Robert Bryan

Senior Branch Manager & Senior Investment Advisor

March 11, 2026

Access the PDF version of our Spring Newsletter 2026 here.

"Nothing changes on New Year's Day." This famous line from a 1983 U2 song captures a truth often overlooked in financial markets — while the calendar may flip, the underlying macro and market trends rarely undergo dramatic shifts overnight. 2026 has begun much like 2025 ended: Global stock markets continued their upward trajectory, supported by expected strong earnings growth, anchored inflation expectations, and optimism around potential Central Bank policy easing.

Yet, as was the case last year, investors face a proverbial "wall of worry," none of which we believe is likely to derail the market advance. These include but aren't limited to: Persistent geopolitical tensions (China / Taiwan and Russia / Ukraine) and new flashpoints such as the developments in Venezuela and at the time of writing, the US bombing in Iran. Additionally, questions surrounding the independence of the Federal Reserve (Fed), the legality of the Trump administration's tariffs and the USMCA renegotiation.

"The history of markets is one of overreaction in both directions." – Peter Bernstein

History does not move in straight lines. Markets ricochet between excess and restraint in violent cycles. That said, we are also wary of the broader lack of concern for stretched valuations, extreme market concentrations, leverage in retail investor accounts, tight credit spreads and potential shocks from "unknowns". Having seen nearly 35 years of market cycles, history has shown time and again that financial accidents come unexpectedly in different forms and from places few expect. With increased signs of excessive risk-seeking behaviors, we believe a high degree of prudence and patience is required in today's markets.

Managing risk is as important as a good return each year. We aim to "win by not losing" as mathematically, portfolios experiencing significant losses face an increasingly difficult task to reach break-even. We have purposely been staying defensive with higher cash / fixed income balances to capitalize on future market pullbacks. This does not mean we have stopped investing, but rather at the margin, we are becoming more selective and seeking investments with low correlations.

2026 marks the end of pandemic-era stimulus and the start of a new cycle driven by credit markets, technology infrastructure, and mandatory and fiscal policy frameworks. Global liquidity is increasing, deregulation continues, inflation stabilizing and equity market participation broadening. Historically, market breadth has been a useful guidepost as a precursor for larger market draw-downs, to date, the increasing number of stocks participating in this bull market is a positive development.

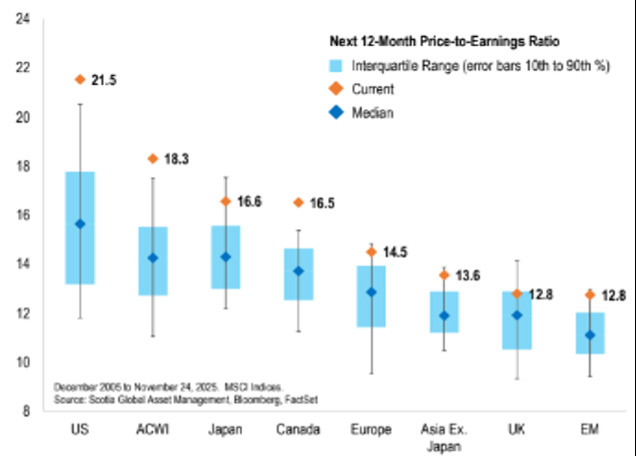

Bull markets do not end on valuations alone, however current set up for US stocks give us pause with high P/E valuations, market concentration, leverage and bullish sentiment (i.e. CAPE near historical highs). For half a century, Wall Street has preached a simple gospel: bull markets end when stocks become "too expensive," and every four years a mid-cycle correction cleanses excess.

Regional Equity Valuations

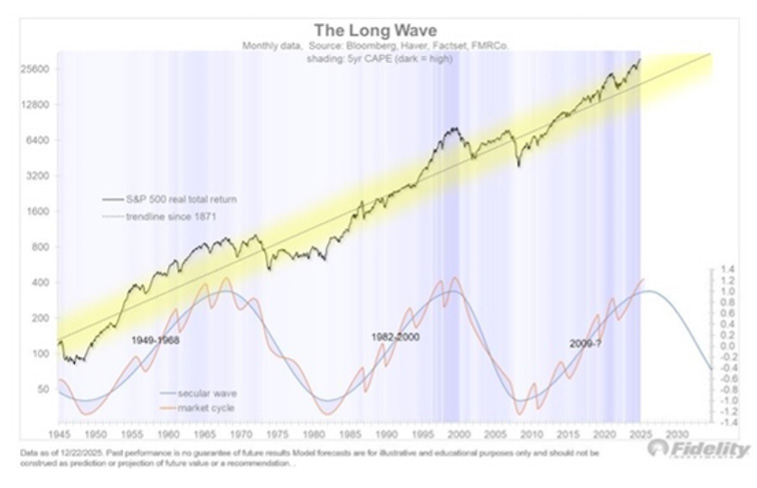

The Long Wave theory suggests we are in the late innings of this secular bull market, a generational cycle lasting on average 16 years. This is an important distinction: during secular bull markets, we experience shorter cycles—averaging 3 years up and 1 year down—versus secular bear markets (1969-1981 and 2001-2014), which average 2 years up and 2 years down. Of course, volatility exists in both environments, but in a secular bear market, it simply feels like taking two steps forward and then two steps backward repeatedly.

