Paul Chapman

Senior Portfolio Manager & Wealth Advisor

March 30, 2026

“Most investors are concerned not with what an investment is really worth to a man who buys it ‘for keeps’ but with what the market will value it at, under the influence of mass psychology, three months or a year hence.” – John Maynard Keynes, 1936

Note that the contents of this memo are all my thoughts, and not the views of RBC Dominion Securities. As well, no part of this content was AI-assisted or created.

[YOU CAN LISTEN TO THE ABBREIVATED PODCAST VERSION OF THIS NOTE HERE]

Friends & Partners,

It has been a wild first quarter (particularly March!) of 2026, and that is part of what I signed up for in my line of work. Volatility and uncertainty is embedded in the nature of investing, but also the reality of the world. Unpredictability is a feature and the norm – it’s always there, just in different forms and levels. Discipline in managing multiple market dynamics and narratives is essential because it reinforces process, principles and philosophy, and helps avoid bad (i.e. emotional!) behaviour.

I have no intention (or ability) to prognosticate geopolitics, but I can distil down and frame the risks and opportunities, negatives and positives as I always aim to do here in my Partner Memo. At the end of the day, this too shall pass, but not before more volatility gets the best of those who let it… Luckily not our clients and portfolios.

Remember, equity markets are down close to 10% from their January peak. Is that a lot? This is right in line with the median annual corrections off an all-time high since the March 2009 low. We see a decline of this amount or more during most calendar years. This is the price of admission....

As we exit Q1, investors have had no shortage of developments to digest. Recent market volatility has been shaped by a number of factors, including a pullback in technology shares amid evolving AI expectations, emerging concerns in private credit, the Supreme Court’s decision to limit the use of tariffs, and most recently, the escalation of conflict in Iran. The conflict has contributed to a sharp move higher in oil prices, with crude rising above US$100 per barrel over a relatively short period.

The Strait of Hormuz closure is proving to be more than a short-lived geopolitical event, as it is evolving into a meaningful and likely lasting shift in physical markets that is squeezing regional supplies and materially lifting the price of oil and refined products. And the longer oil stays elevated, the more it will feed through to 1) corporate margins, 2) consumer spending, and 3) ultimately growth.

This is also affecting the market’s expectations of how Central Banks will change interest rates. A few weeks ago, markets expected rate cuts moving through 2026 – the possibility of a rate hike in 2026 appeared for the first time in recent memory. A market that understands the rate path forward is typically stable and bullish for risk assets, even if rates stay higher. But a market suddenly uncertain whether the next move is a cut or a hike is a very different and far more volatile environment, and we are seeing that feed into the recent volatility.

War in Iran has injected new uncertainty into the global economy, reviving concerns that high oil prices could drive inflation up, strain consumer spending and weigh on economic growth.

At this point, markets have assumed that:

· The oil shock won’t cause a recession, but we will experience at least a short-term affordability shock that restrains consumption and growth.

· Higher energy prices are the first-order effect. We see this first in gasoline prices.

· The second-order effect will be higher costs for intermediate goods, including transportation. This will raise the cost of travel and business. Inflation could be going higher…

· The third-order effect will be on food prices due to transport costs and fertilizer prices.

· The pre-war February CPI inflation report was already showing a spike in food prices, which now seems like it could accelerate.

There were already some signs of cracks in consumer spending and decidedly mixed labour market data prior to the conflict. So the million dollar question is – ‘how long will this last’? Markets are struggling with this one.

The Fed has noted that inflation expectations remain well-anchored, and to be fair, they are not wrong, but some market-based inflation expectation readings are beginning to quietly rise. But inflation expectations in the market (notable the 5-Year Breakeven Inflation Rate) are ticking higher. This is a challenge for central bank’s ‘dual mandate’ to support the economy with lower rates and hold down inflation via higher rates.

In comparing the current inflation situation with the energy shock of 2022, it is important to note the energy shock from the Russia-Ukraine conflict was that war collided with a post-pandemic economy shaped by pent-up demand, government stimulus, and tight labour markets, amplifying inflation. Today, fiscal policy is tighter, labour markets are looser, and policy rates are already neutral to restrictive, reducing the risk of sustained inflation, which is a positive.

