Kelly Bogdanova

Vice President, Portfolio Analyst, Portfolio Advisory Group – U.S.

May 19, 2026

Key points

- The sitting president’s party has almost always lost House seats in midterm elections, and those losses have often been large. Presidential popularity has played a role.

- U.S. equity returns in midterm election years have been the most muted, although gains in the following year have been robust.

- The market has often welcomed political party gridlock in Washington—but not always, and less so with a Republican president at the helm

- Election results have not been the main driver of equity prices over time. Corporate innovation, Fed policy and economic and earnings trends have mattered more.

- Five factors framing the election

With all 435 House of Representatives seats and 35 of the 100 Senate seats up for election on Nov. 3, there are some typical and atypical factors that could impact political party control in Washington.

A referendum on Trump 2.0

Midterm elections are often a referendum on the president’s term, even though the president’s name is nowhere on the ballot. And they are usually tough sledding for the president’s party when it comes to House races.

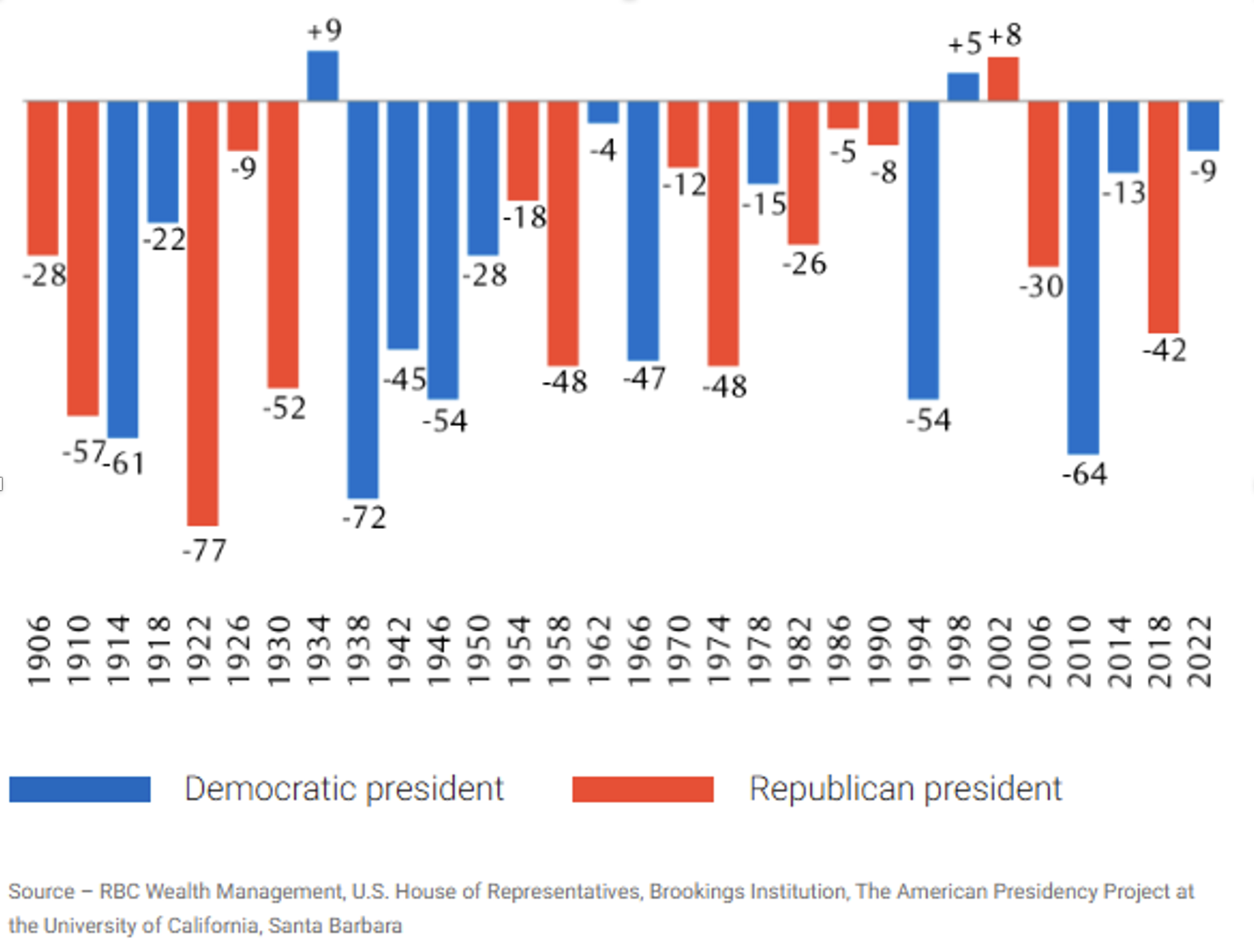

Since 1906, the president’s party gained House seats only three times in midterm elections, and the pickups were just single digits. Big losses were far more common, with Republicans and Democrats each shedding 28 seats on a median basis.

