Nick Milau

April 16, 2026

Weekly Wrap

Stock markets recovered all week long and are now sitting above their highs in February leading me to facetiously wonder; has something really great happened since the last weekend of February? This is not a risk off or risk on market…it is a risk dumb market. Canadian stock markets gained 1.5% as did EU markets. US stocks rode a tech recovery to a 4.5% gain this week. Investors seemed confident that Trump and Iran will negotiate a deal while Israel and Lebanon announced a ceasefire this morning. Like most people I am pleased to hear this news but a lack of trust in the leaders involved leaves me highly skeptical. Oil prices plummeted 15% while the Loonie gained over a penny against the US Buck. Interest rates drifted lower, a much less dramatic reaction to the détente as bond investors seem more risk aware than equity investors. While Trump has fallen in the polls, Mark Carney has officially secured a majority in Canada making it smoother for him to advance his economic agenda. Meanwhile economic data released this week continued to paint a picture of a softening North American economy; manufacturing is slowing, consumer sentiment is falling and there is no relief in sight for Canadian real estate.

Market Insights

Fear not the cries of sustained inflationary pressures. Following a sustained period of above average inflation since 2022, concerns about the recent jump in energy prices leading to another inflationary spiral seem overdone. With that said, concerns about a longer term dent to economic growth may be worth consideration. Why do we believe that inflation will not be as bad this time around? First, labor markets are no longer as tight as they were then. Wage growth has moderated meaningfully from its 2022 peak, alongside easing in other measures including the US employment cost index and job availability. This points to less risk of a wage-price feedback loop taking hold (where consumers anticipate higher prices and therefore demand wage increases, that then fuel further price increases in a circular manner). From the perspective of a wage earner, however, higher energy prices without a commensurate rise in wages is a concern and this could negatively impact spending. Second, interest rates are not as low as they were in 2022 and thus not adding to excessive spending. Third, household balance sheets have normalized. Savings rates in both the US and Euro area have retraced from the elevated levels seen during the pandemic, suggesting less pent-up and price insensitive demand to amplify price increases (i.e. revenge travel is done). Finally, growth momentum is softer. While activity remains positive, it is notably weaker than at the start of 2022, reducing the likelihood that higher energy costs translate into broad-based inflation. Inflation is a concern when it increases and there is no doubt recent energy price increases have raised inflation thus far in 2026. But inflation only becomes a major concern when it continues to spiral. The recent jump in energy prices is likely to be more one time in nature; it has moved up and while it may jump around and stay elevated for a while, there is no reason to believe that it will continually rise and filter through to inflation. In fact, it is likely to be a deflationary contributor in the short term (crude oil has dropped from $110/barrel to $81 this morning). Meanwhile, data from this week showed that non-energy related inflationary pressures have softened a touch (expect this to continue as consumers cut demand in order to pay their higher energy bills). But…the cost of living has gone up, and if it remains up this is another dent in the ability for the average consumer to consume.

Canada narrows the wealth gap while Americans divisions grow K-shaped. All income groups in Canada have improved their net wealth since 2019 according to RBC Economics. Despite economic headwinds, appreciation in home prices (up 25% nationally since 2019, despite recent pullback) and growth in non-pension financial assets (such as equity market profits) drove wealth gains, according to a new report by RBC Economics. Surprisingly, these gains have favoured lower-income groups, leading to a sizeable narrowing of the wealth gap, with the ratio comparing the wealth of the top quintile to the bottom two compressed from 3.2 times in 2019 to 2.1 times in 2024. This is not the case in the US however. With the recent jump in energy prices, Americans now expect inflation to rise 4.8% annually (a forecast already reshaping spending behavior across the country). Beneath these aggregate numbers lies a starker reality: the US economy is increasingly characterized by divergent outcomes across income groups. This is a phenomenon termed the "K-shaped economy ." Higher-income households, bolstered by income-generating assets, continue to thrive, while middle- and lower-income Americans struggle under mounting daily costs. Band of America Research confirms this divide: after 13 consecutive quarters of decline through 2025, luxury spending has surged back to life. Since Q4 2025, luxury consumption has accelerated dramatically, surging 12% year-over-year through March 2026 (almost entirely driven by higher-income households). JPMorgan research shows US consumer cash balances rising across demographics over the past year as households rebuild spending capacity. This finding is notably at odds with prevailing research suggesting US consumers have depleted their pandemic-era savings and face financial strain. Higher-income households are recovering faster and stronger than others. Yet this masks a troubling reality: lower-income households are actually worse off on an inflation-adjusted basis, as their modest savings gains fail to keep pace with the 4.8% annual price growth they expect, according to Bloomberg.

