Barasch - Wellwood Wealth Partners

February 9, 2026

From the Super Bowl to Silver

Our story begins in 1959, when a wealthy Arkansan named Lamar Hunt applied for an NFL expansion franchise in Texas. At the time, baseball was the dominant sport in the United States with football barely an afterthought and Hunt’s application was rejected on the grounds that the NFL did not wish to oversaturate the market. Not to be deterred, Hunt sought out a group of similarly rebuffed individuals and together they formed a rival upstart league called the American Football League (AFL) with Hunt owning the Dallas Texans franchise. The NFL responded by founding its own Dallas-based franchise – the Cowboys – which, needless to say had a negative impact on the Texans ability to draw fans to the new team in the new upstart league. After three years of toiling in the head to head with the Cowboys, Hunt moved the Texans to Kansas City and rebranded them “the Chiefs”.

By 1966, the AFL was successful enough (and was driving up the cost of players) that it had become clear that the NFL would be better off considering some sort of merger between the two leagues. While the ultimate merger would not be concluded until 1969, beginning after the 1966 season, the two leagues would play what was to be called the AFL-NFL Championship. Hunt, however, did not like the name, and wrote a letter to then NFL commissioner Pete Rozelle that included the line: “I have kiddingly called it the 'Super Bowl,' which obviously can be improved upon.”

While Hunt may have been “kidding”, the media quickly picked up on the name “Super Bowl” and this became the de facto moniker for the upcoming first intra-league battle. By 1969, Super Bowl would become the official name of the game with the first two AFL-NFL Championships retroactively rebranded as Super Bowls I and II.

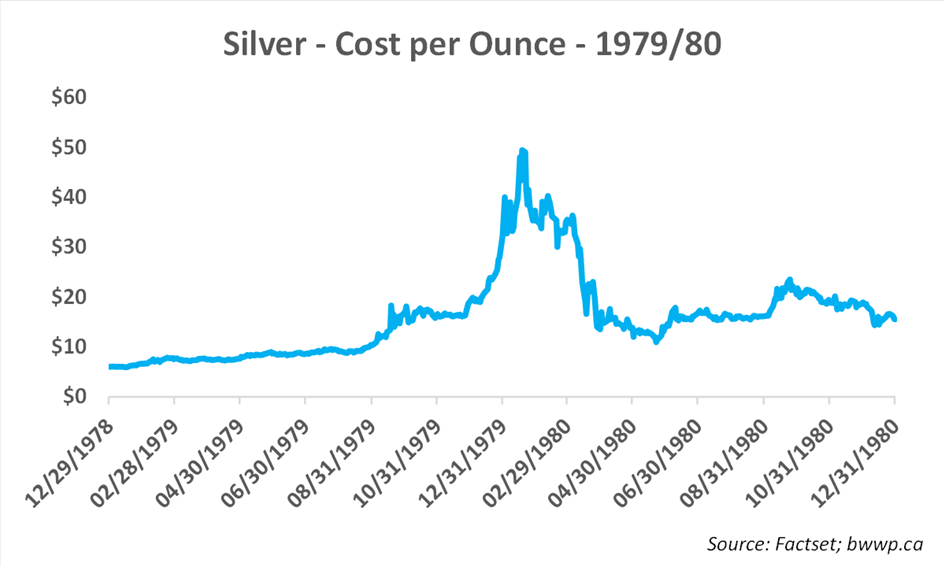

Fast forward more than a decade to 1979/80 and Hunt, along with his brothers Nelson and William, made the news in an entirely different way. For much of the 70s, the three brothers had bought an inordinate amount of silver. This buying accelerated in 1979 when the brothers may or may not have attempted to corner the entire silver market (they gain controlled of close to 1/3rd of the market) driving prices through the roof. From the beginning of 1979 through January of 1980, the price of silver went up seven-fold with the Hunt’s making billions, at least on paper. However, as with any market than goes parabolic, the end came swiftly and violently, leading to what came to be known as “Silver Thursday”:

Beginning in early 1980, after the price peaked at nearly $50/ounce (it had been under $6/ounce in late 1978), silver prices began to fall, culminating on Thursday March 27th, 1980 when a consortium of banks were forced to bail out the Hunt brothers for fear that the entire financial system was at risk of their folly (a similar thing happened in 1986 when a Chicago magnate named Abe Froman attempted to corner the market on sausage). Along with their other investments, the Hunt’s lost billions in the 1980s, culminating in a bankruptcy filing in 1988; although, Lamar Hunt, “father of the Super Bowl” would remain owner of the Chiefs until his death in 2006.

