Smooth(er) sailing – How investment income can help stabilize your portfolio through market “storms”

Portfolio Advisor

April 17, 2026

Picture a sailboat cutting through open water on a perfect summer day. The seas are calm, the wind is steady, everything feels under control…even smooth. Then the weather shifts. Waves build, wind gusts sideways, and suddenly that smooth ride becomes a violent roll from side to side. Without stabilizers – those crucial systems that dampen motion and keep the vessel leveled – even experienced sailors can find themselves thrown off course.

Your investment portfolio can face the same challenge from time to time – it is, as history has shown us, a reality of investing. Markets can shift without warning. Economic downturns can arise quickly, almost as fast as geo-political ones can build and explode. When market volatility hits, investment income from dividends and interest can act as your portfolio's stabilizers, often determining whether you stay on course or are thrown off balance.

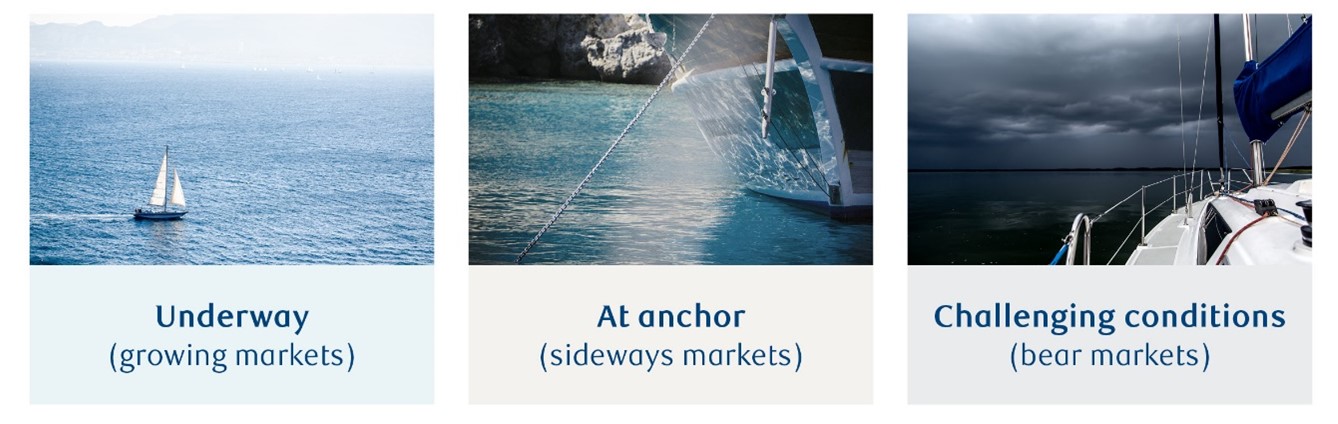

The three modes of stabilization

Just as marine stabilizers work in three distinct conditions – underway, at anchor, and in challenging seas – investment income can help provide stability through every market environment:

When your portfolio is moving forward during bull markets, dividend and interest income can reduce the side-to-side swings that come with short-term volatility. They can also provide solid returns and add to the compounding benefits of capital gains, even adding opportunities to buy more income-producing assets on a regular basis through programs like Dividend Reinvestment Plans (DRIPs). You can stay focused on your goal, not getting distracted by daily price fluctuations. | During flat or range-bound periods when prices go nowhere, dividends and interest payments can keep your wealth growing. Your portfolio generates returns even when capital appreciation stalls. And you continue to generate important cashflow even if your portfolio is moving sideways.

| When storms hit and markets decline, income becomes your primary source of stability. Regular cash flow allows you to meet expenses without selling assets at depressed prices – transforming you from a forced seller into a patient investor. And, the income you receive can be reinvested into the market at an advantageous time, boosting the effects of compounding over time.

|

The 2022 storm: a case study in the power of stabilizers

Market volatility is an inevitable part of investing in public markets, as the last bear market “storm” proved when the S&P/TSX Composite Index fell 8.66% in 2022 amid climbing interest rates.1 Many investors watched their portfolios decline and faced a difficult choice: sell assets at depressed prices to generate needed income, or stay invested, forego generating income and hope for a speedy recovery.

Those holding dividend-paying stocks experienced something very different. The S&P/TSX Canadian Dividend Aristocrats Index – which captures companies that have increased dividends for at least five consecutive years – fell only half that amount over the same timeframe.2 More importantly, these companies also continued sending quarterly payments to shareholders, providing income that helped ensure investors received the cashflow they needed without forcing a sale of their shares at less-than-advantageous prices. And, for those who didn’t need the cashflow, the dividend gains helped eliminate unrealized loses over the same timeframe.

Ideally, a portfolio that generates regular dividends and interest allows you to meet living expenses, fund your retirement, or reinvest – all without touching your principal.

The hidden cost of selling: why patience can preserve wealth

Selling assets during a market decline can create a permanent loss. When you liquidate shares at 20% or 30% below their previous highs, you can lose important gains or even lock in a loss. Worse, you sacrifice the future gains those shares might have delivered when markets recover over time.

