Conflicting Objectives Of The U.S. Federal Reserve

While most central banks focus on keeping inflation near a given target, the Fed is charged with maximizing employment consistent with stable prices. Keeping long-term interest rates moderate, usually goes unmentioned, but remains a key consideration.

While most central banks focus on keeping inflation near a given target, the Fed is charged with maximizing employment consistent with stable prices. Keeping long-term interest rates moderate, usually goes unmentioned, but remains a key consideration.

Michael Capobianco

June 11, 2026

While the U.S. Federal Reserve is thought to have complete freedom in setting policy, wealth effects and massive deficits limit its flexibility more than many realize.

While most central banks focus on keeping inflation near a given target, the Fed is charged with maximizing employment consistent with stable prices. Keeping long-term interest rates moderate, usually goes unmentioned, but remains a key consideration.

To achieve its mandate, the Fed is often viewed as having complete freedom in setting monetary policy. In particular, the macroeconomic importance of asset prices and the harsh realities of the federal government’s budget deficit can limit the Fed’s overall autonomy.

A consistent refrain is that asset prices are not a factor in monetary policy setting. While the Fed may not be targeting a given equity level, it will be cognizant of how stock prices are filtering into GDP growth and labor demand.

The key link is household consumption, which accounts for roughly 70 % of U.S. GDP.

Since production demands labor, the Fed—with its mandate to maximize employment—keeps a wider eye on spending trends. Growth demanded workers, and labor shortages led to higher wages, which in turn led to robust household spending.

The cycle continued until it created inflation, and the Fed stepped in to raise lending rates.

While asset prices tended to rise during these periods of strong growth, the causality largely flowed from strong labor demand to consumption to GDP growth to equity prices.

The situation today is distinct.

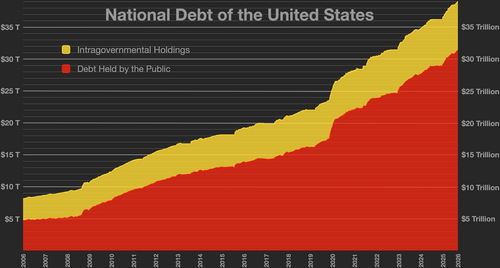

Source: The United States Treasury / Fiscal Data / Wikipedia

While consumption still drives the U.S. economy, the driver of gains is increasingly coming from the top 10 % of households by income, a sector that now accounts for a third of all economic activity in the U.S. These households tend to adjust spending in response to changes in their net worth, which is largely a result of fluctuations in stock prices.

A significant fall in stock prices, therefore, is likely to have real-world impacts on consumption, which in turn will hit GDP growth and eventually labor demand. The Fed must consider how falling stocks filter through the economy.

The U.S. is growing its debt at a pace that is well above the norm for an economic expansion—nearly 6 % of GDP per year. In addition, the U.S. government has been increasing its reliance on short-term funding vs. longer maturities—more than 20 % of federal debt matures in less than one year.

All of this comes against the backdrop of a total U.S. debt burden that is larger than the U.S. economy.

The 2 main reasons the Fed must be aware of fiscal policy when thinking about rates:

- Shorter Maturity Bonds Are Sensitive To Fed Action

Tightening policy implies a higher probability that the U.S. government must dedicate more resources to paying interest and less to tax cuts and spending priorities. This pressures growth downward as it moves funds away from high-powered government programs to T-bill investors, conservative style investors

- The U.S. Debt Burden Is Large Inflation Lowers The Cost of Repayment.

While setting rates to facilitate government deficits sounds alarming, higher inflation to help slow the pain of fiscal normalization may not be ruled out under the current mandate.

Historically, home prices were the key catalyst linking asset prices and consumption—this was a broad-based boost to demand, but it relied on cash out mortgage refinancing. After the post-COVID wave of low-rate mortgages, this channel is effectively cut off. As a result, the importance of equity prices on consumption has risen.

While the U.S. debt has been growing steadily for years, both the pace of accumulation and the current magnitude make it a more pressing concern.

The central bank is essentially creating a one-way ratchet on asset price moves:

- When asset prices go up, the Fed dismisses those criticisms based on the efficient markets’ hypothesis and the difficulty of identifying overvaluation in real time.

- When a bubble bursts or stocks falter, the Fed is quick to rush in to cushion the selloff.

If markets are efficient on the way up, why are they inefficient on the way down?

If the secondary impact of falling asset prices is a justification for rate cuts, why do we fail to consider the whole range of secondary impacts of rising asset prices?

It is both difficult and arguably dangerous for central bankers to be sitting in judgment on where the “correct” price of future cash flows should lie. Moreover, today’s equity market is not in any way stretched to the point of the pre-Global Financial Crisis period or the internet run-up of the late 1990s.

The Fed cannot compel the various branches of government to curb spending. In practical terms, investors need to think about the constraints on the Fed’s decision making when evaluating likely future policy moves.

In reality, the central bank may find its hands tied by the dual constraints of wealth effect spending and an ever-rising U.S. debt

If you have any questions or comments, please feel free to let me know.

Many Thanks,