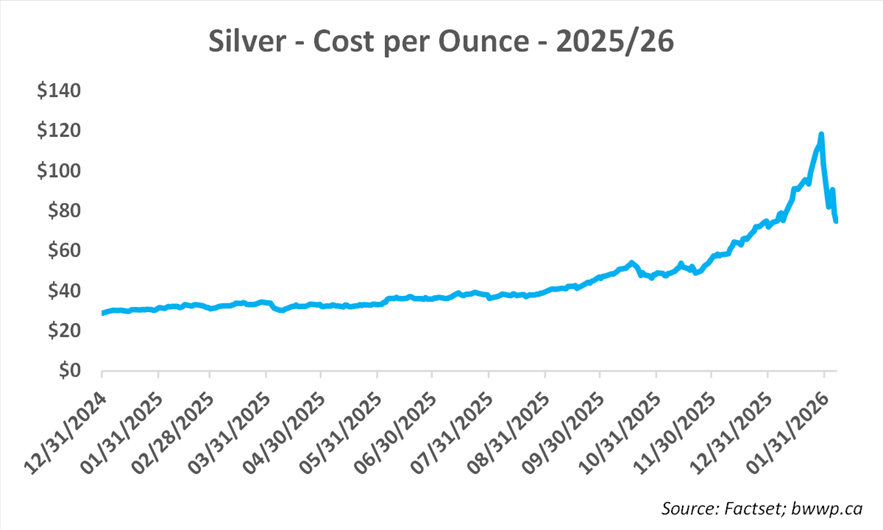

We are reminded of Hunt not only because this happens to be the week after the Super Bowl, but also because the silver market has recently demonstrated a very “Hunt-like” run-up (4x from January 25 to January 26) and recent run-down (~-37% last week):

We will not from here focus specifically on silver, but rather what has unfolded over the first month+ of the year and how this impacts our forecast for 2026.

Volatility Returns

The first five weeks of 2026 have seen a return of volatility with stocks, bonds and especially commodities experiencing extreme price moves at several different times. Let’s look at a few of the reasons:

Did Trump just choose a hawk? Donald Trump has made no secret of his love and desire for lower interest rates. In fact, every time the Fed does not cut rates on his watch, he tends to get, umm, angry, usually tweeting something about how his Fed Chair (who Trump appointed to the job, by the way) is the worst and the dumbest in history and a whole lot of other things not appropriate for a family publication. Anyway, Jerome Powell, who is the current “worst and dumbest” will see his term expire in May and Trump, with much fanfare, chose Kevin Warsh to replace Powell. Except Warsh has generally been an inflation hawk and his general view has been that rates were too low, not too high over the past two decades. Is it possible that Warsh will not be the dove that Trump hoped for? His record would say “maybe”; although, considering how so many former free traders, and free speech’ers, and deficit hawks have, umm, loosened their principles in the Trump era, we think these worries may be overblown.

