Michael Wilkie

April 10, 2026

A Word from Mike

Hello,

Geopolitics continue to dominate the narrative for financial markets and major economies. I discuss what’s transpired, macro developments, and earnings expectations in more detail below.

Geopolitical Headline Whipsaw

After weeks of trading deadlines and escalating rhetoric, the U.S. and Iran reached a temporary ceasefire contingent on Tehran reopening the Strait of Hormuz (SoH) to commercial shipping. The agreement has reduced the likelihood of worst-case economic outcomes stemming from a severe disruption to energy markets. Markets responded constructively: equities recovered a portion of recent losses, oil prices pulled back, and bond yields declined. Lower energy costs, if sustained, should ease pressure on consumers and businesses, moderating concerns around the inflation backdrop and earnings outlook.

Despite the collective sigh of relief, the prudent interpretation is likely “less bad” rather than “problem resolved.” The ceasefire provides time for both sides to find common ground and, ideally, a framework that lets each claim some version of a win. For many economies and businesses, a challenging second quarter may be largely unavoidable. What remains to be determined is whether that headwind gives way to a gradual normalization or renewed disruptions. Should the ceasefire hold and eventually become permanent, I believe the most likely outcome remains a period of slower growth and somewhat elevated inflation before conditions improve later in the year.

Global Economic Resilience Tested

The softening observed two weeks ago has become more broadly visible. The latest business surveys suggest growth moderated across major economies, with the pressure most evident in consumer-facing areas. Globally, hiring trends have cooled and cost pressures have risen, reflecting the effects of higher energy prices.

In Canada, conditions are mixed. The manufacturing sector stalled and services activity contracted for a fifth consecutive month as consumers delayed spending decisions, but business confidence reached a six-month high on optimism around trade prospects and a potential resolution in the Iran conflict. Overall activity levels remain consistent with continued expansion, albeit at a slower pace than before the war.

In estimates published before the ceasefire, RBC Global Asset Management’s forecasts aligned with the direction now visible in the data. They estimated that a sustained energy price shock could lift inflation by roughly one percentage point in North America, and by more in Europe and Japan. Growth impacts vary by region, with Europe and Japan again bearing the brunt of a slowdown, while Canada’s position as a net energy exporter could translate into a modest boost to growth.

Eyes On Corporate Guidance

Despite heightened uncertainty, corporate profit estimates in Canada and the U.S. have continued to move higher. However, upward revisions have been concentrated in the energy and technology sectors. Outside of these companies, revisions have been limited, suggesting analysts have yet to fully incorporate the softer economic backdrop.

Earnings forecasts can lag economic developments, which is why the upcoming corporate reporting season will likely carry more weight than usual. Management guidance on business conditions and consumer demand will provide valuable signals on whether the current trajectory in earnings is sustainable and whether it can provide fundamental support for equity markets.

Takeaway

The economy and markets remain in a “stress testing” phase, but the ceasefire represents an encouraging step toward stability. A key indicator I am monitoring is the normalization of shipping activity through the SoH, which would signal improving commodity supply constraints. While periods of rapid news cycles and sharp price swings in both directions can challenge investor confidence, these moments underscore the importance of maintaining a balanced perspective. I believe portfolio allocations should be closely aligned to long-term target weights, while acknowledging that markets may experience renewed bouts of volatility as U.S.-Iran negotiations unfold.

Highlights

An evolving role for the dollar and the Fed

With war and geopolitics dominating headlines, it’s easy to overlook slower-moving changes in the investment background. We think it is important for investors to re-examine some long-held assumptions on policy impacts and investor behavior.

Regional developments: Liberals near majority and Canada’s trade deficit widens; U.S. equity markets remain optimistic despite turbulence in Middle East; European fingers are crossed for a lasting U.S.-Iran ceasefire; Asian risk assets remain sensitive to developments in the Middle East.

Please take some time to review the Global Insight Weekly.

Global Insight Monthly: April 2026

I am pleased to share the latest investment strategy report from RBC Wealth Management—Global Insight, which provides our current thoughts on asset classes, the economy, and timely issues that impact investment strategy.

Full report: Global Insight

This month’s highlights:

Global equity: Buckle up but don’t give up

Amid the uncertainty swirling from the Middle East crisis, several forces are pushing and pulling on stock markets. Investors should expect bouts of unnerving volatility, but we argue portfolios should remain committed to equities up to but not beyond their long-term targeted exposure.

Global fixed income: Central banks going out for a hike

One month ago, markets had largely expected a relatively tranquil backdrop where most global central banks were at least likely to keep interest rates steady, if not biased toward further cuts this year. But markets are now bracing for the potential of multiple rate hikes from multiple central banks.

Regional commentary

Our regional analysts present their views of equity and fixed income markets, the outlook for commodities and currencies, and how to position portfolios.

Construction on Canada’s first “nation-building” project begins

Prime Minister Mark Carney was in Contrecoeur, Que., 45 kilometres outside Montreal, for the groundbreaking of what the government says will be the largest Canadian port expansion ever. The government says the project, located on the south shore of the St. Lawrence River, will increase capacity of the Port of Montreal by about 60%. This is the first of a series of nation-building projects that the government is fast-tracking with the aim of diversifying its economy in the face of growing trade tensions with the U.S.