The data suggests presidential popularity played a role.

Since the Second World War, the two presidents who had high approval ratings in Gallup polls one month before the midterm election fared best: Democrat Bill Clinton in his second term and Republican George W. Bush in his first term. Their parties added five and eight House members in the 1998 and 2002 midterm elections, respectively.

Presidents with approval ratings below 50 percent in Gallup polls one month before election day in the post-Second World War era saw their parties stumble, with a median loss of 30 seats (range: 9–64 seats); for those with approval ratings above 50 percent, the median loss was only eight seats.

The president’s party has often suffered big losses

Change on House of Representatives seats held by the president’s party

This historical pattern is relevant for the upcoming midterm election given President Donald Trump’s approval ratings have been well below 50 percent in many polls for some time and Republicans currently control the House by only a narrow margin.

Regardless of where the presidential approval rating sits in the last few weeks before the November vote—when this rating matters most—there is little doubt in our minds that this midterm election will be a referendum on Trump 2.0 given the president’s outsized influence in the domestic political arena (and on the global stage too).

This has the potential to affect not only House and Senate races at the federal level but also some “down ballot” state races, shaping political party control over state legislatures and governorships.

Most House seats up for grabs in many years

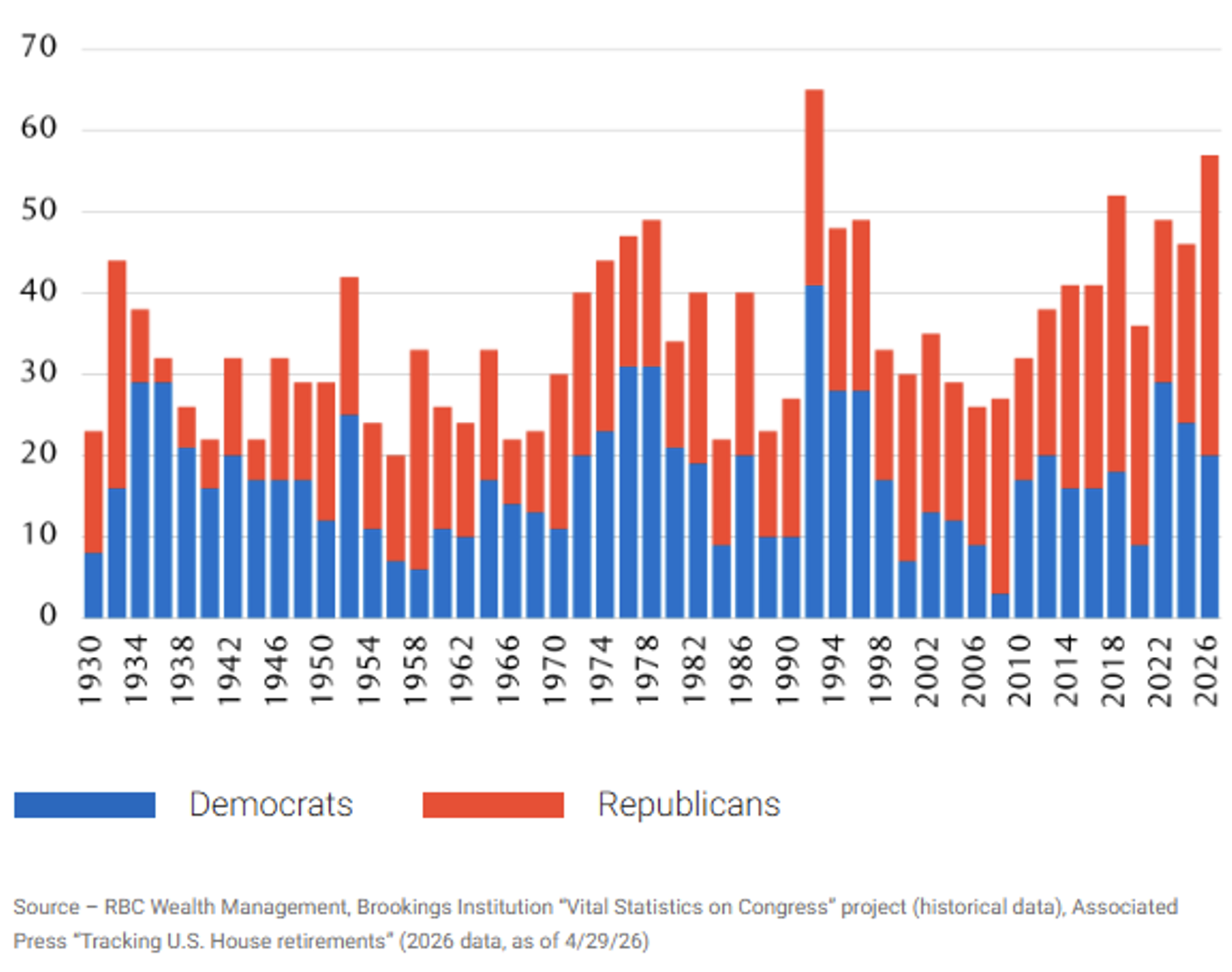

Another factor indicating to us that it will be challenging for Republicans to retain House control is the high number of open seats where no incumbent is running for office.

Among the 435 total House seats, 57 are open with 37 of those Republican, as of this writing. This is the second most total vacancies since 1930 and the largest number of Republican open seats during this period.

Second-highest number of House departures and highest number of Republican departures since 1930

Number of U.S. Representatives not running for reelection (either retiring or seeking a different office) by election year

Many of the vacancies are in districts that will likely be uncompetitive, where voter registration leans heavily toward one party or the other.