None of this is risk-free: geopolitical shocks, energy price spikes, conflicts, cyberattacks, premature policy clampdowns, midterm US elections, uneven AI adoption / bubble, unwind of the Yen carry trade, or a surging USD dollar destabilizing emerging markets could all trigger brutal repricing. These are risks to manage—not excuses to sit out.

Despite tight credit spreads, corporate bond yields are still higher today than they were at any period between 2009 and 2022. Higher bond yields have increased the appeal of maintaining traditional fixed income in balanced portfolios as well as providing some ballast during volatility.

"Bonds are a global market" is a phrase we often hear, and the brief bout of volatility experienced last fall served as a good reminder of that fact. A snap Japanese election call and a disappointing 20-year auction sent Japanese bond markets tumbling. As long JGB yields surged, the impact rippled across bond markets throughout the world.

The Long Wave theory suggests we are in the late innings of this secular bull market, a generational cycle lasting on average 16 years. This is an important distinction: during secular bull markets, we experience shorter cycles—averaging 3 years up and 1 year down—versus secular bear markets (1969-1981 and 2001-2014), which average 2 years up and 2 years down. Of course, volatility exists in both environments, but in a secular bear market, it simply feels like taking two steps forward and then two steps backward repeatedly.

In this century and the last, the market effects of geopolitical crises have generally been short-lived. Persistent geopolitical tensions can affect the real economy however, if consumer sentiment declines, equity markets can experience temporary draw-downs.

Conclusion

The path forward may not be linear, but the ingredients for continued upside are in place. With individual stock participation broadening, corporate profits forecasts up double digits, and (fiscal & monetary) policy becoming more accommodative, we remain constructive on the macro and market structure outlook for first half of 2026. In all, I will sum it up as a world that will continue to see periods of significant volatility perpetuated by geopolitical hotspots, however a global economy that should continue to grow. Demographics and debt should keep a lid on inflation. Remember that 2% inflation isn't the holy grail for Central Bankers, it's "price stability".

