Kelly Bogdanova

VP, Portfolio Analyst, PAG - US

June 2, 2026

Anyone who has fixated on the recent U.S. stock market rally without paying attention to other news might have assumed that all is right with the world.

The S&P 500 has surged 17 percent since the late March Iran war low and is up 8.6 percent year to date through May 20.

This impressive run has materialized despite a barrage of challenges:

- Ongoing energy and fertilizer supply problems along with uncertainties about whether the U.S.-Israeli war with Iran could reignite, further damaging the region’s infrastructure

- Another domestic and global inflation wave linked to high energy prices

- Treasury yields jumping to multiyear highs

- Market-based expectations about Federal Reserve policy shifting from a forthcoming rate cut to at least a long pause, and even the small possibility of a rate hike later this year

- Consumer sentiment in the U.S. dropping to the lowest level since records began in 1978

- Americans’ poor attitudes about the economy in multiple opinion polls

Is the stock market living on another planet?

AI buildout gets most of the credit

From our vantage point, the market is grounded where it normally is, on corporate profits. This is why it has defied the challenges thus far:

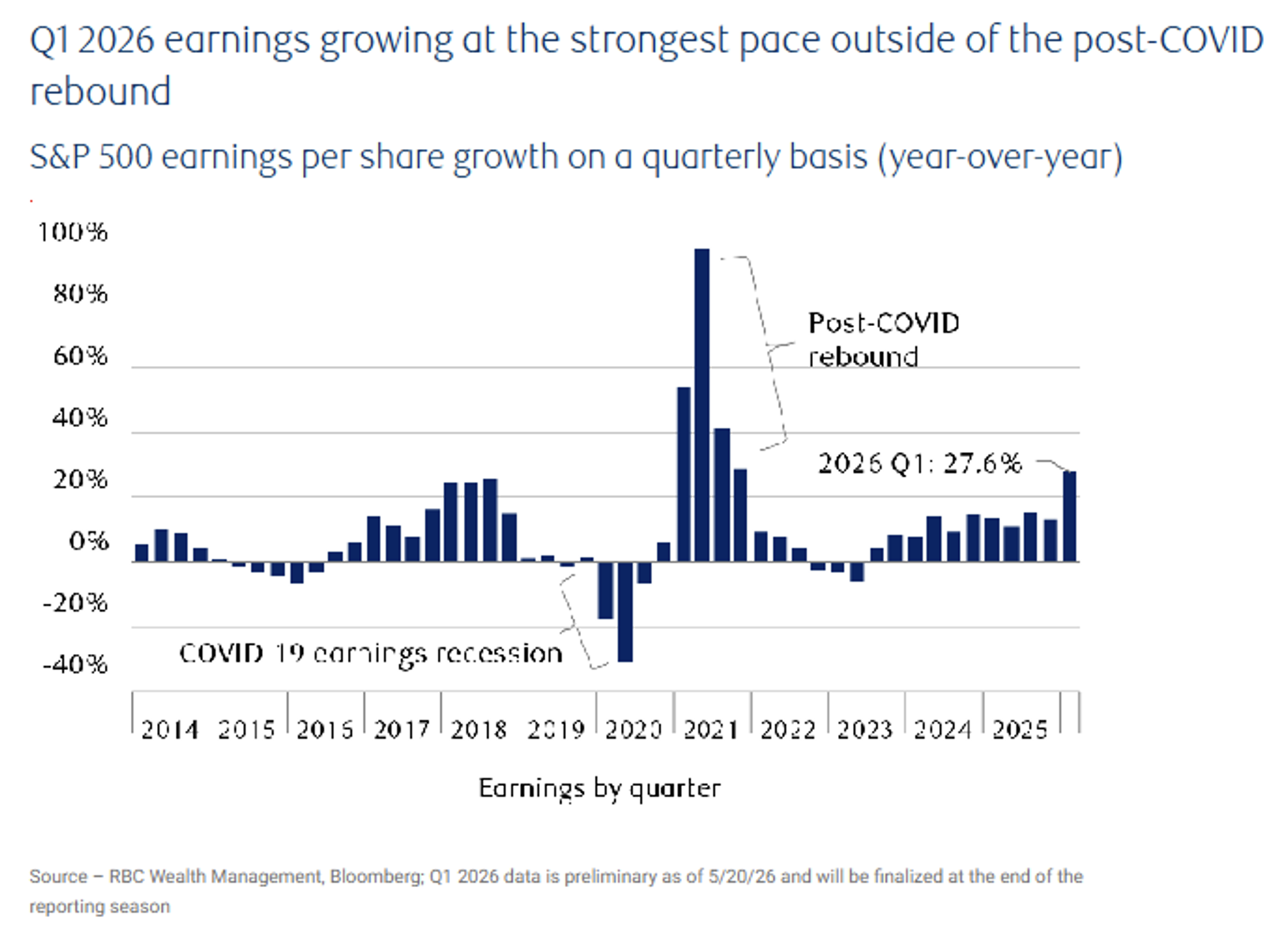

- S&P 500 earnings growth is pacing at 27.6 percent year over year in Q1

- This is more than two times higher than the 12.4 percent consensus forecast just before the earnings reporting season began in mid-April

- Outside of post-recession rebounds, earnings growth rarely exceeds expectations by such a large magnitude—in other words, it’s an eye-popping difference

