Markets Recover While Clarity Remains Elusive

Markets corrections tend to conclude when situations improve from terrible to awful, not when all problems vanish, as we have seen time and again, with notable examples in 2009 and 2020. Emotional reactions to fear-mongering by the media can destroy wealth as missing a few best trading days permanently damages portfolios. Staying in the path laid out in one’s financial plan requires ignoring media hysteria and focusing on corporate fundamentals. History shows that the most rewarding investing opportunities emerge precisely when conditions feel most uncomfortable.

Markets corrections tend to conclude when situations improve from terrible to awful, not when all problems vanish, as we have seen time and again, with notable examples in 2009 and 2020. Emotional reactions to fear-mongering by the media can destroy wealth as missing a few best trading days permanently damages portfolios. Staying in the path laid out in one’s financial plan requires ignoring media hysteria and focusing on corporate fundamentals. History shows that the most rewarding investing opportunities emerge precisely when conditions feel most uncomfortable.

Robin Gullason

Associate Portfolio Manager & Lead Strategist

April 24, 2026

- Markets rebound when crises shift from "terrible" to "awful", not when all problems are resolved.

- Markets price in future expectations rather than current events, causing recoveries to occur while news remains dire and geopolitical tensions persist, but a glimmer of hope emerges.

- The 2008/9 Financial Crisis, 2020 COVID crash, and recent corrections all demonstrate that market bottoms arrive unexpectedly during peak panic, not after recovery is evident.

- The 24-hour news cycle weaponizes fear, often leading investors to take actions that are contrary to their long-term financial well-being.

- The market’s best performing days often come shortly after some of the worst. Brief sideline absences can permanently impair long-term portfolio growth.

- Rather than tracking geopolitical noise, our attention is turning to this month’s corporate earnings releases, which will give us a sense of how well businesses have weathered the recent storm.

- Yet again, we have all learned that timing the market is challenging and following the narrative of the media can lead to really poor investor outcomes.

The paradox of market corrections is that the stock market often starts to rebound even as the headlines remain dire. To the casual observer, the sharp recovery in global equity markets in recent weeks might seem disconnected from reality. After all, the Strait of Hormuz remains effectively closed and the “ceasefire” between Iran and the U.S./Israel seems fragile at best. If we look back at market history, this isn’t unusual. Markets do not wait for the "all-clear" signal to move higher; they move when the reality of the situation transitions from "terrible" to "awful." The technical term in the industry is that things are getting “less bad”.

The "Less Bad" Phenomenon

Markets are forward-looking mechanisms that price in future expectations rather than current events. It is sometimes difficult to remember this when the headlines of the day remain troubling. When a geopolitical crisis erupts, the market quickly discounts a worst-case scenario. However, once it becomes clear that the worst-case is being contained, the market begins to recover, often quite quickly. In the stock market, "less bad" is often the equivalent of "very good" when it comes to short-term returns. As fear evaporates, prices rise long before whatever is troubling the world is completely sorted out. We have seen this cycle repeat across every major crisis in recent memory.

