Jamie Burak

Jamie Burak

July 1, 2026

Friends & Partners,

We are officially past the halfway point of 2026, and RBC Capital Markets used the occasion to publish its Mid Year Outlook Update, a comprehensive refresh of the models that guide our thinking about where markets are headed. The headline, RBC has lifted its 12 month S&P 500 price target to 8,150, up from 7,900, implying roughly 11% further upside from where the index closed in late June. That is not a heroic call. It reflects subdued investor sentiment that still has room to climb a wall of worry, earnings tailwinds that are offsetting pressure from a trickier interest rate environment, a solid GDP backdrop, and a monetary policy picture that remains constructive even as the market now prices in the possibility of a Fed hike rather than a cut.

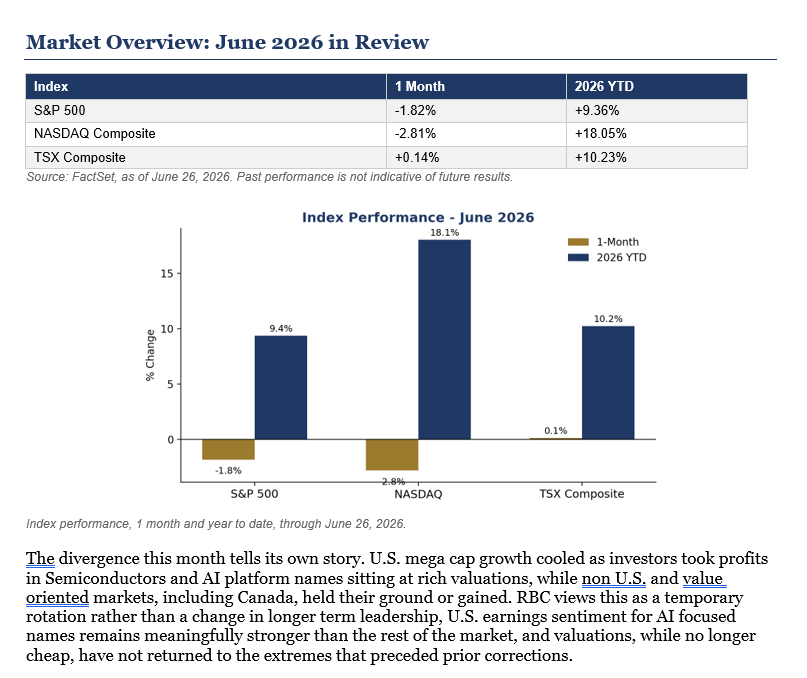

June itself was a rockier month than May, and the numbers below the surface make that clear. The S&P 500 slipped 1.8% and the NASDAQ fell 2.8% over the month as profit taking hit richly valued Semiconductor and AI platform names. Nvidia's year to date gain, for example, has come in from the high teens in May to under 6% today, and Microsoft has moved from a modest single digit decline to down more than 20% year to date. Canada, by contrast, held up notably better, with the TSX essentially flat on the month, up 0.1%, and still up over 10% for the year. We used the wobble in U.S. growth names as an opportunity to make an adjustment to the portfolio, which we detail below.

Mid Year Outlook: What RBC's Models Are Telling Us

RBC's price target is built from five models spanning investor sentiment, valuation and earnings, stocks versus bonds, the GDP backdrop, and monetary policy. Four of the five, sentiment, the earnings yield gap, GDP, and the Fed model, are essentially unchanged from May, and all point to further gains over the next twelve months. The valuation and earnings model improved because the bottom up consensus for 2027 corporate earnings has moved higher since the last update, even after RBC's own 5% haircut for conservatism.

RBC is candid that the path will not be linear. The list of tactical risks they are watching mirrors what we have been telling you all year, further profit taking in richly valued Semiconductor and AI names, the possibility of renewed war related setbacks, the U.S. midterm elections this fall, historically a rocky stretch for equities, and the chance that bond yields push through 5% if the Fed ends up hiking rather than cutting. RBC's own framework suggests any pullback from here is likely to stay in the 5 to 10% garden variety range, absent a recession or a genuine rate shock, not the 15 to 20% plus drawdowns that define a true growth scare.

On the ground, corporate America continues to look healthier than the headlines suggest. RBC's read of the Duke CFO survey shows executives are more optimistic about their own company's prospects than about the economy broadly, a gap that has persisted since COVID and speaks to management teams that have learned to manage through noise. Inflation and non labor costs, not tariffs, are now the top concern in the C suite, and importantly, two thirds of firms say they are absorbing higher input costs rather than passing them fully through to customers, a sign of pricing discipline, not desperation.

Index performance, 1 month and year to date, through June 26, 2026.

The divergence this month tells its own story. U.S. mega cap growth cooled as investors took profits in Semiconductors and AI platform names sitting at rich valuations, while non U.S. and value oriented markets, including Canada, held their ground or gained. RBC views this as a temporary rotation rather than a change in longer term leadership, U.S. earnings sentiment for AI focused names remains meaningfully stronger than the rest of the market, and valuations, while no longer cheap, have not returned to the extremes that preceded prior corrections.

Portfolio Focus: Making Room for Two New Names

We made one deliberate adjustment to the U.S. portfolio in June. We sold Cameco (CCJ, the U.S. side of the position) and BWX Technologies (BWXT) to make room for two new additions, Applied Optoelectronics (AAOI) and Tempus AI (TEM).