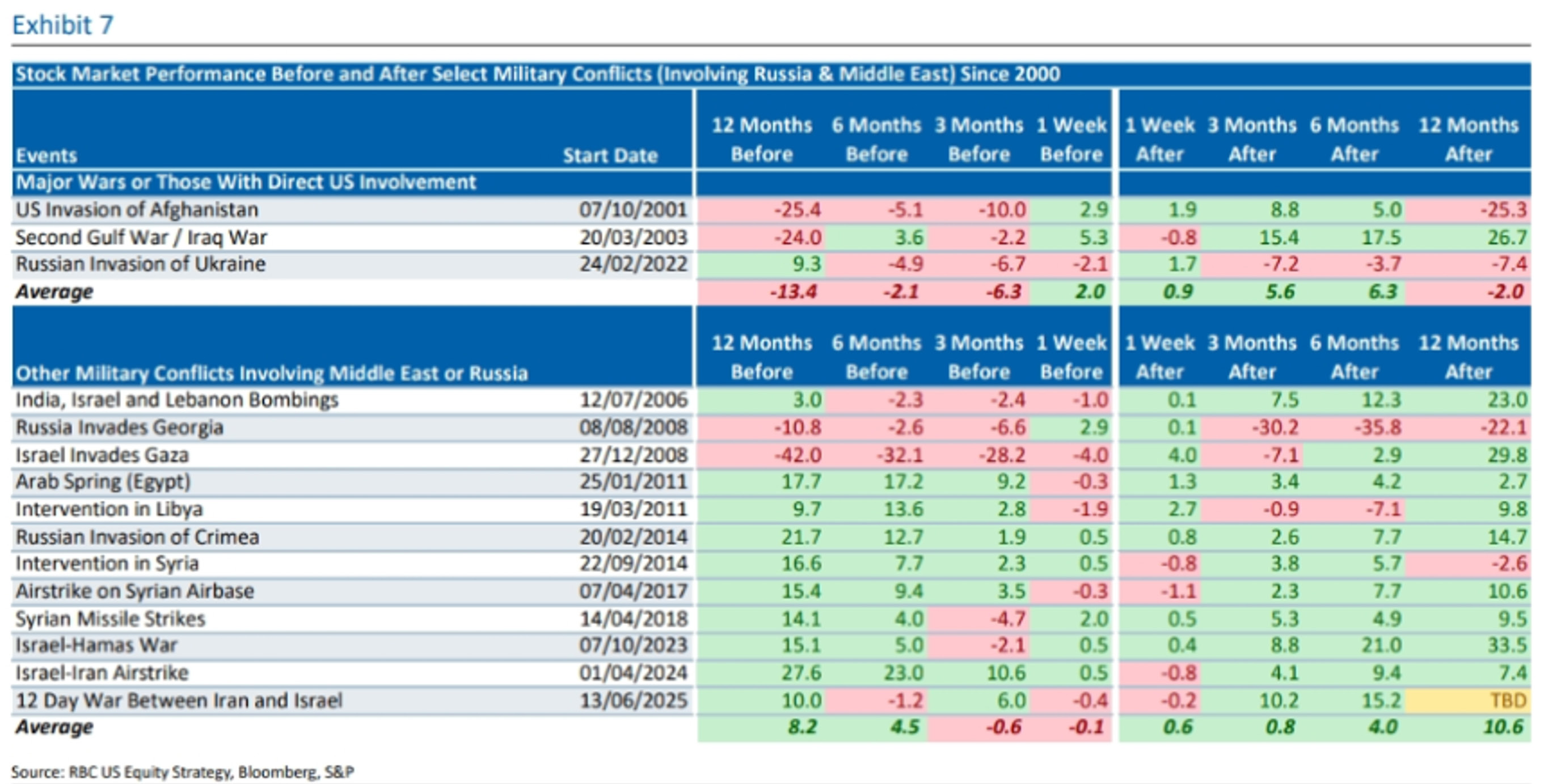

Global conflicts

In the table below, RBC U.S. equity strategy summarized market moves around select conflicts involving Russia and the Middle East. The key takeaway is that equity performance following major wars has not been consistent (and the sample size is limited). At the same time, the examination of other military conflicts suggests that their market impact tends to be limited in magnitude and time.

RBC Celebration of Impact

• RBCers donated a record-breaking $33.6 million to over 13,400 charities worldwide;

• RBCers tracked over 368,000 volunteer hours – a nine per cent year-over-year increase; and

• More than 24,000 RBCers volunteered in their communities – a new record!

