Barasch - Wellwood Wealth Partners

May 4, 2026

In poker parlance, there is something called a bully. The bully has the largest stack of chips and essentially uses this stack to “bully” other players into folding otherwise playable hands. The fold usually occurs because the lesser stacked (fewer chips) player does not want to risk getting knocked out of the game entirely (i.e. run out of chips) and the bully does not have the same concern as he/she has ample chips to survive the fight.

There is also something known as a maniac. A maniac is a player that, regardless of his or her hand, plays far more hands than he or she should and often bets with little consistency (i.e. sometimes big bets on poor hands and small bets on good hands). Maniacs can prove especially troubling for good poker players as good players generally rely on other players playing a certain way, which allows the good poker players’ skills to shine through.

But what happens when a bully meets a maniac? While we suppose this could go in several different ways, we would say generally that it is bad for the bully. The bully relies on his or her stack and the threat of large bets leading to sub-optimal folds by the other players at the table. But this is unlikely to phase the maniac, who does not follow the predictable rules of most poker players. The bully may still be able to outlast the maniac, but this more comes down to luck than the effectiveness of the bullying strategy (i.e. scaring your opponents into sub-optimal folds).

Donald Trump – the bully meets the maniac

If we look back across the 5+ years of Trump’s two presidencies, we think the poker bully analogy fits to a tee. President of the United States is the ultimate large stack – the biggest economy in the world by far coupled with the world’s reserve currency and the largest military. If the U.S. wants something, it is generally going to get it as the rest of the world is more apt to fold its hand, regardless of the cards it is holding. Trump has relied on this both domestically and internationally with some effect.

For example, take his 2021 cabinet appointments, many of whom were very controversial and would likely not have gotten through past Senate confirmations. Trump, however, played the bully, essentially threatening any Republican senator with a primary if they failed to confirm his nominees, which is how we ended up with a Fox News commentator as Secretary of War (even though we are not supposed to call things “war”), RFK Jr. as Secretary of HHS and a myriad of other less than fully qualified applicants.

But, if we look back at those 5+-years, we also see another disturbing trend – when Trump runs into a maniac, he has no plan B. The most infamous example of this in Trump’s first term was COVID (the maniac), which became less and less predictable as days and weeks passed in 2020. Trump tried to essentially bully it out of existence – “it’s going to disappear. One day it’s like a miracle, it will disappear.” – and as it became apparent that it would not “disappear”, his approach became more and more scattershot to the point that he essentially abandoned any strategy at all; that is – no plan B.

And while we would love to say that things have gone better in Trump’s second term, the opposite has been true. While he has tried to play the bully repeatedly, he keeps running into a veritable buzzsaw of maniacs.

- Tariffs: Trump tries to bully the rest of the world with tariffs, but the table has an unforeseen maniac– investors. For two weeks, the S&P 500 drops like a stone, while interest rates surge, threatening mortgage rates and the broader economy. Trump is forced to back down (birthing the TACO acronym) and what follows is a back-and-forth tariff policy with one wary bully-eye always glancing nervously at the maniac on the other side of the table.

- Redistricting: Trump bullies Texas into a mid-cycle redistricting designed to keep control of the House of Representatives in the 2026 midterm elections, relying on the likelihood that Democrats, who generally fold their hands, will not respond. But the Democrats, who for the most part have been predictable poker players, suddenly become the maniac with massive redistricting efforts in California and Virginia, having now essentially “won” the redistricting hand. We would note that other than a couple of angry tweets, Trump has essentially moved on from redistricting as the hand has been lost.

- And, of course, Iran: to put a bow on this analogy, let’s look at the game of poker that has unfolded (in Texas Hold Em, each player is dealt two hole cards that only they can see, then three community cards are turned together (the flop) with all players able to use those cards with their two hole cards, then another community card is flipped (the turn card) and finally a last community card is flipped (the river) with all players that are still in the game using their two hole cards and the five community cards to make their best five card poker hand. Betting occurs between each of the above steps).

- The U.S. and Israel drew king/queen off-suited (different suits) - hardly a surefire winner, but a good hand to bully with as there are lots of outs (ways to win) - high pair, a straight, even high card. Iran drew a 2/7 off-suited - a terrible hand with few outs - a pair - but the maniac doesn’t necessarily care.