More than anything, the large number of Republican open seats is a marker to us. We doubt so many Republicans would be moving on if rank-and-file members felt confident the party would retain House control.

It’s well known inside the Washington Beltway that the majority party holds more power and perks—this is by design—and these preferences diminish noticeably for those same members, especially those in leadership, when party control flips and they are in the minority.

Redistricting shenanigans

The Trump administration and House Republicans set out to improve the party’s prospects in this midterm election by encouraging Republican-leaning states to voluntarily redraw their congressional districts in order to increase the likelihood that Republicans could win more seats. This process is often called “gerrymandering.”

Among the many criticisms of this process, redistricting can end up dividing voters within cities or counties who have shared interests, lumping them together with communities that differ greatly. Both Republicans and Democrats have engaged in gerrymandering for decades.

This cycle, initially the process did not go as Republicans had planned because some Democratic-leaning states ended up gerrymandering as well.

It remains to be seen how redistricting efforts could affect the balance of power in the House. There are some court challenges outstanding, and a recent landmark Supreme Court ruling about racial gerrymandering in Louisiana has raised the possibility that additional states could redraw congressional districts ahead of primary elections.

A high hurdle to flip the Senate

Republicans currently control the upper chamber with 53 of the 100 seats, and it would take a net gain of four seats for the Democrats to take control (a 50-50 tie would give the president’s party the majority as the vice president votes to break ties).

Republicans have a natural geographic advantage this election cycle. Among the 35 Senate seats up for election, more of them are in red states (those that tend to vote Republican) than in blue states (those that usually vote Democratic).

Polls have shown for many months that the Democrats would have to clear a high hurdle to take control of the Senate. However, a number of pollsters have recently shifted some seats to the “contested” bucket that just a couple months ago looked likely to be Republican wins.