Portfolio Update

This week we decided to sell our shares of Telus. For decades Telus has been a stable, dividend paying stalwart for Canadian portfolios but with growing competition in the telecom sector leading to tighter and tighter margins for telecom operators, the outlook was slanted to the downside. All of the Telecom businesses have large amounts of debt and with Telus’ dividend now sitting at 10% and their debt ratios getting weaker, the odds of the company opting for a dividend cut to preserve their credit rating are growing. I do not foresee an imminent demise for Canadian telecom companies as a whole, but I see no upside catalysts. The need to preserve credit ratings at the expenses of shareholders leads me to think that if we wish to have any telecom exposure at all, it’s best done with telecom bonds and other types of fixed income rather than equities. This is a growing trend intoday’s market: many areas of the stock market offer return outlooks that are similar to that of their fixed income (i.e. Telus bonds pay a guaranteed 5%+ yield). For the time being we will be keeping the cash in short term interest bearing investments. The investment environment continues to be far too complacent given elevated valuations combined with a multitude of challenges and, as such, this further reduction in equity exposure makes sense.

Planning On

The Prescribed Rate

The CRA has announced that the prescribed rate on family loans will remain at 3% for the second quarter of 2026, marking the fourth consecutive quarter at this rate. Simultaneously, the interest rate on overdue taxes stays at 7% (always 4 percentage points higher than the prescribed rate).

This 3% rate represents a significant opportunity for tax planning—it’s the lowest level since late 2022. The prescribed rate is calculated from the average of three-month Treasury bills in the first month of each preceding quarter, rounded up. After hitting 6% in early 2024, rates have been declining and have now stabilized at this lower level for several quarters, creating favorable conditions for strategic financial planning such as a spousal loan.

A spousal loan strategy leverages the prescribed rate to enable income splitting between spouses. It works when there is a sizeable difference in incomes. Here’s how it works:

- The mechanism: The higher income earning spouse loans money to the other at the prescribed rate (currently 3%), with formal loan documentation required.

- Tax benefit: The borrowing spouse can invest the loaned funds and generate income. While they must pay prescribed-rate interest to their spouse, the investment income is taxed in their hands (typically at a lower marginal rate if they earn less). The interest income is generally available as a tax-deduction.

- Family trust option: Alternatively, loans can be made to a family trust, which then distributes income to lower-income family members, maximizing overall tax efficiency.

- Current advantage: At 3%, this strategy is particularly attractive, as lower prescribed rates enhance the tax-planning opportunity by reducing the interest cost while allowing income generation in lower-bracket hands.

For those high-income earners with sole owner non-registered accounts, this could be a very effective tax-reduction strategy.

This information is not intended to provide legal, tax, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified lawyer or accountant, as applicable, before acting on any of the information.

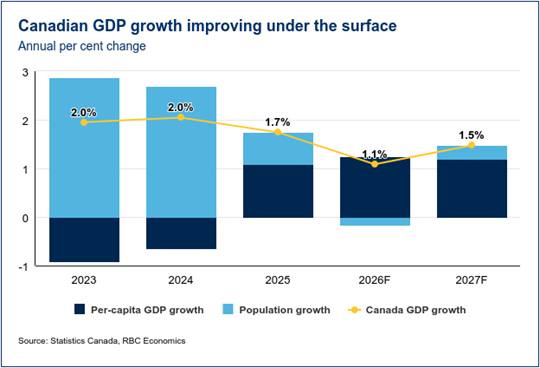

Charts of the Week

Spare Time Updates

Tax Tips: How Taxpayers can Protect their Data this Season

Tax season is a busy time for cyber crime. With so much high-value data moving between taxpayers, accountants and government systems. A few smart data protection habits can go a long way toward keeping your tax return out of the wrong hands.

12 Fascinating Facts About the Spring Equinox in 2026

These spring facts will brighten your day and make you fall in love with the season all over again.

Feel free to pass on this email to anyone you think would benefit from its information or see some value in it.

Thank you very much for reading through our commentary. Feedback is welcome!

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. â / ™ Trademark(s) of Royal Bank of Canada. Used under license. © RBC Dominion Securities Inc. 2026. All rights reserved. This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. This publication is for information purposes only. Graphs and charts are used for illustrative purposes only and do not reflect future values or changes. Past performance is not indicative of future returns. This commentary is based on information that is believed to be accurate at the time of writing and is subject to change. All opinions and estimates contained in this report constitute RBC Dominion Securities Inc.'s judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. Interest rates, market conditions and other investment factors are subject to change. Past performance may not be repeated. The information provided is intended only to illustrate certain historical returns and is not intended to reflect future values or returns. This publication is not intended as nor does it constitute tax or legal advice. Readers should consult their own lawyer, accountant or other professional advisor when planning to implement a strategy.