Hayes Vickers Private Wealth

September 25, 2025

When central banks announce a rate cut, it makes headlines. Beyond the news cycle, what does this mean for the economy - and for you? In this update, we will break down what rate cuts are, why they matter, how they affect the housing market, and how tools like the First Home Savings Accounts (FHSA) can support your financial goals.

Understanding Rate Cuts and Their Impact

A rate cut happens when a central bank lowers its key benchmark interest rate, referred to as the overnight rate. This is the rate banks use to lend to one another overnight, and it sets the tone for borrowing costs throughout the economy.

Central banks use rate cuts as a policy tool to support the economy by encouraging borrowing and investing, especially during times of slower growth or financial stress. The ripple effect touches everything from your monthly mortgage payment to corporate expansion plans.

Why does this matter? Generally, when interest rates are reduced:

- Borrowing costs - mortgages, auto loans, and business financing often see lower rates.

- Savings returns - savings accounts and short term investments see lower returns.

- Markets - stock markets often react positively, while bond yields typically fall.

Rate Cuts in Today's Economic Environment

Both the US Federal Reserve (Fed) and the Bank of Canada (BoC) lowered their benchmark interest rates this month. This is a significant policy decision after a long period of no changes due to trade and economic uncertainty.

The Fed cut its benchmark rate by 0.25%, down to 4.0%-4.25% for the first time since December 2024. It came after some weaker job numbers over the summer which heightened concerns over a potential growth slowdown.

The BoC followed suit, also cutting rates by 0.25% this month to 2.5%. The decision reflects easing trade tensions (with most trade flows still being protected under USMCA and the removal of retaliatory tariffs) which has helped keep inflation in check.

Policymakers are still being cautious, emphasizing that they would be “proceeding carefully”, because the policy and economic environment is still uncertain.

Economic implications for Housing

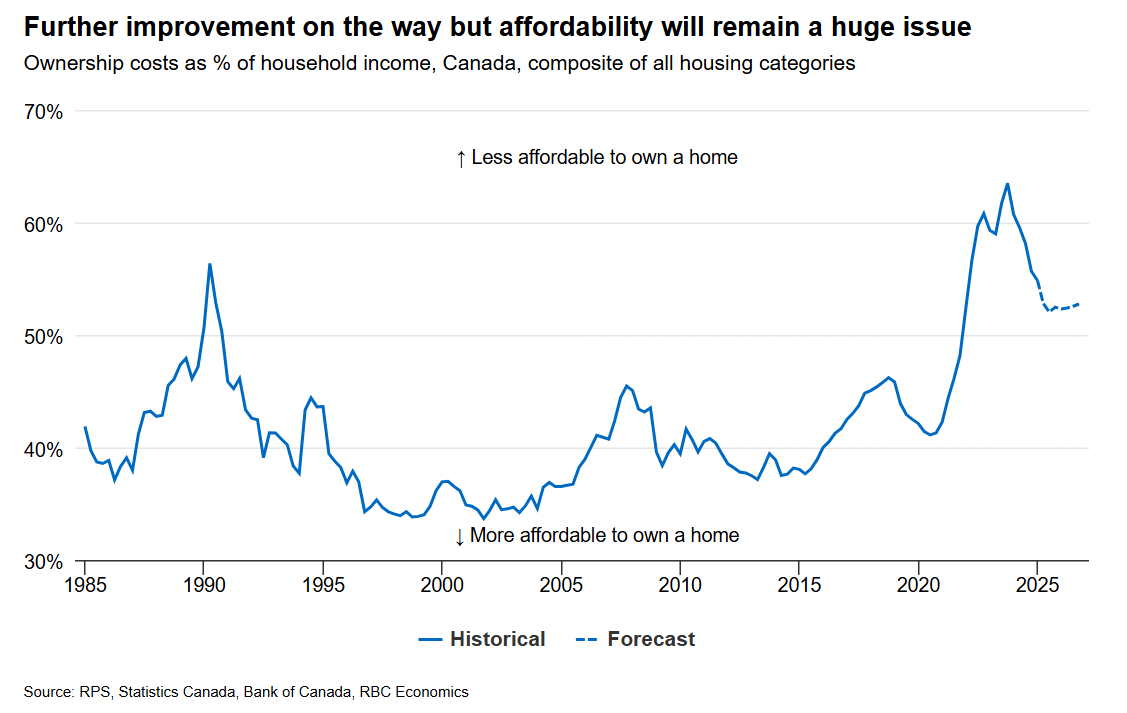

Lower rates usually help housing and other parts of the economy that rely on borrowing such as small businesses and companies. In Canada, housing activity has increased recently, with existing home sales reaching a 2025 high this month. This is partly due to relatively lower prices and more homes being available. However, some regions, like Ontario and British Columbia, still have elevated inventory levels, which can affect property values. Overall, the housing sector continues to face some challenges, including affordability, slowing population growth and broader economic uncertainty. Lower financing costs could provide a timely boost to demand in the Canadian housing market. RBC economics notes that owning a home in Canada is the most affordable it's been in three years and predicts small improvement in the months ahead, although most of the recovery is likely behind us as the BoC approaches the end of its rate cutting cycle.

Similar dynamics apply south of the border, where the Fed has just begun it's rate cutting cycle. Lower mortgage rates could provide relief in a market constrained by affordability challenges and muted builder activity.

Key Takeaways

- Central banks are trying to balance controlling inflation with supporting jobs and growth. Rate cuts can help keep the labour market stable.

- Rate cuts also provide a short-term boost to the housing market but may not solve the affordability issues.

- The outlook remains uncertain over how far and how fast interest rates will fall, as central banks are also committed to maintaining inflation stability. Households and investors should expect a data-dependent and gradual path forward.

- We will be watching monetary policy closely alongside government bond yields as central banks navigate the complex tradeoffs between the labour market, inflation, and the broader economy.

First Home Savings Account (FHSA)

If you are planning to buy your first home, or if you are the parent or grandparent looking to help the next generation, The First Home Savings Account is a valuable tool. It allows eligible individuals to save up to $40,000 tax-free for their first home. This account combines features of RRSP and TFSA where contributions are tax deductible (like RRSP) and withdrawals, including earned income are tax-free (like TFSA). If you are interested in learning more about this account, please don’t hesitate to contact us.

Conclusion

Rate cuts are more than just a policy move - they ripple through the entire economy, influencing borrowing, saving, and investing. Understanding these dynamics is our priority to continue to support you attaining your financial goals.

Next Steps

- If this blog generates new ideas or questions about your family's goals don't hesitate to contact us.

- Share this blog with your friends and family.