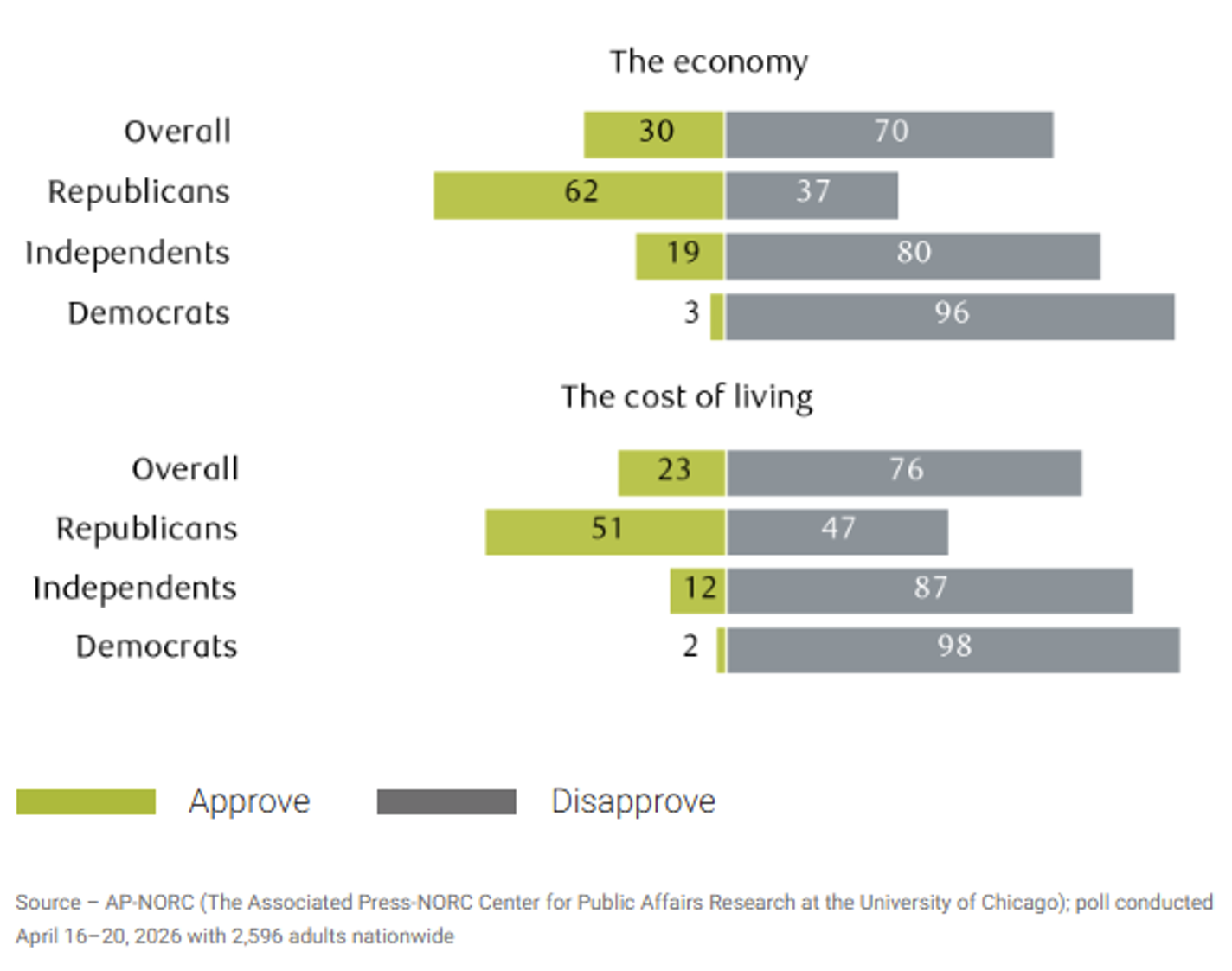

Closer to the election, we think the president’s approval rating and voters’ opinions about their economic prospects and inflation could impact some key Senate races. Pocketbook issues tend to be the most important concern of American voters in each and every election.