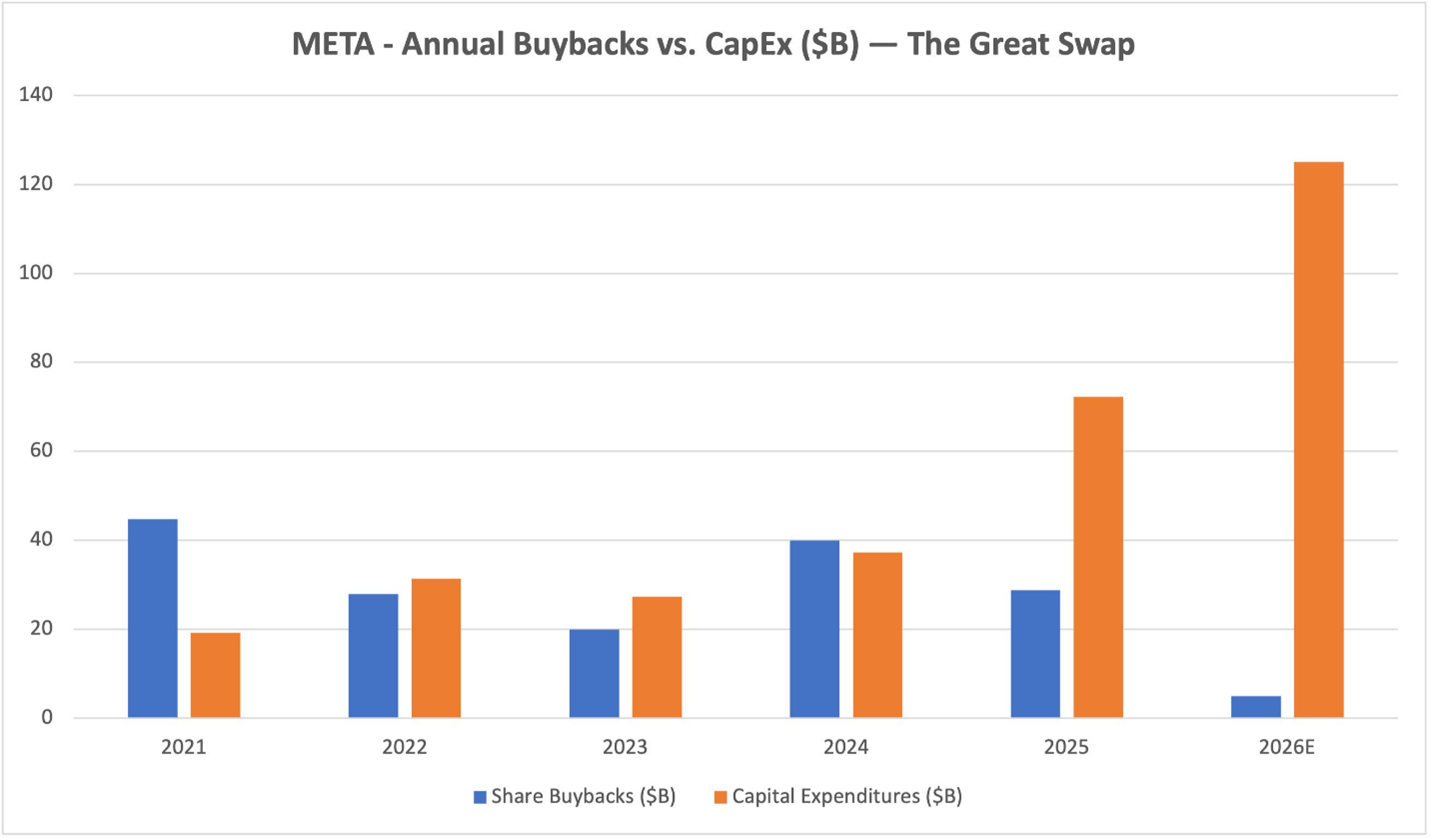

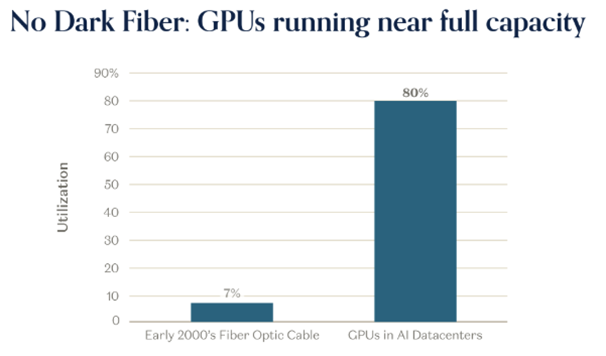

The Mag 7 wobble: A large part of the market run-up over the past decade has been the so called Mag 7 and their contribution to returns. These businesses were generally categorized as “asset light”, meaning that they generated a lot of free cash flow and since their capex needs were fairly low (as most of their businesses were digital and virtual), they used this cash flow not only to grow, but also to buy back their own shares. With the AI boom that began in late 2022, this “asset light” dynamic has shifted with capital expenditures skyrocketing as everyone tries to build out the infrastructure necessary to support this new technology. Let’s look at a chart and then comment:

Above is a chart of Meta and the amount it has invested in share buybacks vs. capex over the past 6-years. As you can see, buybacks generally have exceeded or at least come close to capex, but this shifted in 2025, while in 2026, Meta has virtually no planned buybacks as it spends more than $120 billion on capex, which is more than Meta spent on capex from 2021 to 2024 combined. Over the past month, investors have punished the likes of Meta, Amazon, Alphabet, Microsoft and others not for bad results (the results have generally greatly exceeded expectations), but rather for capex spending plans that went well beyond forecasts. Our view is that the market may take a little while to digest this ramp up in spending, but that it will ultimately move past it. We continue to like several members of the Mag 7 (although, not Meta) and with valuations now close to the lows of 2022, we may even look to allocate new money at some point in the near future should weakness persist.