Bank of Canada weighs inflation risks amid energy price shock

Minutes from the Bank of Canada’s March deliberations show policymakers see a growing tension between supporting a weak economy and containing inflation following a sharp energy-price surge tied to the Iran war. The central bank held its benchmark rate at 2.25% on March 18, noting it has room to wait as inflation remains close to its 2% target and underlying price pressures appear contained. However, gasoline prices have risen by nearly one-third over the past month, and officials expect this to push headline inflation above target in the near term. Governing council members outlined a difficult trade-off: raising rates could further slow already weak growth and a soft labour market, while cutting rates risks fuelling broader inflation. Markets have shifted expectations accordingly, now pricing in at least a half-percentage-point increase in rates by the end of 2026. Policymakers highlighted that higher energy costs lifting inflation expectations, or weak economic conditions limiting the pass-through of those costs into broader prices. The Bank signalled it will closely monitor whether price increases spread beyond energy and become persistent, emphasizing a cautious, data-dependent approach.

U.S. eyes targeted changes to USMCA via bilateral protocols

U.S. Trade Representative Jamieson Greer recently signaled that the upcoming July 1st review of the USMCA is likely to preserve the core trilateral framework while introducing two separate bilateral protocols with Canada and Mexico to address country-specific issues. While acknowledging the key "load-bearing pillars" of the agreement remain effective, U.S. officials view modifications as necessary given differing trade balances, labour conditions, and policy priorities across trading partners. Negotiations are already underway, though officials expect talks to extend beyond the formal review date, likely entering a multi-year renegotiation window rather than a straightforward 16-year renewal. Both Canada and Mexico continue to favour maintaining the trilateral structure, albeit with bilateral components. Key U.S. concerns include Canadian dairy quotas, digital rules, procurement policies, and Mexican labour enforcement and energy investment restrictions. Broader U.S. objectives include tightening rules of origin, aligning external trade policies, and limiting Chinese supply chain exposure, alongside addressing existing tariff disputes.

U.S. job growth rebounds in March but Iran war clouds outlook

U.S. job growth rebounded in March, with nonfarm payrolls rising by 178,000 - well above expectations and marking the strongest gain in over a year - following a sharp, downwardly revised decline of 133,000 in February. The unemployment rate also edged lower to 4.3%, though the improvement was driven largely by a drop in labor force participation as roughly 396,000 individuals exited the workforce, pushing the participation rate below 62% for the first time since the pandemic. Job gains were led by healthcare, construction and hospitality, supported in part by the end of strikes and improved weather conditions, while employment declined in federal government, financial activities, and segments of professional services. Despite the stronger headline, underlying details were more mixed, with average hours worked falling and wage growth slowing to 3.5% year-over-year, the weakest pace in nearly five years. Overall, the report suggests the labor market remains resilient but is gradually cooling, and while it likely predates any potential economic impact of the Iran conflict, the stronger-than-expected data may reinforce expectations for the Federal Reserve to remain on hold as it assesses evolving inflation risks.

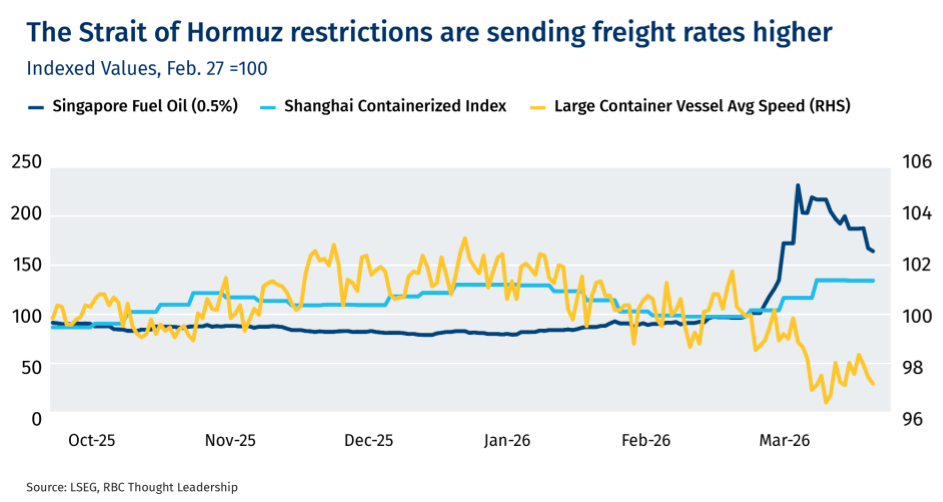

Chart of the day

Trade Zone: The Middle East conflict is a slow-moving shock to the cost of moving goods

Interesting tidbits

- Amazon is imposing a 3.5% surcharge on Canadian and U.S. sellers. The e-commerce company blamed elevated fuel and logistics costs for its decision. Other North American shippers, such as FedEx and UPS, already have fuel surcharges in place that are adjusted weekly, based on the average price of fuels such as diesel or kerosene-type jet fuel. Other companies are also slapping new surcharges, with Air Canada Vacations, Porter Airline and Air Transat rolling out fuel surcharges. Meanwhile, DoorDash and Lyft introduced a program meant to help their drivers offset higher fuel costs.

- 17.2%. The chance of winning any Lotto Max prize—better than the current 14.2% odds before the lottery introduces new changes. The odds of winning the jackpot? Now worse at one in 33.4 million, from 33.3 million before.

- Hollywood is facing a jobs crisis. Tinsel town has seen a 30% drop in employment from the 2022 peak for actors, costume designers and other professions involved in the Los Angeles production hub. Craftspeople worked 36% fewer hours in 2025 compared to 2022, while on-location production activity in the city has dropped considerably for TV, feature films and commercials. Production of major movies also fell from 251 in 2021 to 159 in 2025 in the U.S., with locations like Canada, the U.K. and Australia luring producers with favourable tax incentives.

Today’s funny

“I find that worrying about what might happen takes my mind off worrying about what has happened.”

REMINDER: Most of my new clients come to me via word of mouth as I don’t advertise or engage in marketing programs. Please keep my team in mind if you hear of anyone with over $1 million in investable assets who is in need of wealth management services.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.