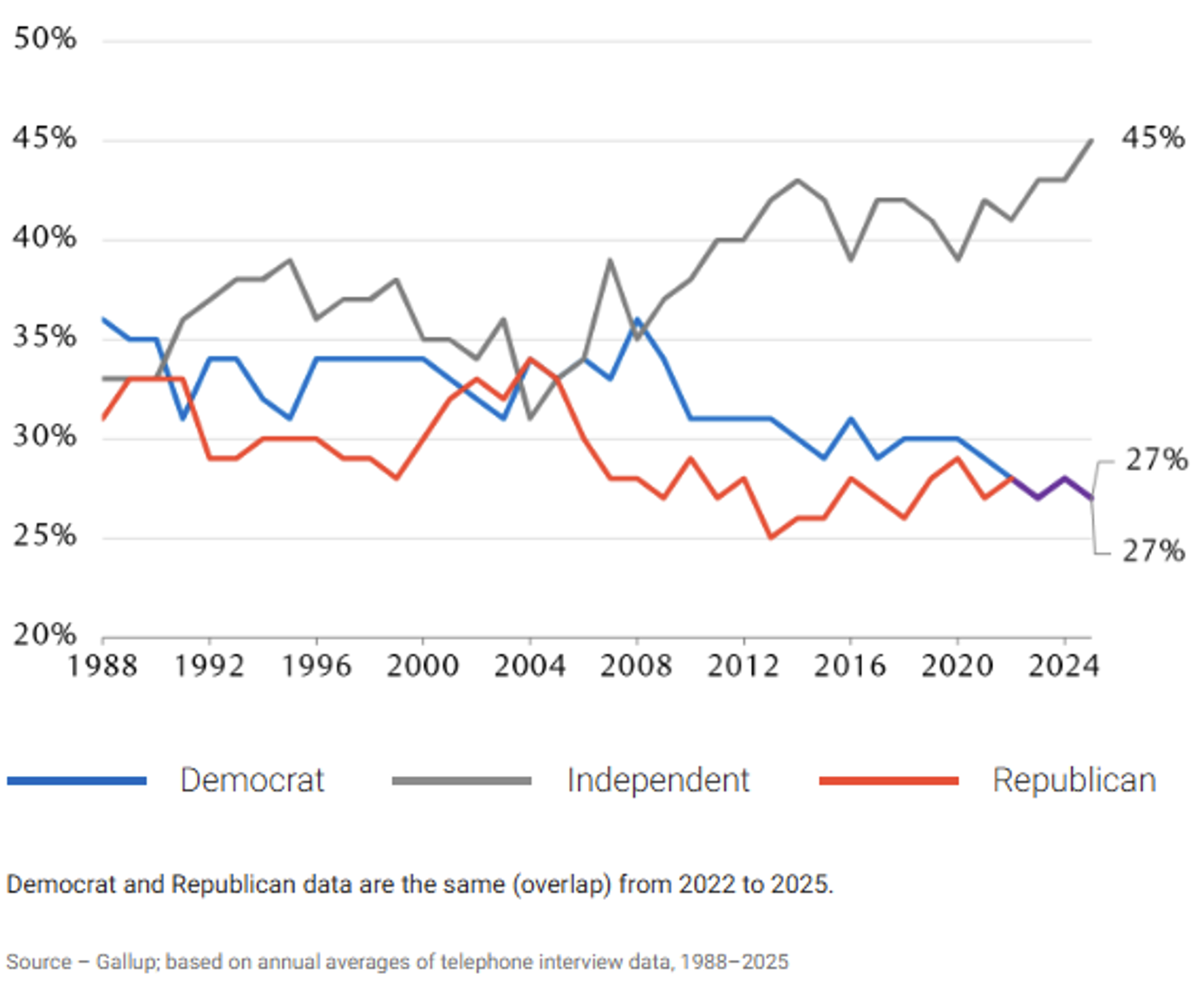

Independent voters in command

We think independent voters will tip the scales in some hotly contested House and Senate races this November.

Party loyalty has been decreasing for many years, and more voters now self-identify as independent rather than as a Republican or Democrat.

These are voters who are not registered as either Republicans or Democrats, or who are registered to one of these two major parties but no longer think of themselves as loyal party members or have a low opinion of both parties.

Independents still growing

Gallup poll question: In politics, as of today, do you consider yourself a Republican, a Democrat or an independent?

President Trump won the 2024 election with the help of independent voters, and many of these supporters perceived their economic prospects would brighten with his return to the White House.

But since then, independent voters’ assessment of the president’s handling of the economy has soured. Discontent about ongoing inflation seems to be a key reason.

Independents and Democrats rather negative about economic issues

AP-NORC poll question: Overall, do you approve or disapprove of the way Donald Trump is handling the economy and the cost of living?

What historical patterns say about the election effect

The big questions for investors are, do elections impact stock market performance and does political party control in Washington matter for the market?

Four-year presidential cycle

When we analyze return data within the framework of the four-year presidential cycle, there are some notable patterns.

