Barasch - Wellwood Wealth Partners

June 16, 2026

Now, some ground-rules are in order before we launch into this: 1) this is not about individual pain – yes, we get it Leaf fans, it’s been hard for the last 300-years, but the Raptors won in 2019 and the Bue Jays won twice in the 1990s, so you need more than just Leafs pain to win this thing. 2) the combination has to make sense. For example, no one is a fan of the Buffalo Bills (no Super Bowl wins, but lots of losses), the Cleveland Guardians (no World Series wins in like 100 years) and the Toronto Maple Leafs (no Cups since the Beatles were still releasing new music). We suppose someone might root for Buffalo and the Leafs, but you are not going to convince us that this same person roots for Cleveland. 3) You have to have reasonable other choices. In other words – you could have picked the Lakers (who win titles like every other year), but you chose to root for the Clippers (who implode every year) – and when you add this to the other choices you made, well, you got fan-hosed.

Anyway, we mention this today because before this past weekend and really before the last two months, there was one answer to the question of the most painful combination. We are, of course, referring to the combination of those who hail from New York and chose to root for the Jets (no titles since before we landed on the moon) over the Giants (four Super Bowl titles in the last 40-years), the Mets (one World Series title that is now 40-years old) over the Yankees (213 World Series titles in the last 30-years), the Rangers (literally one Stanley Cup in 86 years) over the Devils (way too many Cups to count and the Islanders (four Cups in a row once) and the New York Knicks (no titles in 53 years).

Now, surely, none of these poor fools exist – I mean, who could be this combination of sheer dumb bad-luck? Well, sadly, they do exist – in fact, the author of this very piece happens to be one of those sad, pathetic souls who is almost never allowed to have nice things.

But, beginning on April 23rd, when the New York Knicks lost to the Atlanta Hawks by one point for the second straight game to fall behind 2-1 in their opening round playoff series – something magical started to happen. These sad, pathetic losers of whom I am one – wait, sorry – was one – were treated to the truly extraordinary. Thirteen consecutive wins, 15 out of 16, blowout victories, multiple rallies from 20+ point deficits and at last – an NBA championship that was more than 19,000 days in the making.

For those that are – sorry were – part of this sad, sad group – enjoy this moment – you deserve it. And as I said to my son Jalen OG Anunoby Brunson Barasch – we got one, dag nabbit, we got one.

As we head into the second half of 2026, we thought we would point to five things that we think will be keys to the back of the year. They are in no particular order of importance, so let’s get to it.

The IPO-pocalypse – beginning with SpaceX (note that we are restricted about writing about SpaceX but will do so when the restriction is lifted) and then followed by Anthropic and OpenAI, the stock market is about to see roughly $4 trillion of initial public offerings (IPOs) in the next few months from the new Big 3. All three are likely to raise between $50bn and $100bn when they initially come public, which is a staggering amount by historic standards. Add to this recent equity issue announcements from the likes of Google-parent Alphabet ($85 billion) and Facebook/Instagram-parent Meta (no amount disclosed as of yet but thought to be ~$50 billion) and this is an unprecedented amount of new equity coming to the markets.

The largest issuance of stock in history on an IPO was Saudi Aramco in 2021 when it raised ~$30bn, so what we are about to see over the next several months is truly boldly going where no IPO has gone before. And we are basically going to do it 5x, if we include Alphabet and Meta. Now, the U.S. stock market is ~$75 trillion, so while the IPOs/issuances are a big nut to swallow, the market will ultimately manage through it. But we would not be surprised to see some odd dislocations in certain stocks that have similar exposure to the Big 3, as investors will need to find the funds necessary to add these new positions.

Bottom Line: markets are going to have a bit of a supply/demand issue over the next few months, and we would expect this to weigh on the share prices of some names that will likely be a source of funds for these new positions. We plan to use this weakness as an opportunity to add to some of the companies that we like, as we do not see this supply issue creating a long-term headwind.

