The Path Forward

With geopolitical headlines dominating the short-term narrative, we outline the specific signposts we are watching to identify when the markets can move on. Key to any recovery in stocks will be the reopening of the Strait of Hormuz, and in recent days we have seen halting progress as negotiations seem to be taking two steps forward, one step back. Despite renewed geopolitical turmoil and the surge in energy prices, U.S. economic data has held in strong, while consumers have kept up their spending patterns despite $4 gasoline. As markets have moved higher as they contemplate the end to hostilities, we will soon have a new data point to examine as corporate earnings season is right around the corner.

With geopolitical headlines dominating the short-term narrative, we outline the specific signposts we are watching to identify when the markets can move on. Key to any recovery in stocks will be the reopening of the Strait of Hormuz, and in recent days we have seen halting progress as negotiations seem to be taking two steps forward, one step back. Despite renewed geopolitical turmoil and the surge in energy prices, U.S. economic data has held in strong, while consumers have kept up their spending patterns despite $4 gasoline. As markets have moved higher as they contemplate the end to hostilities, we will soon have a new data point to examine as corporate earnings season is right around the corner.

Robin Gullason

Associate Portfolio Manager & Lead Strategist

April 1, 2026

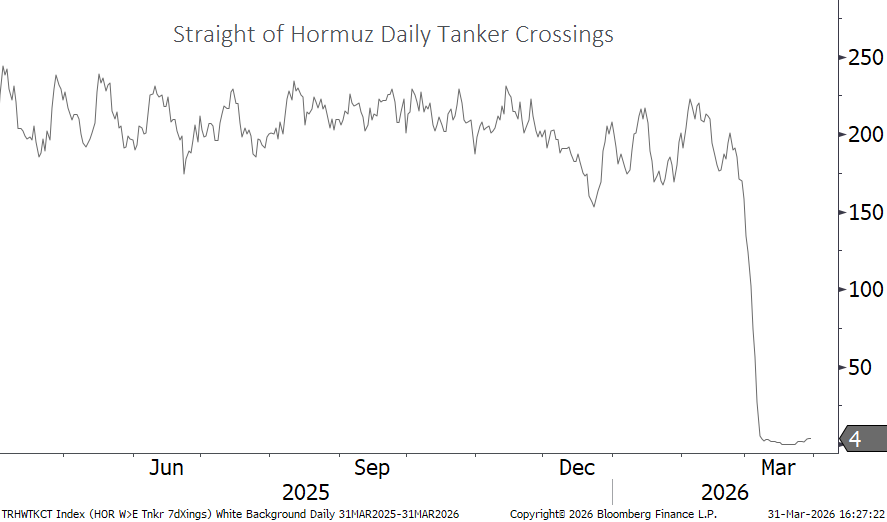

- There is one priority on the mind of markets today, and that is when the Strait of Hormuz will open for transit once again.

- Markets staged a rally early in the week on optimism that a timeline has been established for the end of hostilities but significant uncertainty remains, as evidenced by the President’s speech Wednesday night.

- After the post-Liberation Day rally last year, investors have been conditioned to “front run” expected White House policy announcements.

- There are heavy incentives on both sides to move on, but it is unclear how serious ongoing negotiations are.

- We are certainly seeing optimism that hostilities in the middle east will soon be on the wane, but in our view it is too early to signal the all clear.

- U.S. economic data has been holding in well, and we will receive the latest corporate earnings releases in the coming weeks.

- Our advice throughout has been to stay the course, as markets are likely to resolve higher when the strait reopens. The typical pattern for acts of war has been a sharp selloff followed by a recovery in the weeks and months after so long as economic growth continues.

- We cannot fully discount a prolonged closure of the strait and the implications thereof, though we would note the Canadian and U.S. economies are among the best positioned in the G7 for such an outcome.

