Nick Milau

July 9, 2026

Weekly Wrap

Global stock markets were mixed this week with North American stocks gaining while the International equities were under water. Canadian stocks gained 1% with energy stocks rising while materials stocks sold off. With the Iran War ‘back on’ again oil prices half-heartedly rose 5%. The rise in oil prices was fairly modest, however, when compared to prior Middle East flare ups. Developed International Markets and Emerging Markets fell 2% and 1.5%, respectively, as they continue to show their vulnerability to energy price volatility. The IEA did provide some welcome updates, however, indicating that they expect that demand for energy to fall this year, largely as a result of weary consumers rationalizing their usage following the chaotic price volatility we have seen thus far in 2026. Interest rates rose in sympathy with the jump in energy prices as yields crept up 0.05%.

Market Insights

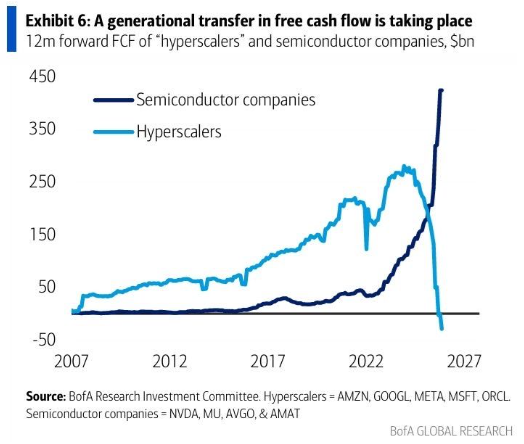

Cash flow and credit concerns already creeping into the Hyperscaler sector. As hyperscalers continue to deploy cash into their AI infrastructure plans, a stunning reversal of fortune is taking place. As shown below, the previously parabolic growth in cash flow for the hyperscalers (Amazon, Google, Meta, Microsoft and Oracle) has now gone in reverse and this cash is now flooding the pockets of the chip companies (Nvidia, Micron, Broadcom and Applied Materials). To fill the funding gap the hyperscalers have been borrowing at record pace and the investor enthusiasm for tech bonds is also beginning to go south. Amazon saw a drop in demand for their recent bond issuance and just yesterday Oracle had their credit rating downgraded to one notch above junk. The voracious appetite for capital needed to fund AI-related infrastructure is well documented at this point, and numerous raises to spending guidance from hyperscaler companies have put expected capex spends for the sector this year in excess of $700 billion. Among the major hyperscalers, Oracle has the highest debt load, and as such their bonds are the riskiest of the bunch but this should serve as a warning that if and when the demand for tech debt, and the quality of that debt, goes south you can expect an abrupt halt to said capex spending plans. The current pace of borrowing and spending simply can’t continue and I would expect that this will be an impending headwind for an economy that is increasingly relying on AI spending for growth.

US Trade Deficit Widens in May. The US trade deficit widened by 42% in May as AI related investment drove capital goods imports to a record high. This marks the widest deficit since May 2025, according to the Commerce Department's Bureau of Economic Analysis and the Census Bureau, which was exacerbated by front loading efforts by businesses as potential tariffs and the Iran conflict raised cost and supply chain uncertainty. Imports grew by 3.3% to the highest level since March 2025, likely supported by a strong greenback, with goods imports increasing by 4.0% to the highest level since April 2025. Capital goods imports rose by $1.1 billion to a record $138 billion, driven by import growth of computer accessories and semiconductors. Higher capital goods imports tend to imply strong business investment, but analysts have highlighted that rising price pressures may complicate the picture. Adjusted for inflation, capital goods imports fell to $108.7 billion in May from $110.5 billion in April. Exports, on the other hand, declined by 3.2%. Trade has detracted from economic growth in the US for two straight quarters. The Atlanta Federal Reserve's GDP forecast model is currently projecting 1.4% annualized growth in the second quarter. US trade policy is clearly hurting their economy but the Trump administration remains eerily silent on this fact.

Portfolio Update

Late last week we added a new stock to our portfolios: Blackstone Group (BX). BX is the world’s largest alternative asset manager and, yes, they manage the Blackstone Private Equity Strategies Fund that most of you hold. Blackstone’s business model is impressive for the following reasons:

- Strong competitive advantage(s): deal sourcing, economies of scale, reputation, proven track record

- High earnings growth with modest capex: 10% average growth over the last 10 years but with some annual volatility

- Secular growth prospects from the opening up of ‘Alts’ to the broader investment community

While buying a stock now may seem counterintuitive given our concerns about ‘market’ valuations, BX shares are down 20% in 2026 offering too good of a deal to pass up. The shares are down largely due to what we feel are excessive concerns about the Private Credit market but we are bottom up investors so we prioritize buying good companies over where we think the market is going. In order to free up the cash for this we have trimmed some of your RBC shares.

Please note any changes apply to our PIM Portfolios Only, subject to restrictions. Please call to clarify if you have any questions.

Planning On

This week’s Musings submission is less around planning and more about insights. As we make our regular calls to our clients, meet for annual reviews and present to our bank and other partners, two topics have often come up recently. One is AI. We hear a lot about Artificial Intelligence but it focuses mostly on generative AI specifically large language models. But what about physical AI which spans a number of different technologies. The other topic is space with Space X having recently gone public with much exuberance although it is currently trading just above its IPO price.

We thought this week we would share some thoughts on these two topics (as well as some others) from RBC Global Asset Management’s Managing Director, Chief Economist and Head of Investment Strategy Research Eric Lascelles. He and his team always produce great stuff (they helped me get through COVID by just focusing on the data and not the noise) but the sections on the economics of space * near-term, medium-term and long-term * are a really good read as is the section on physical AI. If you have some time during the down summer months and are interested in these two subjects, please click on the link below. Look for the sections “The economics of space” and “Let’s get physical (AI)”.

#MacroMemo - July 7 - 20, 2026

This information is not intended to provide legal, tax, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified lawyer or accountant, as applicable, before acting on any of the information.

Charts of the Week

Feel free to share this newsletter with anyone who might benefit from it or find value in it. Thank you for reading our commentary. We welcome your feedback!

Return to homepage

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. â / ™ Trademark(s) of Royal Bank of Canada. Used under license. © RBC Dominion Securities Inc. 2026. All rights reserved. This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. This publication is for information purposes only. Graphs and charts are used for illustrative purposes only and do not reflect future values or changes. Past performance is not indicative of future returns. This commentary is based on information that is believed to be accurate at the time of writing and is subject to change. All opinions and estimates contained in this report constitute RBC Dominion Securities Inc.'s judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. Interest rates, market conditions and other investment factors are subject to change. Past performance may not be repeated. The information provided is intended only to illustrate certain historical returns and is not intended to reflect future values or returns. This publication is not intended as nor does it constitute tax or legal advice. Readers should consult their own lawyer, accountant or other professional advisor when planning to implement a strategy. Insurance products are offered through RBC Wealth Management Financial Services Inc.("RBC WMFS"), a subsidiary of RBC Dominion Securities Inc.* RBC WMFS is licensed as a financial services firm in the province of Quebec. When providing insurance products in all provinces except Quebec, Investment Advisors are acting as Insurance Representatives of RBC WMFS. In Quebec, Investment Advisors and Estate Planning Specialists are acting as Financial Security Advisors of RBC WMFS. RBC Dominion Securities Inc., RBC WMFS and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. and RBC WMFS are member companies of RBC Wealth Management, a business segment of Royal Bank of Canada. â / ™ Trademark(s) of Royal Bank of Canada. Used under license.

RBC Dominion Securities Inc.