Hidden in plain sight: The concentration risk index investors miss

You think you're diversified. Your portfolio likely says you are. But have you considered that your 'different' funds might be invested in many of the same companies? We explore why true diversification is more nuanced than you might think.

You think you're diversified. Your portfolio likely says you are. But have you considered that your 'different' funds might be invested in many of the same companies? We explore why true diversification is more nuanced than you might think.

Kevin Deckert, CFA

Portfolio Analyst, RBC GAM

July 7, 2026

Investment diversification became widespread in the ‘50s by the American economist Harry Markowitz. His research created the foundation for modern portfolio theory, which showed how combining different, uncorrelated assets into a single portfolio lowers overall risk while maintaining target returns.

Most investors are familiar with these diversification principles today. However, many DIY index investors are mistaking owning more funds as effective diversification, exposing themselves to unintentional concentration risk.

Unintentional exposure

Consider a client who believes that they are globally diversified because they own a broad U.S. index, a global equity index, and a global technology index within their portfolio. Their portfolio might include:

- S&P 500 Index

- MSCI World Index

- MSCI World Information Technology Index

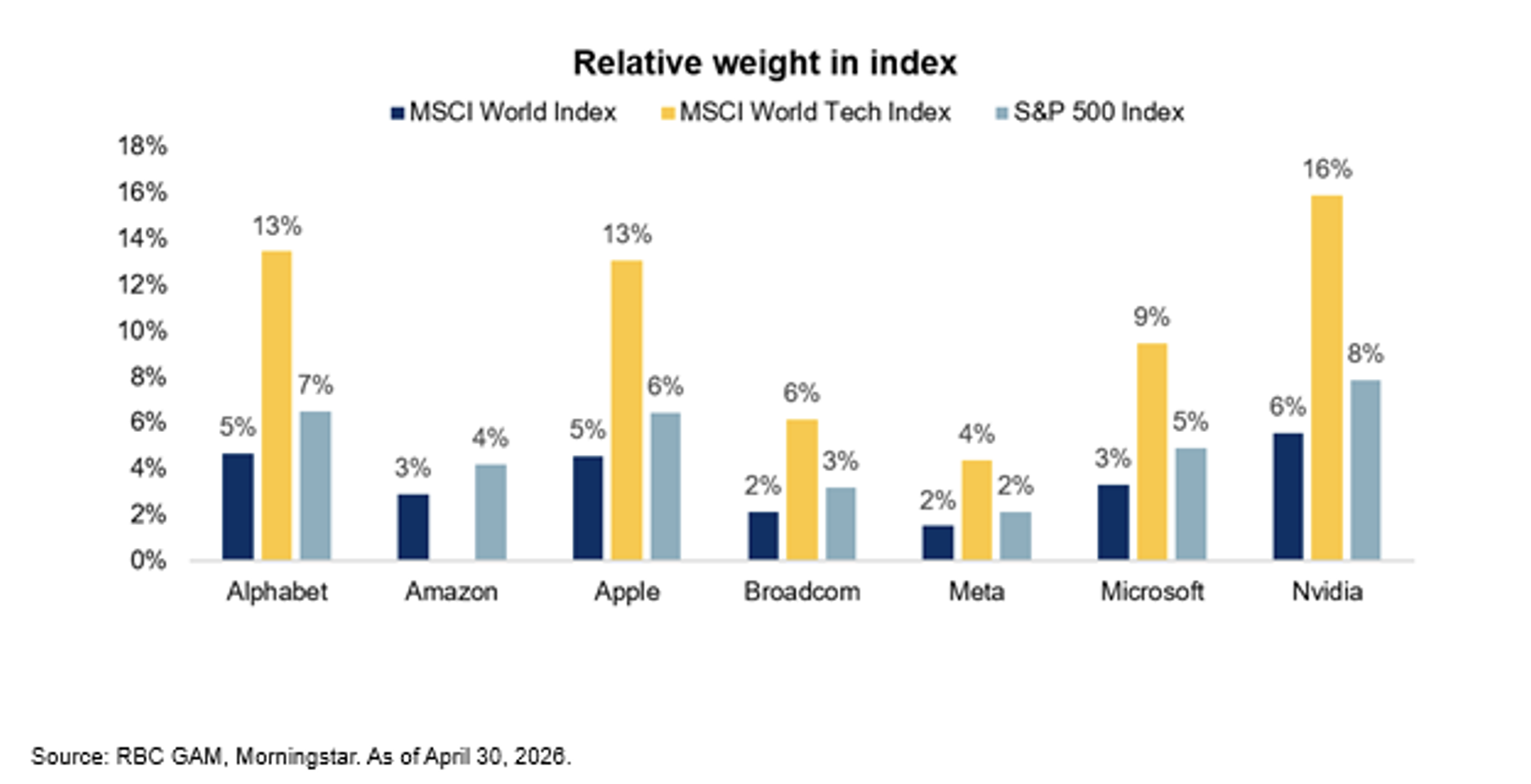

At first glance, the portfolio appears thoughtfully diversified across U.S. and global equities, while also participating in the broader AI theme by investing in the largest technology companies across the globe. Look beneath the fund labels, however, and a different picture emerges. These mega-cap leaders appear repeatedly.

These seven companies alone comprise 25% of the MSCI World Index, and 35% of the S&P 500 Index. Many index-tracking investors may not realize that they’re holding many of the same companies when investing across different funds. This investor is diversified by wrapper, but not necessarily by individual exposure. This is the quiet structural consequence of index investing.

The illusion of diversification

We have discussed a few real-time risks index investors face compared to an actively managed portfolio, such as concentration risk and valuation risk. As seen above, overlap can exist across commonly used equity indices. For example, over two-thirds of the MSCI World Index is allocated to the U.S. and thus its returns are strongly correlated to the S&P 500 Index. For clients, it’s imperative to be aware that different funds can have similar drivers of return.

This is where the illusion of diversification becomes important. Investors often evaluate diversification by counting funds or strategies. But if multiple funds are driven by the same underlying companies, then the portfolio may behave far less independently than it appears during market stress or periods of narrow leadership.

The concern is not that these companies are weak investments. Many are highly profitable, globally dominant businesses. The issue is that portfolio success becomes increasingly tied to a narrow set of economic forces such as technology leadership, U.S. mega-cap performance, and capital flows into the largest names. This is correlation risk disguised as diversification.

Final thoughts

When measuring diversification within a portfolio, a more relevant question becomes: how many truly independent sources of return does the portfolio contain? A client may own multiple index funds yet still have a majority of equity exposure driven by the same handful of companies and themes.

Actively managed strategies can assist with this problem by intentionally reducing exposure to overvalued areas, avoiding concentration risk, and positioning portfolios defensively when warranted. This ability to identify market leadership changes and pivot when necessary, can make all the difference when corrections occur.

In today’s market, diversification is no longer just about owning more securities or funds. It’s about understanding how those securities and funds interact, overlap, and respond to the same underlying forces. With seven companies representing a third of major indices, that distinction may be one of the most important portfolio conversations you can have with clients right now.