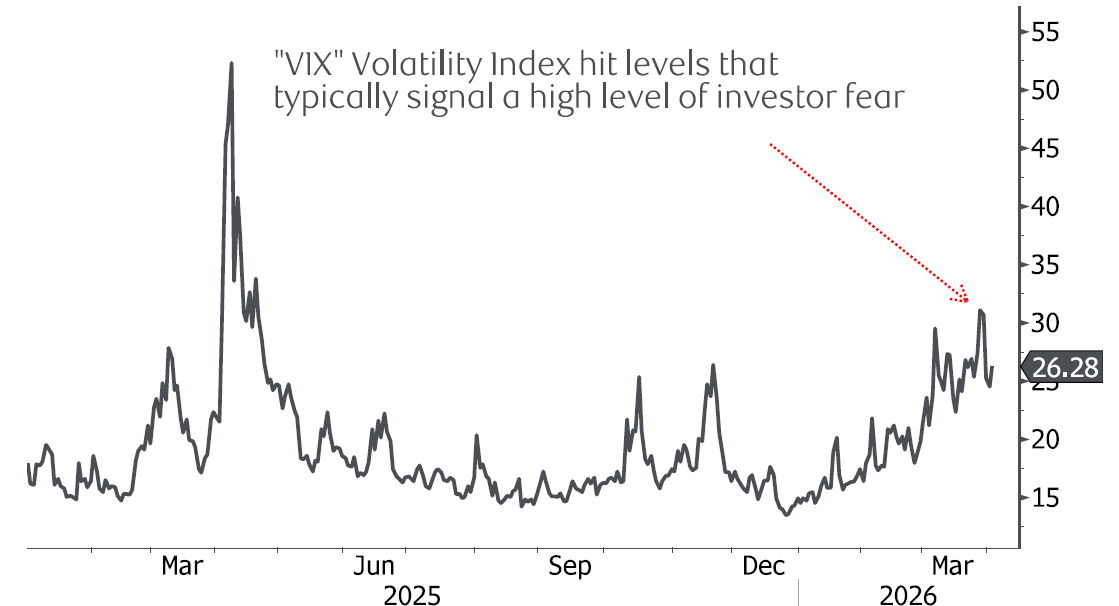

The typical market response to acts of war has been a sharp selloff followed by a cooling off period of a couple of weeks, then a resumption higher in prices so long as the economy continues to grow. Despite the scary headlines, this is what has happened the vast majority of the time. The evidence we have in hand thus far is following this historical pattern. Also fitting with this pattern has been a spike in the so-called VIX volatility index, known as Wall Street’s “fear gauge”. Time and again a jump in the market’s measure of investor trepidation has proven a timely entry point into stocks.

Source: Bloomberg

The Rally of Expectations

In recent days, a "risk-on" sentiment was palpable across major indices, driven by diplomatic whispers suggesting that the daily bombardments throughout the middle east were nearing a conclusion. Messaging from the White turned somewhat more challenging on Wednesday night, causing stocks to walk back some gains. As such, we remain somewhat cautious – a lack of progress on negotiations may lead to further escalation up to and including “boots on the ground” in Iran. While we don’t think this is on the U.S.’s wish list, we cannot fully cast the possibility aside.

We fully understand why investors are attempting to look two steps ahead. We have all been conditioned by the post-Liberation Day rally of 2025, an event that saw strong gains for those who moved early. This has created a strong incentive to "front-run" expected White House policy announcements. The fear of missing out on a massive relief rally often outweighs the perceived risks of a diplomatic collapse, leading to the aggressive buying patterns we witnessed this week.

Diplomacy vs. Quagmire

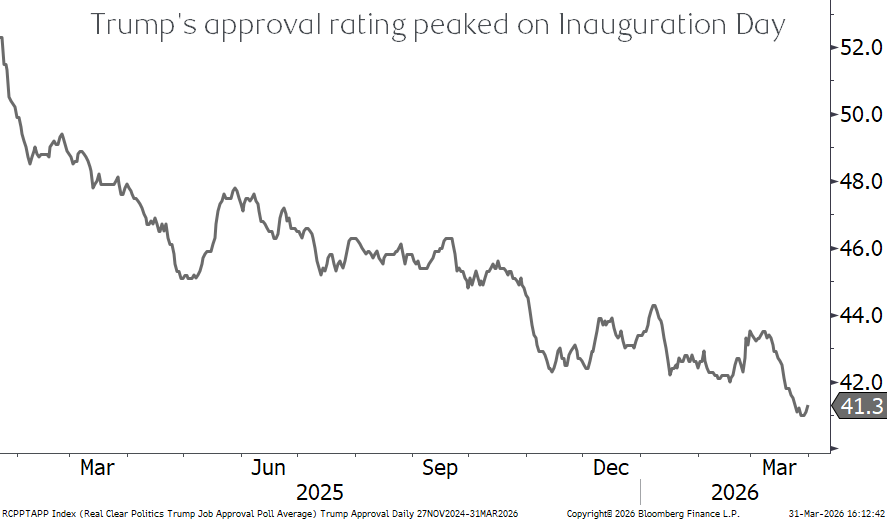

There is no denying the heavy incentives for all parties involved to move on. For Iran and its Gulf neighbours, the economic pressure is real, and exacerbated by heavily reduced oil export revenue. For the U.S., the inflationary pressure of disrupted supply chains is a political liability. Indeed, gasoline prices in the U.S. now average $4/gallon, while President Trump’s approval numbers plumb new lows and the mid-term elections loom. It seems clear the U.S. is looking to extricate itself from this situation but it may not be up to them at this point. What we do know is that the American public’s appetite for another drawn-out middle eastern conflict is quite low, to the point where polling suggests the Democrats now have a fighting chance of winning both the House and the Senate.