But if the economy slows from this, and inflation ramps up, we have a problem.

In the Fed’s ideal scenario, they keep rates on hold just above neutral and continue to drag core inflation back toward their 2% target. In the more likely event that inflation pressures build, economic data show signs of weakness, or worst of all, both simultaneously, the Fed would logically err on the side of caution and hike rates at the expense of the economy, all but certainly tipping growth negative and initiating a recession. The reasoning is straightforward: the Fed has plenty of room to cut once a slowdown tamps down inflation, but repeating the Arthur Burns 1970’s era mistake of easing prematurely before inflation was fully contained would be a historically embarrassing and economically detrimental policy error. The Fed is well aware of that.

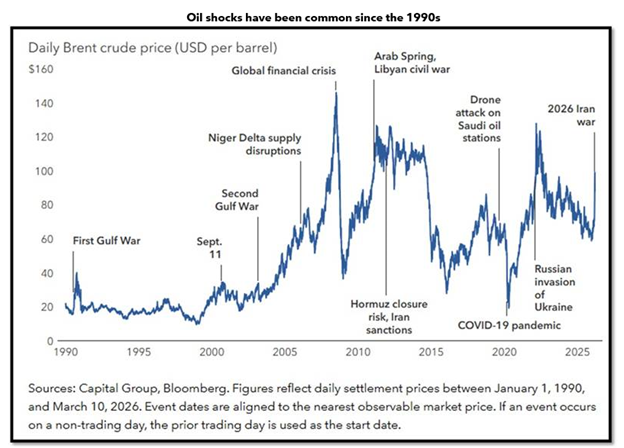

It is important to remember that we have seen forms of this movie before:

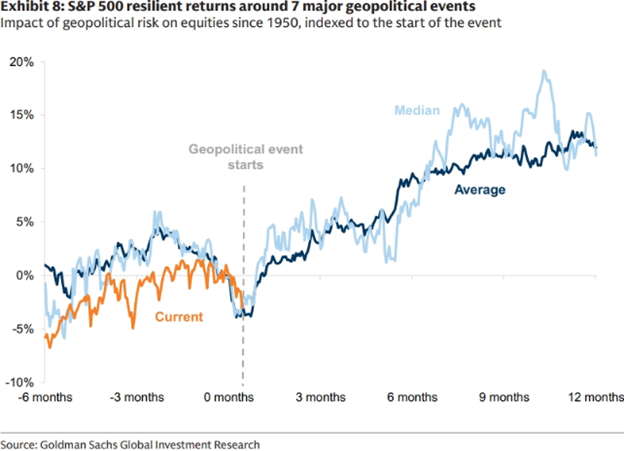

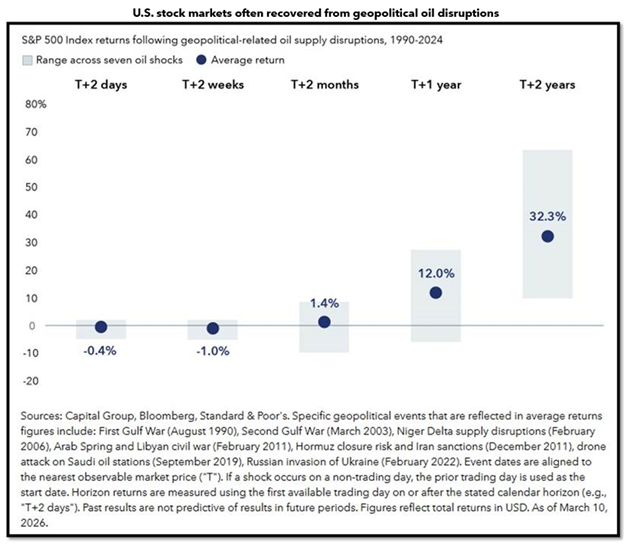

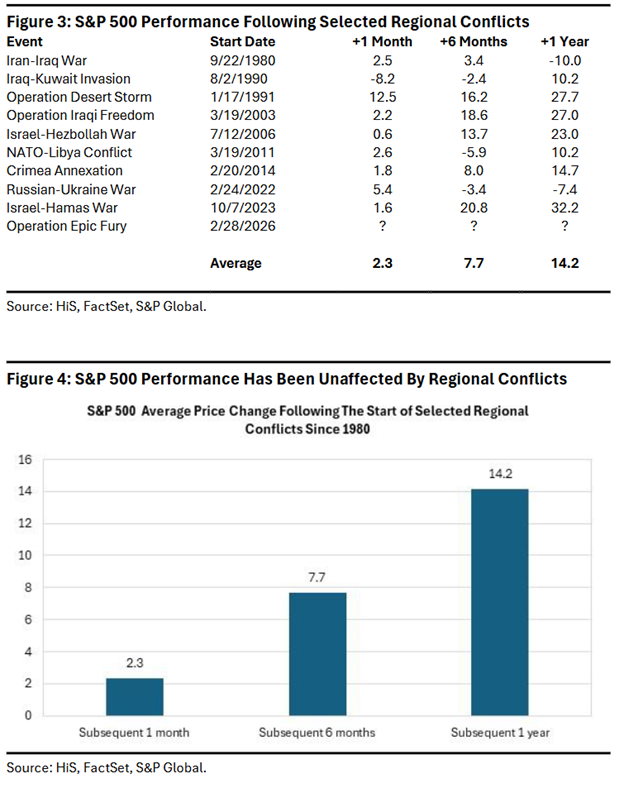

And despite the high valuations across markets and the worse growth/inflation mix, it is important to acknowledge that geopolitical and energy shocks have historically led to relatively short corrections, with the S&P 500 often particularly resilient:

So, in many cases, equities have moved past such events and, at times, performed better as uncertainty begins to fade. That said, the key exception tends to be when the economy is already weakening or approaching a recession, where geopolitical shocks can amplify downside risks. The good news is that the global economy remains broadly constructive – the latest global PMIs for February point to the strongest growth in nearly two years, and Bloomberg consensus continues to project a median 3.1% real global growth rate for 2026 – even after a number of estimates were updated in mid-March following the onset of the current conflict.

There is a scenario where geopolitical tensions subside fairly rapidly, oil prices correct from current levels, and the labour market stays resilient in the coming quarters. The upcoming midterm elections and downside risks to the economy could limit President Trump’s tolerance for a prolonged war.

Now, let’s look at what we have that is market positive and provides an offset to the negative views: If we can get a start to the end of the conflict, we have ~$160bn of US tax refunds hitting accounts this quarter. That is up 14% from last year, and fuelling consumer spending. As well, the Fed’s balance sheet is expanding for the first time in 3.5 years, which has historically been good for risk assets. On top of that, the US is aiding in lowering mortgage rates and support housing (attempting to). Finally, financial deregulation with lower bank reserve requirements should provide more access to credit and liquidity.

The problem, though, is that most of the benefits from these things are temporary in nature rather than lasting. So, the question is all about timing and longevity. Oil persistently over $100 takes about 0.3% off of global GDP and adds as much to inflation. If those offsets cease and that paradigm continues, then markets will need to contend with that reality as there could be longer-term economic damage. But there is also no single global outcome since some economies, such as the United States and parts of Latin America, are relatively insulated due to domestic energy production. Others — including Europe, Japan and much of Asia — are more exposed to sustained price increases and supply chain interruptions.

So, the war has presented a rather manageable shock, for now, but it requires a resolution at some point soonish to avoid a broader negative outcome. It is obviously tough to handicap this: not only is it a war and thus inherently unpredictable, but the war aims of the US and Israel are not in synch and have changed over the course of the conflict. Expect persistent volatility in the meantime.