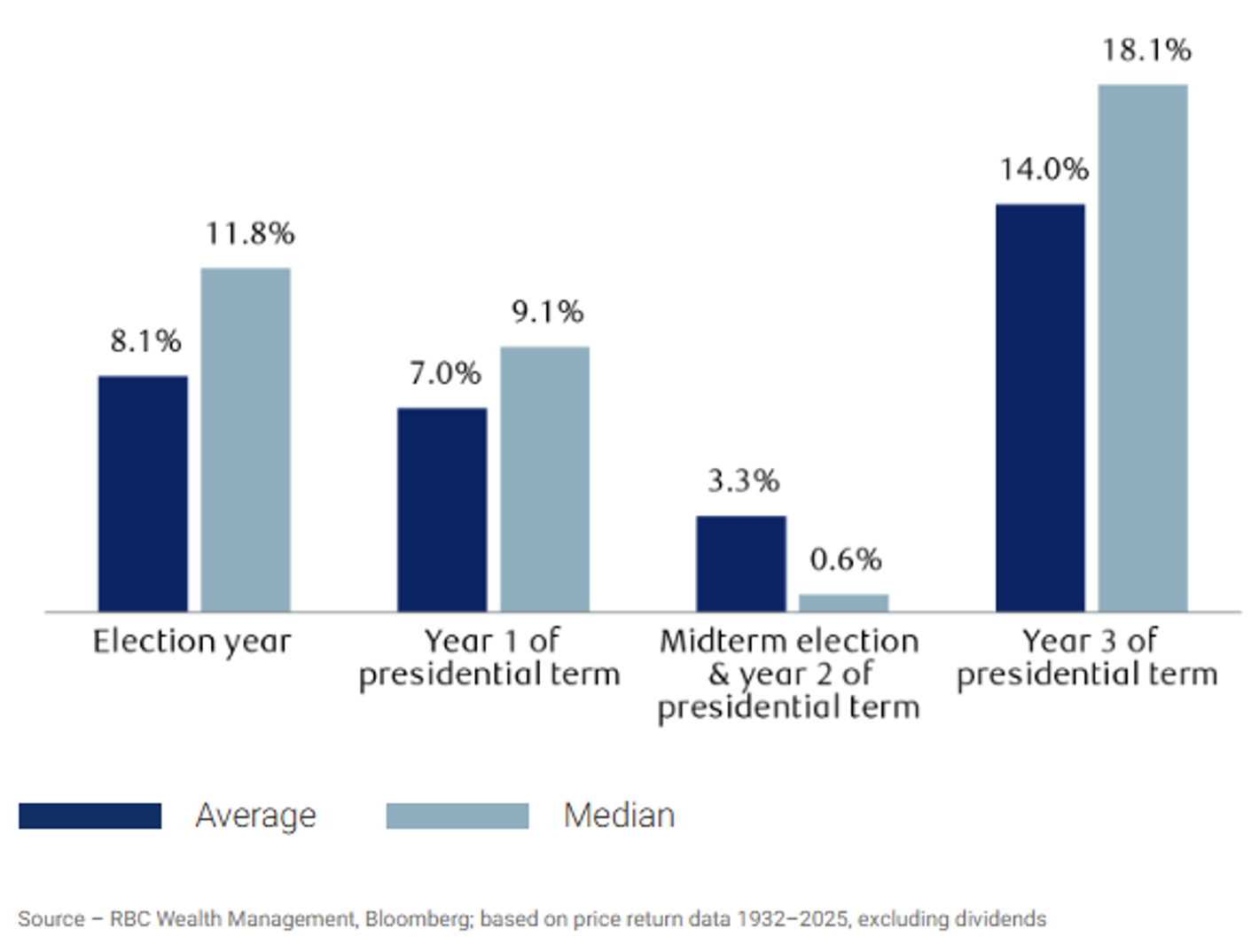

Stock market returns in midterm election years tend to be the most muted of the four-year cycle, with the S&P 500 rising 3.3 percent on average in those years since 1932. However, gains in the year following the midterms tend to be the most robust, with the index rising 14.0 percent on average.

Midterm election years tend to be weak, but the following year is typically strongS&P 500 performance during the four-year presidential cycle since 1932

Midterm election idiosyncrasies

Within the four-year cycle there are market return patterns associated with midterm elections that are not captured by the annual performance data, and these patterns have persisted regardless of events in Washington, and regardless of which party was in power or was gaining or losing momentum.