Economic Resilience

While the geopolitical drama captures the headlines, the underlying fundamentals of the U.S. domestic economy provide a necessary counterweight. U.S. economic data has been holding in remarkably well, showing a resilience that many analysts didn't expect. Now that the U.S. is an energy exporter, the net impact of higher oil prices has a negligible impact on GDP growth. The main concern is that consumer spending will be dented. Recent data suggests it remains solid and the labor market has avoided the significant cracks that usually precede a major downturn. This resilience will face a moment of truth in the coming weeks. As the focus on the Strait continues, we are entering the window for corporate earnings releases. These reports will offer a ground-level view of how companies are managing the dual pressures of geopolitical uncertainty and high energy costs. If earnings beat expectations, it could provide the fundamental floor for a market that has seen valuations measured by forward price/earnings ratios fall 15% in aggregate.

The Path Toward De-escalation

Every day it seems like the media floods us with a dizzying amount of news surrounding the war in Iran. Negotiations to end the war appear to be taking place in the shadows, but the two sides contradict each other so much it is difficult to tell where we are. While the media moves on to the next headline, the global financial landscape is currently fixated on a single, narrow geographical chokepoint. While inflation data and central bank rhetoric typically dominate the headlines, lately they have been largely relegated to the sidelines. There is one undisputed priority on the mind of markets today: when the Strait of Hormuz will open for transit once again. Given the importance of the price of oil to the global economy, markets are watching this development over all others right now.

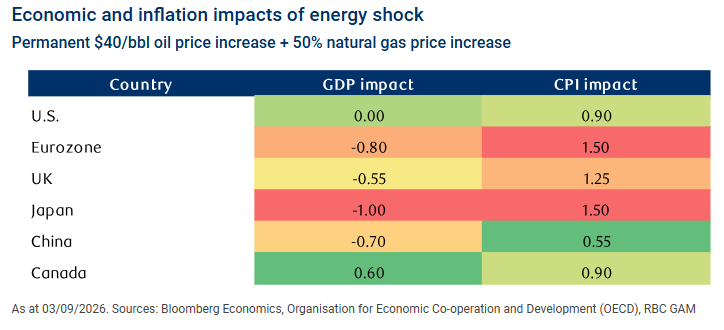

We need to consider the possibility that the Strait of Hormuz remains effectively closed for a long period of time and what those implications may be. We note that we are already seeing workarounds by the likes of Saudi Arabia shipping via the Red Sea and for better or for worse, Iranian crude continues to flow, mitigating the impact somewhat. A prolonged shutdown likely puts increased pressure on the global economy, but there was a time not too long ago that $100 oil was the norm and the global economy continued to grow, while the energy intensity of GDP growth declines each year. As seen below, the U.S. and Canada are the least impacted among the G7, providing a degree of insulation for portfolios with a North American focus, especially considering many of the market’s largest contributors (i.e. technology) aren’t materially impacted by oil prices. Nonetheless this is a risk that we are actively monitoring, and we stand ready to adjust portfolios if required.

Invested, but vigilant

For the time being, our strategy remains one of cautious participation. Because of the possibility of a quick resolution, our advice to investors has been to stay the course. The incentives for peace are real, and in our view time is the necessary ingredient for tensions to calm. Given the binary nature of the market’s biggest worry, the number of signposts we can use are limited. We are watching the headlines, and we are also weighing the data. In a market front-running the White House, the "fact" must eventually live up to the "rumor" before a sustainable recovery can take hold.

The Harbour Group - 416-842-2300

Putting you first, every time, to help you navigate the complexities of managing your wealth. All of our team members, all of our resources, all of our collective insight: ALL FOR ONE: YOU™.

The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc. and its affiliates may have an investment banking or other relationship with some or all of the issuers mentioned herein and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. RBC Dominion Securities Inc. and its affiliates also may issue options on securities mentioned herein and may trade in options issued by others. Accordingly, RBC Dominion Securities Inc. or its affiliates may at any time have a long or short position in any such security or option thereon. Mutual funds are sold by RBC Dominion Securities Inc. There may be commissions, trailing commissions, management fees and expenses associated with mutual fund investments. Read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member CIPF. ®Registered Trademark of Royal Bank of Canada. Used under licence. RBC Dominion Securities is a registered trademark of Royal Bank of Canada. Used under licence. ©Copyright 2019. All rights reserved.