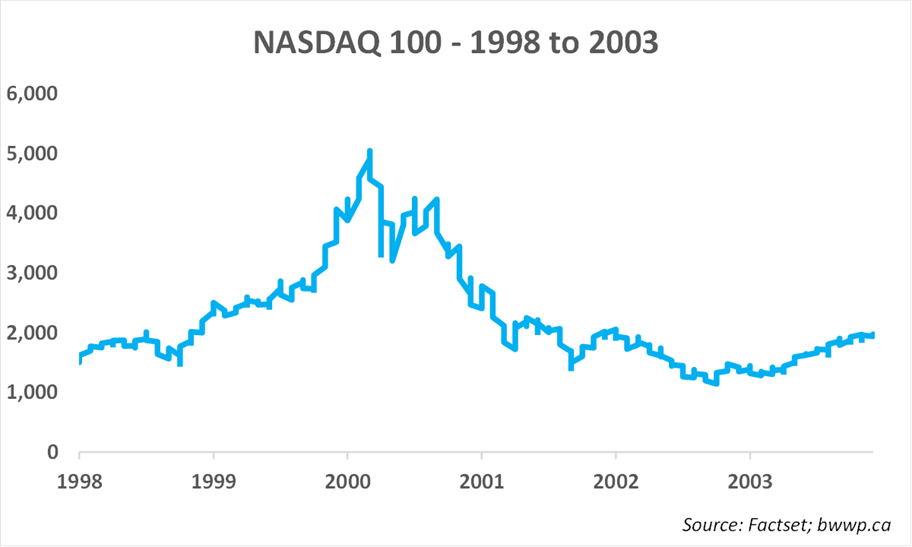

The bubble is bursting: While there are a number of different themes on this, the basic argument is – the Mag 7 and a bunch of other stocks linked to AI have run up a lot and it is thus a bubble that is now bursting. The historic corollary that this frequently sited is the technology bubble of the late 1990s and the subsequent crash of the early 2000s:

Our pushback on this would be twofold: 1) valuations today do not come close to approaching what we saw in the late 1990’s when many of the Internet and telecom companies had no earnings; and 2) much of the investment that took place during the tech boom was for a future that did not develop, while much of the investment in AI is a response to current demand, as opposed to future needs:

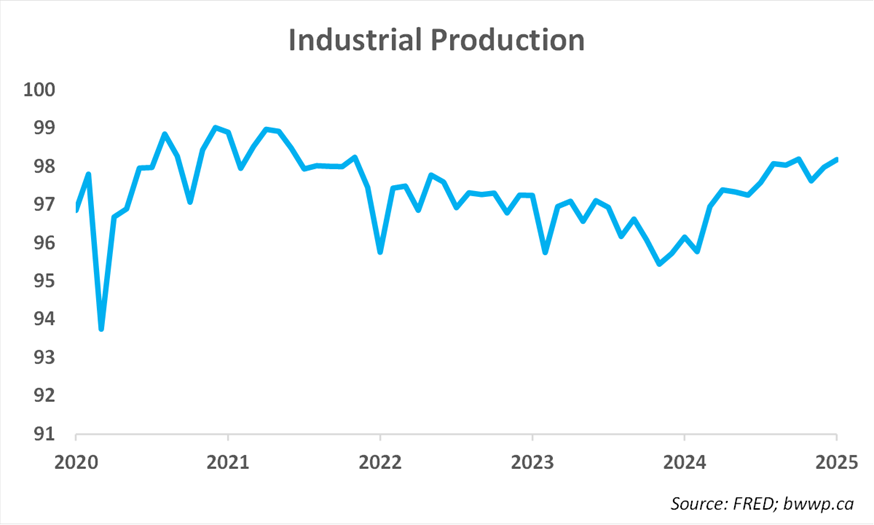

The K-shaped economy remains in place: The aforementioned capex boom is starting to show up in the economic data with industrial production pushing higher through much of the past two-years on the back of Biden’s Inflation Reduction Act:

Now, normally, when you see an industrial boom such as this, you would expect the rising tide to lift most boats. However, as we and others have noted over the past year, while this boom has helped to push pockets of the economy and the stock market higher, the lower ends of the income/asset spectrum remain extremely negative on the state of things:

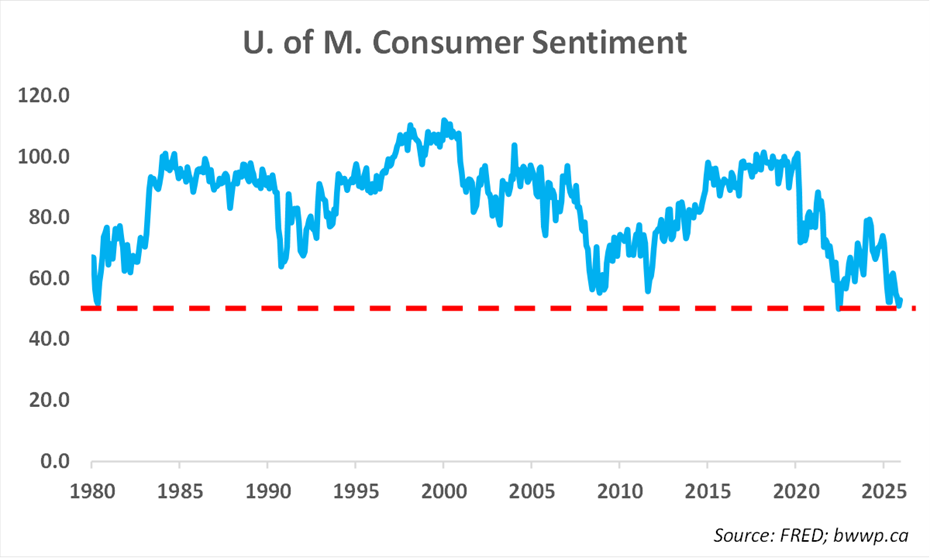

Consumer sentiment remains near all-time lows despite an underlying economy that is doing pretty well. The main driver of this (as we have noted before) is that while Wall Street focuses on the level of inflation and how fast prices are rising, Main Street focuses on the level of prices, which remain elevated following four years of high inflation.

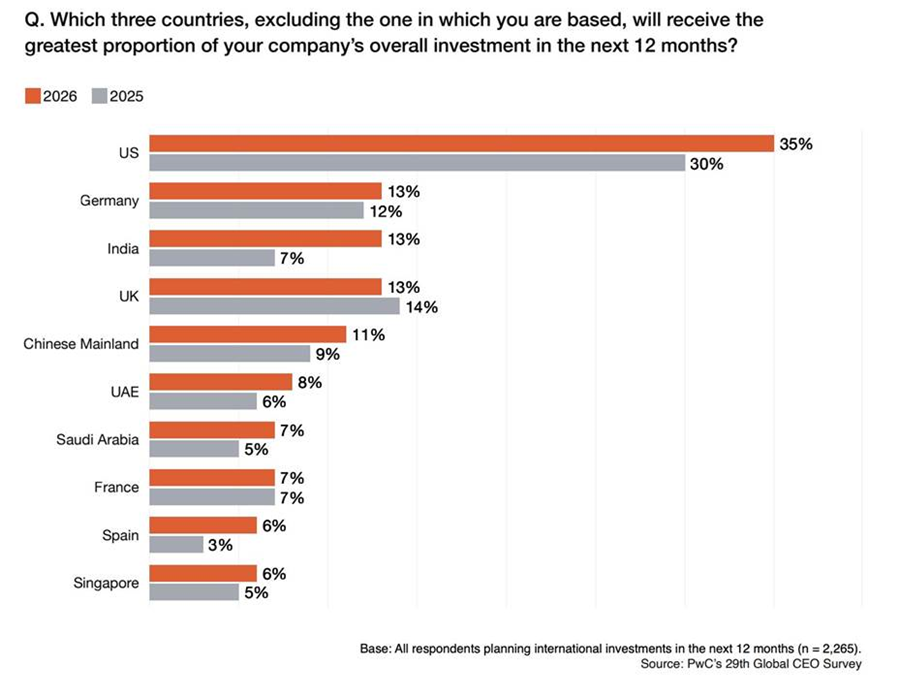

That said – overall, we think the U.S. economy as well as most of the global economy remains in the midst of a cyclical recovery driven by significant monetary and fiscal stimulus. In addition, the stop/start nature of the 2025 economy, borne mainly by tariff uncertainty, undoubtedly delayed significant investment that is likely to show up in the 2026 data. Further, the U.S. consumer is likely to see a significant cash flow boost in March/April/May as tax refunds are expected to be higher than recent years as a result of the One Big Beautiful Bill. And while one might assume that the U.S. would see a negative foreign investment impact from all that it wrought in 2025, surveys suggest otherwise:

Final Thoughts: We continue to have a cautiously optimistic view toward 2026, despite the volatile start to the year. Growth continues to be strong and corporate profits are likely to grow more than 10%. We remain concerned about inflation given all the stimulus in the system, but we continue to think the risks are several quarters out and we will watch key indicators for signs of a more significant flare up. We would also add that the mythical “Patriots Indicator” named after the most hated team in all of professional sports, especially by former New Yorkers and long suffering Jet fans (imagine the Leafs, but 10x worse) flashed a buy signal this past weekend as the median return on the S&P 500 in years in which the Patriots have lost the Super Bowl is ~13%, while the median year in which they win the Super Bowl has been only ~6%.