- The flop is a king/queen/7 – giving the bully a pair of kings and queens and the maniac a pair of 7s - and that’s essentially the first few days of the war (sorry, “conflict”) - Iran’s defenses are wiped out and most of its leadership is dead or on the run. Emboldened by two pair, the bully pushes in more chips, but the maniac, despite having few outs (another 7, which would give him three-of-a-kind, or the more unlikely 2/2 on the turn and the river), not only sees the bet, but raises - Iran bombs the entire region and while most of its drones/missiles are shot down, enough get through to cause pain to the region. Now, the bully is confused and calls the raise - more bombs.

- The turn card is a 5 - no help to anyone, but a great card for the bully as there is now only one out left for the maniac (that pesky 7) - so the bully bets big. More bombs and now lots of rhetoric about annihilation (apparently legal both constitutionally and biblically, so shut up, Pope), but still the maniac presses on and not only sees the bet but also raises to all-in (pushing all of his/her chips in) - shutting down the Straits of Hormuz.

There is no river card - that is still yet to come. Either the U.S./Israel gets terms that are favorable (anything but a 7) or Iran does (the 7). The time it will take for the dealer to end the stare down is unknown (i.e. deal the river card). To be sure, both sides are coffeehousing (talking a lot to try to influence their opponent’s next move), but most of the hand has already been played and the bully does not have a lot of moves left.

From our lens, the out for the bully at this point is to hope for a deal similar to the JCPOA, which was the deal signed with Iran back in 2015, but was repudiated by Trump in his first term. We are skeptical it will be as favorable as the JCPOA for the simple reason that the maniac has learned that some of its tactics – shutting down the Straits – give it leverage in the game that it did not have before. As far as the impact on the economy, read on.

Mid-Year Health Check

While we are not quite at mid-year yet, we thought now would be a good time to gauge the early impact of the Iran war. Let’s start with the economy and then look at inflation and markets.

Economy

Let’s start with the U.S. and say simply – the U.S. economy is very difficult to derail. Despite on-again/off-again/on-again tariffs, near-stagnation in the size of the U.S. workforce, inflation that remains well above the levels of 2000 to 2020, and now the Iran war, the U.S. economy continues to fire on most cylinders. While Trump is not the only President we could say this about, the way we would put it is – the U.S. economy remains strong despite the actions of the President, not because of them. Let’s look at a chart and then comment:

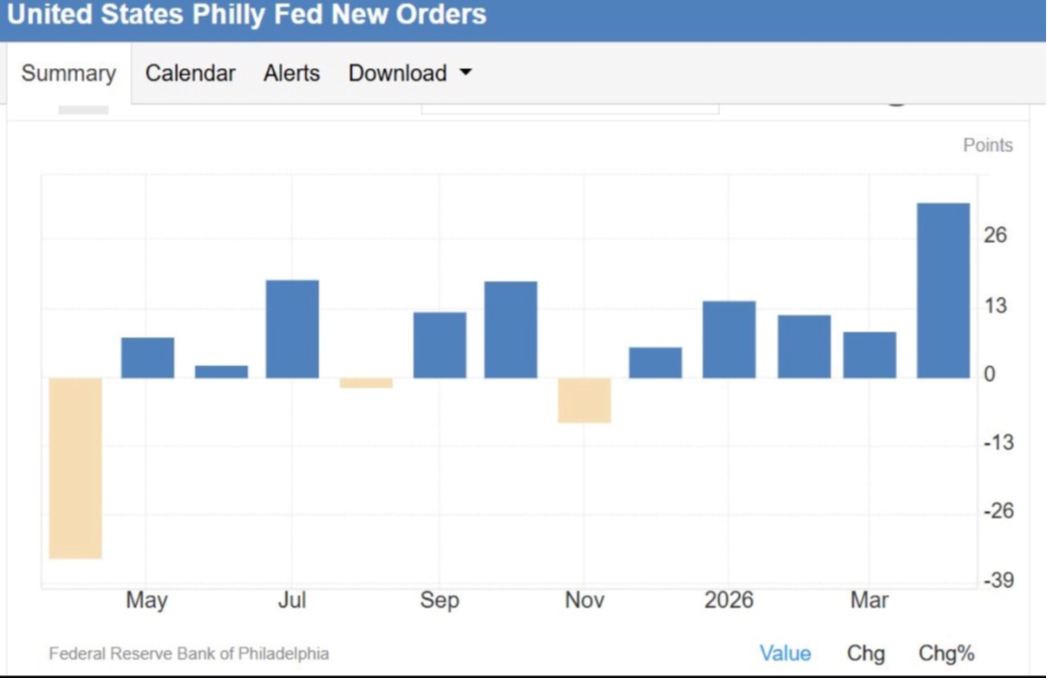

After a stop/start 2025, new orders from factories have been steadily positive with a sharp move up in April. The April move is not surprising as the virtual shutting down of the Straits of Hormuz has sent businesses scrambling for future inventory, but the bottom line is that this is not an economy at or near the brink of recession, at least from a corporate perspective. Let’s look at another chart and continue:

