22x for U.S. large-caps

- Earnings Growth: Projections of 20% over the past year now match or exceed those of the U.S.

- Currency Tailwinds: A stable or weakening U.S. Dollar benefits emerging markets by reducing the cost of servicing US$-denominated debt and encouraging capital inflows

- Demographics and GDP: Emerging markets represent over 80% of the world’s population and drive the majority of global GDP growth. These markets are outperforming the developed world and are forecasted to contribute the bulk of global economic output by 2035

- Risk Profile: In a significant shift from previous decades, the volatility of emerging market equities has moderated substantially and is now comparable to that of the U.S. and other developed equity markets.

- Alternative Strategies: We continue to utilize uncorrelated equity alternatives, such as private equity and private infrastructure. These are managed by strong operators and offer a compelling illiquidity risk premium.

To gain deeper insight into current geopolitical dynamics, we invite you to review a recent publication from Kelly Bogdanova and the RBC Global Portfolio Advisory Committee. Their analysis, titled 'Then and now: Market reactions to military conflicts and what they mean today,' can be accessed at the link below: