Rita Li, CFA, MBA, CFP

Senior Portfolio Manager, Wealth Advisor

May 19, 2026

We expected a volatile year in 2026 given that it is a U.S. midterm election year, but few anticipated the degree of geopolitical uncertainty that has emerged under the second Trump administration. Entering the year, the economic backdrop appeared constructive: inflation was moderating, economic growth remained resilient, and corporations were issuing stronger earnings guidance.

That outlook shifted meaningfully following the Iran–U.S. conflict, which triggered one of the largest oil supply shocks in recent history. The scale and duration of disruptions in the Strait of Hormuz have been unprecedented, with broad implications for global growth. Beyond crude oil, the region is also a key transit route for commodities such as fertilizers, helium, and sulphur, creating additional inflationary pressures across global supply chains.

The key questions now are how severe the economic impact may become and whether structural growth drivers — particularly continued investment in artificial intelligence — can offset some of the headwinds associated with higher energy and commodity prices.

Earnings Remain Resilient

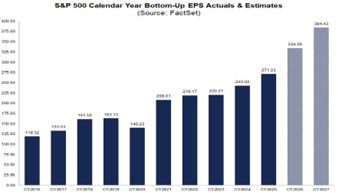

Despite growing geopolitical concerns, corporate earnings have remained supportive of equity markets. As of May 15, 91% of S&P 500 companies had reported positive earnings surprises, while 84% exceeded revenue expectations. The blended earnings growth rate for the first quarter of 2026 stands at 27.7%, marking the sixth consecutive quarter of double-digit earnings growth for the index.

Within the Information Technology and Communication Services sectors, companies such as Nvidia, Micron, Alphabet, and Meta have been among the largest contributors to earnings growth. Amazon has also been a notable contributor within the Consumer Discretionary sector. Meanwhile, the S&P 500 forward price-to-earnings ratio currently stands at 21.4x, above the 10-year average of 18.9x.

Source: FactSet Earnings Insight May 15, 2026

Analysis of corporate earnings calls between March and May suggests that while many companies have acknowledged the geopolitical risks associated with the Middle East, relatively few have revised guidance lower. To date, the most visible impacts have been concentrated in travel and tourism-related industries. Broadly speaking, most S&P 500 companies have not yet incorporated material downside assumptions related to a prolonged conflict or sustained increases in input costs.

Rising Inflation and Government Debt Concerns

At the same time, market participants are increasingly focused on the sustainability of U.S. government debt levels. Gross U.S. federal debt has risen to approximately 128% of GDP, underscoring the growing dependence of economic growth on fiscal spending since the Global Financial Crisis.

Financial markets are particularly sensitive to changes in government borrowing costs because U.S. Treasury yields serve as key benchmarks for the pricing of many financial assets globally. As debt levels rise, the long-term sustainability of higher financing costs becomes increasingly important.

The outlook for interest rates has also become more uncertain in the current geopolitical environment. Entering 2026, many economists expected interest rate cuts as inflation continued to moderate. However, persistent commodity-driven inflation pressures have shifted expectations, with some economists now anticipating additional rate increases instead.

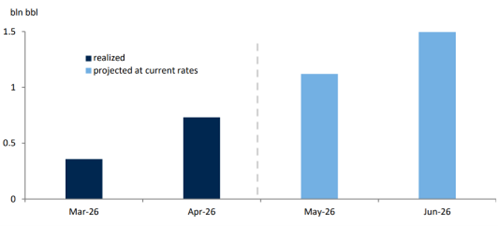

At present, markets largely view the Iran–U.S. conflict as an inflation shock rather than a structural growth shock, assuming that commodity prices may normalize once the conflict subsides. However, the longer the conflict persists, the greater the cumulative crude production loss and the longer it may take for oil prices to return to pre-war levels. Should elevated energy prices persist, the risk of slower global growth would likely increase meaningfully.

Realized and Projected Cumulative Middles East Crude Production Loss (at Status Quo)

Source: Petro-Logistics, Kpler, RBC Capital Markets estimates.

The Growing Importance of Diversification

As investors navigate a world increasingly shaped by “fat-tail” risks — including pandemics, supply chain disruptions, and regional conflicts — the case for broader portfolio diversification continues to strengthen.

Traditional balanced portfolios consisting primarily of stocks and bonds may face greater challenges in periods of elevated inflation and geopolitical instability. As a result, asset classes such as commodities, real assets, and alternative investments may help improve diversification and provide additional downside protection during periods of systemic stress.

At the same time, significant developments are taking place across international markets. South Korea and Taiwan have continued to gain prominence in global equity market capitalization, overtaking several European markets. Earlier in the year, prior to the Iran–U.S. conflict, investors had already begun rotating toward international equities in search of greater diversification away from the increasingly concentrated U.S. market, particularly its heavy exposure to artificial intelligence-related companies.

International diversification may ultimately prove to be one of the more important long-term investment themes emerging from this environment. We continue to monitor these developments closely as we seek to enhance diversification and improve long-term return potential for client portfolios.

Rita Li works with professionals, business owners, and high-net-worth families to provide tailored investment advice, risk management, and financial planning solutions. Her team includes professionals with deep expertise in taxation, insurance, and legal planning, enabling the delivery of a comprehensive wealth management experience. Rita is a CFA® charterholder and Certified Financial Planner (CFP®) and holds an MBA from the Richard Ivey School of Business.