2025 - Second Quarter - The Vanishing

Ever feel you missed out on something? It could be the overtime goal in the hockey finals, attending the Taylor Swift Eras tour or the last free chocolate donut in the lunchroom. In this newsletter we discuss some of the opportunities that investors may soon miss out on and how I almost missed out on a once in a lifetime opportunity with my dad.

Ever feel you missed out on something? It could be the overtime goal in the hockey finals, attending the Taylor Swift Eras tour or the last free chocolate donut in the lunchroom. In this newsletter we discuss some of the opportunities that investors may soon miss out on and how I almost missed out on a once in a lifetime opportunity with my dad.

Joshua Brown

June 29, 2025

In 1983 a band few people had heard of was playing in the small and intimate Queen Elizabeth Theatre in Vancouver and my dad, in the sixth row was there along with 3,000 other people. That band was called U2.

Now 35 years later as one of the world’s best-selling artists, U2 was back in Vancouver for opening night of their new tour to play the original ‘Joshua Tree’ album in front of a sold-out crowd of 50,000 fans at BC Place. It was the hottest ticket in town with fans coming from all over the world but with an enormous donation to StubHub, my dad and I had scored floor tickets. I had seen U2 several times before but this was the first time with my dad so my anticipation level was higher than awaiting Trump’s next tariff announcement. Four decades ago, my dad would have never imagined U2 would become one of the biggest bands in the world and that he would be seeing them again with his son, especially since I didn’t exist at that time. It was a beautiful day, and I was grateful to share this special experience with him. He even made a special exception to stay up late, if it was up to my dad no events or shows would run past 6:00PM so he could in bed by his usual 8PM bedtime.

We arrived at BC Place early…joining the thousands of other “early” fans vying for the best spots on the floor and after some mild pushing and shoving and light fisticuffs, we found our perfect spot 15 feet from the stage. I had to go to the washroom and told my dad I would be right back. After bumping into a friend along the way and chatting for a bit, I returned to where I had last left him at the back of the crowd. He was gone.

It should have been easy to find him but the crowd had grown immensely since I left to answer the call of nature and with no designated seating on the floor, my dad was nowhere to be seen, lost in the middle of a densely packed and raucous mass of humanity among thousands of screaming U2 fans.

I thought of my dad and said to myself, am I going to see this concert with or without you?

This once in a lifetime experience to see U2 with my dad was slipping away as the minutes ticked by, just like the disappearing opportunities today in fixed income.

***as a special tribute to the U2 concert that we saw, I have incorporated U2 song titles in the body of this newsletter and marked them in italics. See how many titles you can spot. PS. There have been 2 so far.

Why invest in Cash?

Two years ago, cash used to be the sweetest thing as short-term rates were high and rising. Now as investors are notified of their GIC’s maturing, seeing the renewal offers are causing them a mild case of nausea. Rates today are almost half of what they were last year.

2024, the Start of a New Rate Cut Cycle

A record amount of monetary and fiscal stimulus was unleashed into the economy during 2020 Covid pandemic and it took off like a Space-X rocket, well a Space-X rocket if it didn’t malfunction and explode. Two years later, things got really out of control. The economy was overheating, inflation rose to 40-year highs, and there was only so much Wordle, crochet and Peloton we could take. To cool down the economy, which was turning into a raging Alberta wildfire, we waterbombed the unforgettable fire by raising interest rates. Interest rates at 5% and 16-year highs did the trick, and the inferno was quenched with a loud hissing sound. Things were finally settling back to normal for the first time since toilet paper demand outpaced crypto currency during the depths of the pandemic.

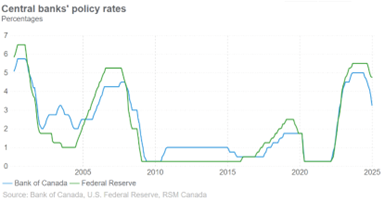

The wild ride was over and central banks could start lowering rates. The Bank of Canada cut rates by 2.25% and the US FED by 1%.

