Shannon Boakes

Investment & Wealth Advisor, Financial Planner

March 31, 2026

A conversation came up recently that has stayed with me.

She had done everything right. Saved consistently over the years, built up her RRSP and TFSA, carried very little debt. On paper, she was in a strong position. The kind of position most people work toward for decades.

But as we started talking about retirement, she paused for a moment and said something that shifted the entire conversation.

“I don’t actually know what this turns into.”

She wasn’t talking about her accounts or her investments. She meant her life. What it looks like when the income she has relied on for years is no longer coming from an employer, but from what she has built herself.

That question comes up more often than people expect. And for many women, it carries an added layer. Time spent supporting others, stepping back from work at different points, navigating changes in roles or responsibilities, and in some cases, finding themselves making these decisions on their own.

Which is why this stage of planning feels different. It is not just about whether you have enough. It is about understanding how everything you have built actually works together when the direction of money changes.

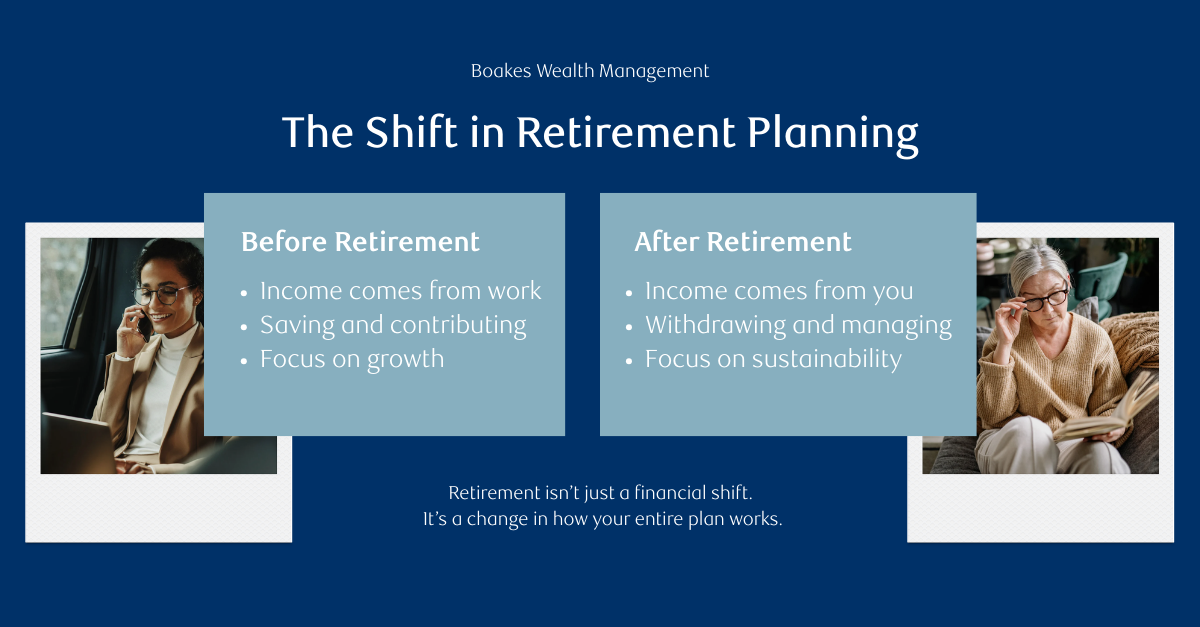

For most of our working lives, the focus is straightforward. You earn, you save, you contribute, and over time, you watch things grow. There is a rhythm to it that feels familiar.

Retirement shifts that rhythm entirely.

Now the question becomes how to turn those accounts into something that feels steady and reliable. Something that supports your lifestyle without creating a constant sense of uncertainty. And this is often the point where even very well prepared individuals start to feel less clear, not because anything is missing, but because this phase was never fully mapped out.

Over time, most people have built a mix of accounts. An RRSP from earlier in their career, a TFSA that has grown steadily, sometimes a non registered account, and occasionally a pension layered in. Each of these serves a purpose, but they do not behave the same way when it comes to income.

Withdrawals from an RRSP or RRIF are fully taxable. A TFSA is not. Non registered accounts carry their own tax treatment depending on what is held. So the question shifts from how much you have to how you actually use it, and that is where thoughtful planning starts to make a meaningful difference.

Government benefits are another important piece, but they are often misunderstood or oversimplified. CPP can be taken earlier or delayed, with permanent adjustments to the amount you receive. OAS begins at 65 and is tied to your income, which means it can be reduced if your income rises above certain thresholds.

The decision around when to start these benefits is not just about maximizing a number. It is about how they fit into the broader picture. Taking CPP earlier might provide immediate support, while delaying it increases long term income but requires other sources to carry you in the meantime. Both CPP and OAS are taxable, which means they interact with the rest of your income in ways that are not always obvious at first glance.

One of the most overlooked parts of this entire process is something we refer to as sequencing. It sounds technical, but in practice it simply means being intentional about where your income comes from and when.

It can be tempting to draw from one account until it runs out and then move to the next, but that approach can create unnecessary tax pressure or limit your flexibility later on. A more thoughtful approach often involves layering income, drawing smaller amounts from different sources, and allowing certain accounts to continue growing while others are used more strategically.

What I see most often is not a lack of preparation, but a lack of clarity. Women who have built strong financial foundations, but have never been shown how the pieces come together in this stage of life. They are not asking whether they did enough. They are asking how it all works now.

And that is a very different kind of question.

Because this phase is not about getting everything exactly right. It is about understanding your options and making decisions that feel steady and aligned with the life you want to live.

If you find yourself thinking about this, even in a general way, it can be helpful to sit with a few questions.

- Do I know where my income would come from if I stopped working tomorrow, and how long it would need to last?

- Have I thought about when I plan to start CPP and OAS, and how that decision fits into my overall plan?

- Do I understand which accounts I would draw from first, and what that means from a tax perspective over time?

- And perhaps most importantly, am I planning based on what I have accumulated, or how I actually want to live?

You do not need to have all of the answers right away. In many cases, the clarity starts simply by asking the questions and giving yourself space to explore them.

Most of the women I speak with are far more prepared than they think. They have built something meaningful over time, often while balancing far more than just their own financial goals. This next phase is not about starting over or doing more. It is about understanding what you already have and learning how to use it in a way that supports you, both financially and in how you want your life to feel.

And that is something worth taking the time to get right.

Shannon

Shannon Boakes

Investment & Wealth Advisor, Financial Planner

Boakes Wealth Management

Phone: 519-758-1270

This community extends beyond one conversation. It’s built through shared ideas, thoughtful planning, and staying connected over time.

Follow along on LinkedIn and Facebook, or reach out if you’d like to talk through your own situation or refer someone who could use support.