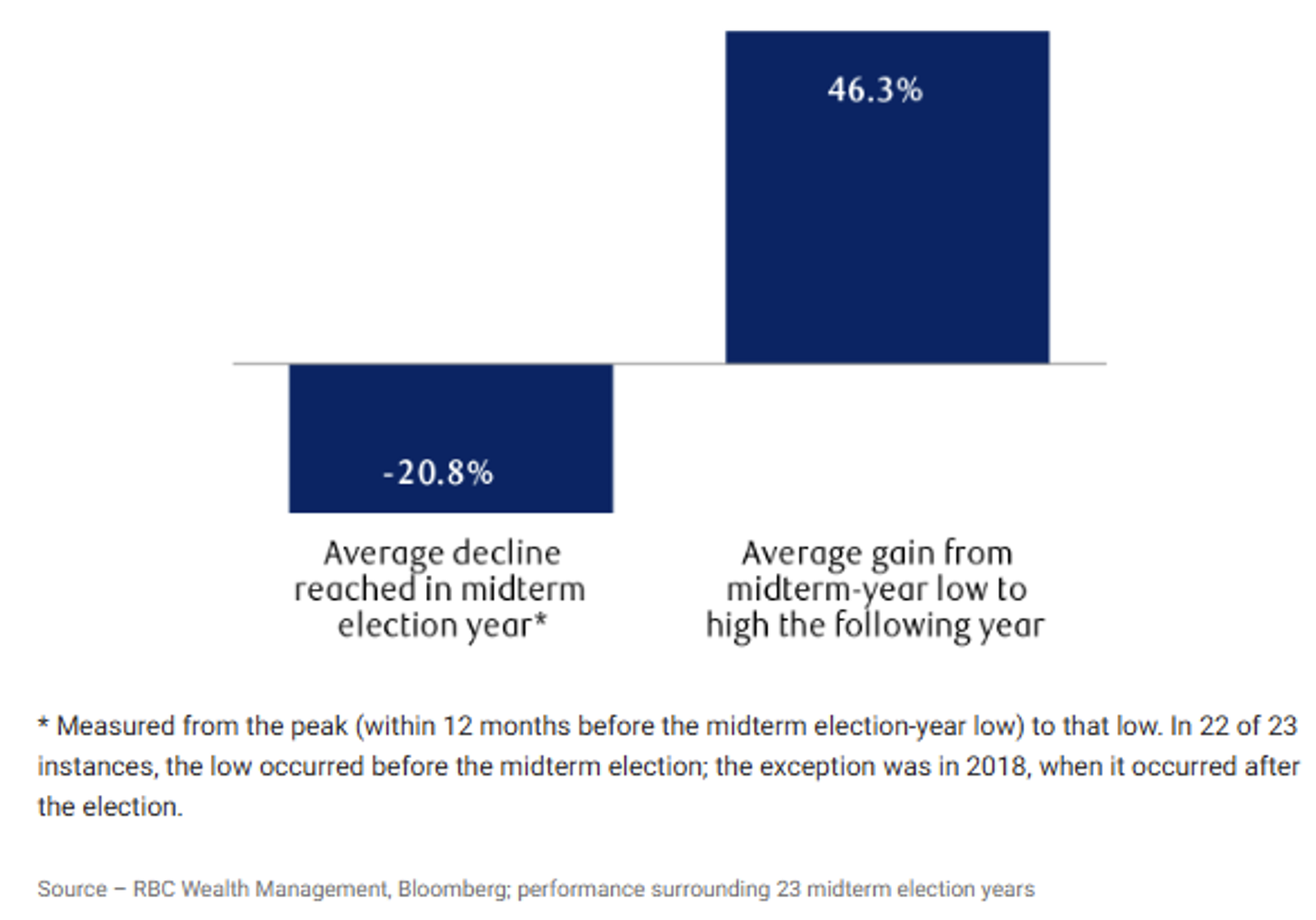

In the 23 instances we examined stretching back to 1934, the S&P 500 typically pulled back or corrected at some point during the 12-month period before the midterm election. The index declined 20.8 percent, on average.

However, the downside quite often was more than made up for with subsequent rallies. In those 23 instances, the market was higher at some point in the calendar year after the midterm election by 46.3 percent, on average.

As is typical with historical market data, there was significant variation in returns. The data behind the 46.3 percent average gain represents a wide range—from a 14.7 percent to 87.1 percent gain—although the market was able to exceed its previous high on 74 percent of the 23 occasions.

Corrections are common in midterm years, and so are follow-on rallies

S&P 500 returns surrounding midterm elections (1934–2023)

It’s also notable that during previous midterm election periods that were accompanied by inflation challenges, the market reached a new high in the year after the midterm election less frequently than during noninflationary periods.

