Rita Li

October 1, 2024

Taking Temperature of the economies on both sides of the border

The central bank rate cutting cycle is now underway, sparking a more cheerful tone in markets as lower interest rates and the prospects of future interest rate cuts will help to ease financial conditions and stimulate economic growth. One of the leading economic indicators as measured by the Citigroup Economic Surprise Index has pivoted to positive surprises. The U.S. job numbers for September were also stronger than expected. Both the payrolls and household survey suggested an acceleration in hiring in recent months. In the fall of 2024, the U.S. economy looks to remain on a soft-landing path.

Economic surprises have started to rebound

As of 10/03/2024. Sources: Citigroup, Bloomberg, RBC GAM

As with the U.S., Canada’s job numbers managed to deliver positive surprises. The rate of hiring has picked up over the past few months. Canada’s latest quarterly Business Outlook Survey showed continued subdued demand, but with an upward tilt in economic activity and a downward tilt in inflation pressures. Both are welcome.

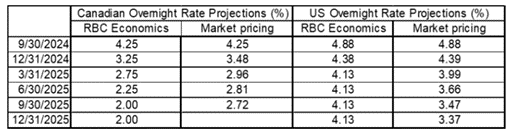

While both economies are seeing positive momentum and lower inflation, there is a growing gap between the two countries’ GDP growth as measured by GDP per capita (per person). Given the diverging path in growth between the two countries, RBC Economics has forecasted a more aggressive rate cutting cycle in Canada vs. the U.S. and that has been reflected in both the pace of the interest rat cuts as well as the magnitudes. If the forecasted interest rate paths prove to be accurate, the growing gap in the benchmark interest rates between the two countries can put further pressure on the Canadian dollar.

RBC Economics’ U.S. and Canadian Overnight Rate Projections

Source: RBC Economics, Bloomberg

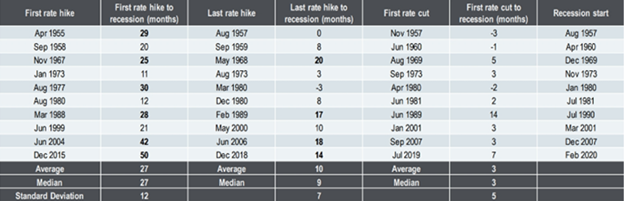

With the increasing soft-landing narrative, is Recession no longer a concern?

So far central banks have been able to bring down inflation without causing significant harm to the labour market and economic growth. However, there is a significant lag between when the recession starts and the first Fed rate hike. It takes on average 27 months for the impact of higher interest rates to work into the economy itself. Historically, most interest rate easing cycles have been associated with a recession or an approaching recession with exceptions in 1984, 1995 and 1998. Given that consumer spending accounts for approximately 70% of the U.S. economy, it will be crucial for us to see unemployment rates stabilize near current level and do not further deteriorate.

Source: RBC GAM, Federal Reserve, NBER, Bloomberg.

S&P500 Earnings Update for Third Quarter 2024

The third quarter earning season so far has been slightly disappointing with lower beats and lower earning revisions. Of the 37% of S&P 500 companies that have reported already, 75% have exceeded analysts’ EPS estimates. This beat rate is slightly below the five-year average of 77% but matches the 10-year average. However, the margin of these earnings beats has underwhelmed, averaging just 5.7% above estimates compared to the five-year average of 8.5% or a 10-year average of 6.8%.

At this stage of the earnings season, the blended earnings growth rate, which includes both reported and estimated results, stands at 3.6%. This would represent the fifth consecutive quarter of year-over-year earnings growth for the index but also the lowest growth rate since Q2 2023, when earnings declined by 4.2%.

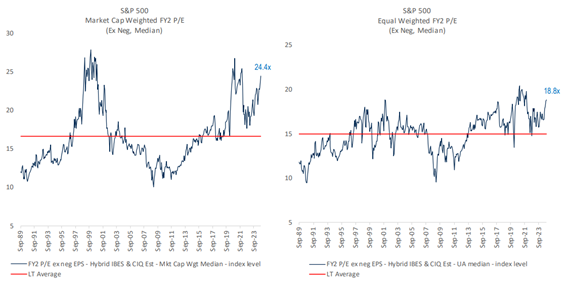

Looking ahead, analysts expect a year-over-year earnings growth rate of 13.4% for Q4 2024. For 2024, the anticipated earnings growth rate is 9.3%. The forward 12-month Price to Earnings ratio is 21.7x, which is above the 5-year and 10-year averages of 19.6x and 18.1x, respectively.

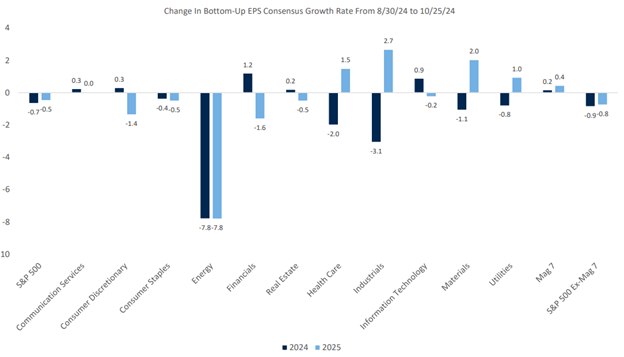

Consensus S&P500 EPS growth forecasts have softend for both 2024 and 2025 recently

with Energy accounted for much of the downtick in 2024’s consensus EPS growth rate forecast

Source: RBC US Equity Strategy, Bloomberg. As of 10/25/2024

We have been talking to clients about gaining more exposure to the S&P Equal weighted index as opposed to the capital weighted index as the gap between the Magnificent 7 and the S&P500 excluding Magnificent 7 on an earnings per share basis is expected to narrow in 2024 and 2025. From a valuation stand point, the Price to Earnings ratio for the Equal Weighted Index is also less demanding in the context of a shrinking earnings growth gap.

S&P 500 Valuations continue to creep up, but remain a little below peak

Source RBC US Equity Straegy, Russell, S&P Capital IQ/ClarifFI, CIQ estimates, IBES estimates; as of 10/23/2024