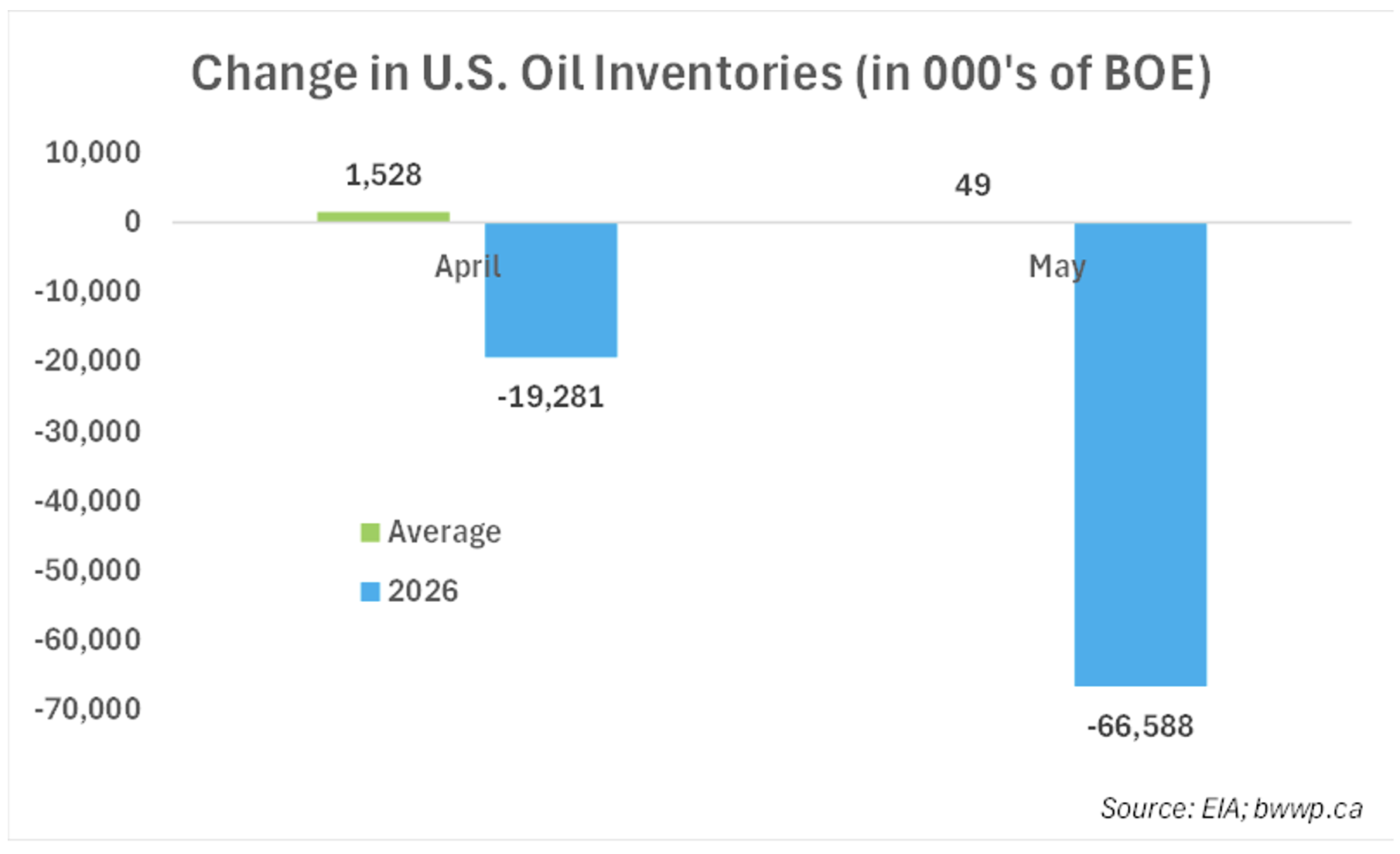

The Potential for an Oil-pocalypse – this is a fascinating time for the oil market. Let’s start with a chart and then comment:

The “don’t call it a war” in Iran and the virtual shutting down of the Straits of Hormuz has put significant pressure on global oil reserves as markets try to adjust to the loss of ~10-15% of global oil flow. U.S. oil inventories are now down ~85 million barrels over the past two months, which is ~35 million more barrels than have been drawn from inventory over any other prior two month period over the past 45-years.

Now, it’s important to note that North America still has ample reserves of oil – the U.S. still has nearly 800 million barrels of reserves, which is nearly two months of their daily consumption – but the rest of the world is in varying degrees of trouble as reserves were not particularly large to begin with and have been rapidly drawn down as the Iran conflict dragged on.

