Steering Through Uncertainty: Four future paths for Canada’s auto industry

This report is part of RBC Thought Leadership’s Growth Project, our ongoing initiative to generate new ideas for the Canadian economy. Canada’s auto industry, which employs 125,000 people and accounts for 10% of Canadian exports, is central to the dynamism of the country’s wider advanced manufacturing sector and economic relations with the U.S. Over the past 10 months, to help chart a path forward for the industry at this critical moment, we spoke with automakers, parts suppliers and other industry experts to inform the research, which sets out four different futures for the industry.

This report is part of RBC Thought Leadership’s Growth Project, our ongoing initiative to generate new ideas for the Canadian economy. Canada’s auto industry, which employs 125,000 people and accounts for 10% of Canadian exports, is central to the dynamism of the country’s wider advanced manufacturing sector and economic relations with the U.S. Over the past 10 months, to help chart a path forward for the industry at this critical moment, we spoke with automakers, parts suppliers and other industry experts to inform the research, which sets out four different futures for the industry.

By Jordan Brennan

May 14, 2026

Key findings

- Canada’s auto industry is at an inflection point within the North American industry. Washington’s focus on reviving domestic production threatens to rip up decades-old Montreal-to-Detroit supply chains. In our most pessimistic scenario, auto assembly plants in Canada could shutter by 2040.

- Alternatively, Canada’s unit volume could grow to two million by 2040. Continued tariff-free access to the U.S. market could ramp up manufacturing in our most optimistic scenario.

- The industry is also grappling with two global transitions unfolding at different speeds. Electric vehicle adoption is proceeding more slowly than forecast, stranding billions in investments. Meanwhile, AI, autonomy, and software revolutions are accelerating faster than original equipment manufacturers (OEMs) can embed in assembly lines, creating a mismatch between capital commitments and market-ready technology.

