China's Economy: 2026 Performance and Outlook

China delivered solid economic growth in the first quarter. Investors now anticipate a broadening earnings recovery across different sectors. However, the Middle East conflict and the global AI spending boom have altered the economic trajectory that many anticipated at the start of the year.

China delivered solid economic growth in the first quarter. Investors now anticipate a broadening earnings recovery across different sectors. However, the Middle East conflict and the global AI spending boom have altered the economic trajectory that many anticipated at the start of the year.

Michael Capobianco

June 4, 2026

Today we’ll evaluate China’s current economic performance and the equity market outlook for the remainder of 2026.

China delivered solid economic growth in the first quarter. Investors now anticipate a broadening earnings recovery across different sectors.

However, the Middle East conflict and the global AI spending boom have altered the economic trajectory that many anticipated at the start of the year.

How is the Chinese economy handling the energy shock?

Energy experts in China note that the country is relatively well-insulated from direct energy price shocks due to its “energy security” policy. The country diversifies its crude oil sources across different suppliers, with no single supplier accounting for more than 20 % of China’s total oil imports.

The country’s energy consumption is also more diversified and less expensive than most countries, with coal accounting for nearly half and the remainder distributed across fossil fuels and renewables, including hydroelectric, solar, wind, and nuclear power.

Additionally, China strategically accumulates oil reserves during periods of low prices.

China’s total oil reserves are estimated by analysts at 1.3–1.4 billion barrels, but the actual number could be 30–40 % higher, which is able to cover more than one year of oil consumption at the current drawdown (consumption) rate.

This gives policymakers flexibility to respond to prolonged energy disruptions.

China’s diversified energy mix and inventory buffers have delayed the impact of the Strait of Hormuz disruption. However, the impact of the Middle East conflict became visible in some April economic data.

Industrial activities have been affected the most, with production of refined petroleum products and chemicals showing the largest sequential monthly declines.

China’s producer inflation is likely to continue to rise in the coming months, albeit from a lower base than many countries. Companies will be exposed to both rising input costs and slowing demand as the conflict drags on.

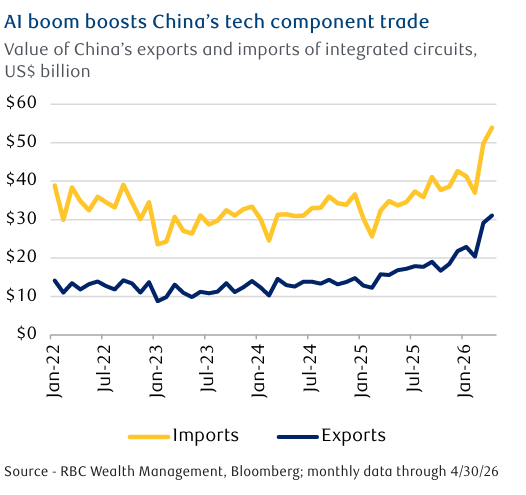

AI exports have emerged as a new export driver this year.

China’s total exports climbed to record levels in April, to around US$350 billion monthly in seasonally adjusted terms, a 14 % year-over-year increase.

Roughly half of this expansion stems from goods supporting global AI infrastructure development.

However, China occupies a downstream position in the AI value chain.

Unlike South Korea and Taiwan, which produce cutting-edge semiconductors, this positioning requires China to import substantial quantities of AI related components for domestic use or final assembly.

Consequently, China’s imports surged alongside exports.

This simultaneous rise in both flows means the AI boom has generated minimal net impact on China’s trade surplus. This differs sharply with other sectors, such as solar panel and electric vehicle, where most of the supply chain operates within China’s borders.

There are two ways to consider the implications:

- Elevated AI imports could create cost pressures on corporates and even the whole economy. If memory chip prices rise further, manufacturers’ profit margins could suffer. Net exports could become a modest drag on China’s economic growth, even as gross exports remain robust.

- Because the AI boom is not inflating China’s trade surplus, it positions China more favorably in international trade relations, potentially alleviating concerns among trading partners about mounting surpluses.

These two factors, along with whether AI spending sustains its momentum and the duration of the Middle East conflict, will largely affect China’s trade outlook for the remainder of the year.

Was the Trump-Xi meeting a non-event ?

Despite initial low expectations, many expressed disappointment about the outcome due to the absence of a joint statement and comprehensive trade agreement, the two sides’ readouts also revealed divergent priorities.

China’s statement emphasized building a stable and sustainable trade relationship, while the U.S. focused on increasing Chinese purchases of American goods, reopening the Strait of Hormuz, and denuclearizing North Korea.

Nevertheless, the meeting produced tangible progress. The two countries agreed to establish a U.S.-China Board of Trade and a U.S.-China Board of Investment to manage daily bilateral trade and investment matters.

These bodies will aim to foster longer-term solutions for more predictable and stable trade and investment relationships.

While fundamental differences and structural tensions persist, the summit’s outcomes appear pragmatic. Trump’s invitation for President Xi Jinping to visit the U.S. in the autumn suggests to us a reduced near term risk of further escalation before that visit.

The Middle East crisis has introduced uncertainties for China’s economic recovery and postponed the anticipated broader corporate earnings recovery. At the index level, Chinese equities have demonstrated resilience since the conflict began. However, year-to-date performance remains modest relative to major peers, particularly regional peers such as South Korea and Taiwan.

The performance partly reflects index composition. The Consumer Discretionary and Financials sectors represent 26 % and 19 % of MSCI China Index weight, respectively, while technology hardware companies are underrepresented compared to other major markets, limiting the index’s capture of Information Technology sector strength.

Given surging global demand for AI-enabling products and the accelerating push toward electrification, China’s technology sector, including companies in the AI, humanoid robotics, and lithium batteries supply chains, are well-positioned to capitalize on the trend and appear undervalued.

It would be wise to maintain a Market Weight position in Chinese equities within global portfolios. This allocation provides resilience should the Middle East conflict escalate, while positioning investors to capture upside potential from the AI growth story

If you have any questions or comments, please feel free to let me know.

Many Thanks,