Beware the mystique of illusion!

The increasingly popular world of “Private Equity” and “Private Credit” investing can also lend itself to the world of illusion. Investors seeking good returns should look for an investment with actual merits.

This article addresses the Illusion of safety and what it means for your investments.

The increasingly popular world of “Private Equity” and “Private Credit” investing can also lend itself to the world of illusion. Investors seeking good returns should look for an investment with actual merits.

This article addresses the Illusion of safety and what it means for your investments.

Mark Krygier

Senior Portfolio Manager & Wealth Advisor

May 4, 2026

Ho hum, another month and another attempted assassination on the life of the American President. I recently watched a podcast which listed six attempted assassinations of President Trump – starting with an attempted forklift attack on his passing vehicle in September 2017 up to the most recent attempt in April 2026 at the annual White House Correspondents’ Association dinner – an unprecedented record in American history. While Presidents Lincoln (1865), McKinley (1901) and Kennedy (1963) were assassinated, no other President has faced as many attempts on his life. Violent rhetoric has unfortunately become commonplace in America and throughout the world, a sad reflection on a so-called “advanced” civilization. This decline in moral clarity, as to the acceptance of violence, can perhaps be illustrated best by the voices coming out of Hollywood – the epitome of American culture. Literally two days before the most recent attempt on the President’s life, an American comedian, hosting a “mock” White House Correspondents’ Association dinner, made a joke about the sitting First Lady having the “glow of an expecting widow.” In the context of the numerous attempts at murder, most can agree such language is tasteless at best. In contrast, in March 1981, following the attempted assassination of President Ronald Reagan, Hollywood postponed its scheduled “Oscars” awards ceremony to the following day. When it did open the following day, famed media personality Johnny Carson, the MC of the event that evening, stated that the entertainment adage of “the show must go on” did not apply the previous day, considering the terrible act of violence. When he then announced the good news that the President was recovering, the audience applauded enthusiastically. Oh, how times have changed…

Hollywood is based on the creation of illusion, and woe is to the person believing that anything coming out of Hollywood has any bearing on reality. In the financial world, there can also be an aspect of illusion as tantalizing as a Hollywood thriller. The reason why illusion works is that it preys on emotions – and some of the strongest emotions are fear and greed. When it comes to Hollywood, the art of illusion creates role models only in the imagination. In finance, the art of illusion helps investors cope with their fear of losing their hard-earned capital and it also preys on their emotion of greed when it comes to making money. Consider that even something as mundane and “risk-free” as a GIC or a CD (Guaranteed Investment Certificate in Canada and Certificate of Deposit in the U.S.) contains an element of illusion. What may you ask can be illusory about a GIC/CD? The answer relates to the liquidity risk and the lack of transparency inherent in such instruments. When an investor purchases a 5-year GIC/CD, they are “guaranteed” a rate of return over 5 years, and their capital is guaranteed at term end. So, what’s the catch? Well, for anyone evaluating their rates of return, the daily “value” of that investment is artificially presented as being equal to the ending guaranteed value, throughout those 5 years. Those who purchase “bonds” and other “fixed income” instruments know that the price of the bonds fluctuates every day. GICs/CDs also fluctuate in value every day, but since there is no readily accessible market for them, and since they cannot be liquidated until the term matures, investors are comforted into believing the illusion that the current value is the same as the maturity value.

The increasingly popular world of “Private Equity” and “Private Credit” investing can also lend itself to the world of illusion. Investors seeking good returns should look for an investment with actual merits. There is no intrinsic reason why a “publicly” traded investment should perform better or worse than one that is “private” (i.e. not traded on the public stock markets). Public markets provide access to purchase or sell an investment in an efficient and cost-effective manner. Anyone can buy shares in Royal Bank, Coca Cola or Nike, as publicly traded investments. Not everyone can buy shares in a private company that may be just as good quality as these three companies. However, some investors seeking to generate “higher” or more “risk-averse” returns have turned to the world of Private Equity and Credit, which are popular amongst large institutional investors. The “catch” or the illusion of private equity can however resemble that of the GICs – limited liquidity and limited transparency as to the value of the investments on any given day. In contrast with a portfolio of publicly traded securities, in which the market values are literally available on-line 24/7, once an investor has placed money in a “Private” investment, one often has no idea how that investment is performing and one has limited access to that money until a “liquidity event” occurs, whereby the invested money with some return is (hopefully) returned to the investor. Author and investment newsletter writer Jared Dillian has stated that the biggest advantage of “private equity” is that investors truly view their investments as “long-term” holdings, which means they are less likely to panic in times of market turmoil. I still remember the 40-year stock market veteran, who instructed me in late March 2020 to sell all his investments, two days before the market bottom of the Covid induced downturn, as he made clear to me, “I can’t take it anymore.”

Investors in private equity may be less likely to panic based on news headlines, perhaps because it may not be clear what their investments are worth, and even if the values are known, there may be limited opportunities to sell the investments on-demand. The “illusion” of private equity may also hide layers of additional fees which can limit the ultimate return to the investors. Recently, I have been hearing from investors in private equity, private real estate deals and private mortgage funds, who are unable to get their money out and who are questioning the merit of having invested in such illiquid and non-transparent investments. Clearly, being “private” does not automatically improve the intrinsic merits of the underlying investment.

Bottom line

Hollywood reflects American society for better or for worse. Investors need to decide if they prefer clarity, transparency and liquidity, or the comfort of being unaware of the value of their investments at any given time and not having access to liquidity from their investments whenever they choose. Ultimately, the success or failure of any given investment, public or private, ought to result from its actual quality. The tug of war between facing reality vs. chasing illusions motivated by fear or greed is an ongoing battle. To better understand the contents of your portfolio, contact us and let’s schedule a time to chat!

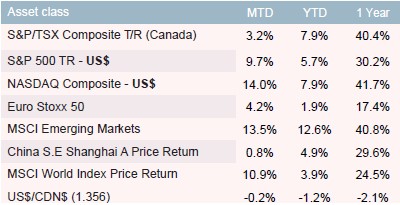

Global benchmarks

As of April 30, 2026 (Canadian $ Returns – except where noted)

Source: Bloomberg

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © 2026 RBC Dominion Securities Inc. All rights reserved.