George Stedman, CFA

Senior Portfolio Manager

April 7, 2026

First Quarter 2026

Investors today are faced with two very different massive unknowns: Donald Trump’s behavior and

Artificial Intelligence (AI).

Trump’s proclamations, threats and deadlines create tremendous uncertainty, and, in financial

markets, uncertainty is risky. Last night, April 7, Trump declared a two-week ceasefire in his war on

Iran. Today, April 8, stocks are up, and oil is down. The Iran war is unforecastable, however I believe

that this too will pass. Hopefully Trump will find a way out. For now, we don’t know how long the

energy crisis will last or how much damage has been done to oil facilities. If oil doesn’t go down, I

don’t see stocks going up.

Trump has made various threats, against Canada and others. We don’t know if there will always be a

TACO Tuesday. Trump’s trade wars are another persistent uncertainty.

Warren Buffett famously was once asked by CNBC about the threat of a third world war. He said if

he knew that there would be a world war he would still be buying the same kinds of stocks. He would

prefer productive assets, such as businesses and farms, over cash as inflation would reduce the value

of cash, but businesses would be able to adjust their prices for inflation. During World War Two

stock prices went up. Companies that make things that people want, and need, are a good store of

value.

The importance of AI is hard to calibrate. Reinhardt Krause reports “Four hyperscalers – Alphabet’s

Google, Amazon.com, Meta Platforms and Microsoft – are now expected to spend $645 billion in

2026, representing growth of 56%, or $230 billion on a dollar basis.” (Dow Jones Newswire 8 April)

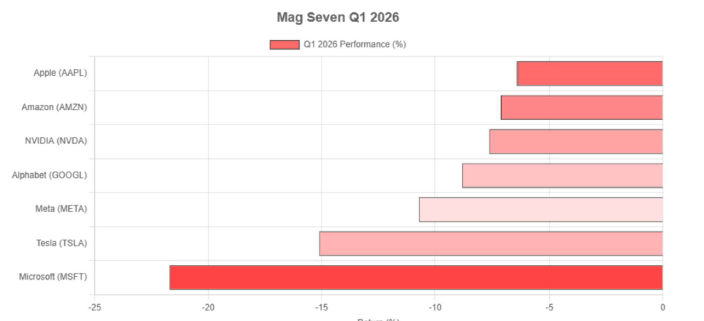

In the first quarter concerns grew that these capital expenditures are too much. In the first quarter

NASDAQ was down 7.1%, the largest quarterly decline in a year with a 4.8% drop in March alone.

All 7 of the Magnificent Seven were down, Microsoft, which late last year was one of the most

valuable companies in the U.S., was the worst, down 23%. The Mag 7 became, at least for a time, the

Lag 7. Software As a Service (SAAS) stocks everywhere were down a lot, irrespective of their

geographic location. About the most valuable company in Canada late last year, Constellation

Software, was down 28% in the first quarter. SAP, about the most valuable company in Germany,

was down 31%. There was a concern that customers could write their own software leading, as was

said, to a SAASmageddon in the first quarter.

Generated with RBC Assist Pro – Data from Benzinga.com – April 1, 2026

Microsoft Corporation (MSFT-NASQ) - $370.67 Jan 3, 2023 – March 31, 2026, Daily

FactSet – April 9, 2026

Huge capital expenditures are reducing the free cash flow of the hyperscale cloud companies, but

strongly benefiting manufacturers of components used in AI data centers. Corning is a spectacular

example. Its fiber optic cables are sought after as better for data centers than copper wire. Corning

shares are up about 90% just since January 1. In many portfolios, where the proportion in equities

has risen above long-term targets, and, where Corning has become an overweighted position, we

have been reluctantly trimming it, as part of our regular portfolio rebalancing.

As an aside, I often hear suggestions to invest in certain geographies. To my way of thinking, as

someone who prefers to buy shares in companies instead of market indices, industries or sectors that

companies are in are more important than their locations. The Canadian stock market will do well

relatively if Energy or Financials do well. U.S. stocks will do relatively well when technology stocks

do well, because of their large weighting in those indices. We saw this in the first quarter where the

Canadian market was up because of oil and gold, and the U.S. stock market was down largely because

of the Mag 7.

Some companies were insulated from the threat of AI. Think HALO, heavy assets, low obsolescence.

Companies that transmit electricity, like Fortis, that operate landfills and garbage trucks, (Waste

Connection), railroads (Canadian National), pipelines (TC Energy) and water (Xylem) are not likely to

be replaced by AI soon.

In the face of these two big risks, AI and Trump, we will, as I like to say, try to keep calm and carry

on consistently rebalancing portfolios to our long-term asset allocation targets. We will remain

balanced and diversified and continue to monitor position sizes to mitigate risks. Stock markets

usually bottom among uncertainty and climb a wall of worry. Hopefully this time will be no different.

I hope you had a nice holiday, and I wish you some fine Spring weather. Thanks for reading.

Sincerely,

George Stedman, CFA

Senior Portfolio Manager

Please visit us at www.georgestedman.com

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC

Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / ™ Trademark(s) of Royal Bank of

Canada. Used under licence. Used under licence. © RBC Dominion Securities Inc. 2023. All rights reserved.