Hyah Alnehmi

Associate Portfolio Analyst, RBC Global Asset Management

May 19, 2026

In many cases, equities have matched or exceeded returns from Canadian real estate, particularly when the power of reinvested income and compounding is considered. That conversation is becoming increasingly relevant as Canada’s residential market continues to soften in central regions.

The long-term numbers may surprise investors

Since 2005, a hypothetical $300,000 investment in the S&P/TSX Composite Total Return Index would have grown to $2.0 million assuming dividends were reinvested. By comparison, the Canadian national average home price grew to roughly $834,600 over the same period.

Even the S&P/TSX Price Return Index, which excludes dividends and offers a closer comparison to home price appreciation alone, grew to more than $1 million.

Over time, that gap widened significantly as reinvested dividends continued compounding year after year, a reminder that long-term wealth creation is often driven as much by reinvested income as price appreciation itself.

Rental income narrows the gap — but not entirely

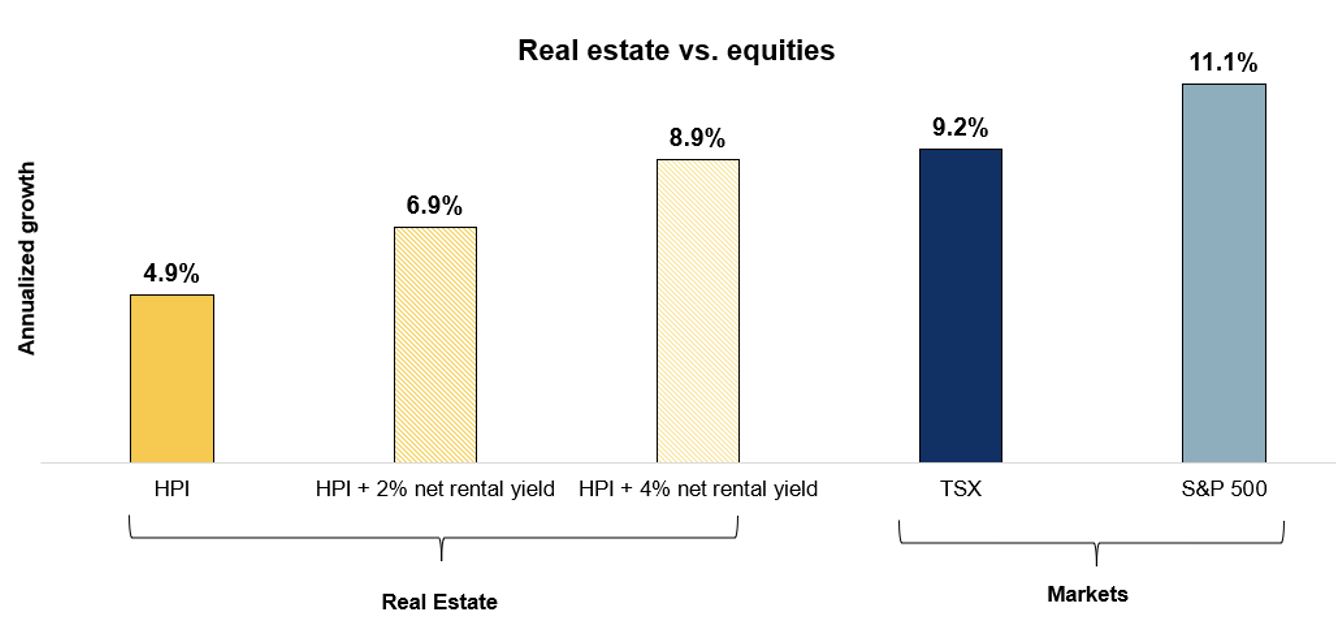

According to the Canadian Home Price Index (HPI), home prices have grown at an average rate of 4.9% a year since 2005. But price appreciation is only half the equation. Rental income can materially improve returns for investors who own income-producing properties.

To account for this, we modeled three real estate scenarios using Canadian housing data since 2005:

- Owner occupied - Home price appreciation only: 4.9% annualized return

- Average rental market - Home price appreciation + 2% net rental yield: 6.9% annualized return

- Hot rental market - Home price appreciation + 4% net rental yield: 8.9% annualized return

For comparison:

- TSX annualized return: 9.2%

- S&P 500 annualized return: 11.1%

Even under the strongest rental income scenario, both the TSX and S&P 500 continued to outperform over the long term.

A note on leverage

These comparisons assume unleveraged investments. In practice, most Canadians buy real estate with a mortgage, which can significantly improve returns by allowing investors to control a larger asset with less capital up front, though interest costs and maintenance reduce the net gain.

Key take-aways:

- None of this suggests real estate is a poor investment. For many Canadians, home ownership remains an important source of stability, leverage and long-term wealth creation.

- However, history also shows the risks of relying too heavily on a single asset class. Equity markets have consistently rewarded disciplined investors through diversification, reinvested income and exposure to global economic growth.

- Real estate will likely remain a cornerstone of wealth for many Canadians. But history shows that long-term financial success is rarely built through a single asset class alone.