Mark Krygier

Senior Portfolio Manager & Wealth Advisor

January 31, 2026

One thing you have to say about President Trump, love him or hate him, is that he certainly knows how to stay in the limelight! I do not recall a politician generating such a strong reaction from people, and perhaps deservedly so, as his antics are certainly not what we have come to expect of world leaders. In the past month alone, he has had the leader of a foreign nation, albeit a corrupt leader who abused his own populace to enrich himself and his cronies, kidnapped and brought to the U.S. to stand trial on criminal charges for trafficking in drugs, amongst other infractions. He threatened tariffs on the European Union countries if he was not allowed to buy a foreign territory – Greenland – only to backtrack, drop the tariff threat and claim a deal is in the works to get access to materials from Greenland, and for more space on which to plant more U.S. troops, to ward off potential military threats from Russia and China. His promise to get the last of the Israeli hostages from the October 7th massacre by Hamas terrorists returned to Israel was fulfilled, including both the living and the murdered ones, while he invited several global leaders to join an international “Board of Peace” for managing Gaza in the future, including Canada, only to revoke the invitation to Canada after our PM made remarks that the President did not like. He sent troops and warships to the Middle East to be positioned to threaten the brutal dictatorial Iranian leadership, even while it murders untold numbers of their own people in the streets. Back on the domestic front, some are questioning whether civil war is the future of the U.S., as we see daily news reports of violent protests against Federal immigration officials trying to arrest and deport illegal aliens across America. While all of this makes for dramatic headlines, it is no wonder the stock markets have been so volatile or that the “risk-off” trade of gold and other precious metals has performed so well!

On a completely different note, I am beginning to wonder if the greatest threat facing us today is the attitude of complacency. I have heard it lately from several amateur stock market investors or from those who have only witnessed stock markets climbing higher, literally expressed as, “what could go wrong at this point?” I hear it from pre-retirees that are used to the cash flow they are receiving from mature businesses or their careers in the peak earning years, as they have not yet had to draw income from their investment portfolio (consider that it can take $4 million of savings to generate the equivalent of $200,000 in pretax income, based on a 5% cash yield on one’s investments, something not readily available from “safe” instruments like GICs/CDs). Until very recently, I heard it nonstop from real estate investors, as in most major cities housing prices were climbing year after year for the better part of three decades (with a little blip during the Great Financial Crisis of ’07-09). I even hear this attitude of complacency from people in their 50s, 60s, 70s and sometimes 80s, who still don’t have properly drawn up wills or powers of attorney for property and personal care – as up until now, they have not needed such documents…

Another aspect of complacency which I have seen is the approach many people have when it comes to their retirement years. Most people plan for their career growth, whether it is higher education required, or gaining the necessary practical skills to move up the proverbial corporate ladder. Others have family plans, whether it’s where they want to live or what type of lifestyle they are seeking. However, when it comes to planning for retirement or the “post-working” years, how many people do you know that have formulated “a plan”? Do most people consider how much money they will need to have set aside by the time they retire to maintain their lifestyle? When was the last time you heard of someone discussing how they will keep themselves motivated to get up each day once the grind of 9-5 is no longer on the agenda? I hear plenty of, “I’ll take some time to think about what I want to do,” or “I am looking forward to catching up on my reading, or to playing more golf and travelling”, but without any thought about how often one can read, play golf or tennis, or how many days in the year will realistically be spent travelling. Even if one travels two months at a time, a couple of times a year – something most in practice will not do – that still leaves many months in a year with no plans to do anything at all. In almost 30 years of managing investments for clients, through many ups and downs in the market, the only people I have seen really panic during times of market volatility were retirees spending their days reading panicky news headlines intended to generate high emotion in order to sell more ads, instead of doing what they ought to be doing – enjoying themselves and reaping the fruits of their years of hard labour to save for retirement. It is not just about having the money, it’s about what you do with it and how you will spend your time – that also requires planning!

Bottom line

So far in 2026, there has a been a lot of dramatic news events in a very short amount of time. Precious metals like gold and silver are suddenly the talk of the town, after being shunned by investors for most of the previous several decades. Investors need to be cautious about jumping into investments which have increased dramatically in a short period, as “what goes up…” Finally, we all need to make sure the word “complacency” is not in our vocabulary. Taking off time to relax and rejuvenate is essential for one’s physical and mental health, but it is not a plan for long-term well-being. Contact us if you have any concerns about the markets, your current state of planning for your retirement, or any other wealth planning needs, and stay warm!

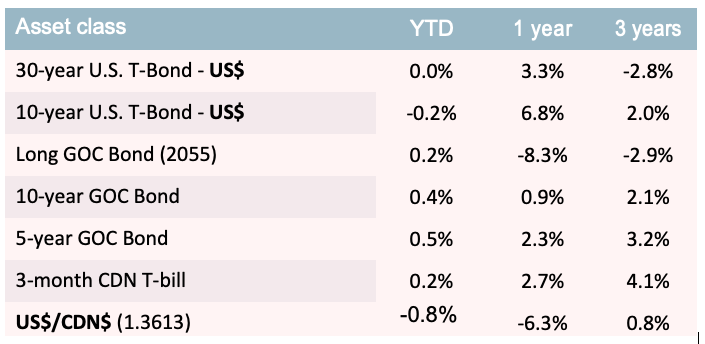

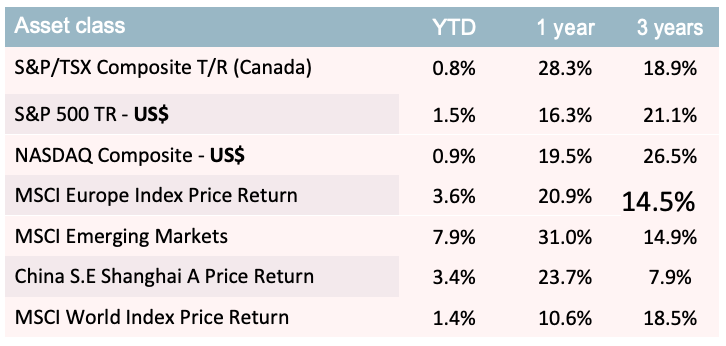

Global benchmarks

As of January 31, 2026 (Canadian $ Returns – except where noted)

Source: RBC Capital Markets Quantitative Research