Moments like this help to explain why our portfolios are structured the way they are, with a “hope for the best and plan for the worst” investment process that prioritizes risk management, broad diversification and an institutional construct. When bad things happen in the world and markets, we want to ensure that we are always well invested and emerge from the storm to be stronger. Asset Allocation should reflect what we do not know, not what we do know…

Other Interesting Things To Highlight

Given the state of the world, join us for an exclusive virtual event Tues Apr 7 at 2pm ET featuring retired military leader and former director of the CIA, General David H. Petraeus as he shares insights on the rapidly evolving situation in the Middle East and its implications for global markets. Drawing on his firsthand experience leading coalition forces, General Petraeus will offer a timely and informed perspective on recent developments in the conflicts and what they may signal in the weeks ahead.

This event is hosted by John Stackhouse, Senior Vice-President in the Office of the CEO, Royal Bank of Canada, the discussion will explore

·The strategic dynamics shaping the region, including the roles of the United States and Iran

·Implications for energy markets and global economic stability

·The broader geopolitical landscape and what it means for investors

Register for this virtual event HERE

I am proud to be supporting My Friend’s House again this year, and they have a few wonderful events coming up soon. The good news is, the next one (East Coast Kitchen Party on May 20th) quickly sold out! My Friend’s House is a non-profit agency offering support for abused women and children living in the Georgian Triangle. Since opening in 1991, My Friend’s House has helped thousands of women get the safety and support they need to rebuild their lives, and serves 600 women and their children each year. This is an important one to support.

Can This Market Remain Resilient?

Are markets entering an early stage of something more structural? That is the question. What started as a routine Q1 pullback could be the beginning of something more cyclical given 1) the breakdown through key moving averages, 2) the collapse in breadth, 3) the "quasi-shock" in Fed expectations, 4) the quiet repricing of credit spreads.

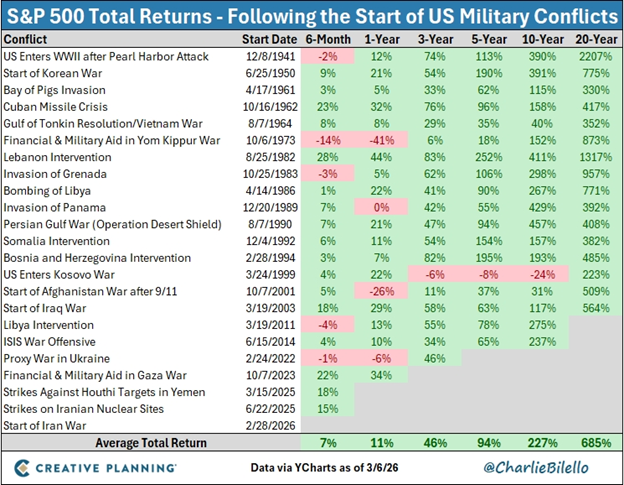

When it comes to wars and stock market returns, there is no typical outcome. Every single time is different. That should make sense because there are so many variables that influence the stock market and so many unknowns when it comes to wars. Just a few of the many questions today: How long will the war last? Will it expand into a regional war? How long will the Strait of Hormuz be closed and what impact will that have on the price of oil/gas? Will the U.S. send ground forces? Will Russia or China intervene? What is the endgame? What are the economic consequences? None of the answers to these questions are known today.

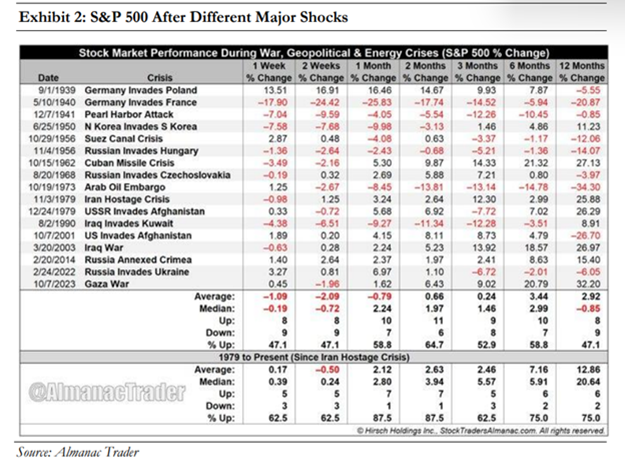

Most charts show that one should ‘buy the dip’ following an invasion:

But a table from Jeffrey Hirsch at Almanac Trader tells a slightly different story. Hirsch excluded some of the more minor shocks in his event study such as the Asian Financial Crisis and Brexit. Average and median returns are directionally similar inasmuch as stock prices tend to react to the initial shock and then rise afterwards, but the magnitude of the returns is dissimilar to the more optimist view. In addition, post-shock returns improve significantly if investors focus on the post Iran Hostage Crisis period. The worst of the initial short-term price shocks were attributed to World War II and the early days of the Cold War:

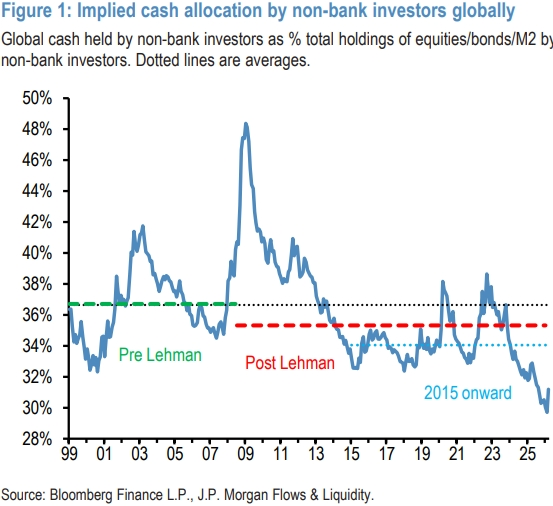

There has been a pick up in cash on the sidelines, which means that there is dry powder potentially to buy stocks and bonds. But this chart shows that, while there has been an increase in cash allocations over the past month, this increase has been rather modest thus far compared to 2022 and started from a significantly lower level. Still-low cash allocations by historical standards present a headwind to both equities and bonds going forward for as long as geopolitical and macro uncertainty remain elevated.

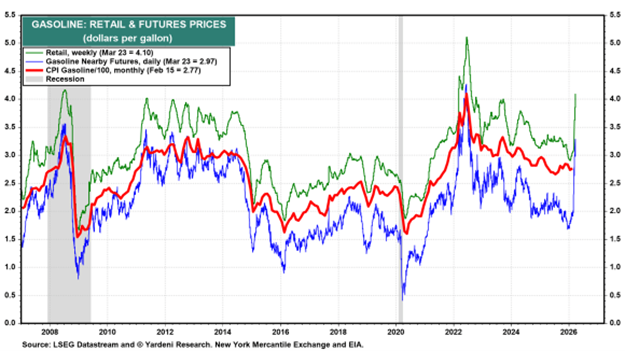

The odds of a US recession remains around 35%, according to Polymarkets.com, despite the huge jump in gasoline prices, which might depress consumer spending:

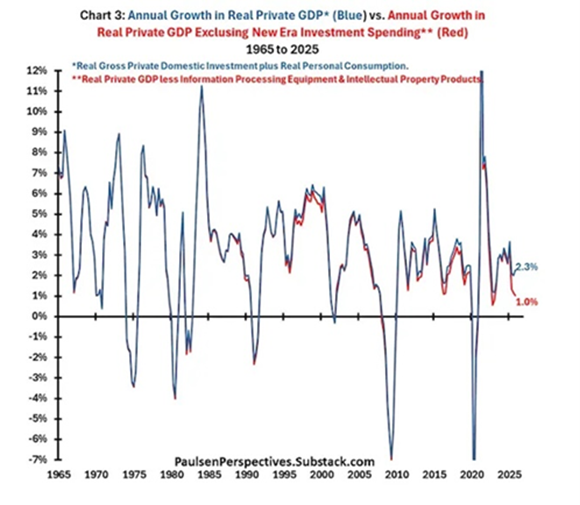

But, the economy outside AI is apparently struggling a bit, borderline recession.

There Is Always a Positive View

We currently have a relatively constructive economic backdrop. Consumer balance sheets remain healthy, corporate earnings growth has been solid, and unemployment is still near historic lows despite the most recent jobs report. The economy broadly speaking is in decent shape.

Here are more charts on why the Iran conflict shouldn’t affect markets longer term:

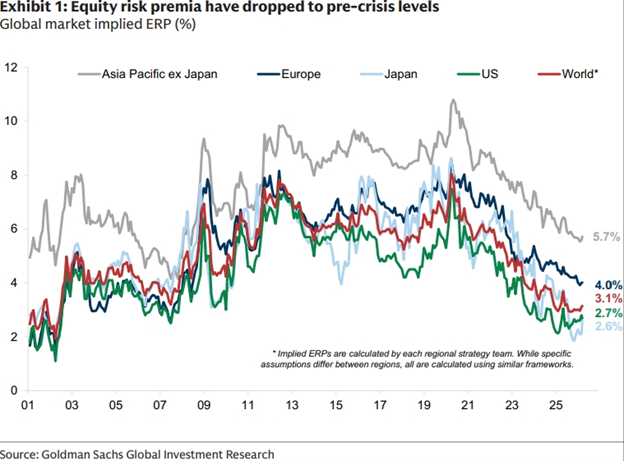

Risk premiums have risen modestly but remain rich, suggesting equity markets continue to expect a reasonably quick resolution to U.S.-Iran conflict. Is this resilience or complacency? Time will tell:

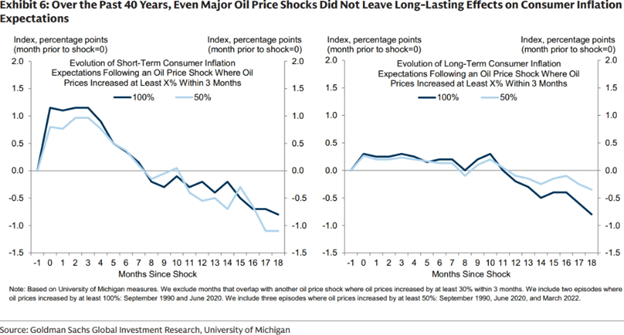

While some measures of U.S. inflation expectations can be sensitive to energy prices, over the past 40 years even major oil price shocks where prices rose by 50% or 100% did not have long-lasting effects on inflation expectations: “And with the labour market now notably softer than in 2021 and 2022, the potential for a meaningful boost from second-round effects should be more limited.”

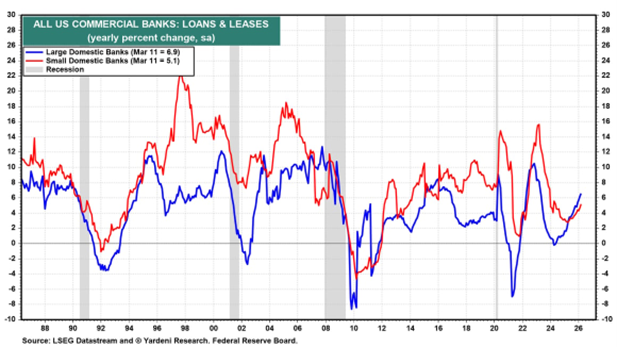

Most past recessions were caused by economy-wide credit crunches. That is not happening at this time because the banks are lending:

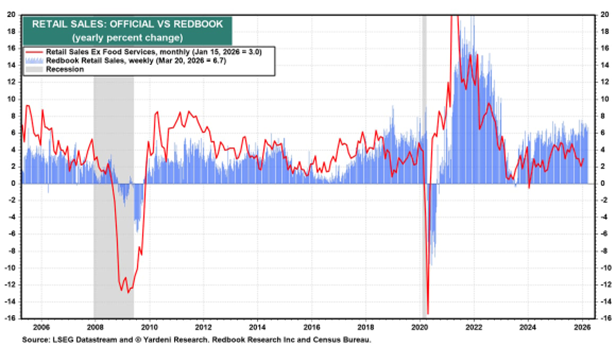

The Redbook Retail Sales weekly index rose solidly by 6.7% y/y during the week of March 20th. So far, consumers are still spending:

Private Credit – Is This A Systemic Risk?

