Michael Capobianco

June 18, 2026

Though much of this week’s meeting focused on potential changes to how the Fed operates, the initial proposals made by new Federal Reserve Chairman Kevin Warsh are largely superficial. The bigger surprise came in a foundational shift in where the broader policymaking committee sees rates heading—and that is potentially higher.

Warsh has made it no secret that he is not a fan of forward guidance or excessive Fed communications. The Fed’s output under its chairs has expanded from essentially nothing during the Alan Greenspan era in the early 1990s, to the first quarterly press conferences under Ben Bernanke in 2007 and later the Fed’s document containing economic and interest rate projections.

By Bloomberg’s estimates, that culminated in over 75,000 words published in 2025 via the Fed’s various publications, compared to barely 300 in 1995.

For the past 25 years or so, the results of the policy vote, both in favor and against, have been published in the statement.

But at the top of this meeting’s policy statement, this appeared: “The Federal Open Market Committee approved the following statement for release by a 12‑0 vote”.

While that is indeed a vote result, prior statements referenced the vote tally for or against monetary policy action. The distinction is significant.

One risk many market participants have flagged was the potential for the Fed chair to cast a dissenting vote on policy decisions, something without real precedent. For example, if a simple majority of the 12-person voting committee votes to raise rates, there would be less headline risk on decision days, at least in the immediate aftermath.

Regardless, it appears that Warsh truly wants to keep Fed business behind closed doors. While not a major issue for markets, it could inject some volatility amid the added uncertainty.

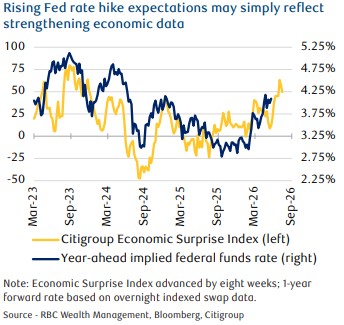

The big surprise at this week’s meeting, was the sheer number of policymakers favouring rate hikes this year with 9 of the 18 submissions seeing at least one hike

While much has been made about the Middle East conflict’s impact on oil prices, inflation, and the related shift in the market’s pricing of rate hikes from central banks, what was missing was the interest rate outlook.

Markets now see a fundamental case for rate hikes, especially as inflation remains above the Fed’s 2 % target and at risk of running even higher if the economy runs hotter.

Warsh announced five task forces on:

- Communications

- The Fed’s Balance Sheet

- Data Sources

- Productivity & Jobs

- Inflation

He often cited these task forces when asked specific questions and though they featured heavily during his press conference as a key initiative. Historically, the Fed is bad at forecasting rates. Markets are bad at forecasting rates. Everyone is pretty bad at forecasting rates !

The Fed meeting sparked significant market swings, with the policy-expectations-sensitive 2-year Treasury yield seeing large moves along with stock market declines—but both have already been unwound to varying degrees.

Though uncertainty remains high with respect to what comes next, the bar for rate hikes has certainly been lowered. Though he was likely brought in by President Donald Trump to lead the charge toward lower interest rates, Warsh may try to keep hikes off the table, but his reputation has always been as an inflation hawk.

Therefore, while he might not vote to raise rates, he likely won’t preempt the voting committee’s desired direction. During his press conference, he certainly didn’t stand in the way of the rate hike sentiment that appears to be percolating amongst the committee.

Ultimately, Warsh could see near-term rate hikes as necessary to finally get inflation back down to the two percent target. On top of that, the math next year should work in favor of lower inflation readings as the data will “lap” current high inflation numbers north of 4 %.

Our current forecast has annual headline Consumer Price Index inflation at just 1.5 % in Q2 of next year. At that point, he could claim the inflation victory that had eluded Powell to this point.

Will this ultimately portend to an AI-induced productivity boom that fuels strong economic growth and labor market strength, leading to lower inflationary pressures?

We shall see, but this week could have marked a bigger— or at least earlier—shake-up at the Fed than many had been prepared for.

If you have any questions or comments, please feel free to let me know.

Many Thanks