- The ongoing AI infrastructure buildout is by far the main reason

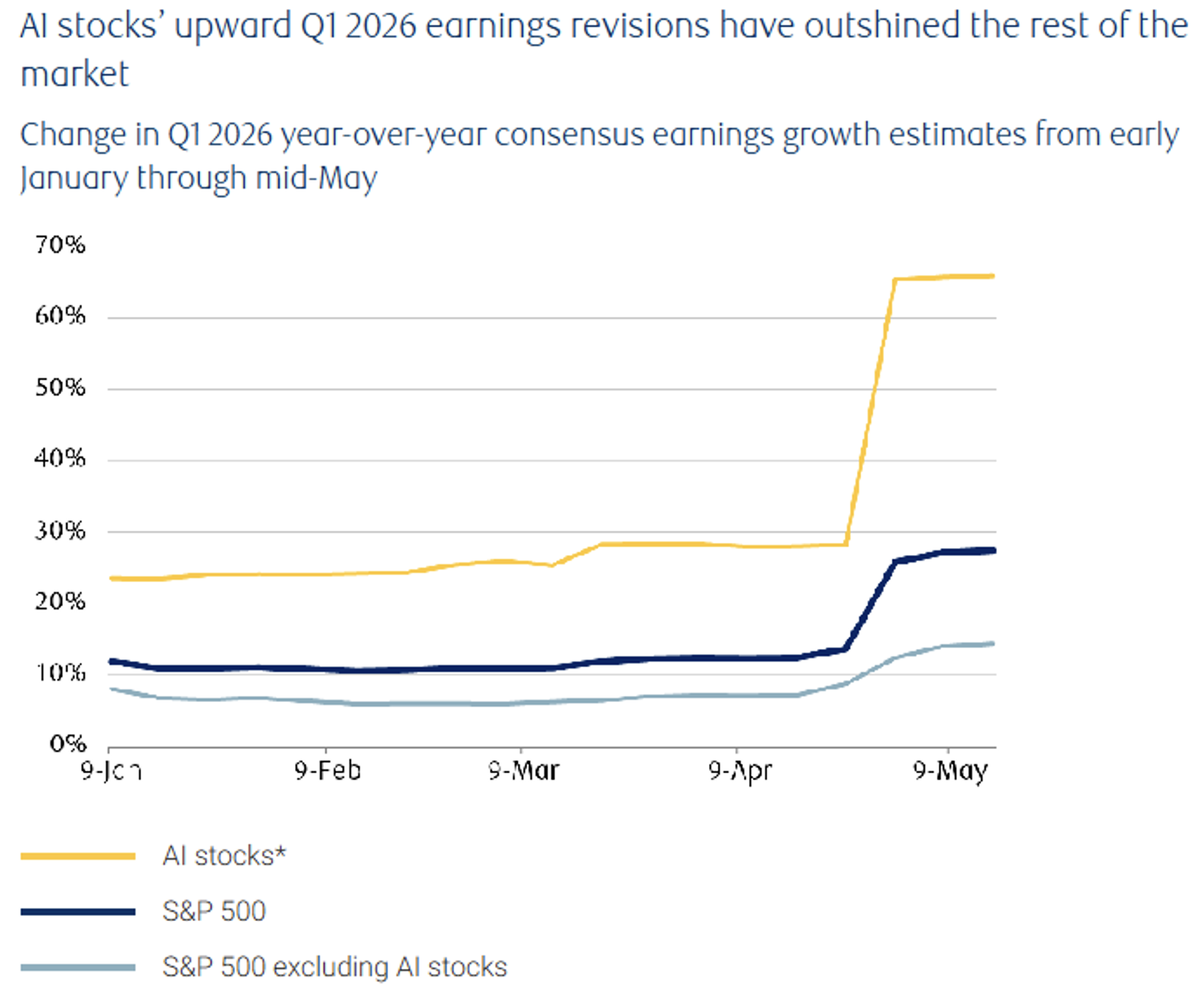

- Within the S&P 500, the AI basket of stocks saw its Q1 consensus earnings growth forecast surge from 23.6 percent in early January to nearly 66 percent recently

- Inside the AI group, semiconductor and semiconductor capital equipment stocks have led, delivering 85 percent year-over-year earnings growth in Q1

When AI stocks are excluded from the S&P 500 data, at first glance the earnings growth rate looks much less impressive at 14.4 percent year over year.

Investors should keep in mind, however, this non-AI profit growth rate is above the S&P 500’s long-term average level. And it is rather high on a historical basis when the fastest-growing area of the market is excluded at any given time, especially outside of post-recession rebounds.

Seven of 11 sectors are on pace to grow earnings at double-digit rates in Q1, including Materials at 44 percent and Financials at almost 23 percent year over year.

The S&P 500’s overall 27.6 percent earnings growth rate in Q1 is also impressive compared to most years since 2014. It’s the strongest growth rate outside of the highly unusual post-COVID period, which followed abrupt and deep earnings and economic recessions and included unprecedented fiscal stimulus.

Mindful of Middle East risks

As long as S&P 500 earnings growth has the potential to rise at a respectable clip over the next 12 months or more, we think the bull market can persist, notwithstanding some turbulence along the way.

A strong relationship between earnings growth and stock market returns has historically played out over time.

When profit growth rises over a number of quarters or years, the stock market tends to remain elevated or push higher. Conversely, when earnings growth falls during periods of economic weakness or recession, the market tends to wobble or decline.

The consensus forecast currently calls for double-digit profit growth in each of the next six quarters, driven by the AI infrastructure boom amid a non-recessionary environment. At this stage, RBC Economics forecasts U.S. GDP growth of 2.1 percent in 2026 and 1.9 percent in 2027.

Risks to this scenario, in our view, largely centre on the Middle East:

- Whether the region’s energy and chemicals infrastructure is further damaged due to a renewed military clash, and/or

- Whether Strait of Hormuz commodity flows remain constrained for a prolonged period

While the consensus earnings growth prospects look attractive to us, the chances that shipping traffic through the Strait of Hormuz could remain throttled for additional months are too big to ignore. We would continue to hold U.S. equities up to, but not beyond, a Market Weight allocation.