We hosted a virtual private credit event in early March given the noise out there in the sector. We hosted two senior thought leaders in the space – one from Oaktree and the other from Accelerate. With over 100 attendees, the feedback was uniformly excellent.

Bottom line is this may be the most amateur reporting on a subject that I have seen in my career. But, we are not about to hear the end of private credit drama, and we have not heard of the last default, or impairment, or story that is made to exacerbate clicks and noise. Like any strategy, some private credit managers are going to be much better than others. But fear has set in, and redemption are likely to persist for some time yet, regardless of asset or manager quality. The select few managers will capitalize on this dynamic…

Here are the dynamics (facts):

· AI disruptions that impact selected software companies would be impacting the equity of those companies far more than the debt (which, by definition of capital structure, is senior to equity). Isolating this broad narrative to “private credit” is silly. And then applying it not just to private credit but also to private equity and public equity requires some parsing of each company, each collateral particularity, the cash flow dynamics, each strategy, etc.

· In the only real case of meaningful loan sales we have seen so far (Blue Owl’s sale of loans in non-traded BDC, OBDC II), the loans were sold at 99.7% of par value, with sophisticated institutional co-investors doing their independent due diligence and serving as unrelated buyers to effect these transactions.

· If (when) it turns out that there were undisciplined managers during the credit boom who engaged in poor underwriting and took on excessive leverage, the investors in those managers would face losses. They took on a high-reward investment, and that comes with risk. And that is not “contagious.” It is not in the deposit base of banks, nor is it connected to the capacity of our financial system to extend credit. It is not in the context of a universally held asset (i.e., residential housing). It is a potential loss to investors, not a systemic one. There are no counterparties who then risk repayment loss that then bleeds into the global financial system.

· Any potential wash-out of bad or reckless asset managers fortifies the system remember, reallocating capital more efficiently and productively.

· Redemptions are high given the fear instilled across this asset class, expect more before it subsides. The redemption limits (gates) are a function given the underlying asset, not a bug.

We haven’t seen any fundamental deterioration across core private credit markets. There are pockets of stress, but default rates remain low and sit below their 5-, 10 and 20 year averages. The data does not support the notion of a systemic problem and equity coverage is at very healthy levels, in fact among the strongest we have seen in some time. It’s also important to keep the headlines in context. Even with its rapid growth, private credit still represents a relatively small share of the global credit universe, roughly a mid-single digit percentage of outstanding corporate debt which limits its systemic impact. Finally, while early private credit vintages (15–20 years ago) leaned toward distressed and mezzanine financing, today’s market is far more diversified, institutionalized, and quality focused. It now spans senior direct lending, asset backed finance, and real asset credit, generally with stronger documentation than what we see in public markets.

What Do We Make of the "SaaS-Pocalypse" Headlines?

AI’s impact on software is still unfolding. The core fundamentals that make software attractive remain intact at least for some of the companies in that space: high margins, scalability, recurring cash flows, strong network effects, and exceptionally sticky customers. Mission critical software embedded in workflows is difficult, often impossible to replace, and these companies are far more likely to integrate AI to strengthen their offerings than to be displaced by it. It is most likely a deal by deal dynamic rather than a sector wide threat, which is why manager and deal selection matter more than ever (as it has always been).

For those that want to dig in deeper and keep abreast of things, Blackstone is a major and quality player in the space and is hosting an event that clients can join:

Title: Private Credit End Client Event: What the Headlines Miss

We are pleased to invite you and your clients to a conversation on private credit on Tuesday, April 7th at 4:30PM ET with Jon Gray, President & COO of Blackstone, and Michael Zawadzki, Global CIO for Blackstone Credit & Insurance.

In this timely discussion, Jon and Michael will cut through the noise around private credit, sharing why we believe the asset class is more resilient than recent headlines suggest. They will address key investor questions, discuss how we are navigating today’s market environment, and explain why we continue to view private credit as a long-term core portfolio allocation.

Register HERE