That said – oil prices have come down sharply since President Trump promised for the 37th and 38th times that an Iran deal was near and since he has now announced a treaty that probably should not be called a treaty since there was never actually a war – oil has begun to normalize – albeit it remains ~20% higher than the start of the do not call it a war.

Bottom Line: we are generally positive on oil stocks as they are benefitting from what we would call “bonus free cash flow”. This cash flow, which is a result of the $20-$30 pickup in oil prices since the Iran war began, is going straight to share buybacks and debt reduction, which will make these stronger companies for existing shareholders when oil prices eventually settle back down.

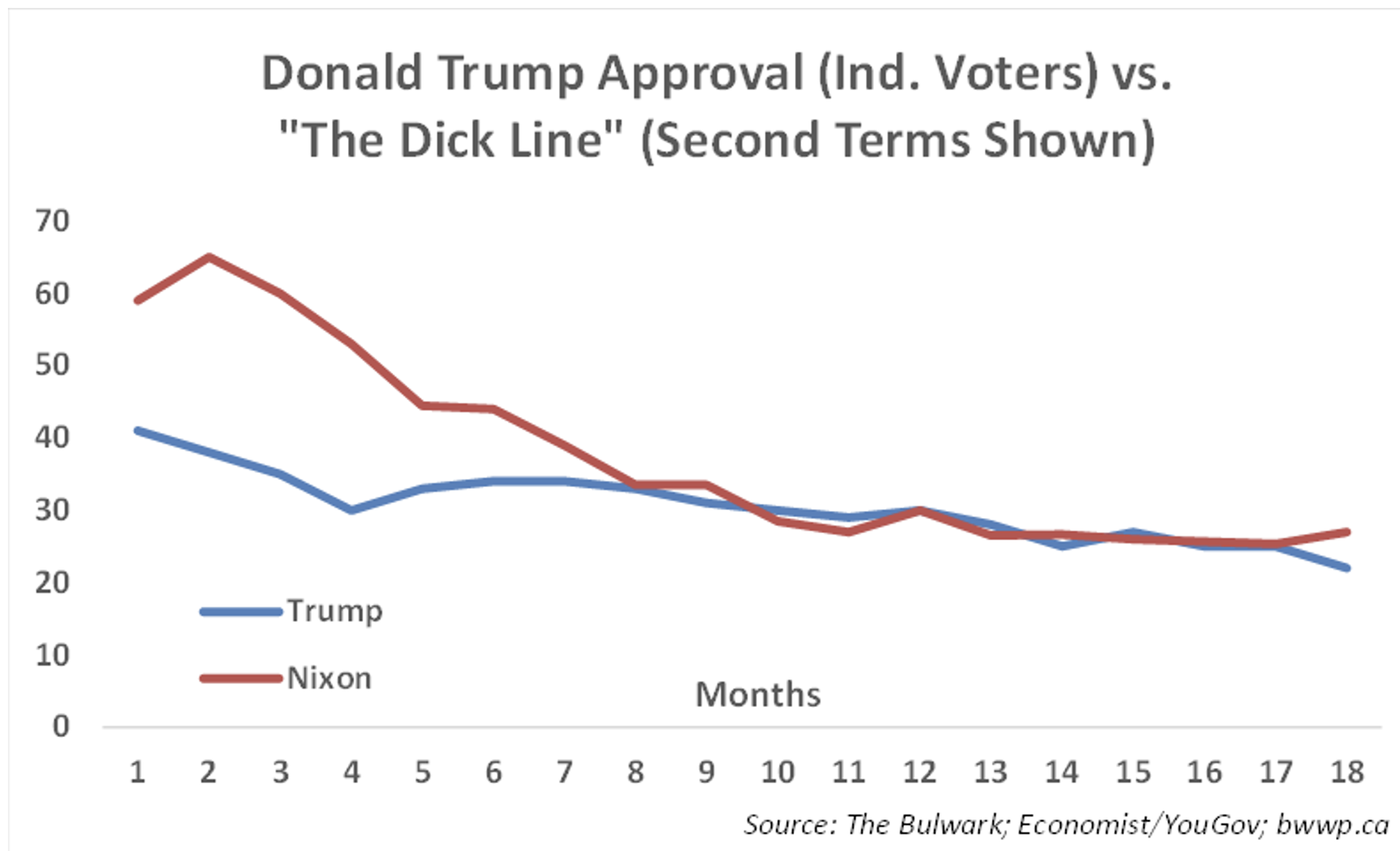

Trump’s Approva-pocalypse – we will not spill too much more ink on the upcoming midterm elections. They are generally bad for the incumbent party; although, through various re-districting efforts that have given the Republicans a further advantage, what was likely to be an overwhelming Democratic wave, is likely to now only be, umm, “whelming”. And while midterms are almost always bad for the incumbent party, they are usually especially awful when the President is sporting an approval rating that is below various lines. There is the obvious – 50%, which is indicative of a President who has less than half of the electorate on his side – and then the less obvious – the so called “W Line”, when the President has less support than George W. Bush did at his nadir in 2006 and 2008 (around 35% support). And there is “the Dick line”; and before your mind goes somewhere it should not, we are referring to the approval rating that President Richard “Dick” Nixon experienced during his second term. Let’s look at a chart and then comment:

Above we have compared Donald Trump’s support amongst Independent voters, which, given the partisan nature of U.S. politics, is a better gauge of where his support truly lies, vs. Nixon’s support in his second term.

Living at “The Dick Line” is not going to bode well for Trump and the Republicans in November and it is so bad that the Senate, which should not be in play given the number of red states the Democrats need to win to takeover – Texas, Alaska, Ohio, maybe Iowa – is very much in play with most betting sites giving the Democrats a better than one in three chance of winning.

