2026 TPWP Outlook: Navigating the Path of Disciplined Optimism Does three back-to-back-to-back years rule out a strong 2026?

Each year in early January, RBC Dominion Securities hosts its annual portfolio management conference. Bringing together top-tier money managers, strategists, and analysts, the event provides a critical forum for stress-testing our investment theses for the year ahead. The 2026 conference was defined by a notable energy: a clear optimism regarding corporate earnings, tempered by the complex geopolitical crosscurrents currently shaping the global horizon.

Each year in early January, RBC Dominion Securities hosts its annual portfolio management conference. Bringing together top-tier money managers, strategists, and analysts, the event provides a critical forum for stress-testing our investment theses for the year ahead. The 2026 conference was defined by a notable energy: a clear optimism regarding corporate earnings, tempered by the complex geopolitical crosscurrents currently shaping the global horizon.

Troy Private Wealth Partners

January 30, 2026

Each year in early January, RBC Dominion Securities hosts its annual portfolio management conference. Bringing together top-tier money managers, strategists, and analysts, the event provides a critical forum for stress-testing our investment theses for the year ahead. The 2026 conference was defined by a notable energy: a clear optimism regarding corporate earnings, tempered by the complex geopolitical crosscurrents currently shaping the global horizon.

The Case for Resilience

The prevailing consensus among analysts is one of resilient confidence. We are seeing strengthened earnings visibility across key sectors - most notably in technology, where AI-driven productivity gains are materializing; sustainable energy, which is transitioning into post-subsidy innovation; and consumer staples, which continue to show robust demand.

Corporate leaders are providing guidance that points to operational efficiency and margin expansion, supported by stabilizing input costs and more adaptive supply chains. This visibility, earned through years of volatility, suggests that companies have emerged from recent cycles leaner and better positioned to capitalize on growth pockets.

Market Forecasts and the "Geopolitical Premium"

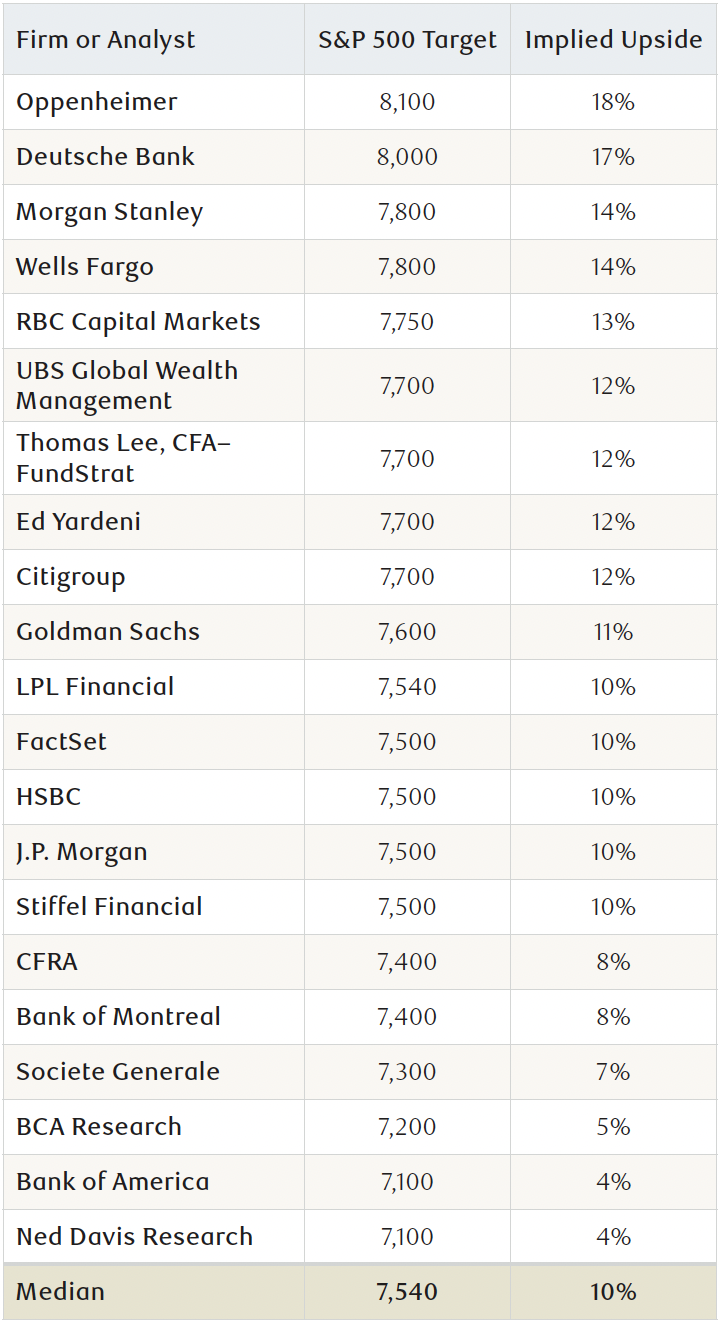

While we emphasize preparedness over mere prediction, current market data provides a useful compass. The median forecast for the S&P 500 currently stands at 7,540—representing a +10% increase from the 2025 year-end. This consensus is built on expectations of stabilizing inflation and accommodative monetary policy tailwinds.

Source: Bloomberg

However, the wide spectrum of targets—ranging from RBC Capital Markets’ bullish +13% to more cautious estimates of +5%—underscores the importance of not fixating on a single headline number. History reminds us that strategist targets often miss the mark significantly; for example, 2025's actual returns were nearly 50% higher than the median forecasts made a year prior.

Crucially, portfolio construction must now account for a "geopolitical premium". This involves favoring companies with robust contingency planning and exposure to secular growth themes that are less susceptible to political shifts.

The Psychology of the Market

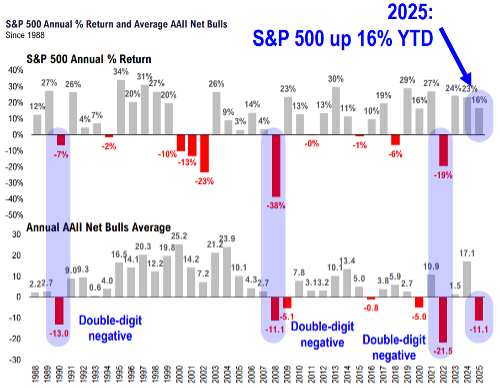

Source: Fundstrat, Bloomberg, AAII

Sentiment remains a powerful contrarian indicator. When the AAII "Net Bulls Average" falls below -10% (deep bearishness), the S&P 500 has historically delivered positive returns the following year in every instance since 1987. Conversely, extreme euphoria (above +20%) has led to flat or negative returns 75% of the time. This data serves as a reminder that markets often "climb a wall of worry".

Charting the Path Ahead

It is natural to feel uneasy when the headlines are dominated by crisis. However, looking back at the last 30 years, we see that market growth has persisted despite constant global turmoil.

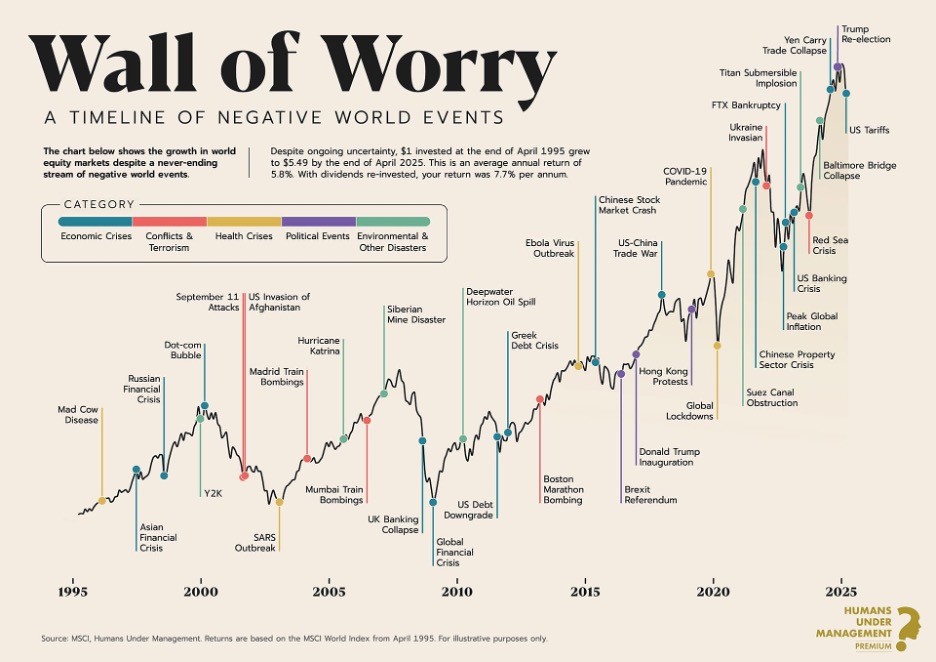

The MSCI world Index depicted below (1995-2025) illustrates that while ‘black swan’ events cause temporary dips, they have historically been followed by recovery and growth.

Source: MSCI, Humans Under Management. Returns are based on the MSCI World Index from April 1995. For illustrative purposes only.

- The 2020 Pandemic Crash: A 34% plunge in just 33 days, followed by a historic rebound fueled by innovation and stimulus.

- Supply Chain & Inflation (2021–2022): Port closures and the Fed's fastest rate-hiking cycle since Volcker led to widespread "hard landing" predictions that never materialized.

- Geopolitical Flashpoints: We have navigated everything from U.S.-China trade tensions to the current 2026 military intervention in Venezuela.

The recent events in Venezuela also known as “ Operation Absolute Resolve” and the capture of Nicolás Maduro in January 2026, have introduced immediate volatility into energy markets and global shipping. While these events send shockwaves through the headlines, markets are forward-looking discounting machines; they price in worst-case scenarios swiftly and then pivot toward recovery narratives.

Our strategy for 2026 remains one of disciplined optimism. While the global landscape remains complex, our commitment to a data-driven, resilient strategy is unwavering. The road ahead will not be without its challenges, but we are prepared for it. Thank you for your continued partnership and trust as we navigate the path ahead.

Wishing you all the best in 2026.