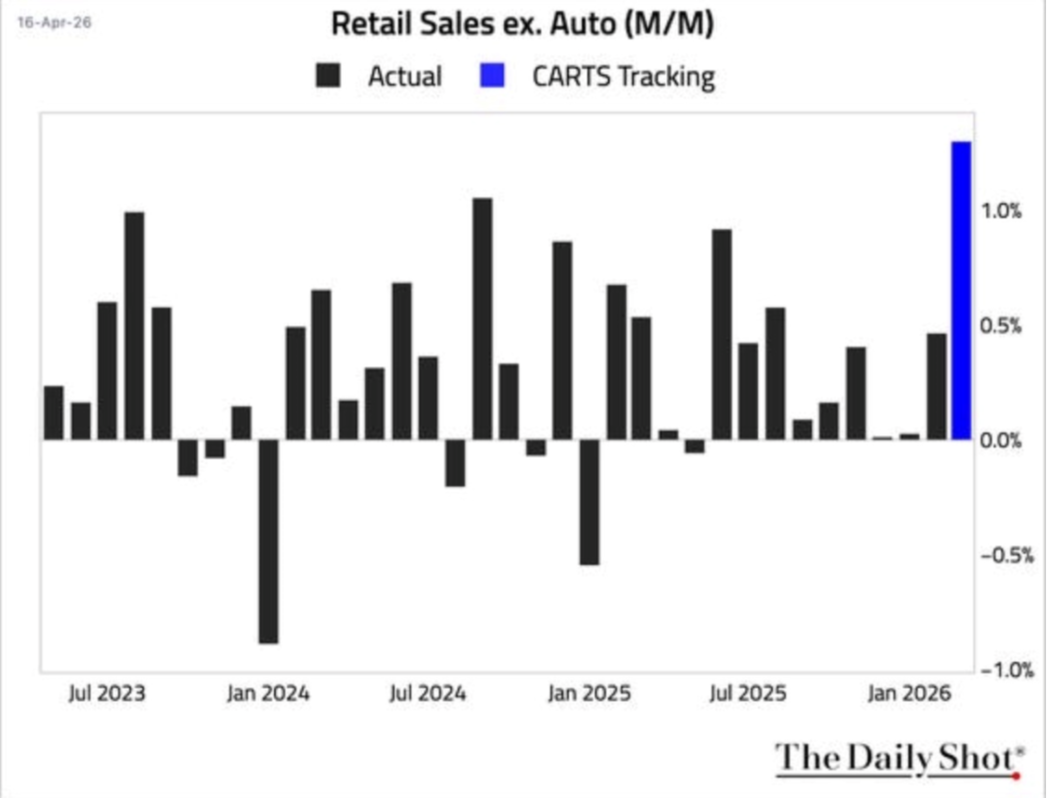

Here, we are looking at the consumer and there is some nuance. Despite a myriad of headwinds, the U.S. consumer continues to spend with April retail sales forecasted to show the biggest rise in more than three years. Of course, inflation will play a big role in this (hence the nuance) as the surge in oil prices and the clogged global shipping lanes are once again leading to higher prices, not only at the gas pump, but also across the retail spectrum. As we have noted before, the so called “K-shaped” U.S. economy, which sees the higher-end consumer responsible for most of the spending, remains alive and well. This generally bodes well from an investing perspective but may not be good news for the GOP when it comes to the November election as the majority of voters may not be enjoying the economic benefits of the current recovery.