Sold Cameco (U.S. side, CCJ) and BWX Technologies (BWXT). Both names have been solid, quiet performers on the nuclear and defense theme, and Cameco remains a core holding on the Canadian side of the book. We used the proceeds to sharpen our AI infrastructure exposure rather than change the portfolio's overall risk profile.

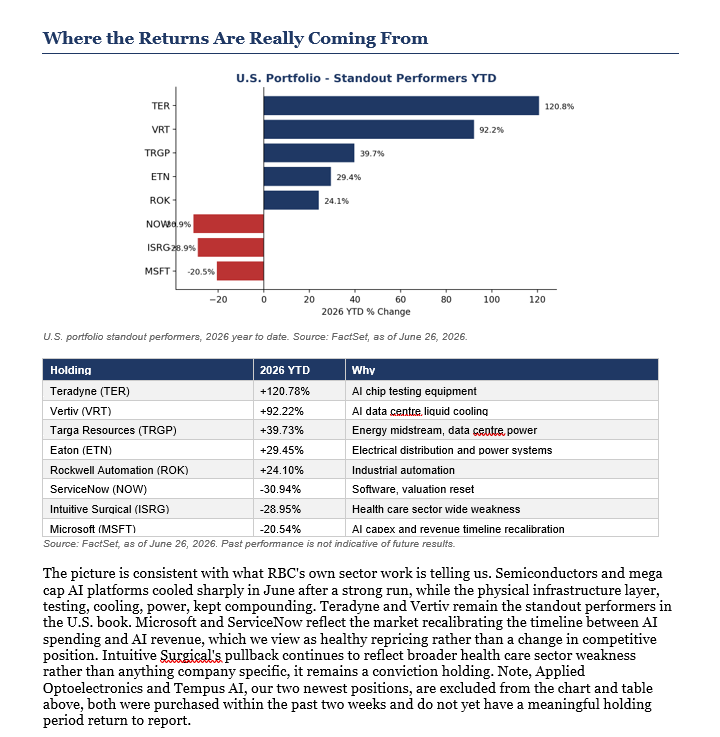

Added Applied Optoelectronics (AAOI) and Tempus AI (TEM). Applied Optoelectronics makes the optical components that move data between and within AI data centres, a picks and shovels name in the truest sense, benefiting from the same hyperscaler capex cycle as Vertiv and Teradyne. Tempus AI gives us direct exposure to the application of AI in health care, specifically precision medicine and diagnostics. Both positions were established in the past two weeks, so we do not yet have a meaningful performance track record to report. You will see them included in our standout tables starting next month.

As always, the core holdings, the AI infrastructure names, the AI platforms, the Canadian bank and energy anchor, and the defense positions, remain unchanged and continue to do the heavy lifting.

The Broader Picture

AI Infrastructure vs. AI Platforms. This remains the central organizing idea in the portfolio, and June was the clearest illustration yet of why we own both sides. RBC's sector work shows Semiconductors sitting at post tech bubble high valuations, rich, but a level the group has sustained before, and June's pullback in Nvidia and the broader AI platform trade reflects exactly that kind of profit taking. We would be more interested in adding to Semis on a further pullback. In the meantime, the infrastructure layer, Vertiv, Teradyne, Eaton, and now AAOI, continues to do the heavy lifting.

Power and Energy. Constellation Energy and Vistra have had a difficult year on rate sensitivity and utility repricing, but the underlying driver, AI data centres needing round the clock baseload power the current grid cannot fully supply, has not changed. On the Canadian side, Canadian Natural Resources, Pembina, TC Energy, and Enbridge continue to generate strong free cash flow, and RBC's sector work rates Energy attractively on both valuation and earnings revisions.

Defense. Lockheed Martin remains a core position. The thesis, sustained U.S. defense spending, was in place before this year's geopolitical events and remains in place today.

July Planning Focus: Estate Planning, Wills, and Powers of Attorney

July and August tend to be quieter months on the tax and portfolio review calendar, which makes this the right window each year to revisit something easy to put off, your estate plan. If it has been more than two or three years since you last reviewed your will, your powers of attorney for property and personal care, or your named beneficiaries on registered accounts and insurance policies, we would encourage you to use part of the summer to do so, particularly if your family situation has changed.

This is not something we do in place of your lawyer, but we are happy to be part of the conversation. We regularly coordinate with clients' estate lawyers and accountants to make sure the plan on paper matches how the portfolio is actually structured and titled. Simply reply to this newsletter or call the office and we will help get the right people in the room.

Closing Thoughts

The first half of 2026 asked a lot of investors, a Middle East war, an AI spending debate that has not fully resolved, and a Federal Reserve whose next move is genuinely uncertain for the first time in years. June's rotation, out of richly valued U.S. growth and into value, non U.S. markets, and Canada, is a reminder of why this portfolio is built the way it is. When one part of the book cools off, another has consistently stepped up.

Our job through the second half of the year is the same as it has always been, stay invested in durable businesses, make sizing and positioning decisions deliberately rather than reactively, and keep the conversation focused on what markets mean for your family and your plan, not on the headlines of any given week.

As always, if any of this raises questions about your specific accounts or your broader plan, please do not hesitate to reach out.

That conversation is always welcome, and it is always about you first.