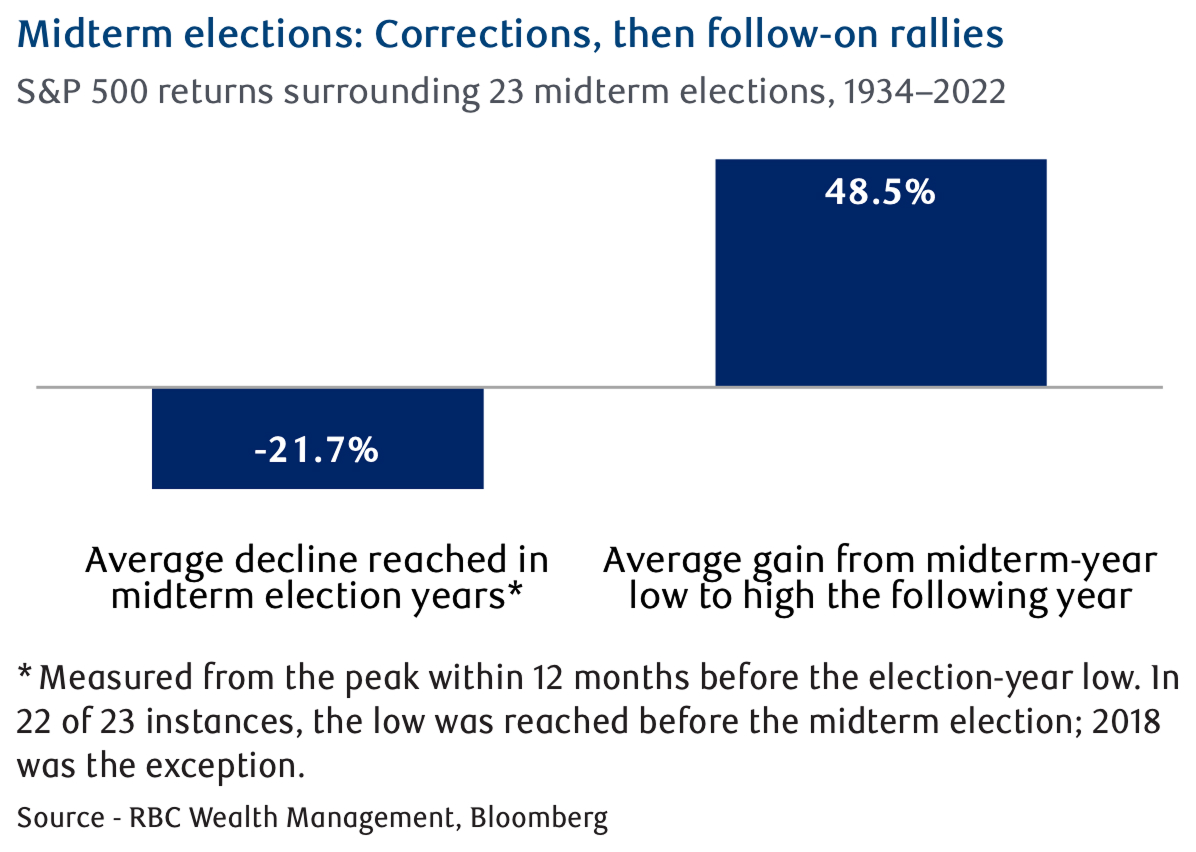

Midterm election-year dynamics

U.S. midterm election years have often experienced a noteworthy market pullback (see chart). The timing of when those corrections have started and finished has been all over the map. Furthermore, the market rebound off the eventual lows has typically been quite energetic and has frequently taken indexes to new all-time highs. The historical probabilities favour both a pullback and a subsequent bullish up-leg to new highs in 2026. However, markets and the economy are unaware of how they are "supposed" to behave according to past experiences. They can and do toss unexpected curveballs from time to time. In fact, 23 of the last 24 mid-term election years experienced a stock market sell off!

Riding with the tide

In today's digital world, investors are constantly bombarded with news, and it's easy to get caught up in negative headlines. This phenomenon, known as "negativity bias", can significantly impact investment decisions. However, successful investors learn to see beyond temporary storms.

Our brains are wired to prioritize negative information, perhaps a survival instinct gained from our ancestral days of dodging predators. In today's 24/7 news cycle, negative information dominates. The old journalism adage 'If it bleeds, it leads' has been amplified by social media and instant notifications. Negativity bias can lead to making irrational decisions.

Stratford & District Business Excellence Awards

RBC was a proud sponsor and presenting partner of the "Business Leader of the Year Award" at the 2025 Stratford & District Business Excellence Awards. Congratulations to all of RBC's business clients that were nominated and a big congrats to all the winners that work so hard to help make our community prosper and build for a better future.

DS Equity conference

Last month I had the privilege of attending RBC DS Equity Conference where leading analysts, strategists, economists, political strategists, and portfolio managers from across RBC and other world-class global financial institutions came to provide insight and thought-provoking discussion. Included in this field of market movers were Risk Reider, (Blackrock CIO… and #2 choice for the Federal Reserve Chairman), Howard Marks (Chairman Oaktree), Frances Donald (RBC Chief Economist), Mark Gerken (BCA Political Strategist), and Paul Warkman (Managing Director KKR).

While there's too much to share here, keep an eye out for highlights in my monthly emails as well as invitations to hear from guest speakers. Senior Vice President and Chief Economist, Frances Donald, joined us last month to discuss the economic outlook for 2026 and addressed topics that are top of mind for our clients in our rapidly-evolving landscape.

Paper or Digital - You decide!

This newsletter has been our way of staying connected throughout the year, sharing insights from the investment realm, as well as what is going on in our own backyard. As the world is vastly changing, we realize that preferences do too. To make sure you're receiving it in the way that suits you best, whether that's paper or electronic, we're happy to offer both options. If you'd like to keep things as they are, no action is needed. If you'd prefer to make a change, simply reach out to Brittany at Brittany.Leppington@rbc.com and we'll take care of the rest.

About the Bryan Wealth Management Group

Robert Bryan, B.Comm, FMA, CIM, FCSI Branch Manager, Senior Portfolio Manager & Investment Advisor robert.bryan@rbc.com

Dean McKelvie, PFP Associate Advisor dean.mckelvie@rbc.com

Brittany Leppington Associate brittany.leppington@rbc.com

RBC Dominion Securities 187 Ontario St. Stratford, ON N5A 3H3 Phone: 519-271-4611 Toll-free: 1-800-265-4596 robertbryan.ca

Extended wealth management team

Steve Wiffen, CLU, CFP, CH.F.C Estate Planning Specialist RBC Wealth Management Financial Services

Shannon Row-Ewing, BA, LL.B Will & Estate Consultant RBC Wealth Management Services

Scott VanEngen Financial Planning Specialist RBC Wealth Management Services

Chelan Mansour Senior Trust Advisor RBC Royal Trust

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc. and Royal Bank of Canada are separate corporate entities which are affiliated. Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © 2026 RBC Dominion Securities Inc. All rights reserved.