Are you looking for the “perfect” investment?

Everyone wants the “perfect” investment, but this piece explains why it doesn’t exist and what actually matters instead. It breaks down how aligning your strategy with your real goals, not chasing certainty, is what leads to better long-term outcomes.

Everyone wants the “perfect” investment, but this piece explains why it doesn’t exist and what actually matters instead. It breaks down how aligning your strategy with your real goals, not chasing certainty, is what leads to better long-term outcomes.

Mark Krygier

Senior Portfolio Manager & Wealth Advisor

March 31, 2026

Capital markets have become very volatile since the joint attack on Iran and the subsequent rise in oil prices. These are the times that both test the “mettle” of experienced investors and when novice investors may start to wonder what they got themselves into. Few people are satisfied with the low returns which come from safe products like savings accounts, money-market funds or GICs/CDs. On the other hand, I suspect few investors actually enjoy the volatility that is inherent with investing in equity (stocks). Canadians often like to reassure themselves that at least the Canadian bank stocks can provide great long-term returns, from both the dividend income they produce as well as the long-term rise in their share prices. However, they also tend to forget the drop of 50% in the value of even these “safe” bank stocks during the sub-prime mortgage financial crisis in 2008-09. A 50% “drawdown” is not comfortable at all, and I can tell you from experience, “been there, done that.”

When I sit across the table from a new client or a prospective client, a large portion of the meeting is spent simply trying to clarify firstly what is their realistic investing time horizon, and secondly, what is their investment agenda. Often, I am told, “I don’t want to invest in anything too risky, and I don’t have high expectations. I would simply like to grow my capital by 8 to 10% a year, with no capital risk and with full access to my money at any time.” In other words – where can I find the “perfect investment?” In the investment world, the starting point is often referred to as the “risk-free” rate of return, which is measured by either the 5-year GIC/CD rate or the 5-year Government of Canada bond yield (or the US Treasury rate). In today’s terms that would be in the 2-4% range, a far cry from the 8-10% sought by so many. Clearly there is a great divide between what investors with “simple” needs want and what the risk-free rate actually provides. In addition, consider that buying a 5-year GIC/CD locks up your money for 5 full years – which means no access to your money if rates go higher or if a buying opportunity in another investment arises. So, what’s the answer?

I am in the middle of reading a book entitled, “No one would listen” by Harry Markopolos, the forensic accountant who blew the whistle on Bernie Madoff, the perpetrator of one of the largest Ponzi schemes in history. One sentence in the book caught my attention as I pondered this dilemma facing investors. Markoplos states, “By offering unbelievably steady returns with almost no volatility, he [Madoff] was providing the holy grail of investments products.” Wow – in a nutshell Markopolos has answered the question of what is the “perfect” investment” – namely, it doesn’t exist! Furthermore, claiming it does is likely a fraud. If investor A needs liquidity – he should place his money in savings accounts, money-market funds or Cashable GICs. The return is low (currently around 1-2%), and the money will not go up in value, but it will also not go down in value, and it is always accessible. If investor B has sufficient liquidity, but cannot tolerate fluctuations in the value of her investments and she wants a higher rate than that offered by short-term products, she can lock in her money for 1, 2, 3, 4 or 5 years (currently between 2-4%). Finally, if investor C has sufficient liquidity, is seeking long-term capital appreciation above the rate of inflation and can tolerate volatility, then investing in the stock markets (public businesses) is a great option, as historically they have provided returns of 8-10%, with the obvious caveat that those numbers are an average rate of return, over long-periods of time, including the great, the rotten and the mediocre years.

The war in Iran may be a source of volatility longer than many had initially thought. This is as good a time as any for investors to assess their tolerance for volatility and to determine whether their hard-earned money is in fact invested in accordance with their needs. Over the years, I have frequently mentioned that I have never got into “trouble” with the stock markets and in response I see the eyebrows start to rise in astonishment. How can that be? Are you telling me that in almost 30 years of advising and after so many bull and bear markets, I can be so bold as to claim that I never got into trouble with the stock market? The answer is a resounding yes, and the reason is simple – I NEVER put clients’ hard-earned money which is needed for short-term liquidity needs into the stock market, which, by definition, is a long-term investment vehicle. The other side of staying out of trouble is that I don’t sell and jump “out of the market” every time the market gets volatile. Why not? Again, the answer is simple, I have yet to find a reliable method for both getting into and out of the market at exactly the right time. Only once in my whole career have I personally observed someone getting out of the market and selling all of their investments at the right time (just before the Covid panic hit in February 2020), but even then the investor missed out on getting back into the market at the right time. If anyone out there reading this newsletter knows of a reliable system for doing both on a regular basis, please contact me at your earliest convenience. Until that time, as the marketing slogan states, earning great long-term returns results from “time in the market, NOT timing the market.” Following this approach starts with owning good quality investments, ignoring the day-to-day bumps and grinds and, of course, having lots of patience.

Bottom line

This war in the Middle East is not the first war and unfortunately it is likely not the last. Will the war end? Certainly. Will things go back to “normal” afterwards? More than likely. Is it worthwhile jumping out to avoid the short-term volatility until things “settle down?” Almost never. The closest investors can get to making a "perfect" investment, is to carefully align their investing decisions with their investing needs (liquidity vs. safety vs. long-term growth). If you are still feeling stressed and want to review your portfolio to ensure it is truly aligned with your needs - contact us and let’s schedule a time to chat!

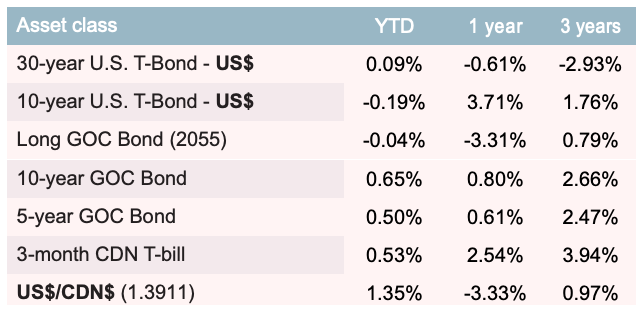

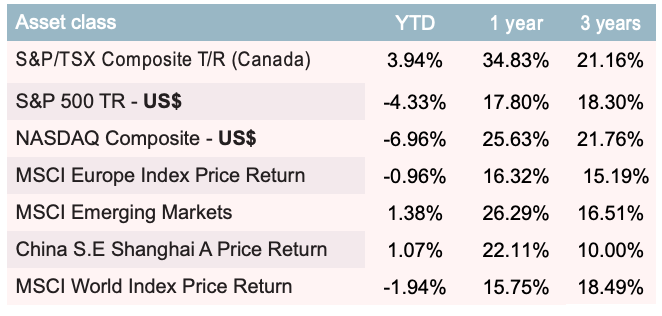

Global benchmarks

As of March 31, 2026 (Canadian $ Returns – except where noted)

Source: RBC Capital Markets Quantitative Research