Bottom Line: the Democrats will take back the House, but the Senate will end at 50/50. From an investor perspective, this likely does not have big ramifications; although, it makes more tariffs less likely as a Democratic controlled House will have some ability to temper Trump’s worst instincts.

The Post-Midterm-olypse – Recent primary elections are giving us a good sense as to what the Republican playbook is likely to be in the days immediately following the November midterms. Several blue states – California being the big one – are slow when it comes to counting mail-in ballots as they are quite liberal in how late they allow ballots to arrive by mail – generally post-marked by Election Day. This is going to lead to situations in which many House races are going to show the Republican candidate leading on Election night (and in the few days that follow), as Republican voters tend to vote in person, while Democratic voters are more likely to vote by mail, thus delaying their vote count. And as we have seen in the primaries, Trump and many of his mouthpieces are likely to proclaim this as some sort of great steal of the Election, when it is simply a bad system for counting votes. With the House likely to be very close, we would not be surprised to see some effort by current House Speaker Mike Johnson (one of the aforementioned “mouthpieces”) to question sitting some of the Democrats that receive the late surge of mail-in votes, which could put us in uncharted territory in the weeks leading up to the new Congressional term in January of 2027.

Bottom Line: The only real historic parallels we have for this are 2000 when we went roughly a month without knowing who had won the Presidential election between George W. Bush and Al Gore and 2020 when Trump attempted to deny that he had lost the 2020 election even though he lost by ~7-million votes. The stock market lost ~8% in 2000 during the period of uncertainty, but we would note that we were already in the midst of a bear market at the time, so it is hard to blame the losses solely on not knowing who had won. Conversely, the post 2020 election saw a massive rally in stocks, but again, we would credit this mostly to exogenous circumstances – finding a vaccine for Covid – as opposed to anything related to the “stop the steal” movement.

