Sunil Bhardwaj

Lead Strategist

April 5, 2026

Our January market commentary noted that, at the time, there was an absence of the typical bear market triggers: a spike in interest rates, a recession, or a significant exogenous global event. The last of those is, by its very nature, difficult to predict. Moreover, every year there are one or two geopolitical events that unsettle investors. We consistently advise investors to look past most such events – including regional military hostilities – as markets tend to overestimate their impact on corporate earnings and, thus, stocks. Last year’s trade war was just the most recent example, as US corporate earnings grew a healthy 13% despite fears regarding the impact of new tariffs.

Occasionally, an event emerges that requires investors to genuinely recalibrate — not panic, but adapt. The Covid pandemic in 2020 was one such moment, and while it caused real short-term disruption, markets recovered and ultimately rewarded those who stayed the course. The current US-Iran conflict warrants the same measured attention: it is a development we are taking seriously and actively positioning for, while keeping the long view firmly in mind.

Why This Conflict Hurts Stocks More Than Most

Most geopolitical events – including regional conflicts – tend to have limited and short-lived impacts on corporate earnings, which is why investors should look past them. However, disruptions to global energy supply are a key exception due to their impact on inflation, consumer spending, and corporate margins. Higher energy prices can also delay central bank rate cuts, keeping borrowing costs elevated.

The current situation falls into that category. The effective closure of the Strait of Hormuz has resulted in one of the largest energy supply disruptions in history given that 20% of global seaborne oil passes through it.

To be clear, we believe that both sides are motivated to find a resolution to the confrontation, and we are not predicting a bear market. Markets appear to be pricing in a near-term resolution, partly because President Trump will want to avoid inflationary pressures ahead of November’s mid-term elections. But even once a ceasefire agreement emerges, we believe energy production from the region will take longer to return to normal than most investors realize.

RBC Capital Markets’ commodity analysts note that because of the Strait of Hormuz blockade, producers have shut an estimated 11 million barrels of oil per day. Such shutdowns can take months to return to full capacity. Then there are the 40+ facilities that have sustained damage – infrastructure repairs could lengthen timelines even further. As a result, the RBC analysts believe that if the conflict becomes extended, oil prices could rise meaningfully higher.

With regards to the natural gas that the region supplies to Europe and Asia, damage from an attack on the world’s largest liquids natural gas facility in Qatar will take years to repair. Asian economies have already implemented energy rationing.

Investment Strategy

Despite near-term uncertainty, we believe selling into this fear would be a tactical mistake. Market recoveries following geopolitical shocks tend to be both sharp and front-loaded. On the day a ceasefire is announced, we believe a significant portion of the rebound will occur within days, meaning investors who sold could miss much of the recovery. As the chart below illustrates, military conflicts can create some near-term volatility but over the long-term, stocks have been resilient.

Our Positioning

While we do not believe selling stocks amidst the uncertainty is the right strategy, we have not taken a hands-off approach to portfolios. Within stock portfolios, we have increased exposure to North American producers of oil, chemicals and fertilizers. Supply of chemicals and fertilizers has also been disrupted by the war. If we are right, prolonged weak supply should keep prices of these commodities elevated well after any ceasefire.

Mid-Term Election Years: The Good and the Bad

Importantly, the geopolitical volatility is occurring within the context of a US mid-term election year. As we noted in our January commentary, the different phases of the four-year US Election cycle create tailwinds and headwinds for the stock market. The first ten months of a mid-term election year are often marked by policy-induced volatility. While the reason for this year’s stock market weakness is different than the norm, the volatility we have experienced fits the historical pattern.

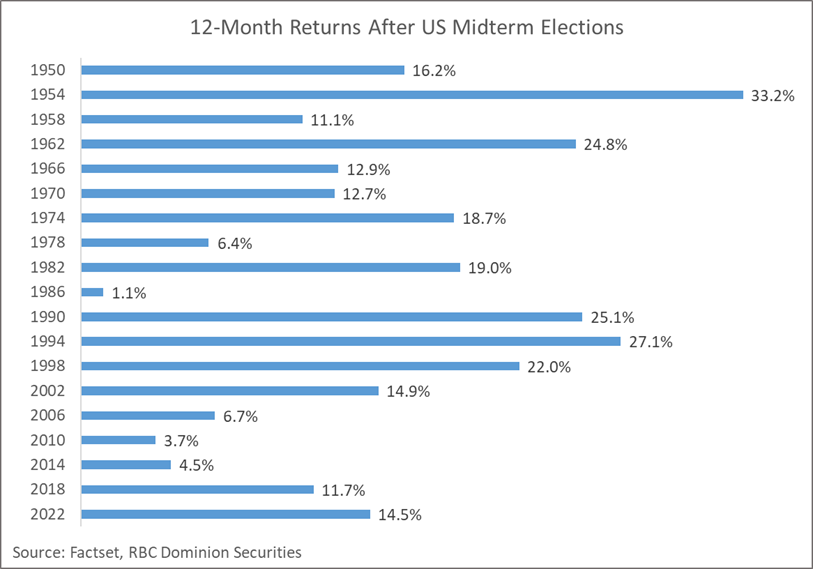

But there is certainly light at the end of the tunnel if the pattern holds: the best period in the US Election cycle is the year after the mid-term elections. The S&P 500 index has generated an impressive average return of 15% in the 12 months after the mid-term elections dating back to 1950. Stocks tend to do well not because of who wins, but because investors finally know what they are dealing with. Once uncertainty fades and policy becomes more predictable, stocks respond favourably.

Conclusion

As we await the potential tailwinds of the post-election period, we will continue monitoring three key indicators: (1) ceasefire negotiations or escalation signals; (2) production restart timelines as the conflict winds down; and (3) inflation data, particularly in energy-dependent sectors. Until those dynamics shift, we will remain overweight North American energy, chemicals and fertilizer producers.

If you have any questions, please do not hesitate to contact us.