Paul Chapman

Portfolio Manager & Wealth Advisor

January 29, 2026

“Our greatest weakness lies in giving up. The most certain way to succeed is always to try just one more time. I never view mistakes as failures. They are simply opportunities to find out what doesn't work.” – Thomas A. Edison

Note that the contents of this memo are all my thoughts, and not the views of RBC Dominion Securities. As well, no part of this content was AI-assisted or created.

[YOU CAN LISTEN TO THE ABBREVIATED PODCAST VERSION OF THIS NOTE HERE]

Friends & Partners,

Well, January was anything but uneventful – I think we got a year’s worth of events in one month. The US government extracted and replaced a foreign leader (Venezuela), the US government subpoenaed the Federal Reserve, the US government threatened to invade Greenland, the US government threatened 100% tariffs on its largest trading partner (Canada!)… to name a few.

The theme of 2026 so far (and admittedly it’s very early) is that, seemingly every week, investors must consider and grapple with some sort of volatile geopolitical, policy or trade headline. Yet, so far, despite these headlines, markets have remained largely stable. Let’s see if that persists..

So, many are wondering: Why are markets ignoring all these headlines?

The simplest answer is because the core factors that determine stock prices remain healthy – that is, earnings growth and underlying economic growth. Corporate earnings growth is expected to be more than 10% between 2025 and 2026, and while reported corporate earnings have been mixed, that’s mostly been from guidance, and few companies are talking about reducing their expected 2026 earnings. Economic growth, meanwhile, is so far stable. The unemployment rate remains in a low historical range; we’re not seeing a spike in jobless claims and activity across industries is generally ‘fine’. So it is these fundamentals that are acting as a buffer against policy chaos. As long as the fundamentals remain in place, markets will continue to be resilient in the face of policy chaos.

However, it is important that investors do not become complacent and fall into a trap of thinking “nothing matters” and that stocks just always rebound – that feels like the playbook recently, but believe me, it isn’t always this way. So far, none of these volatile policy headlines have negatively impacted expected earnings growth or overall economic growth; however, neither are impervious.

So what can make the market go down?!

This isn’t something you’re hearing about from many sources, as evidenced by the fact that Bloomberg found none of the 21 market strategists surveyed at the end of 2025 expected stocks to decline in 2026. All 21 strategists confidently expect a continuation of the 3-year bull market, and while it’s reasonable to expect the majority of analysts to expect a rally (analysts are by default mostly bullish), the reality is the unanimity of positive opinions struck me as a potential red flag in and of itself – too much agreement on anything in markets is often a dangerous proposition.

Things that could present themselves to weaken markets (not a forecast!):

· A recession (finally) comes to fruition, and/or the economy suddenly slows: No one thinks this can happen anymore it seems. Perhaps everyone is now ignoring warnings after being fooled a few years ago (when everyone thought a recession was imminent in 2022), providing excuses as to why we should ignore bad data. Nobody is talking recession at the moment. We begin 2026 with the unemployment rate at a 4-year high, and while most economic data remains generally solid, the reality is that the economy is facing headwinds from years of elevated inflation (affordability) and threats to employment from technology (AI and others). The bottom line is we are in a “no-hire/no-fire” labour market that can turn to a “downsizing” labour market very quickly. Employment has been the lynchpin in the economy that’s allowed people to weather years of higher inflation, but if the unemployment rate rises to and through 5.0%, then the idea of an economic slowdown will be on the table. A contracting economy is not a thing from history books, it can happen...

· A steep rise in bond (Treasury) yields: The last time Treasury yields rose sharply and unexpectedly was 2022, and the stock market fell into a steep bear market. The reality is that upward pressure on Treasury yields could be building in 2026. There are several factors that could push Treasury yields higher: Reversal of the IEEPA tariffs and the selection of the new Fed Chair. Of the two, it’s the latter I’m more concerned about. Put simply, President Trump is playing with fire by nominating a potential Fed chair that is viewed as a too influenced by the administration. In the mid-1970s, bowing to political pressure from an aggressive president, then Fed Chair Arthur Burns cut rates to placate the administration and reopened the door to inflation. Today, inflation remains well above the Fed’s 2% target, and with tariffs likely to stay in place in one form or another, the reality is that ingredients are in place for a sustained move higher in Treasury yields if the Fed is viewed as not independent and interest rates are cut prematurely.

· AI ‘bubble’ burst: AI has been pushing markets higher for nearly 3 years, but the bar for further gains in AI is now very high as investors are starting to demand proof of positive ROI on the dramatic AI infrastructure spending occurring (that’s acted as a private market stimulus program). AI infrastructure spending is the marginal engine of growth of the U.S. economy and if that scales back, then we’d be looking at AI-bubble deflation combined with slower economic growth (or contracting growth), and that’s a recipe for trouble.