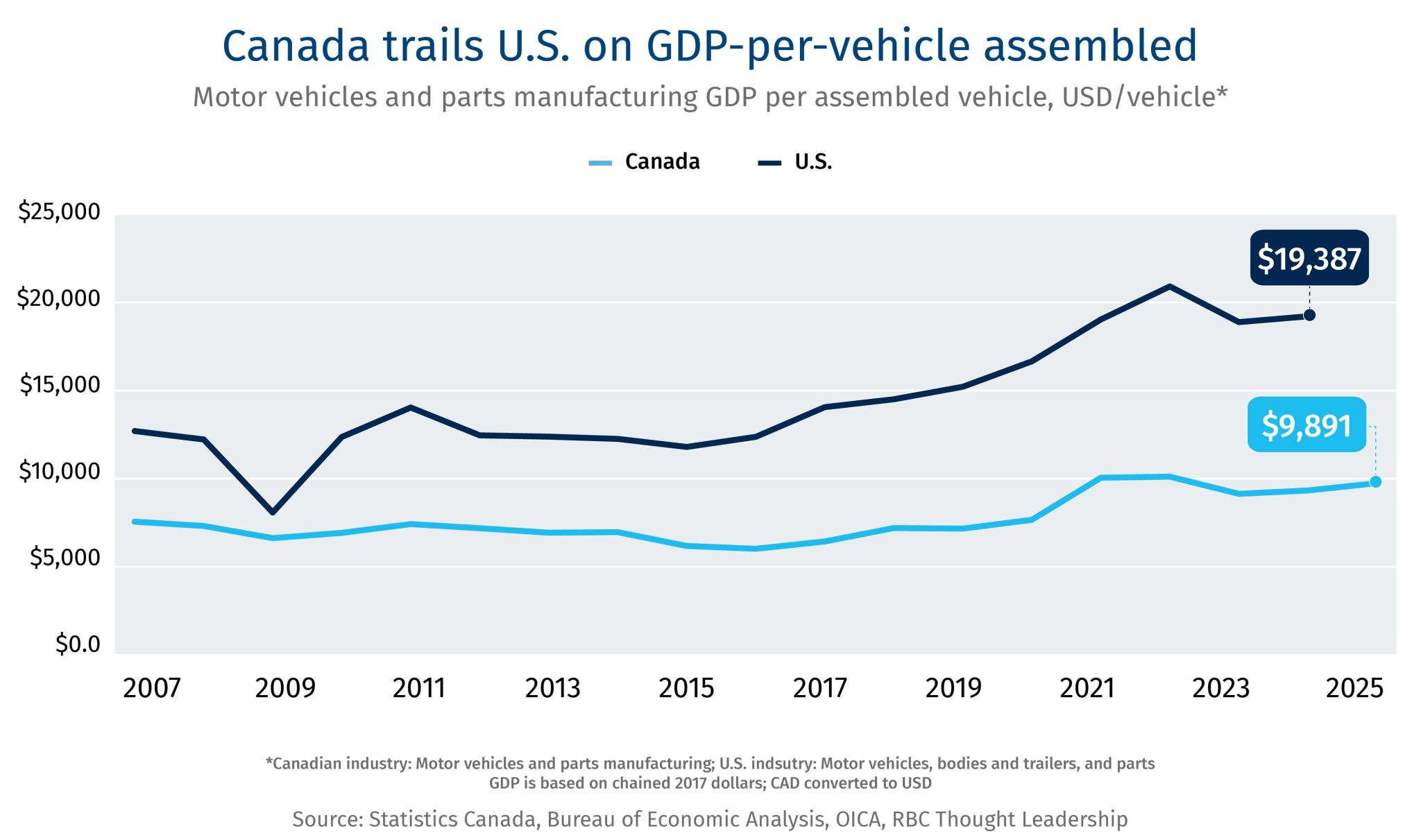

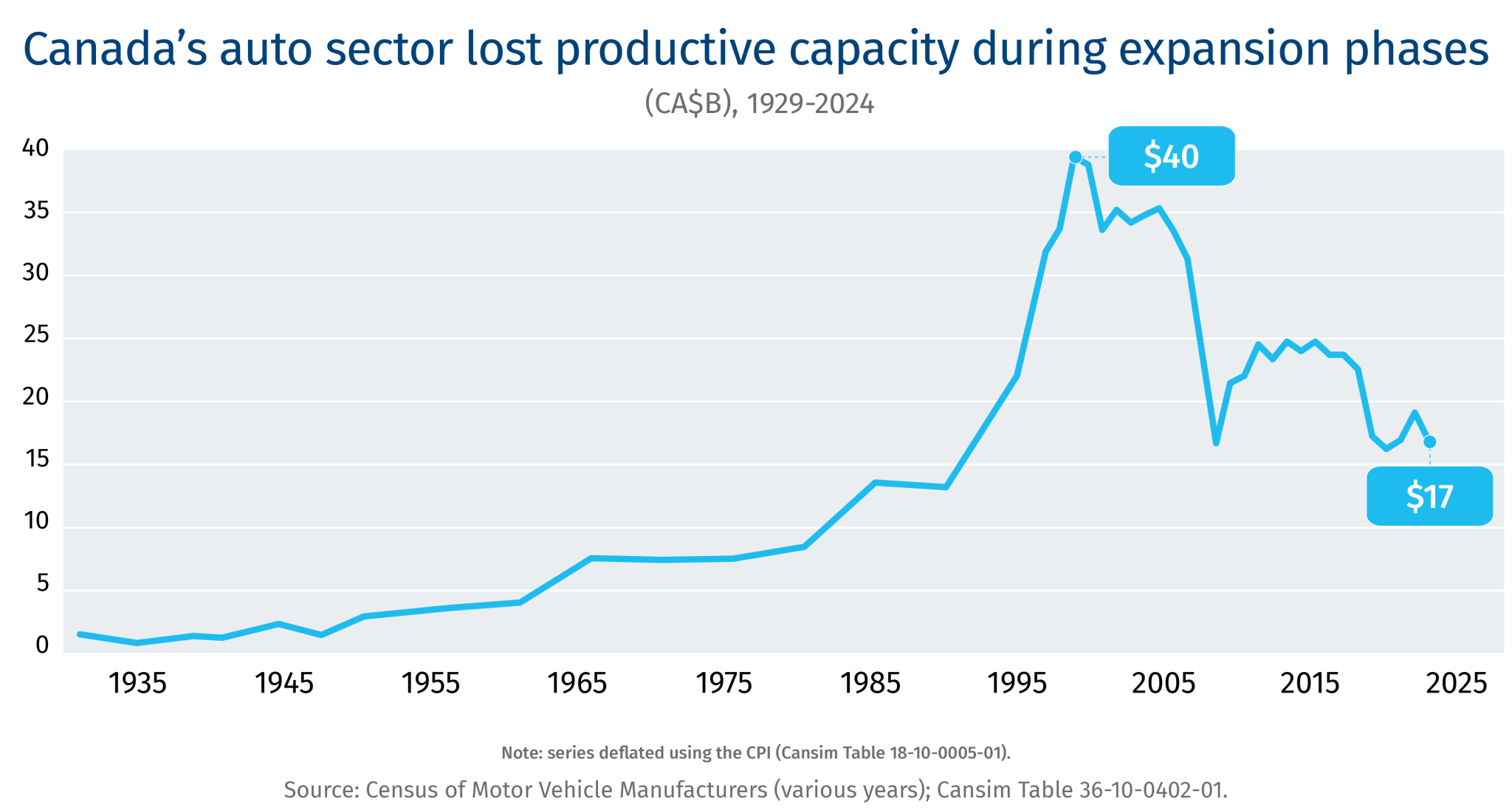

- The auto industry’s future will be increasingly defined by the value generated per vehicle. The U.S. captures roughly twice the amount of GDP per assembled vehicle than Canada–and the gap is widening. Automation and robotics could lead to a world where fewer workers build more vehicles.

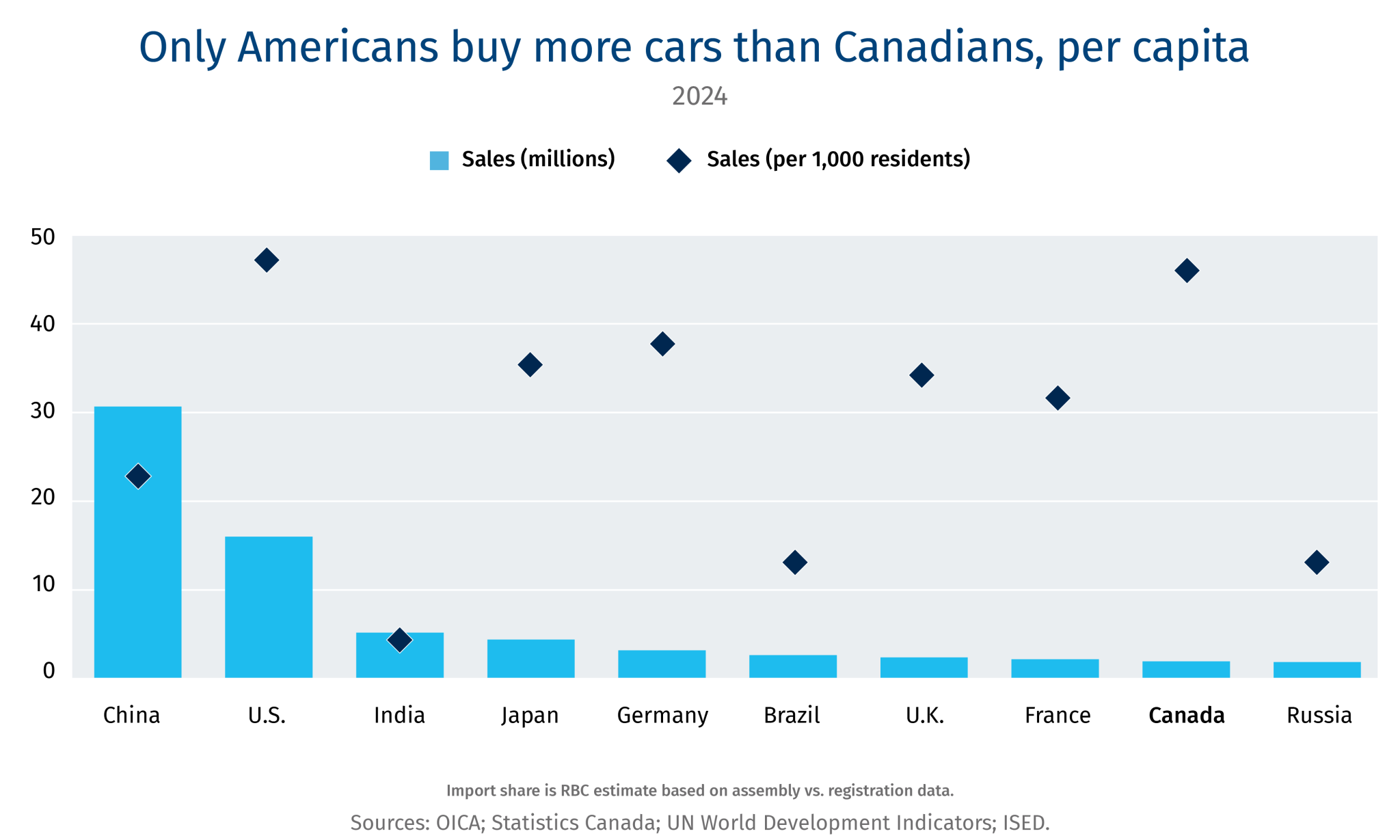

- Market access is a powerful, underutilized asset. Only Americans buy more cars, per capita, than Canadians. With 90% of the Canadian market supplied by imports, Canada can link market access to investment commitments across manufacturing, R&D, software, testing, and certification.

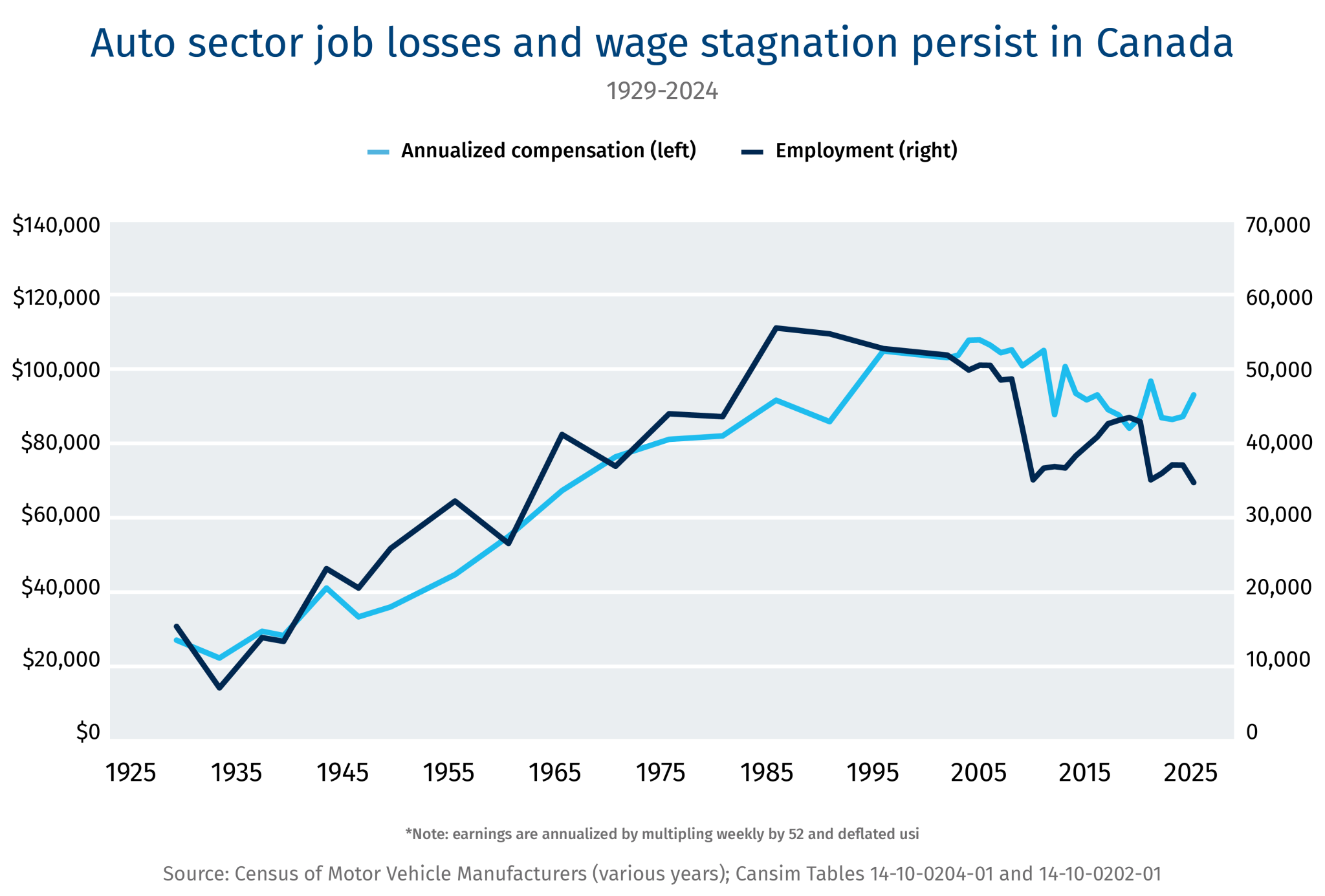

Canada’s auto industry is at the centre of a storm. This isn’t the first time the industry has been threatened by precipitous conditions, but the present deluge poses a serious—perhaps existential—threat. The greatest source of upheaval comes in the form of President Donald Trump’s use of tariffs to repatriate manufacturing capacity to the American heartland. The year following Trump’s re-election was dotted with a painful series of product line cancellations, plant closures, and the most job losses in Canada’s auto industry since the Great Recession.

Adding to the tariff turmoil are four structural shifts in the industry:

Electrification

Electric vehicle adoption initially grew quickly thanks to consumer incentives, emissions rules, and industrial subsidies. But recent incentive rollbacks have made EVs less attractive for consumers, hurting sales, and prompting automakers to pause or cancel EV programs. In the short term, EV adoption may remain uneven due to affordability and charging infrastructure concerns. Long-term, frequent oil market shocks could accelerate adoption as domestically generated electricity leaves countries less exposed to geopolitical instability.

Software

As new models come loaded with connectivity, autonomy, AI, and electric propulsion, cars are increasingly becoming rolling technology platforms. More of a vehicle’s performance and value depends on batteries, chips, sensors, and software. As a result, the value pool expands beyond final assembly. That’s leading to a retooling of the industry as demand for new expertise and components disrupt the established skills and supply chains.

Market

In 2025, some 92 million vehicles were sold globally, down from 95 million in 2017. Sales in the U.S. peaked in 2016, with Canada following a year later.1 The combination of an aging population and rapid urbanization is triggering structural shifts in global demand. That’s even before an impending autonomous vehicle revolution that could reimagine car ownership.

China

Chinese automakers surpassed their Japan rivals as the world’s largest car seller in 2025, having grown its market share from less than 1% to ~35% over the past 25 years. The country’s rising dominance in the global auto market, often with superior technology and lower prices, poses the most significant long-term threat to North America’s auto industry.

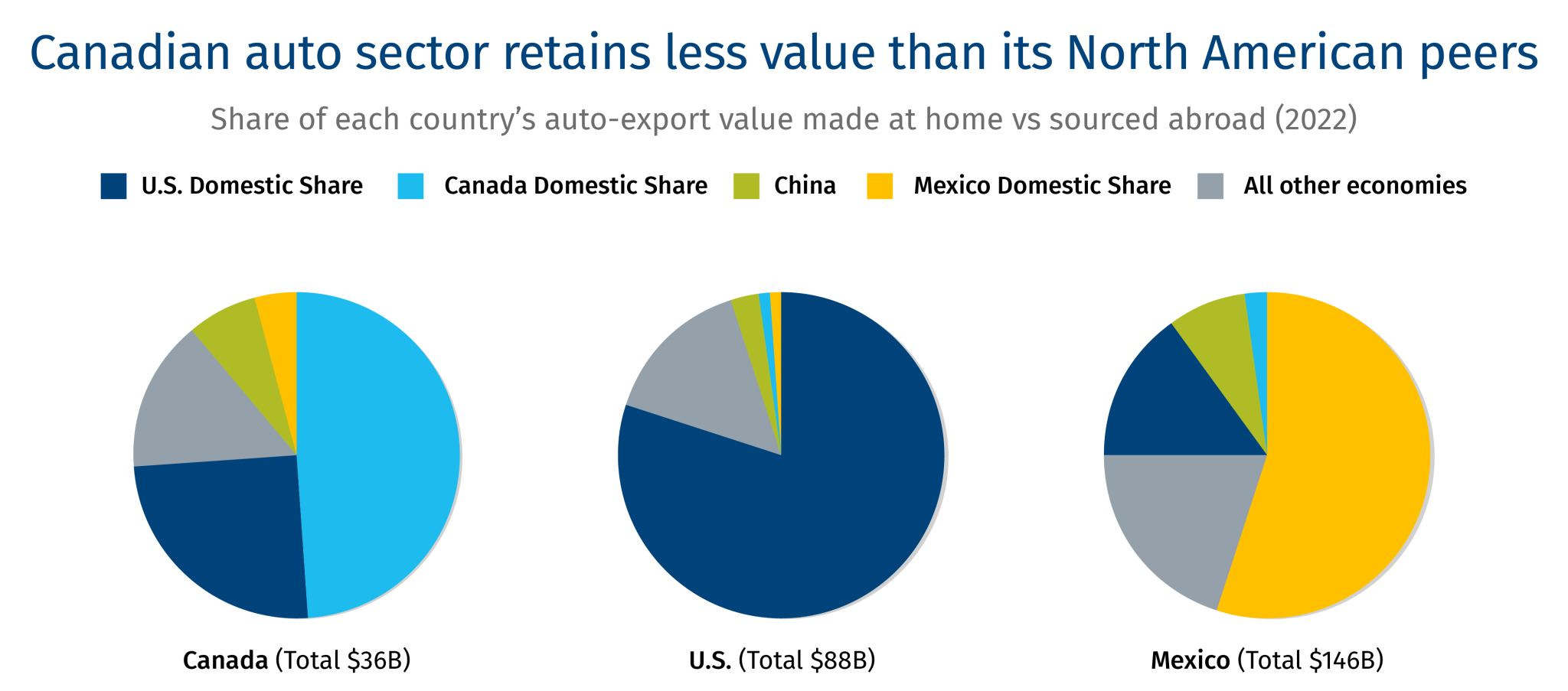

Ultimately, Canada must decide how it positions itself in a transformed global auto system. With US$735 million in annual R&D spending, auto manufacturing is a high-tech, high value industry with substantial spillover benefits across sectors.2 Canada has several competitive advantages, too—skilled labour, clean and affordable power, and award-winning assembly facilities—that position it well to capture value across the supply chain. Success depends on maintaining the competitiveness of the ecosystem of suppliers, services, and technology providers.

With punitive Section 232 tariffs on steel, aluminum and copper still in force and the Canada-U.S.-Mexico (CUSMA) renegotiations imminent, Canadian policymakers and industry need to weigh the tradeoffs between competing strategic orientations. With that in mind, we look out to 2040 and explore four potential paths for Canada’s auto future.

Canada’s OEM Industry Profile

Measure | Estimate Quantities |

Employment | 125,000 workers: assembly (35,000), parts (71,000), body and trailer (18,000) |

Units Produced | 1.3M (2024) |

Value Added (GDP) | $17B (2024) |

Shipments | |

OEMs | Toyota, Honda, Stellantis, GM, Ford |

# Parts Suppliers | 700 |

Gross Capital Stock | $65B (replacement cost) |

Robot Density | 1,475 robots /10,000 employees |

The road ahead

1. Fast Lane—Higher volume, more value and closer integration

Key assumptions

- Canada secures duty-free access to the U.S. market

- Reforms are made to the rules of origin, domestic content requirements, and most favoured nation tariff rates

- Tariffs limit Chinese access to the North American market

- The total cost of EV ownership continues to decline

- Pledged EV investments proceed on a longer timeline

- Advancements in AI and autonomy boost value per vehicle

- Canada expands its low-carbon grid and strengthens its critical minerals refining capabilities.

Life in the ‘Fast Lane’

This is a world where North American integration holds, electrification advances, and value deepens inside existing ecosystems. The five OEMs (General Motors, Ford, Stellantis NV, Honda and Toyota) in Canada maintain their manufacturing presence, but plants that were furloughed or operating at low utilization win new product mandates and increase assembly volumes. The Windsor-Montreal corridor combines assembly plants, Tier-1 suppliers, tooling firms, automation, AI and software firms, and in-market engineering talent that few jurisdictions can replicate. The 700-plus suppliers feature world-class Canadian companies, including Magna, Linamar, Multimatic, and Martinrea.

The Fast Lane is narrow but navigable. The foundation is restored duty-free trade with the U.S. Reforms to the rules of origin, domestic content requirements, and most-favoured-nation tariff rates further incentivize OEMs to allocate product to Canadian assembly plants.3 Simultaneously, a protective tariff wall rises around North America to keep Chinese EVs out—creating the competitive breathing room that North American OEMs need to invest with confidence.

Restored access, coupled with improvement in EV affordability unlocks tens of billions in pledged investment, most of which was deferred during the tariff war. Units assembled climb from 1.3 million in 2025 to 2 million by 2040—as many vehicles as Canadians purchase annually. Plus, Canada’s capabilities in light-weight materials, mobile communications, sensors and controls, software, data analytics, AI, cyber security and battery research are leveraged to win new mandates higher up the value chain.4

The Windsor-Montreal corridor functions as a Silicon Valley of the North—with deep engineering talent in autonomy, AI, lightweight materials and embedded systems. This is important since, as McKinsey projects, the software, sensors, control units, and electronics segment of the global industry will grow from US$335 billion to US$520 billion between 2025 and 2035.

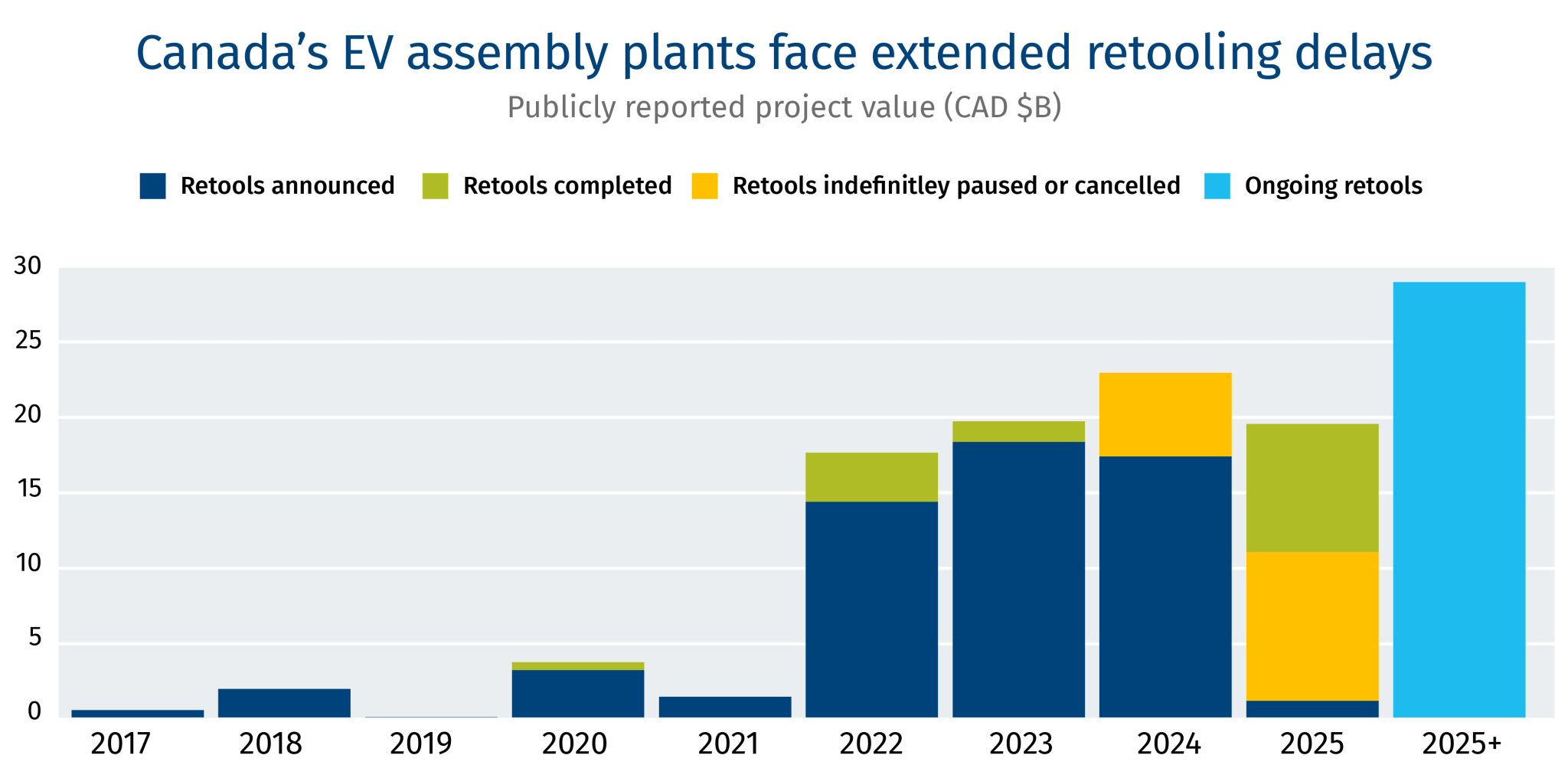

The electrification path is longer than originally forecast, but it arrives. After $70 billion in EV write-downs in 2026, battery costs continue to fall while range and charging infrastructure improve. By 2030, market-driven consumer adoption begins. PHEV and BEV penetration rises from 10% in 2025 to 25% by 2030 and more than 60% by 2040. British Columbia and Quebec lead adoption—EV registrations hold around 20% in hydro-powered provinces even after federal rebates expire—before expanding into other markets as economics improve.

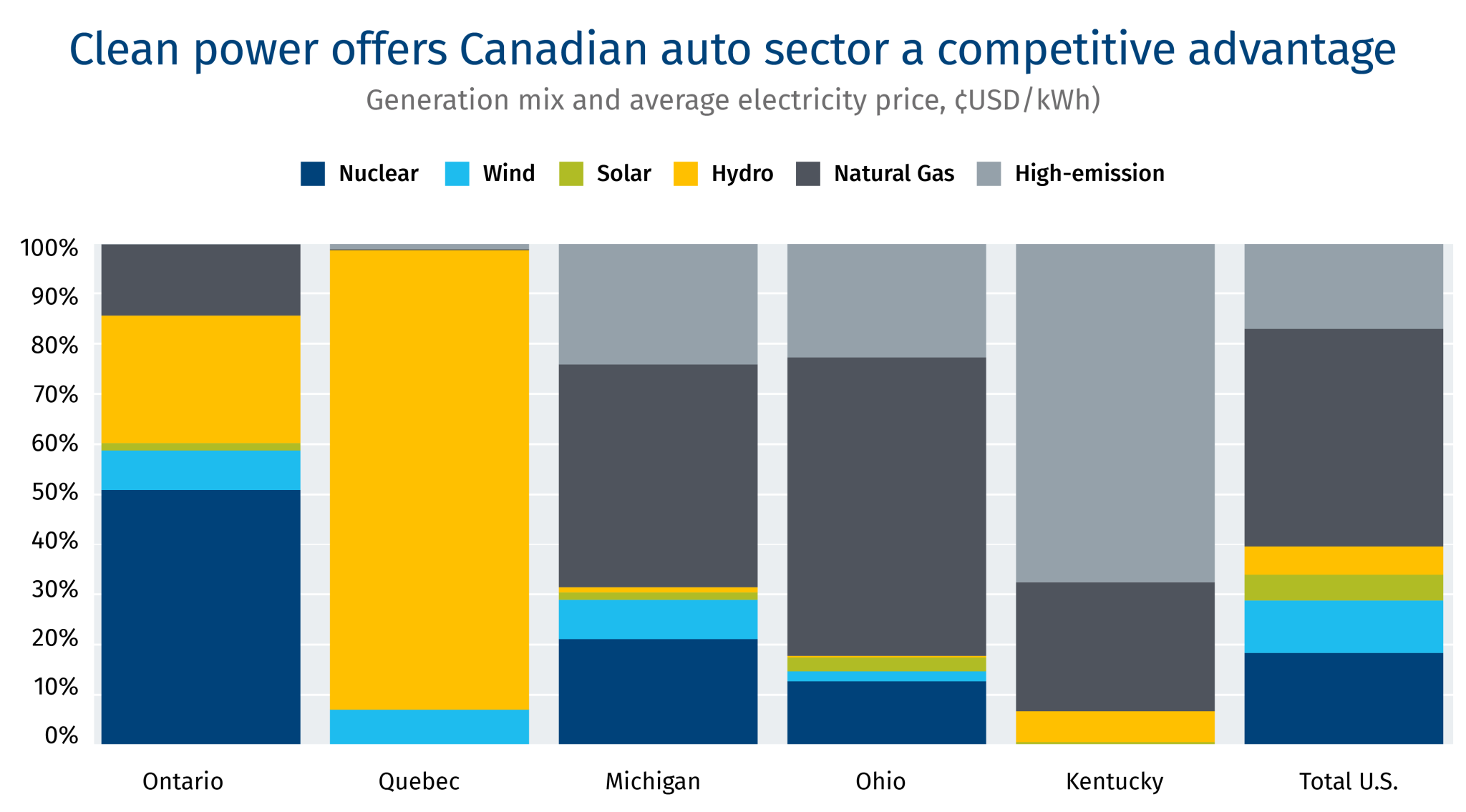

Canada’s critical minerals strategy bolsters Canada’s case. The mining, processing, and secondary manufacture of copper, cobalt, lithium, and magnesium—increasingly concentrated along a Northern Ontario-Quebec supply chain—strengthens battery integrity and reduces OEM exposure to Chinese inputs. Clean, affordable power bolsters the investment case. Ontario and Quebec’s low-emissions grids—Quebec’s electricity prices already sit below auto hubs like Michigan and Ohio—matter more in the smart-car era because electrification raises the power load. Computing, testing, and validation add to that demand. A cleaner, cheaper grid widens the margin and reduces carbon exposure on vehicle exports to increasingly emissions-conscious markets.

The Waterloo-Ottawa-Montreal corridor functions as a Silicon Valley of the North—with deep engineering talent in autonomy, AI, lightweight materials and embedded systems. This is important since, as McKinsey projects, the software, sensors, control units, and electronics segment of the global industry will grow from US$335 billion to US$520 billion between 2025 and 2035.

By 2040, Canada has an ecosystem where value is created across the stack—from the mine to the battery cell to the software-defined vehicle—anchored by assembly.

In this world, it’s clear the auto industry has become a technology platform, not just a manufacturing industry. The winning auto jurisdictions are not only judged on the number of units they assemble, but by the amount of value captured within each vehicle. Industrial ecosystems, not individual firms, bestow sustained competitive advantage.

Strategic tensions

- Canada strengthens its position inside the North America auto system but becomes more dependent (and more exposed) to U.S. policy volatility.

- If OEMs vertically integrate, pulling more EV content, software, and system integration in-house, Canada’s move into EVs and smart cars could be threatened.

- Restricting Chinese imports and foreign competition raises domestic vehicle prices and delays EV adoption, with implications for transportation emissions.

What needs to happen

- In exchange for duty-free access, Ottawa and the provinces could enter a critical minerals auto pact with the U.S., co-creating incentives (e.g., off-take agreements, stockpiling, price floors) that commercially de-risk private investment flows into the mining and processing of nickel, copper, lithium, graphite, aluminum and REE’s, bolstering North America’s strategic industrial supply chain.

- Canada, the U.S. and Mexico could take a coordinated approach to tariffing EVs, steel, aluminum, and auto parts outside the bloc to hedge against Chinese dumping. All three jurisdictions could align policy on the rules of origin and Most Favoured Nation tariffs to incentivize investment within the bloc.

- To ensure an abundance of competitively priced, non-emitting power, Ontario could embark on an aggressive expansion of hydro, nuclear, and wind power, expanding and modernizing the grid. Federal and provincial governments could massively expand charging infrastructure to bolster EV adoption.

- To win new mandates in R&D and software, Ontario and Quebec could consider co-investing with assemblers and parts manufacturers in shared research, testing and validation facilities. Eligibility thresholds for the Scientific Research and Experimental Development (SR&ED) program could be lowered to attract investment mandates in electronics, connectivity, autonomy, cyber security, and lightweight materials.

- Ottawa could consider reforming its immigration strategy to attract and retain professors and graduate students in computer and materials science, mechanical and chemical engineering, and AI and machine learning, deepening the ecosystem of competitively priced tech talent.

2. Slow Lane—Assembly survives, EV adoption slows,value grows elsewhere

Key assumptions

- CUSMA survives but is diluted

- EV adoption continues but is slower than expected

- Chinese OEMs expand their presence in Canada’s consumer market

- The U.S. continues to exclude Chinese vehicles

- Critical minerals and clean power lead to select mandate renewals

- Canada retains strategic value as a site for spillover capacity and assembly diversification

Drifting into the ‘Slow Lane’

Canada maintains its presence within the North American system, but its position and strategic relevance diminish. The trigger for the Slow Lane scenario is a sub-optimal outcome in trade talks. CUSMA survives the 2026 renegotiation but emerges narrower and less predictable. Canada secures a 10% headline tariff—a 5% effective rate on assembled vehicles—which compresses assembly margins close to zero. It’s not fatal to plant economics, but it changes the calculus for OEM investment allocation committees sitting in Detroit, Tokyo, and Stuttgart. And with the perennial threat of higher tariffs lurking in the background, investing in Canadian operations becomes prohibitively risky.

The Slow Lane is not a crisis—it sees Canada retain current production—but the higher value layers of the auto ecosystem grow elsewhere. Plants continue to run, retooling investments occur periodically, and assembly employment is largely maintained. Canada steadily cedes the investments, mandates, and capabilities that determine long-term industrial relevance, however. By 2040, Canada assembles 1.2 million vehicles, but Canada captures a smaller share of the value per vehicle over time.

Ironically, Canada’s auto industry was birthed behind protective tariffs on American-made vehicles.5 In the early twentieth century, a 35% National Policy tariff on imported cars was implemented to protect Canadian production from American competition.6 Rather than sustain Canadian automakers, the tariffs prompted American giants like Ford and GM to hop over the tariff wall and establish branch plants in Canada.7 This result: Canada became the world’s second-largest vehicle producer by 1930. By the turn of the century, Canada was assembling three million vehicles a year and ranked first when benchmarked against population. But the country lost that edge, assembling just 1.3 million vehicles by 2024.

The EV transition compounds the problem. Consumer adoption further slows after federal rebates expire—EV registrations fall below 10% nationally in 2025 and do not recover without sustained policy support. ICE and hybrid platforms extend their commercial life, which sounds like a reprieve for assembly but is a strategic trap: the investments Canada made in EV battery supply chains generate returns below their business case assumptions. EV supply remains stranded behind anemic consumer adoption, hindering Canada’s investability.

Meanwhile, the fast-growing layers of the industry migrate elsewhere. R&D mandates shrink as engineering and software functions consolidate around U.S. and Japanese assembly hubs. Contract revenues from OEM R&D programs thin out for the Windsor-Montreal corridor. STEM graduates take their skills to better-paying markets. Some of Canada’s homegrown giants remain globally competitive—but their growth happens in the U.S. Sun Belt, Mexico, and Germany, not in Ontario.

Top Auto Assembly Jurisdictions: 2024 vs 1999

2024 = 92 million units assembled globally

Rank | Country | Units Assembled | Share of | Units Assembled | Per Capita |

1 | China | 31.3 | 34% | 22 | 9 |

2 | U.S. | 10.6 | 11% | 31 | 8 |

3 | Japan | 8.2 | 9% | 66 | 3 |

4 | India | 6.0 | 7% | 4 | 15 |

5 | Mexico | 4.2 | 5% | 32 | 7 |

13 | Canada | 1.3 | 1.5% | 33 | 6 |

1999 = 56 million units assembled globally

Rank | Country | Units Assembled | Share of | Units Assembled | Per Capita |

1 | U.S. | 13 | 23% | 47 | 7 |

2 | Japan | 9.9 | 18% | 78 | 2 |

3 | Germany | 5.7 | 10% | 69 | 4 |

4 | France | 3.2 | 6% | 52 | 6 |

5 | Canada | 3.1 | 5.4% | 101 | 1 |

Sources: OICA; UN World Development Indicators

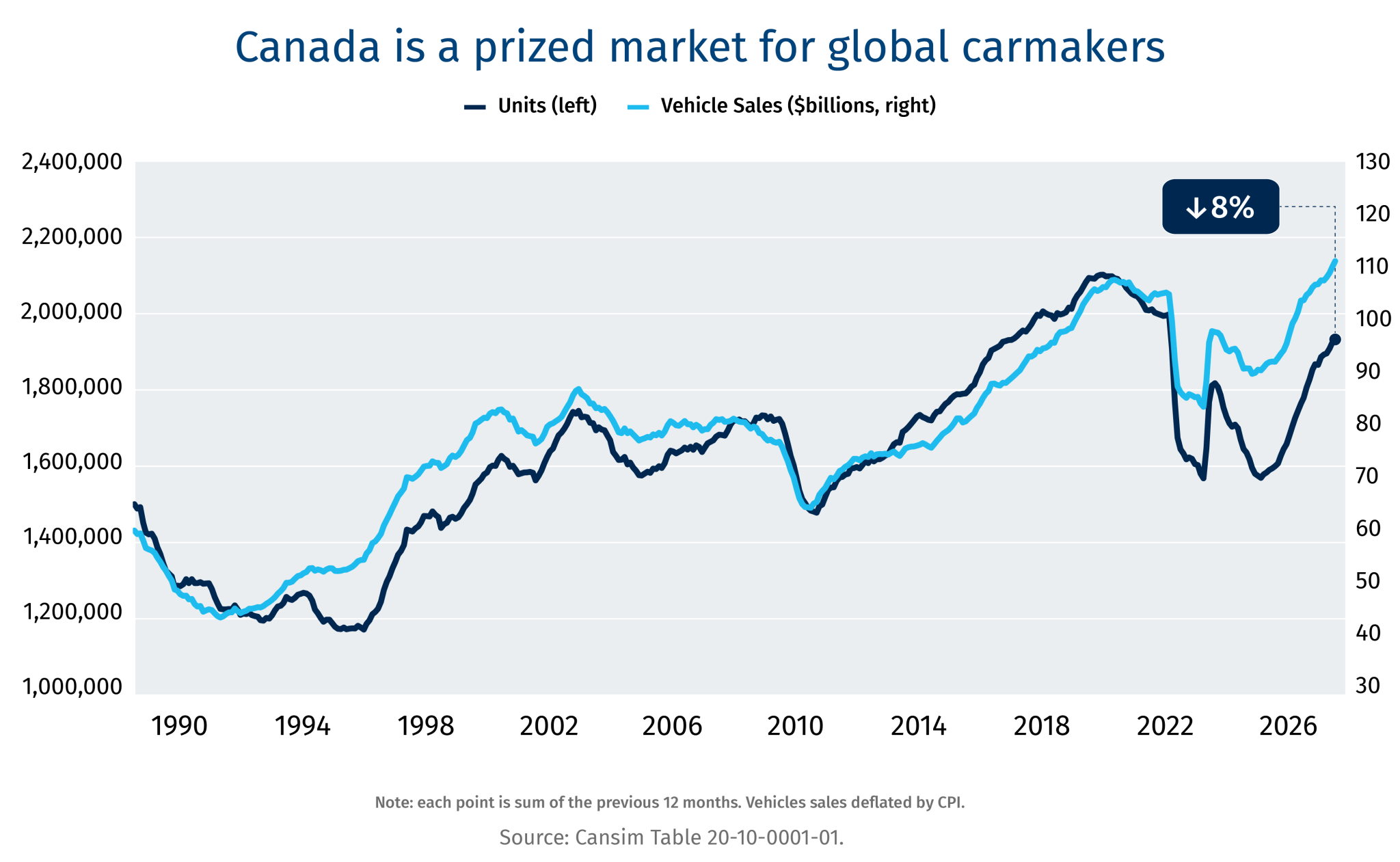

Canada’s aging consumer market reinforces the trajectory. Vehicle sales peaked in 2018 and have not scaled to those heights even as the population had risen by four million by 2025. The slowdown signals structural shifts in ownership patterns among largely urban, younger cohorts who increasingly rely on transit, ride-hailing, and car-sharing. A market that fails to grow in volume gives OEMs less reason to invest in Canadian production capacity.

Governments respond by competing for individual mandates—matching U.S. incentives on a project-by-project basis. The approach is costly and reactive. Each subsidy dollar spent defending existing assembly is a dollar not spent building capabilities—testing infrastructure, advanced manufacturing clusters, engineering talent pipelines—that would make Canada competitive for higher-value mandates. The Parliamentary Budget Office documented that public support for the auto sector between 2020 and 2024 exceeded private capital committed.8 In the Slow Lane, that ratio worsens.

By 2040, Canada still ships vehicles, but a growing share of the value inside those vehicles—the software stack, the battery chemistry, the electronic control systems—originates outside Canada’s borders. The ecosystem gradually thins out with each lost investment mandate.

It becomes clear that industrial erosion can occur gradually—not through collapse in unit production, but through declining value per vehicle. Value can migrate outside Canada’s borders while assembly remains within it. Industrial decline does not require plant closure; it occurs through missed investment cycles and diminished mandates.

Strategic tensions

- Canada preserves employment and assembly operations but fails to capture the high-growth, high-value segments of the industry.

- Governments increase subsidies to retain lower-value layers of the industry, raising fiscal costs without improving ecosystem competitiveness.

What needs to happen

- Canada’s current industrial policy is optimized for this scenario. Investment incentives are concentrated in construction investment, not operational subsidy, and the SR&ED program excludes activities that would have qualified otherwise.

- Public policy measures that lower power costs, improve tax competitiveness, reduce regulatory friction, or strengthen critical minerals supply chains are made sparingly, owing to fiscal constraints and industrial uncertainty.

3. On-Ramp—Canada turns to Eurasia for investment

Key assumptions

- Canadian exports to the U.S. are tariffed at 15%—7.5% effective

- Canada dangles market access as a carrot to attract foreign investment

- Modest tariffs are maintained on Chinese imports

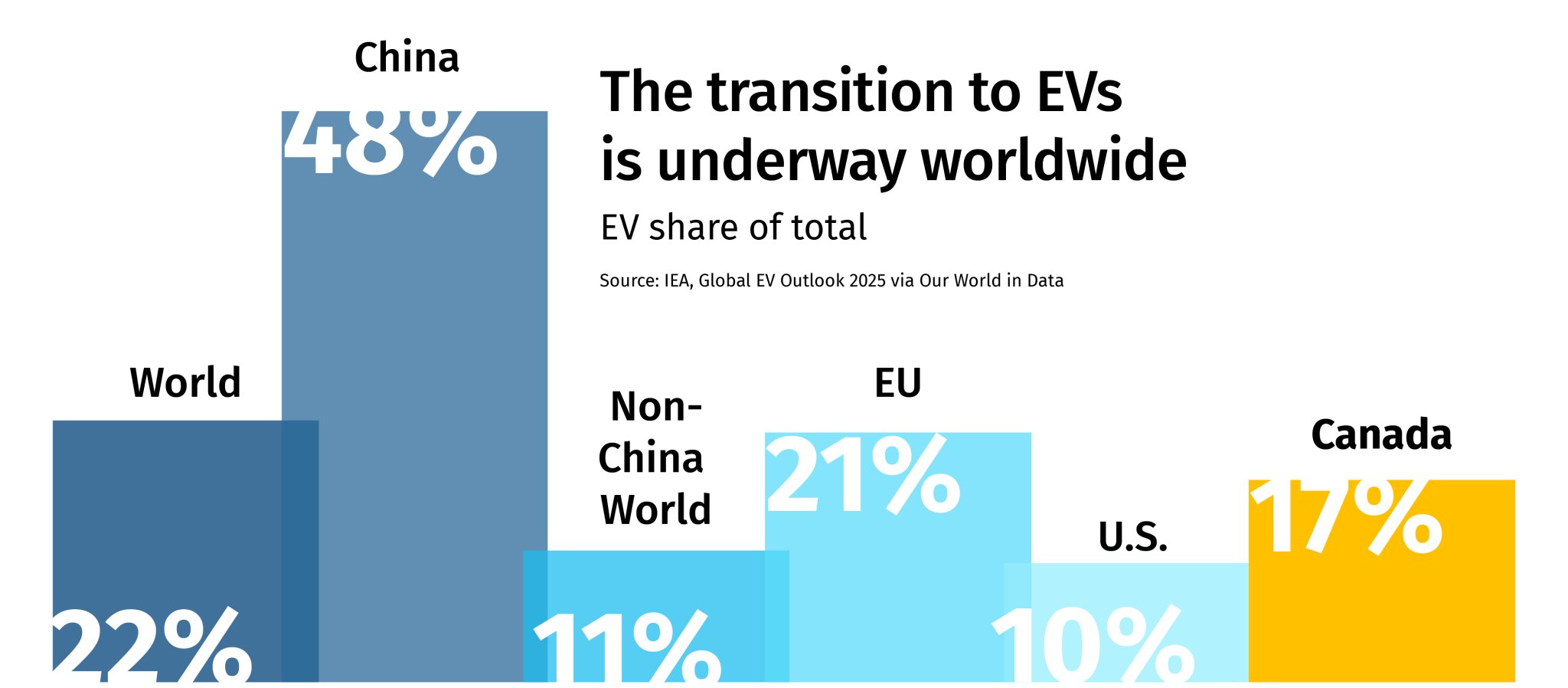

- The EV transition proceeds. By 2040, most vehicles sold in Canada are BEVs

- Canadian auto policy pivots to attract non-U.S. investment

Taking the ‘On-Ramp’

As North American integration slowly fragments under persistent tariffs—Canadian exports to the U.S. face an effective 7.5% rate—Ottawa recasts trade and industrial policy around a strategic remissions framework. OEMs that invest in Canadian manufacturing, R&D, engineering, or certification receive preferential market access. OEMs that do not are tariffed or exit. The definition of ‘investment’ is deliberately widened, encompassing not just assembly and parts but software development, testing facilities, systems integration hubs, and regulatory certification capacity.

This attracts a different mix of firms than the traditional North American model. Asian and European OEMs—Hyundai, BMW, BYD, and a cohort of emerging EV and software-defined vehicle producers—view Canada as a gateway market and a hedge against concentration risk in China and the U.S. Some build or expand assembly operations in partnership or independently; others focus on engineering, testing, and specialized production tied to global supply chains. The Windsor-Montreal tech corridor becomes a hub for compliance infrastructure and software validation, positioning Canada as a trusted jurisdiction capable of certifying vehicles for multiple regulatory markets simultaneously.

The purchasing power of the Canadian consumer also comes into play. Only Americans buy more cars than Canadians, per capita. Canadians spend nearly $110 billion annually on cars. And 90% of those vehicles are built abroad. That gives Canada the ability to leverage market access to secure investments. Canadian consumer preferences shape which OEMs make the investment. The Ford F-Series has been Canada’s best-selling vehicle for 15 consecutive years; the Toyota RAV4 and Honda CR-V dominate the SUV market. This truck-and-SUV profile aligns Canada’s consumer market with higher-margin, higher-content vehicles—the segment where EV and software integration creates the most value. An OEM that wins the Canadian consumer for its next-generation PHEV pickup or smart crossover earns returns that justify the cost of establishing a Canadian R&D or certification presence.

The EV transition proceeds in parallel. By 2040, BEVs represent the majority of vehicles sold in Canada, with PHEVs serving as the bridge for the truck and SUV segments where range anxiety remains most acute. OEMs without an assembly footprint in Canada pivot toward R&D investment, software integration, and certification—embedding themselves in Canadian value chains without owning a stamping press. Employment concentrates in high-skill STEM occupations: systems engineers, software architects, regulatory specialists, and battery chemists working along the Windsor-Montreal corridor.

Canada’s critical minerals endowment and clean power grid serve a dual function. They attract European or Asian OEMs seeking to diversify supply chains away from Chinese inputs, and they give Canada credibility as a partner in global battery supply chains. A vehicle manufacturer that sources lithium and copper through Canadian mining and processing operations builds a supply chain argument for regulators in Europe and the U.S.—and a reason to deepen its Canadian footprint.

By 2040, Canada assembles a million vehicles—the majority sold into its own market. Exports to the U.S. continue to decline, constrained by tariffs that impair competitiveness on lower-margin models. But the measure of Canada’s auto economy is not just units assembled. It is also the value embedded in modules, systems, and services that Canada increasingly exports: software stacks validated on testing tracks in Oshawa and demonstration facilities in Markham, battery modules assembled from Canadian minerals, and engineering services rendered for global vehicle programs. Canada is less central to North American production decisions and more embedded in global value chains—becoming a technology integrator. That’s a more defensible position than the branch-plant model it replaces.

Strategic tensions

- Trade diversification reduces dependence on the U.S., but risks provoking retaliation or reduced cooperation with Canada’s largest economic and security partner.

- Greater openness to Chinese OEMs raises national security, data governance, and supply chain integrity concerns.

What needs to happen

- Canada’s remissions framework could trade market access for investment. OEMs with Canadian operations could import a certain quantity of vehicles duty-free if they maintain Canadian-based production and investment commitments.

- To incentivize OEMs to re-tool their plants for high-mix, low-volume assembly, Ontario and Ottawa could co-create a capital cost offset fund (carefully designed and stringently monitored) and allow full immediate expensing of investments in automation, robotics, and digital manufacturing systems.

- Ottawa could help boost demand for Canadian-made vehicles through public sector fleet procurement and restriction of EV incentives to vehicles made in Canada.

