Michael Capobianco

Investment Advisor

March 22, 2026

War continues to rage on in the Middle East, with no clear end in sight.

Volatility has and will continue to be the order of the day as market direction is driven primarily by headlines. Today is no exception, with White House and Iranian officials at odds over the extent, or even the existence of any cease fire talks.

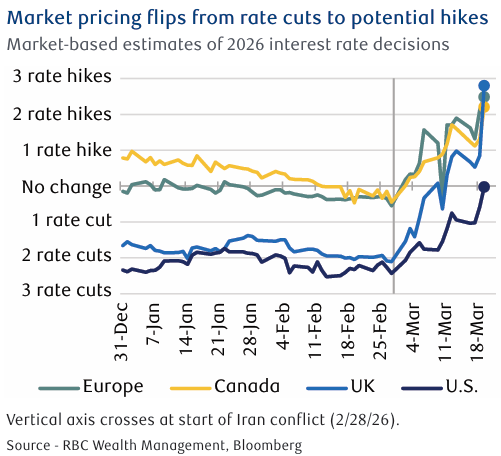

The FOMC, BoC, BoE, ECB, RBA, and BoJ all held policy meetings last week amid an uncertain geopolitical backdrop. Investors believe that global central bank response may need to be tighter policy rates.

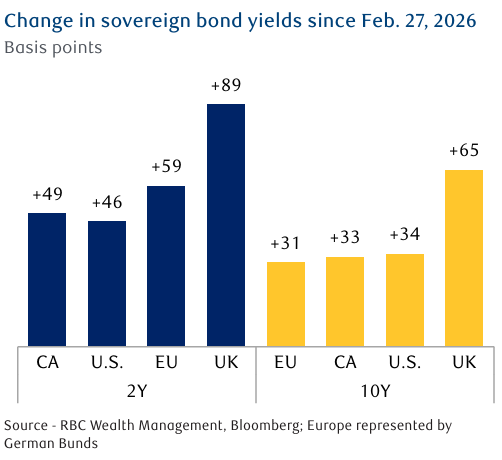

Sharply higher yields and energy prices are the current driver of global markets. As a result, the focus of central bankers this week was on the impact of higher energy prices on inflation and the potential for a negative impact on economic activity.

Markets appear to believe that.

The U.S. Federal Reserve has a dual mandate of price stability and maximum employment. The Bank of England (BoE) was the most hawkish this week, stating that policymakers “stand ready to act” on inflation, which has had a material impact on global bond markets this week.

Markets are now pricing slightly more than two 0.25% point rate hikes by the end of the year. Similar expectations In the U.S., The Fed’s Federal Open Market Committee (FOMC), previously projected to cut twice this year, markets now see it keeping rates unchanged.

RBC Capital Markets, LLC Global Head of Commodity Strategy Helima Croft recently laid out a couple of scenarios for oil prices:

- Should the conflict persist for three to four weeks, Brent oil prices could exceed the $128/ barrel peak level from 2022 in the aftermath of Russia’s invasion of Ukraine.

- Should the war expand and extend for several more months, then oil prices could eclipse the 2008 record high of $146/barrel.

- If oil prices average $100/barrel this year it would add about 0.75% to headline inflation, with annual rates peaking this year at 3.00 % and 3.50 % for Canada and the U.S., respectively.

For central banks, the typical playbook is to look through energy price shocks, particularly short ones, as the feed through to core inflation (excluding food and energy) is generally minimal. However, if sustained, higher energy prices will eventually impact costs throughout corporate supply chains, to say nothing of the potential risks of higher business and consumer inflation expectations— risks that may be amplified in this episode given the inflationary environment that has persisted for nearly five years now.

The FOMC’s first update of the year to its economic and interest rate projections was somewhat confusing:

- Policymakers, on average, upgraded both the inflation and growth outlooks while leaving the unemployment outlook unchanged—but still projected one rate cut this year.

- Chair Jerome Powell noted in his press conference, if ever there was a quarter to skip the forecasts given all the uncertainty, this was it.

It was perhaps Powell’s declaration that he plans to stay on as Fed chair until the Department of Justice’s investigation into his testimony regarding the Fed’s headquarters renovation is “well and truly over,”

The subsequent rise in Treasury yields perhaps implies that markets believe Powell is both more likely to stay on for at least somewhat longer, and to act as a significant counterbalance against political pressure to lower interest rates absent the requisite economic justification.

Our base case in our 2026 outlook was already that the Fed would keep rates on hold this year. We see no reason to change that view but see the bar for rate hikes as exceptionally high.

If you have any questions or comments, please feel free to let me know.