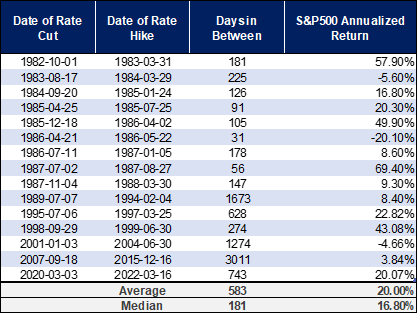

Market Performance During Previous Rate Cut Cycles

The average annualized return of the S&P500 since 1957 is just over 10%.

The average annualized return of the S&P500 over the past 16 rate cut cycle since 1982 is 20%, almost double the long-term average return.

We entered a new rate cut cycle in 2024 as central banks cut interest rates, the S&P500 returned 25% in 2024.

Hitting Pause

Not long after New Year’s Day, 2025, before we could even make a dent in paying down our Christmas bills, uncertainty again clouded the economy with the new US president vowing to implement his trade and economic policies. In early April, after many rumours of trade wars, Liberation Day arrived. The US slapped tariffs on almost everything and everyone, from iPhones manufactured in China to penguins on the Heard and McDonald Islands. Nothing, not even flightless aquatic birds, were spared.

After being traumatized with inflation that reached double digits a few years ago central banks hit pause on interest rate increases, and they hovered at elevated levels, almost like being stuck in a moment you can’t get out of.

The Central Bank

The FED has two mandates. maximum employment and stable prices. Let’s look at each of these.

1. Maximum Employment

Uncertainty around tariffs is weighing on the economy. Businesses and consumers are holding back from new investments and large purchases due to uncertainty and the longer it persists, the more it weighs on the economy.

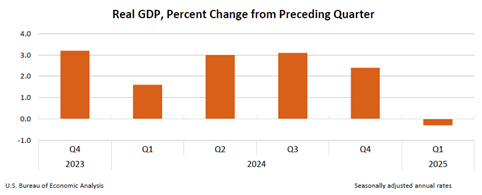

US GDP came in at +2.4% for the last quarter of 2024, then contracted -0.5% in the first three months of 2025[1]. GDP in Canada held up better in the first quarter as businesses rushed to stock up on supplies at pre-tariffs prices, but the Canadian economy is now slowing and contracted in April[2]. The chart below shows US GDP growth quarter over quarter and the dramatic slowdown this year.

With a slowing economy, job growth abating and businesses delaying hiring, weaker economic growth is putting pressure on employment. The job situation in Canada is already as dismal as the Canucks 2025-26 season prospects and unemployment has been rising and sits at 7%, the highest level in 9 years (outside of the pandemic)[3]. The economy seems like it’s running to stand still.

2. Stable Prices

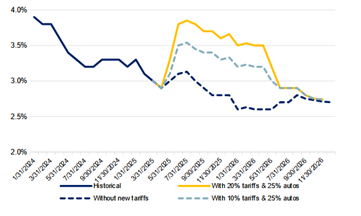

Inflation in both Canada and the US has been falling. Inflation was 9.1% in the US a few years ago, now it’s 2.4%[4]. In Canada inflation has dropped from 8.1% to 1.7%[5]. Inflation is still above the 2% target of central banks in the US but the slack in both the Canadian and US economies, along with a weakening labour market is helping to continue to cool inflation. Central banks are concerned with the short-term impact of tariffs on inflation. As we mentioned last quarter, tariffs are a one-time tax that boosts inflation in the short-term. In the chart below from RBC GAM, if the US implements the full tariffs announced on Liberation Day, we will see a short-term spike but by next year inflation will be back to the same level as if no tariffs were announced. The overall expected trend for inflation is down.

Fear in the Markets Today

The AAII Sentiment Survey asks investors each week if they are bullish, bearish or neutral on the stock market and they have published the results on a weekly basis since 1987. This represents a pulse on investors and their feelings on the market. When most investors are bearish, markets are moving on fear and when most are bullish, markets are moving on greed. The AAII Sentiment Survey offers the best view into the emotions that are in control of the short-term direction of the markets, just like the emotions involved in the ups and downs of our relationships. Imagine the insight men would have if they had a poll on how their wives or girlfriends were feeling each week. They would know if it was a good time to mention the coming week-long golf or fishing trip with the boys or whether it was time to offer a foot massage, flowers and a nice dinner out to try to forestall the coming of the apocalypse.