Canada

Canada is one of the few countries that on net benefits from a sharp rise in oil prices largely because of its vast surpluses in oil and natural gas. Thus, the Canadian economy is likely to improve in the coming months as the lagged effects of higher oil prices begins to show up in the broader economic data. Let’s start with a chart that does not quite capture this impact, but does give a good sense as to where the Canadian economy is:

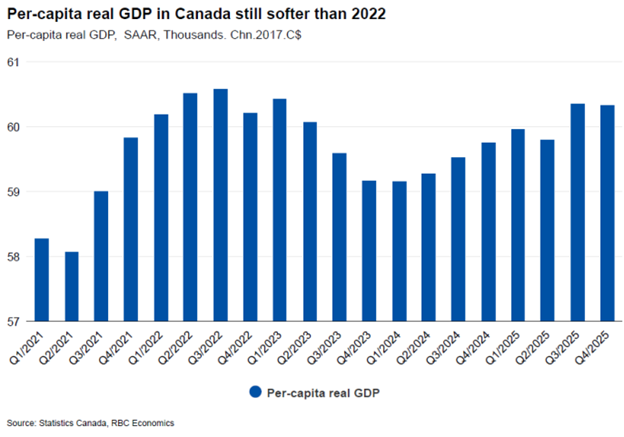

GDP per-capita has recovered following the trade-induced downturn of 2025. That said – as the chart title notes – per capita GDP (the amount of economic production per worker) has only now recovered to the levels of 2022, meaning that productivity, despite the election of Mark Carney, has continued to stagnate. Why? Let’s look at another chart and then comment:

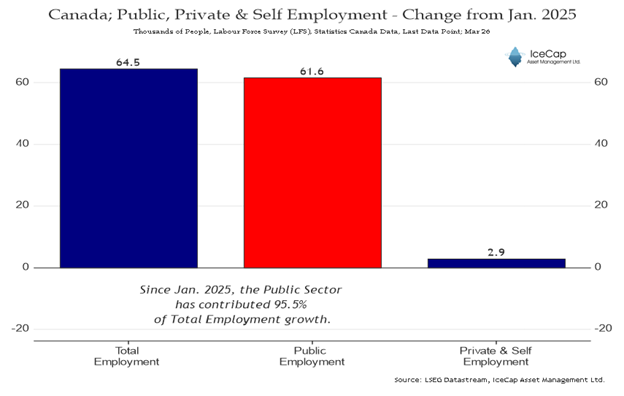

Virtually all of the jobs created in Canada over the past year (~95%) have been in the public sector. And while these jobs tend to be higher paying (~4.8% higher than the private sector), they also tend to come with more absences and earlier retirement (both negative for productivity). While we were hopeful as it related to the election of Carney and the potential for turning around a decade of stagnation in the Canadian economy, the results so far have not yet borne this out.

Inflation

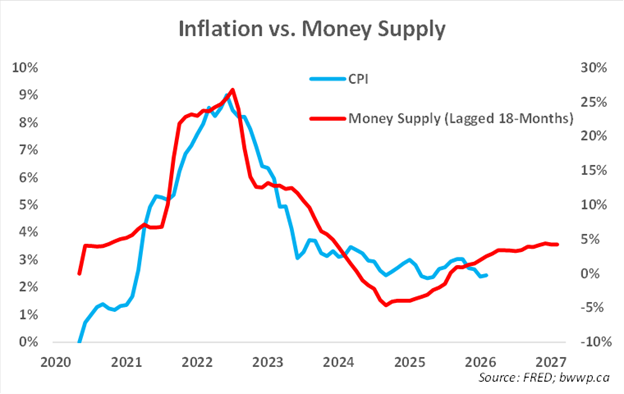

Let’s look at our favorite inflation predictor and then comment:

The U.S. Fed has an inflation target of 2%. Despite the fact that inflation has been above this target for more than 5-years, the Fed basically declared “mission accomplished” in 2025 and began reducing rates again. Against this backdrop, the money supply (M2) has continued to sharply inflect higher, which is an indication that lending is soaring (a relationship we might explore in a future missive). M2 growth is highly correlated to inflation, but generally with a lag of 12-18 months. Considering this latest move up began in the spring of last year, we expect to see higher inflation prints this summer. And this was before Iran war, errr, conflict.