Gridlock is good—sometimes

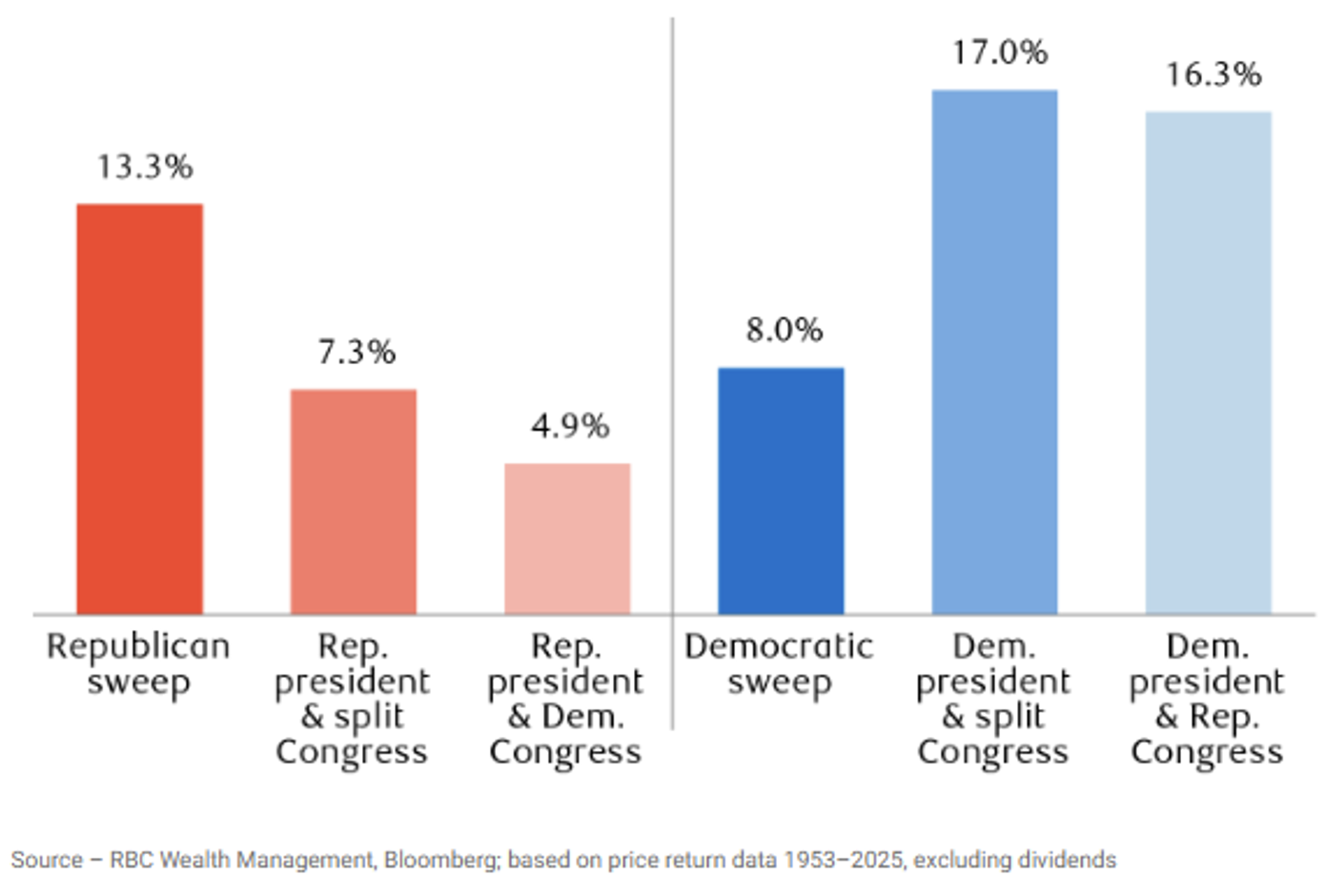

In terms of political party control, the market has welcomed certain forms of gridlock in Washington—otherwise known as split or divided government between the two major parties—but not always.

Our study going back to 1953 found that S&P 500 returns have historically been the highest in three cases:

- When Democrats have controlled the presidency and the two parties have split control of the House and Senate;

- When a Democratic president has served alongside a Republican-controlled Congress; or

- When Republicans have controlled the presidency and both chambers of Congress

By contrast, returns have been more muted with a Republican president and either a split or Democratic-controlled Congress.

Elephant or donkey—or both?

Average annual S&P 500 returns since 1953 by party control

Elections matter, but economic fundamentals matter more

Americans and observers outside the country who are interested in politics and public policy rightly assign high importance to U.S. election outcomes.

The data demonstrates there are indeed market performance patterns associated with midterm election years that we believe are worth paying attention to and respecting.

We are aware that the midterm election sample size is not large enough to permit one to draw conclusions supported by high “statistical confidence.” That said, the data is very suggestive.

In midterm elections, the sitting president’s party almost always loses seats and often those losses are large

The U.S. stock market has usually encountered a noteworthy correction in that year, which also has consistently been the lowest-performing year of the four-year presidential cycle

That correction has typically been followed by a robust rally in the calendar year following the midterm election, most often taking the market to new highs and making that year the strongest of the four-year cycle

In our assessment, however, elections and political party control in Washington are not the main drivers of U.S. stock prices over time. We think other issues have historically impacted the U.S. market more:

- Corporate innovation trends

- The Federal Reserve’s monetary policy decisions

- The natural ebb-and-flow of the business cycle and economy

- Related corporate earnings trends

When it comes to asset allocation recommendations, we focus on domestic economic and corporate earnings fundamentals, and specifically on indicators associated with recession risks. It’s recessions that are usually responsible for ushering in equity bear markets.

We don’t think the approaching midterm election or its outcome in terms of party control of the House and the Senate are reasons for long-term investors to change their allocation to U.S. equities in portfolios.