Extreme readings provide the best insights into the markets. When most investors are bullish there are few left to push prices higher, so markets underperform and the risk of a market correction increases. On the other hand, when the majority of investors are bearish, there are few left to sell and markets move higher. Sustained periods of bearishness when 50% or more of investors are bearish are exceptionally rare. Since 1987 there have only been six instances when more than 50% of investors were bearish for more than 4 consecutive weeks, or twice as often as the Canucks making the Stanley Cup finals during the same time. The previous record was 7 consecutive weeks in 1990, and we just blew that away. For the first time in 38 years more than 50% of investors from the AAII Sentiment Survey were bearish on the markets for 11 weeks straight. If you don’t think 11 weeks of negativity is a long time, just ask Melania Trump how long she has felt that way about her marriage.

There has never been a time when investors were bearish for so long and there are few investors left to sell today.

Since 1987 when more than 50% of investors were bearish on the markets for a month or more the average three-year total return for the S&P500 have been 46.6% and the average five-year return was 94.2%. The longer investors were bearish, the stronger the returns have been after[6].

Disappearing Opportunities

With the clock counting down on showtime, I needed help finding my dad as die-hard U2 fans continued to pour onto the floor like hungry zombies from the Brad Pitt movie World War Z. My cell phone wasn’t working since the thousands of U2 groupies were all using theirs at the same time, so I went back and found my friend to help. He’s 6’5 and he hoisted me up on his shoulders so I could see over the crowd. Resisting the urge to spread my arms like in the movie Titanic and shout “I’m Flying Jack”, I looked in all directions but there was nothing except a sea of haircuts from “That 70’s Show”.

I tried another tactic and started yelling my dad’s name, “Jeff! Jeff!”. I saw a hand shoot up in the middle of the crowd and a voice yell back, “He’s over here”. I had found him! I dove through the jam-packed crowd like a penguin trying to escape from tariffs and I arrived where the outstretched hand had been. I looked around but didn’t see my dad. I asked, “Do you know where, Jeff is?”. A stranger said, “Yes, I’m Jeff.” Apparently, there is more than one person named Jeff at this concert, who knew? I still haven’t found what I’m looking for.

I looked at my watch, five minutes to the show. Time was running out and my opportunity to see U2 open beside my dad was fading faster than many of the bargains in fixed income that have been snatched up in the past year.

We warned about the short window of opportunity as rates stayed elevated and investors who were scared were willing to part with their investments for prices and valuations not seen in decades. Soon higher rates at the bank would be gone and the limited time offers on bargain blowouts would be marked back up to full price. Not unlike the sale prices at the Bay which is now being applied to the entire company during its bankruptcy filing. In the last year and half the S&P500 is up over 30%, the S&P/TSX returned almost 35% and our favourite asset within the fixed income class, preferred shares, are up 35%[7].

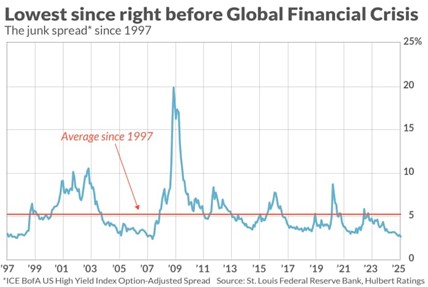

Many of the sales in fixed income are close to or have already ended. The chart below shows the extra return on high yield bonds that investors received. When spreads are low you receive little extra yield, and investors can expect limited future returns. When high yield spreads are large, investors pickup an extra yield and have the ability for outperformance when spreads tighten, and prices rise, like the price of Canucks tickets when in rare scenarios, they are actually winning. Spreads widened significantly in 2009, 2016 and 2020, wider than the age gap between Bill Belichick and his girlfriend, and subsequently high yield bonds returned 50%, 23% and 32% over the subsequent year.

Today, current spreads on high yield bonds are well below average and are at the lowest levels since 2007 offering investors limited upside. Spreads have also tightened in other areas with corporate bonds sitting at near record lows and some preferred shares at decade lows.

As investors have significantly bid up the price of fixed income, it is getting harder for investors to make money in this asset class.With opportunities fading in one area income investors are turning their focus elsewhere. The last two bull markets started because of falling rates but were sustained for years due to continuing low rates. Investors are reaching for yield like the kid reaching for the cookie jar on top of the fridge and as rates shrink on savings, GICs and other fixed income options and once those options disappear, investors have flooded into stock markets resulting in higher stock prices.