Historical Precedents Abound

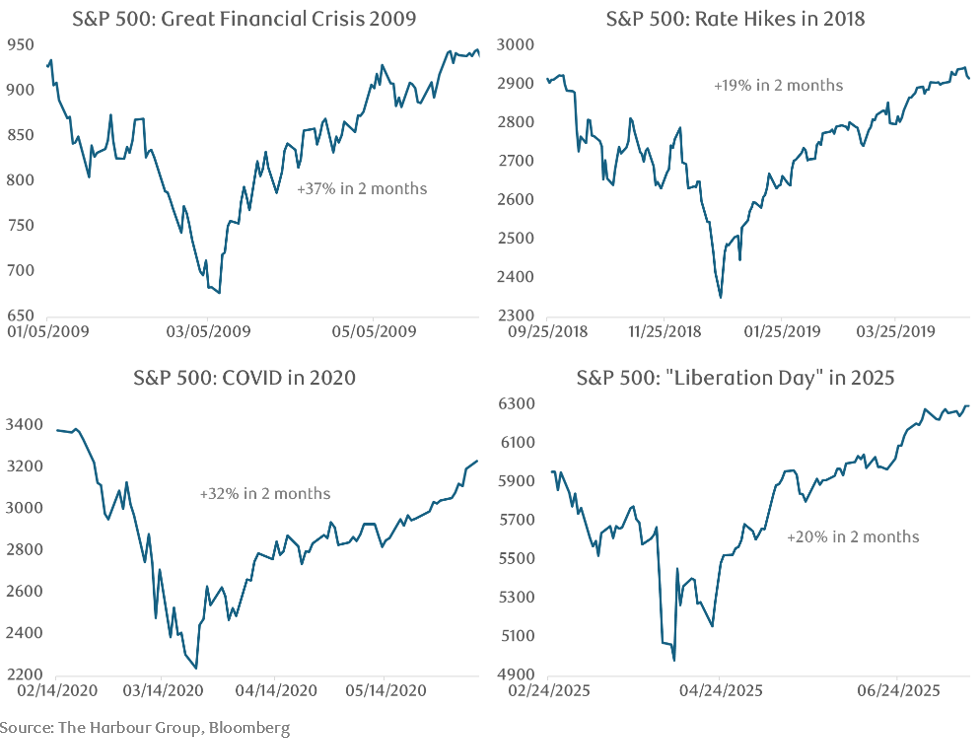

Consider the Global Financial Crisis. In early 2009, the headlines were dominated by bank failures and the potential collapse of the global financial system. The market didn't bottom when the economy was on the road to recovery. It bottomed in March 2009, while unemployment was still rising (it peaked in October) and the news was still objectively terrible. Investors simply realized the world wasn't ending. Similarly, look at the COVID Low and the subsequent recovery. In March 2020, the world was entering an unprecedented lockdown with no vaccine in sight. Yet, the market bottomed just as the news cycle was hitting its peak of panic. By the time effective vaccines arrived, the market had already staged a significant recovery. The market recognized that while the situation was still difficult, the trajectory had shifted from "unknown abyss" to "solvable problem." Similar sharp recoveries were seen after corrections in 2018 and just last year, reinforcing the view that recoveries tend to come when many least expect and don’t leave a lot of time for those on the sidelines to get reinvested.

Market bottoms come quickly and without warning

The Business of Emotion

One of the greatest hurdles for investors is the 24-hour news cycle. Media outlets are in the business of capturing attention, and nothing captures attention like fear. Headlines are designed to trigger an emotional response, often suggesting that "this time is different" or that current geopolitical hostilities are an unprecedented threat to your portfolio. Making emotional decisions based on the evening news or social media is almost always to the long-term detriment of a thoughtfully constructed financial plan. Selling into a panic locks in losses and, more importantly, forces one to make a second, even more difficult decision: when to get back in. Missing just a few of the market’s best days (which almost always occur in close proximity to the worst days) can permanently stunt the growth of a portfolio.

Known Unknowns

With all that said, we do not know what the future holds. If hostilities in the Middle East escalate or new fronts open, volatility will return with a vengeance. Current price action suggests that markets believe the immediate systemic risk has been contained. While the geopolitical noise continues, we are shifting our focus to the signal. As the current earnings season unfolds, we will be watching with interest to see how corporate America has weathered the storm over the last several months. Another key factor will be the impact the artificial intelligence data centre buildout is having on big technology companies’ cash flows, and the prospects of eventual returns on this massive investment.

Investing is all about making decisions without perfect information, with volatility and surprises bound to impact portfolios on a regular basis. History shows us that the most rewarding times to be an investor are often the times when it feels most uncomfortable to do so. Our strategy remains rooted in the compounding returns over the long term. We all know that there is trouble in the world, but we are encouraged by the incredible resilience of the global economy. By tuning out the emotional noise of the media and focusing on company fundamentals such as earnings, we ensure that your capital is positioned to benefit when "less bad" eventually turns into "genuinely good."

The Harbour Group - 416-842-2300

Putting you first, every time, to help you navigate the complexities of managing your wealth. All of our team members, all of our resources, all of our collective insight: ALL FOR ONE: YOU™.

The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc. and its affiliates may have an investment banking or other relationship with some or all of the issuers mentioned herein and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. RBC Dominion Securities Inc. and its affiliates also may issue options on securities mentioned herein and may trade in options issued by others. Accordingly, RBC Dominion Securities Inc. or its affiliates may at any time have a long or short position in any such security or option thereon. Mutual funds are sold by RBC Dominion Securities Inc. There may be commissions, trailing commissions, management fees and expenses associated with mutual fund investments. Read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member CIPF. ®Registered Trademark of Royal Bank of Canada. Used under licence. RBC Dominion Securities is a registered trademark of Royal Bank of Canada. Used under licence. ©Copyright 2019. All rights reserved.