4. Off-Ramp-Assembly anchors leave, industrial policy becomes reactive

Key assumptions

- The auto provisions of CUSMA are scrapped or severely weakened

- Canada opens its market entirely to Chinese imports in exchange for enhanced market access for Canadian agri-food and energy exports to China

- By 2040, most vehicles sold in Canada are BEVs

- Canadian industrial policy is transformed from proactive to reactive

Taking the ‘Off-Ramp’

The Off-Ramp begins with a pattern that has governed Canada’s auto industry for the past quarter century: plants continue to operate, but with diminished mandates. In this case, the mandates expire, as investment decisions tilt toward jurisdictions with lower tariff exposure and stronger policy certainty.

Historically, Canada did not lose assembly capacity during the contraction phase of the cycle; it lost it during the recovery, when the production footprint failed to return, having initially migrated to right-to-work states like Alabama and Tennessee and eventually to Mexico, which grew from 1.9 million units assembled in 2000 to 4.2 million by 2025. The Off Ramp is that dynamic, accelerated and made permanent through the collapse of CUSMA’s auto provisions.

Canada faces an effective tariff of 12.5%, which makes export-oriented assembly economically unviable. Companies continue to assemble vehicles, losing money, but try to hold onto market share for the valuable out-of-warranty parts and servicing of vehicles.

Canada follows Australia in allowing its auto industry to exit.9 By 2040, all auto assembly plants in Canada have shuttered. Low-cost BEVs from Chinese players BYD, Geely, and Leapmotor—already competitive on price and increasingly competitive on quality—fill the demand gap left by departing North American OEMs. By 2040, most vehicles sold in Canada are Chinese-built BEVs. For the Canadian consumer, vehicle prices fall and emissions decline.

For the Canadian auto ecosystem, the consequences are structural and severe. Plants anchor a supplier network that generates more economic activity than the facilities themselves. Tier 1 suppliers maintain their global competitiveness and continue exporting to U.S. and international customers. But the loss of domestic assembly volume erodes the density that makes Canadian Tier 2 and Tier 3 suppliers viable. Tool-and-die shops—of which Canada has few global peers—lose their customer base. Specialized component manufacturers close or consolidate. Some follow production south; others simply shutter operations. The fastest-growing segments of the auto industry—software, batteries and electronic control systems—were never deeply rooted and fade away without assembly to anchor them. The corridor’s density advantage, built over a century of branch-plant production, dissipates within a decade of losing its anchor customers.

The knock-on effects run deep. Steel mills in Hamilton and Sault Ste. Marie that have long supplied automotive-grade sheet metal lose one of their primary customers, as do chemical and plastics producers in Sarnia. The advanced manufacturing ecosystem spanning auto, aerospace, and defence loses the cross-pollination of skills, tooling capability, and engineering talent that assembly concentration made possible. Windsor, Oshawa, and Ingersoll face sustained economic decline: unemployment spikes, real estate prices fall, and tax bases erode, generating long-term pressure on social programs and government transfers.

Canada’s industrial policy pivots from active support to triage. Two separate tracks are pursued:

- Incentives to retool auto parts makers for defence manufacturing. Parts suppliers with the capital and capability to succeed in defence manufacturing are supported through retooling funds, accelerated depreciation, and public subsidy of workforce retraining.

- Transition the remaining workforce. Fiscal supports for OEMs are repurposed to facilitate displaced workers through retirement bridging, retraining programs, relocation.

The Off Ramp makes clear what other scenarios obscure: auto manufacturing is not just an industry. It is an ecosystem anchored by assembly. Remove the anchor and lose the density required for industrial dynamism across advanced manufacturing.

Strategic tensions

- The loss of auto ecosystem density accelerates broader industrial decline, weakening adjacent industries.

- By ending production subsidies, Canada preserves fiscal resources in the short run but loses industrial capacity and capability in the long run. Ironically, this threatens long-term fiscal capacity.

- The end of domestic auto assembly removes the rationale for protectionism. Canada opens its market entirely to Chinese EVs, which create more affordable options for consumers and reduces Canada’s transportation emissions.

- Policy focuses on managing industrial transition, redeploying capital and labour toward adjacent sectors such as aerospace, robotics, defence, and advanced manufacturing, and preparing the workforce for a painful transition.

What needs to happen

- Ottawa could co-create an industrial strategy with key provinces to support the transition of parts makers to defence equipment manufacturing, including financing supports, supply chain integration, workforce retraining, and re-tooling of facilities.

- To support affected workers and communities, Ottawa could strengthen employment insurance (across eligibility, benefit level, and duration) and, with Ontario, co-fund a targeted program to support auto workforce retraining, retirement bridging, and relocation.

- In anticipation of Chinese entry into the Canadian market, Ottawa could enact a connected vehicle security and data governance framework that covers software, hardware, and data localization.

Key considerations

Canada’s auto sector of the future will most likely be some combination of what’s outlined above. What’s critical is that public policy remains flexible and adaptive to any possible future. Cutting across all the scenarios are five strategic considerations that Canada must confront:

- Defend the North American manufacturing corridor. Canada’s industry was built on preferential access to the U.S. market. Roughly 90%-95% of auto exports flow south. This concentration creates both strength and vulnerability.

- Compete for value inside the vehicle. Vehicles are becoming technology platforms, with a growing share of value embedded in software, electronics, batteries, and systems integration. Historically, Canadian policy focused only on assembly volumes and employment. This policy focus needs to expand as automation advances and more value migrates toward engineering, software, electronics, and digital services.

- Use market access as leverage. By global standards, Canada’s domestic auto market is large and lucrative. Production capacity is presently geared towards export economics. Market access can function as a policy tool to secure investment commitments across a range of functions and assets, including manufacturing, R&D, testing, and regulatory certification.

- Deploy public capital strategically. Governments in North America, Europe, and Asia have committed tens of billions to auto manufacturing, battery supply chains, and advanced automotive technologies. Canada faces a difficult balance. Large-scale subsidies can attract investment, but they also expose public finances to significant risk. The Parliamentary Budget Office estimates that between 2020 and 2024, the $46 billion in pledged investment across the EV supply chain was matched with nearly $53 billion in government support. Taxpayers need to see value for money.

- Preserve the industrial ecosystem: Assembly plants anchor a network of suppliers, engineers, tool-and-die firms, logistics providers, and service businesses, but they also create demand for other heavy industries such as steel, aluminum, chemicals and plastics. If the assembly anchors weaken or close, the wider ecosystem that supports advanced manufacturing could lose the density required for dynamism and efficiency.

Download the report

End Notes:

- There are multiple different sources for global auto data, not all of which agree with each other. This analysis draws on RBC’s research and modelling, the source data of which includes IHS, Motor Intelligence, VDIK, CCFA, SMMT, ANFAC, UNRAE, and ACEA. A parallel data source is the International Energy Agency’s ‘Global EV Outlook’ via Our World in Data: https://ourworldindata.org/electric-car-sales.

- Statistics Canada Table: 27-10-0333-01.

- For an interesting analysis of the reforms needed to North America’s auto trade rules, see Helper and Tucker (2026).

- These capabilities are noted in the Tanguay Report (2018), pp. 6-7.

- Walter Redpath is credited with inventing Canada’s first car—the Redpath Messenger in 1903. However, large-scale production did not begin until the Detroit automakers entered. Ford Motor Company of Canada launched in Windsor (Walkerville) in 1904, followed by General Motors of Canada in 1918.

- While it was European engineers and inventors in the mid-nineteenth century who created the automobile—Karl Benz, Gottlieb Daimler, and Wilhelm Maybach—it was American entrepreneurs and inventors in the early twentieth century who transformed it from a luxury product into a massed-produced good. Detroit served as the hub of that transformation. At turn of the twentieth century, Ransom Olds, Walter Chrysler, and Henry Ford employed modern methods of production to birth a new industry. Windsor served as a beachhead for the Canadian industry largely because of geographic proximity.

- For a historical overview of Canada’s auto industry, see ‘Automotive Industry’ in the Canadian Encyclopedia.

- See Giswold (2024).

- The current Australian government pledged $23 billion for its Future Made in Australia plan, which sought to build advanced manufacturing capability in high-tech, high-skill areas.