In December 2008, the FED dropped rates to zero. With limited investments options for cash and fixed income, funds flowed into the markets and from March 2009 the S&P500 returned over 450% to investors over the next 11 years.

Then in 2020 as cash looked for a new home with interest rates at close to zero to counter a worldwide pandemic, funds raced into bonds, then stocks and the S&P500 almost doubled over the next two years.

Hitting Play Again

So far this year, with interest rates still sitting at some of the highest levels in 16 years, employment weakening and inflation falling, pressure is building on central banks to start lowering rates again.

What About Trump?

Investors are worried about the impact Trump will have on the economy and markets. When Trump was first elected as President in 2016 investors had the same worries and panicked. Overnight markets first fell over 5%, but by the end of Trump’s first term the S&P500 had returned almost 68% ranking as the fifth-best market returns during a four-year presidential term since 1980. Trump’s first presidency included trade wars, an economy coming to a standstill during a world-wide pandemic and the US getting rejected trying to buy Greenland.

Investing Today

In the current investment environment, we are finding a few opportunities still in fixed income, but most are quickly finding an exit and disappearing. On the other hand, we are seeing great bargains in certain areas of the equity markets. We have been adding to these opportunities over the past year and even with the strong returns we have generated this year and last, we still see excellent value in International and Canadian stocks, as well as US small and mid-cap companies.

Markets climbed after March 2009 in the face of low rates and investors made almost 4X their money over the next decade in the S&P500 as low interest rates pushed market higher albeit, with some bumps and volatility along the way. The alternative of leaving cash sitting idle in a savings account with falling rates is looking as attractive as Madonna’s recent plastic surgery.

Tactical Changes

This year we took the opportunity to take profits in some of the best performing fixed income assets with limited upside and used the market volatility to pick up additional bargains with our elbows up investment in Canadian equities. We also hedged back some of our $USD exposure as exchange rates reached $1.45 and we are pleased with the tidy profit we made for our clients from that trade.

Now, back to the concert. As the clock counted down to the start of the show, I made one last ditch effort to push my way through the crowd in hopes of finding my dad. The crowd was now more tightly packed than the shopping carts of people leaving Costco but inch by inch hurdled my way through the crowd like Tom Cruise in Mission Impossible, manoeuvring around drunk fans, flying past sharp elbows and waving arms and dodging around selfie takers, I saw a familiar back of a head, one that I recognize from many long car rides to remote camping spots and shouted out to him. It turned...I couldn’t believe it was him! As I reached him, he grumbled, “Son, if you need to take that long going to the bathroom, you need to see a doctor. I have been waiting here for 45 minutes!”.

Investors should also not take so long to wait for the economy to improve, a change in political leadership or rates to start falling again. Some have already missed out on great opportunities and the longer they wait, the less there will be. I am so glad I didn’t miss out on the opportunity to see U2 with my dad. The show was magnificent, and they played all their classics my dad and I have been listening to since my childhood. The next show I attend with my dad I’ll attach one of those stretchy straps to him, the kind moms use to connect their toddlers to prevent them from wandering off so I don’t lose him.

-Kind regards,

Joshua Brown, CFA

Portfolio Manager and Wealth Advisor

[1] https://www.bnnbloomberg.ca/business/economics/2025/06/06/canadas-unemployment-rate-in-may-at-almost-9-year-high-outside-pandemic-years/

[2] https://www.ft.com/content/f75e5fab-431f-4a5a-aaed-883c3c0640e1

[3] https://financialpost.com/news/economy/canada-inflation-rate-holds-steady-may

[4] https://www.investmentexecutive.com/news/research-and-markets/u-s-gdp-shrank-0-5-in-q1-as-imports-surged/

[5] https://www.wealthprofessional.ca/news/industry-news/latest-stats-reveal-how-tariffs-are-biting-chunks-out-of-the-canadian-economy/389581

[6] https://www.fool.com/investing/2025/04/25/wall-street-dubious-history-near-100-success-rate/

[7] Return of the S&P/TSX Cdn Preferred Share Index

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © 2025 RBC Dominion Securities Inc. All rights reserved.