Let’s look at another chart and then comment:

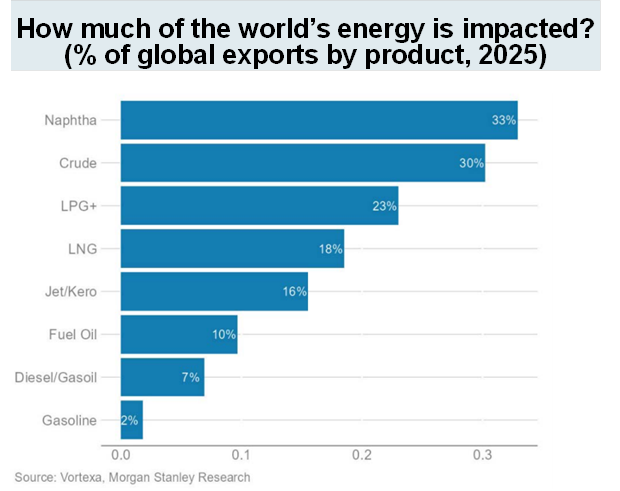

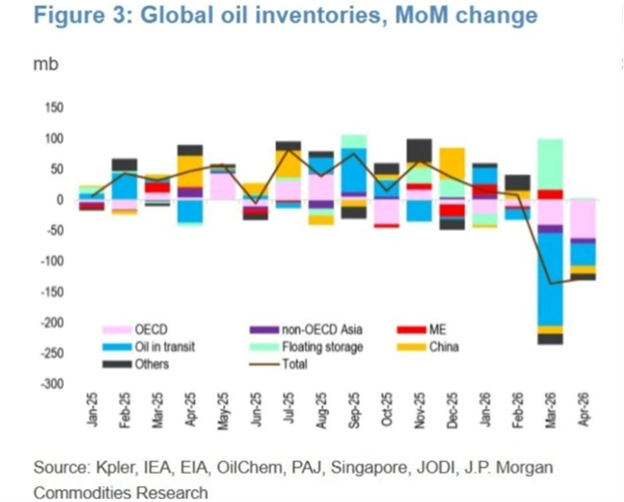

A massive amount of the world’s supplies of oil and its byproducts have essentially been taken off the market over the past two months. This has caused a sharp surge in prices, which, even assuming a rapid resolution to the conflict, is likely to get worse before it gets better. This simplest way to describe why is that it takes a long time for tankers to go back and forth to offload and reload new cargo and global reserves of oil are running low.

As we get into the heavier summer driving and travel season, this disconnect in supplies and demand is likely to push prices higher even if the conflict is rapidly resolved.

Markets

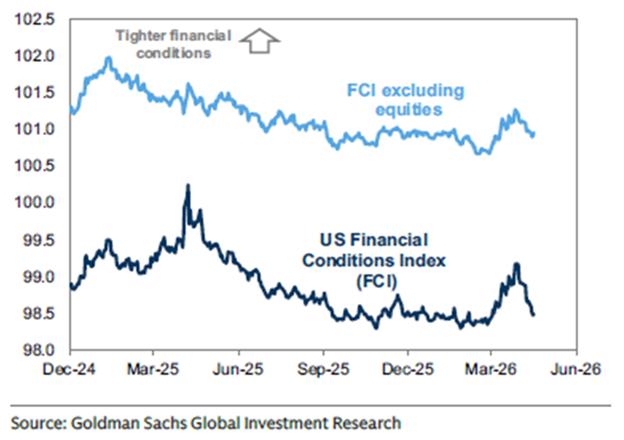

After a tense March, markets have largely shaken off the war and have recently challenged February highs. While we often like to point out that markets have a propensity to scale walls of worry, we will admit that the latest scaling has us a bit concerned as the impact of high oil prices is likely to reverberate for some time to come. Let’s look at another chart and then comment:

Financial conditions have loosened significantly over the past several weeks and are once again approaching the levels of July 2025 through just before the war began. The big drivers of this have been the lagged effects of 2025’s rate cuts and the One Big Beautiful Bill with April’s tax filing season seeing a massive surge in refunds vs. prior years. Looser financial conditions generally keep a bid in markets, which can be a bit of a self-fulfilling prophecy as strong markets will feed positively into financial conditions through the wealth effect (the more wealthy people feel, the more they tend to spend). Thus, while the rise in gasoline prices has put a strain on disposable income, this has, thus far, been more than offset by these other factors.

Bottom Line

While we realize at times such as these there is a propensity to be bearish when it comes to markets. But while we are cautious given the risks to inflation that we continue to see in the back half of 2026 into 2027, we still think a strong underlying economy, coupled with low double-digit earnings growth and loose financial conditions will provide a powerful tailwind over the coming months. While our strategy of owning good businesses with strong management teams and wide moats struggled a bit in 2025 against a backdrop of a market that rewarded lower quality businesses, we remain committed to this approach and have seen many of these stocks begin to recover in 2026. We expect more recovery into the back-half of the year and prefer these businesses over lower quality as they will tend to hold-in better should the market hit a rough patch.