On the other hand, there are some significant positives to counter a weakening consumer and labour market for now. The One Big Beautiful Bill Act in the US (OBBBA) is front-end loaded stimulus for 2026. Oil prices are low. The big tailwind for the U.S. economy is company capital expenditures which are being driven by AI-related data centre spending. We are likely to remain in a “run-hot” economy. A run-hot economy occurs when too much stimulus is poured into the system (either all at once or consistently over a more extended period) and the net result is good economic growth but also higher prices and low affordability. Markets can continue to climb in this environment.

There are a myriad of positives to consider and weigh against the potential risks – see the sections below for further colour on both!

Given that valuations are elevated in some markets, many respected institutions are reinforcing a central message that investors should temper return expectations moving forward, even from a year ago. Way back in 2025, gold was ‘cheap’ at $2,600/oz, European stocks were ‘cheap at 13x forward earnings (8 full points cheaper than the S&P 500), the TSX and Asia were at 15x and Emerging Markets at 12x. Earnings growth was returning, with Europe and Canada going from no growth in 2024 to 9% and 13%, respectively. Today, gold is rocketing thru $5,000/oz, Europe is now at 15x, with the TSX and Asia at 17x, and Emerging Markets at 14x. So, all markets are trading 2 points higher in valuation with a similar earnings growth forecast for 2026 and the S&P500 is still at a high level of ~21x.

Therefore, we have to prepare and position accordingly, and be thoughtful about portfolio allocation and construction, lean into diversification, and be more intentional about sources of return. In this environment, active management/implementation, and risk management are paramount over passive investing and broad market direction. And we have to behave accordingly – most people aim to be long-term investors, and say that they will ride out the ups and downs, but when push comes to shove, they are really tourists. We will find out who all the tourists are in a correction and bear market. We position to minimize the downdrafts to put out minds at ease during those episodes. So far so good…

Other Interesting Things To Highlight

As we continue to grow and keep best-in-class service for our clients, we are proud to welcome Benedikt Walkenhorst to the Chapman Wealth Management team!

Benedikt is earning his Bachelor of Honours in Economics at Queens University. During his studies, Benedikt developed a strong interest in financial and economic analysis and is currently working on his thesis. Benedikt is driven by ongoing growth and skill development and takes pride in delivering a high standard of client service. Originally from Germany, Benedikt moved to Canada for his high school education and has since made Canada his home.

Economic Insights for 2026 with RBC’s Chief Economist, Frances Donald: On February 12 at 6 - 7p.m. ET, Executive Vice President and Head of RBC Private Banking Canada Kim Mason will be joined by Frances Donald, Senior Vice President & Chief Economist, RBC, for our latest virtual client event. In discussion with Kim, Frances will provide an overview of the current economic landscape, share insights from RBC Economics on what is ahead for 2026 and address clients’ questions on what is top of mind for the new year. Register HERE

The Risks To The Outlook

I have listed a bunch, as per usual, as we want to hope for the best, but we prepare for the worst.

This bull market which started in 2009 could be getting long in the tooth, which brings me to the long wave and when (and if and how) it will eventually end. Looking at the 1949-1968 and 1982-2000 secular bull markets, this one appears to be in its final innings.

What could set off a correction? The list is long, and there are always ‘black swans’ that we may get surprised by (as is often the case for market corrections). One currently brewing stems from issues in Japan. This has caused a stronger JPY (currency) and could be dangerous here. If the yen snaps higher too quickly, we could see the following:

1. Carry trades unwind

2. Foreign investors dump risk

3. Domestic capital repatriates

4. Global fixed income markets feel the shock (JPY is a major funding currency)

This is the classic sequence we’ve seen ahead of previous global risk-off episodes: JGB stress → Yen strength → Global deleveraging → Risk-off (i.e. correction).

As I discussed in the opening section, the AI trade could come off at some point. Interestingly, we are seeing AI experts getting much less bullish on AI than the others:

Not only does the general AI investment thesis depend on a friendly regulatory regime, but also a path to monetization that is not currently visible, and a magical ending where everyone wins together. It is also not clear the actual demand for elements of the technology. So the real question is “can the air can be let out of the AI capital-spending bubble over time without it bursting and causing a recession?”

The Positive Outlook From Here (& Selected Market Opportunities)

I’m on a similar page as the consensus, which scares me a little – I think that, ultimately, the set up and outlook from here is generally positive overall for the medium and longer term, but won’t be without its bouts of volatility, pullback and noise along the way (which is inevitable mathematically).

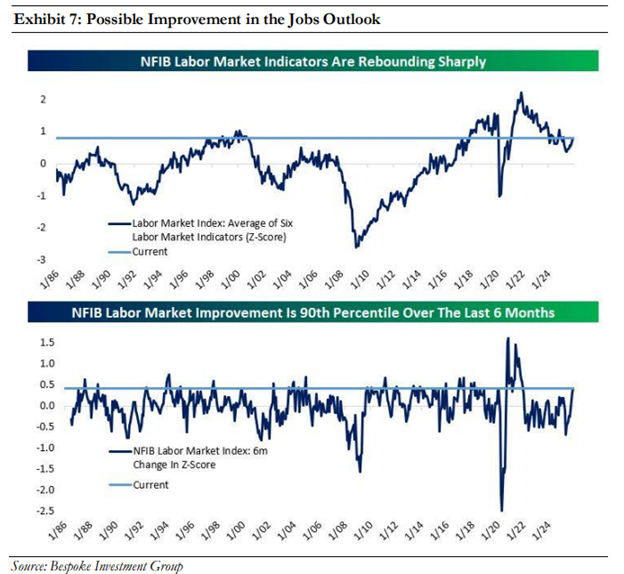

The economy continues to perform relatively well, with a question mark around the employment outlook. But there have also been signs of stabilization and improvement in the employment market. The NFIB small business survey reported a tightening in the jobs market, which could point to job growth stabilization and even acceleration in the coming weeks.

Combined with a neutral to slightly easy bias to monetary policy, this combination points to a decent backdrop for markets here.

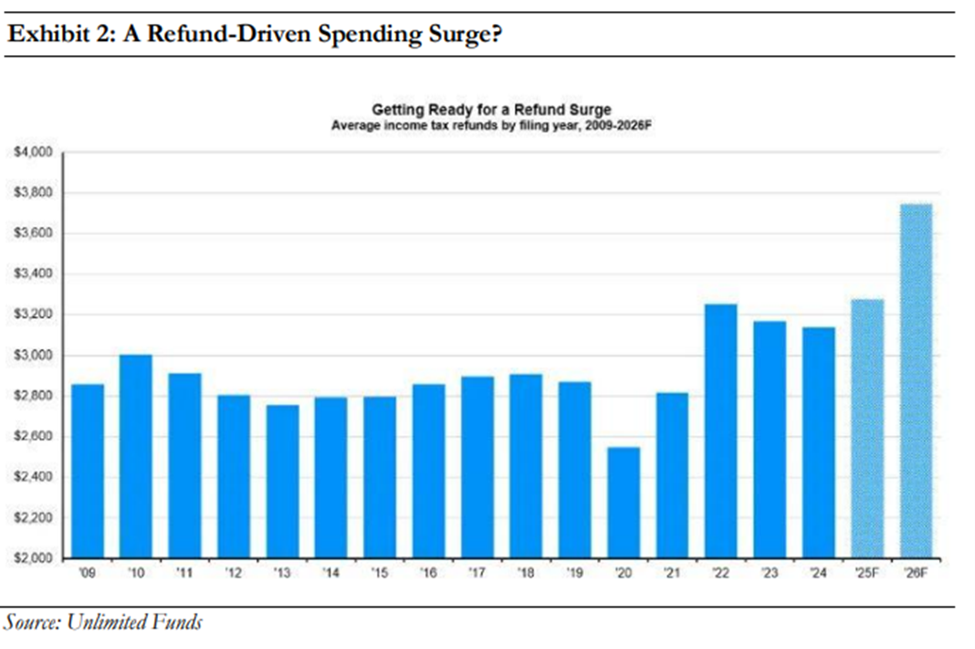

The consumer may also surprise to the upside in short order with the tax refund-driven spending surge from the stimulus effects of OBBB act:

It is consensus that inflation is ‘sticky’ and is coming down slowly, if at all. But, what if we actually get an acceleration of that slowdown? One respected strategies (Lacy Hunt)wrote a recent review that says inflation concerns are unwarranted, citing eight disinflationary forces he thinks will persist in 2026, and makes some good points. He notes that across the entire economy, labour makes up about 70% of total production costs. These costs are either flat or falling, which is disinflationary (and should produce lower long term bond yields).

· Labor market slack is growing with broad unemployment measures jumping as more workers are forced to take part-time jobs.

· Real disposable income is not growing despite the supposedly robust economy.

· Bank loan growth has slowed to almost zero.

· The federal budget deficit shrank $0.3 trillion in calendar 2025, leaving fiscal policy unexpectedly tighter.

· Other than AI, more US manufacturing plants are sitting idle or below capacity.

· Higher tariff rates are suppressing demand in many goods categories.

· Rapid expansion in the AI sector is setting up lower growth in the future.

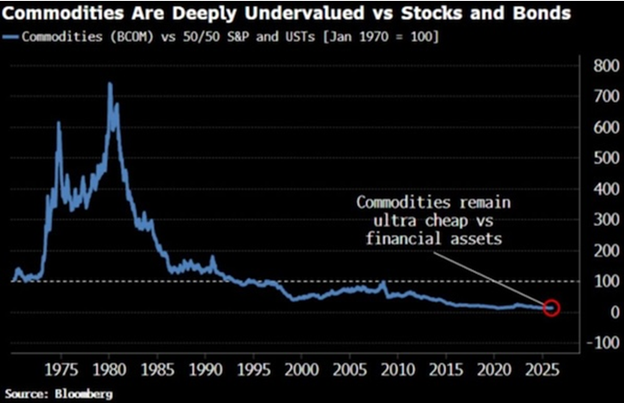

If the AI trade loses some air, and economies still chug along, it’s an even better environment for commodities to forge a generational outperformance over financial assets. Hard assets climb in real terms, while stocks and bonds, denominated in increasingly weakening currencies fall further behind. This is a view we have expressed to date in our portfolios, and remain so:

Canada is heavily exposed to commodities, and note that the Canadian index still trades at a 5-turn discount to the US on 2026 earnings (17x vs. 22x) despite having superior expected earnings growth this year. Food for thought.

Finally, there are other factors that may support markets from here.

· Easier monetary policy: The Federal Reserve has cut rates by -175bp since September 2024. After CPI inflation softened in October and November, and November’s jobs report came in weak, the Fed may cut further in coming months. On top of this, in December the Fed pivoted away from balance sheet contraction towards expansion to address a shortage of liquidity.

· Banking deregulation: Treasury Secretary Scott Bessent is overhauling the US bank regulation apparatus to focus on promoting growth. On December 11, he said economic growth and national security, including economic security, “are both essential to financial stability.” Alongside monetary easing, bank deregulation—including easier capital standards—is likely to give a boost to growth and inflation.

· Positive fundamentals for business investment: According to national accounts data released on December 23, US corporate profits grew strongly in the third quarter of 2025. With the return on capital high and the cost of capital relatively low, this is conducive to business investment, whether financed with earnings or debt.

· Corporate balance sheets are robust: With debt-to-equity ratios low and rising, all this is likely to be positive for business investment, credit growth, and nominal GDP.

The Downside To A ‘Run Hot’ Economy

Back in the fall, the central banks further cuts to interest rates pointed to a run-hot economy. Since then, that’s largely where the economy has headed, given solid growth and stubbornly firm inflation readings. And the fact that we are in a run-hot economy is by design (either purposeful or unanticipated).

Since taking power a year ago, almost all of the administration’s economic and trade policies have increased the chances we get a run-hot economy. This includes the extended and increased tax cuts from the One Big, Beautiful Bill Act (OBBBA) (which stimulates the economy) and increased Federal spending (which stimulates the economy). As well:

· Deregulation across industries stimulates the economy.

· Enticing foreign investment into the country (think of the litany of foreign countries and companies that have pledged massive investments in the U.S. since last year) stimulates the economy.

· Fannie Mae and Freddie Mac buying $200 million of mortgages, to push mortgage rates lower, stimulates the economy.

· Pressuring the Fed to lower rates (and the Fed lowering rates 75 bps last year) stimulates the economy.

· Instituting tariffs on virtually all trade partners boosts prices (how much can be debated, but there’s no doubt it does boost prices).

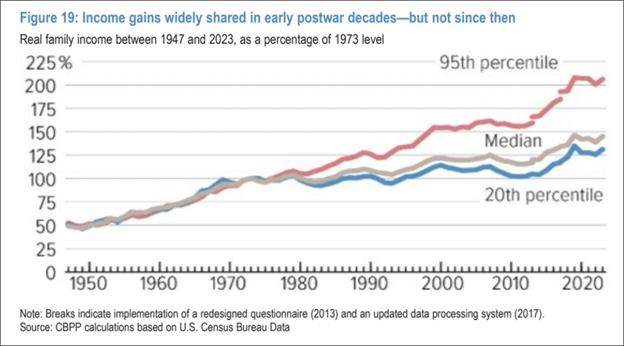

The net result of all of these policies is an economy that has very solid growth (which is a good thing) but also one that has stubbornly high prices, and thus affordability problems, because while the unemployment rate is low and people have rising incomes/asset prices, the cost of everything is so high that the lower-income/no-asset cohort gets squeezed, while the middle class doesn’t feel any benefit from rising asset prices or higher wages.

Inequality is rising, partially due to this dynamic:

If that sounds familiar, it should, because that’s where we are. Broadly speaking, the unfortunate reality is that focusing economic and trade policies exclusively on stimulus and better growth does have negative consequences in the form of stubborn inflation and affordability.

Rate can eventually rise from all of this, and the negative consequence of those rising rates is that they initially exacerbate the affordability problems in the economy (happening now) and, over the medium and longer term, can actually cause economic growth to slow, creating stagflation (because prices don’t fall immediately).