Quality dividend-payers can provide stable income during market storms and deliver superior long-term performance. Consider the following: Canadian dividend-paying stocks have achieved an historical average annual return of 10.7%, compared to just 1.3% for companies that do not pay dividends.3 That is not a marginal difference – it could be the gap between building lasting wealth and keeping pace with inflation.

Building resilience: the strategic power of dividend growth

Some of the most resilient portfolios are built not on companies that simply pay dividends, but on those that grow their dividends consistently year after year.

During the COVID-19-driven market crash of 2020, the S&P/TSX Composite fell almost 38% from its February peak to its March trough.4 Yet even in that extreme environment, the vast majority of Canadian dividend-payers maintained, or even grew, their payouts. The dividend cuts that did happen were concentrated in hard-hit sectors like energy and travel, while Canada's blue-chip dividend “aristocrats” remained largely unshaken.

Companies in sectors like banking, utilities, and telecommunications have built decades-long track records of uninterrupted payments. The Canadian market has a number of companies that have survived recessions, oil shocks, financial crises, and pandemics without missing a payment.

Dividend-growers are typically well-established, financially strong businesses – the “blue-chip companies” that dominate Canadian portfolios. They often operate in stable industries like utilities, banks, and telecommunications, where cash flows are predictable, and even in areas like energy and mining, where business models and long-term demand are proven. When markets fall, these stocks tend to hold their value better than speculative growth companies with no earnings and no dividends.

Inflation protection: Growing income, not shrinking purchasing power

Here is the hidden danger of static income: inflation can erode it. A 4% dividend yield today might sound attractive, but if that payout never grows, inflation will steadily eat away at the purchasing power.

This is why selecting dividend-growers is essential. From 2015 to 2025, Canadian inflation averaged 2.67% annually, while Canadian banks grew their dividends by an average of 7% annually during the same period.5 That is a real return – after inflation – of over 4%, purely from income growth, before accounting for any stock price appreciation.

When it comes to fixed-income investments like bonds, safety is paramount. High-yield bonds might offer tempting returns, but they come with elevated credit risk. If the issuer defaults, you lose both income and, potentially, principal. Sticking with high-quality, investment-grade bonds, or GICs from well-capitalized institutions can help ensure your interest payments remain dependable.

But income is only part of the equation; how much you keep after taxes is just as important.

Beyond performance: The strategic advantage of tax efficiency

Holding Canadian dividend stocks in a non-registered account gives you a significant tax advantage.

Eligible Canadian dividends benefit from the Dividend Tax Credit (DTC), which significantly reduces the tax burden compared to interest income. Interest is taxed as regular income at your marginal rate,. Dividends, on the other hand, are "grossed up" and are then eligible for a federal and provincial tax credit.6

For retirees or anyone generating cash flow from non-registered accounts, this tax efficiency can be a game changer. Managing your investment income properly can help you keep significantly more of your income in your pocket after tax, helping you to meet your needs without eroding your wealth.

Staying the course: the confidence that comes from steady income

Ultimately, the greatest benefit of an income-focused strategy is psychological. When markets fall and headlines scream uncertainty, quarterly – or even monthly – payments hitting your account are a powerful antidote to worry or even panic.

Research shows that dividends typically account for approximately one-third of total returns in any given year, but reinvestment and compounding can increase this to roughly two-thirds over long-term periods.7 That is not a trivial amount. It can be the difference between wealth that compounds over decades, and wealth that stagnates because of selling too early, chasing performance, or letting fear drive investment decisions.

Help secure your financial future with a portfolio engineered for stability and income. Connect with your Investment Advisor today to build your all-weather strategy.

Sources

1.Morningstar. "S&P/TSX Composite Index Performance." https://www.morningstar.com/indexes/xtse/0000/performance

2.S&P Dow Jones Indices. "S&P/TSX Canadian Dividend Aristocrats Index." https://www.spglobal.com/spdji/en/indices/dividends-factors/sp-tsx-canadian-dividend-aristocrats-index/

3.RBC Wealth Management. "The Power of Dividends: Canadian Market Analysis." https://us.rbcwealthmanagement.com/delegate/services/file/173453/content

4.Bank of Canada. "Staff Analytical Note 2020-22: The COVID-19 Market Crash." October 2020. https://www.bankofcanada.ca/2020/10/staff-analytical-note-2020-22/

5.TD Wealth. "Dividends Expected to Deliver in 2026." February 2026. https://advisors.td.com/daviswealthmanagementteam/mediahandler/media/777309/Dividends%20Expected%20to%20Deliver%20in%202026%20-%20Newspaper%20article%20February%202026.pdf

6.TD Wealth. "Dividends Expected to Deliver in 2026." February 2026. https://advisors.td.com/daviswealthmanagementteam/mediahandler/media/777309/Dividends%20Expected%20to%20Deliver%20in%202026%20-%20Newspaper%20article%20February%202026.pdf

7.RBC Wealth Management. "The Power of Dividends: Canadian Market Analysis." https://us.rbcwealthmanagement.com/delegate/services/file/173453/content

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / ™ Trademark(s) of Royal Bank of Canada.Used under licence. © RBC Dominion Securities Inc. 2026. All rights reserved.