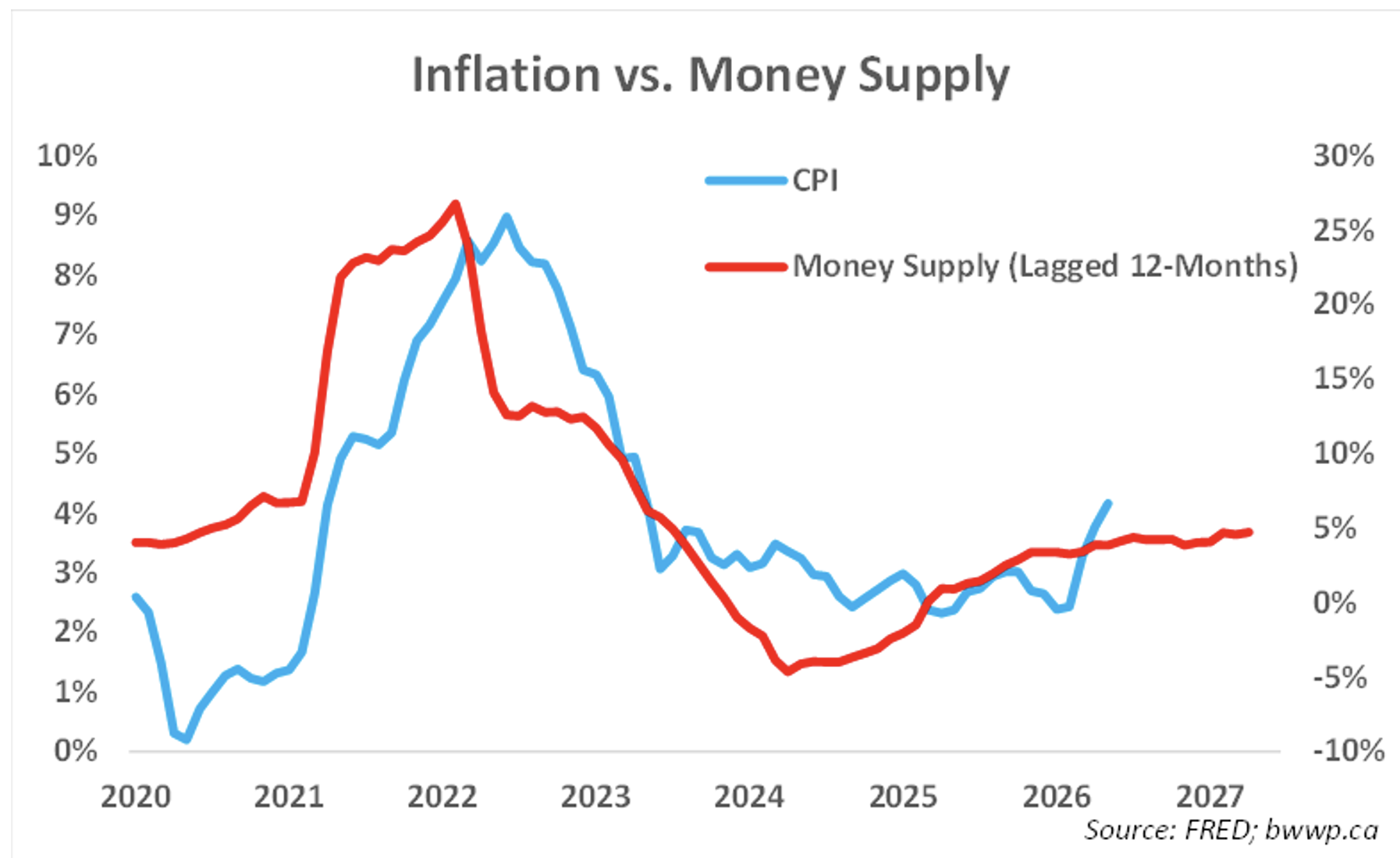

Apoca-flation - not to sound like a broken record as we have been harping on the risks of an inflation flare-up for the better part of the past two years, but we are concerned about an inflation flare-up in the second half of 2026 into 2027. That said – we might already be there, as inflation started flaring over the past couple of months and our favorite gauge of future inflation – the money supply – indicates that we have yet to see the peak:

Central banks and central governments put their collective pedals to the metal in 2025 through rate cuts and massive stimulus packages and that is coming home to roost in 2026. It is great for risk markets as there is unprecedented amounts of liquidity in the system and markets love liquidity. But the downside of this liquidity fix is that it will tend to create inflation unless you take steps to rein it in ala rate hikes and fiscal restraint. Since the U.S. is very unlikely to do either – we would expect to have an inflation problem in 2027.

The one caveat to this would be the dual role that AI is playing in the inflation story. On the one hand, massive spending on infrastructure projects to support the buildout of AI is creating inflation pressures, while on the other hand, AI has the potential to be a deflationary force as it lowers the costs of previously expensive tasks.

Bottom Line: we are currently in what we would call the balanced phase. While inflation concerns and risks are rising, these concerns are offset by the aforementioned liquidity in the system and the powerful tailwind this provides to markets. With corporate profits likely to grow at double digits, we remain generally positive; although we are prepared to act should the delicate balance start to fray.