Paul Chapman

Portfolio Manager & Wealth Advisor

February 24, 2026

“Nothing sedates reality like large doses of effortless money.” – Warren Buffett, who went on to say…

“I would rather sustain the penalties resulting from over-conservatism than face the consequences of error, perhaps with permanent capital loss, resulting from the adoption of a 'New Era' philosophy where trees really do grow to the sky."

Note that the contents of this memo are all my thoughts, and not the views of RBC Dominion Securities. As well, no part of this content was AI-assisted or created.

[YOU CAN LISTEN TO THE ABBREIVATED PODCAST VERSION OF THIS NOTE HERE]

Friends & Partners,

Things just keep getting more interesting by the day, as we venture further into the unknown (i.e. AI and its potential implications on everything and everyone).

There is lots of news (and views) to consider, and a TON of churn beneath the surface of markets – dispersions are high – meaning some stocks are tanking, some are performing very well, leaving the overall index surprisingly stable. Solid active management and being in the ‘right’ exposures and strategies is more important than ever.

The market is pricing binary AI outcomes – struggling to figure out if the tech giant hyperscalers are going to be able to get any return on their massive investments ($650bn in this year alone!) versus a white-collar productivity collapse and which sectors AI will demolish. Investors are shooting first and asking questions later – trigger-happy and unable to distinguish between overwrought scenarios and genuine disruption timelines. Selling pressure within this perceived AI losers cohort has become indiscriminate, with sharp deratings largely driven by narrative rather than fundamentals. Even though earnings momentum remains resilient for the impacted names, the market is pricing that the business models and profitability of these firms should be under serious threat as AI adoption accelerates. Remember that no one really knows, and uncertainty is the market’s biggest enemy…

Put simply, software stocks, in particular SaaS (Software as a Service) stocks have become “ground zero” for concerns that AI will potentially destroy earnings power for large market sectors and that fear is the main reason stocks have been volatile over the past month.

At this point, fears that AI will disrupt entire sectors and industries is outweighing hopes of productivity driven earnings boosts for now and that fear is the main reason some of the AI and growth stocks have been falling. Luckily we are very underweight that stuff in our portfolios, and overweight ‘old economy’ stocks and shares of ‘things that hurt when they drop on your foot’.

For much of the past year, the S&P 500’s rise has been driven by what I have called the ‘four pillars of the rally’. In order of importance, these are: 1) AI enthusiasm, 2) Stable economic growth, 3) Ongoing Central Bank rate cuts, and 4) Tariff clarity. But in recent weeks, those pillars have come under varying degrees of stress, we do need to assess the status of each pillar and thus the outlook for the broader market:

Pillar 1: AI Enthusiasm – Is it still in place? Yes, with a longer-term view, but short term, it’s been a headwind. I have sounded the alarm on the bullish sentiment in the past few Partner Memos as you well know. Recently, the tone towards AI has changed for the worse and it is true that recent AI related headlines have been negative for both the broad market and specific sectors (software the most notable). So, that could lead one to think that AI Enthusiasm is “dead” but, that is not actually the case longer term. It has been reduced and it is not the bullish force of the past year (or three years), but the reality is that AI is still underwriting expectations for substantial earnings growth in 2026. The vast majority of the jump in expected S&P 500 EPS above $300/share in 2026 is due to AI and until that begins to reverse itself (which it hasn’t yet, despite elevated anxiety) and we see earnings estimates come down, then the AI Enthusiasm pillar will remain in place from a longer-term standpoint.

Pillar 2: Stable Economic Growth – Is it still in place? Yes. Economic growth has been the unsung hero of the market over the past 3 months and it’s the strongest “pillar” of this market. Due to numerous factors (including significant pro-growth policy), economic growth is stable and that’s helping to facilitate the rotation trade out of AI/tech and into more cyclical parts of the markets, as the outlook in a run-hot economy for those sectors is favourable and that’s helping to justify that ‘rotation’ trade.

Pillar 3: Ongoing Fed Rate Cuts – Is it still in place? Yes. Although not as forcefully as before. The Fed is a hot topic of debate, but if we look past the drama/politics, the reality is the market does still expect the Fed to continue to cut rates in the near future. Now, it’s true the Fed is likely closer to the end of the rate-cutting cycle (which has been going on for over a year and a half), but the Fed likely isn’t done cutting rates quite yet and while there may only be two rate cuts left, it’s still lower rates from here. So, expectations of lower rates are helping to support this market.

Pillar 4: Tariff Clarity – Is it still in place? Yes (at least from the market’s standpoint). The Supreme Court (SCOTUS) decision invalidating the IEEPA tariffs (which was widely expected) added both certainty (no more credible, flippant tariff threat) and uncertainty to the tariff situation, because the administration will utilize other statutes/powers to implement some of the IEEPA tariffs. But, if we step back, the reality is the tariff threat has largely been mitigated, not just by the SCOTUS decision, but also by repeated evidence of “TACO” (Trump Always Chickens Out) and the ongoing affordability political narrative pushing back on them. Bottom line, the market (rightly) believes that shock tariffs that could damage the economy are not likely regardless of what’s said, and that gives the market needed clarity.

So, where does this leave the market?

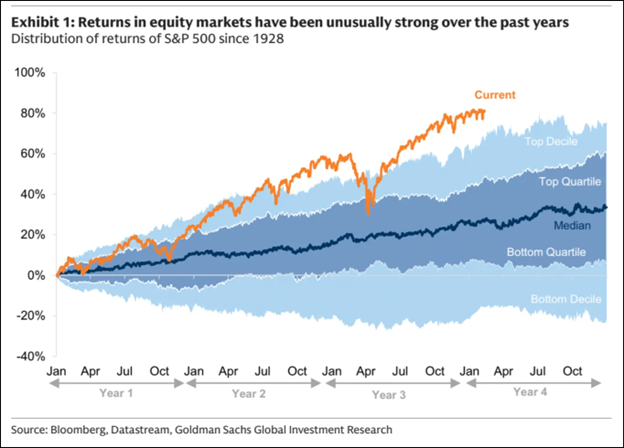

Valuations are generally expensive, sentiment is still too bullish, the market is changing leadership, geopolitical tensions abound, and the use of leverage is high. Tactical defense is a must. But there remain attractive strategies and sectors.

But, the reality is that all four of the pillars of the rally are still largely in place if we look at them from a medium/longer-term time frame. That said, the shift in AI sentiment has not been accompanied by actual, fundamental deterioration in earnings at this point, so looking at the medium/longer-term view, while the pullback likely isn’t over, the outlook for markets is still generally supportive. However, the strength of the positive/bull case has been diminished and that process is why we have had more volatility in the markets in 2026.

Here’s the overarching point we need to understand: the bull market of the past three years has been driven by two factors: 1) increased earnings expectations (as tech companies massively grew profits amidst surging AI demand) and 2) multiple expansion, as investors viewed AI as a productivity boosting machine for all industries, leading investors to pencil in better future earnings growth. Recent headlines are eroding those two beliefs. For this to stop, we need a proof element to appear that shows AI capex is generating a positive ROI and that AI will not destroy entrenched industries, but instead make them more efficient, productive and boost earnings. Until we get that, we can expect mixed sentiment and elevated volatility.

As well, the recent bout of market volatility also due to government policy confusion/chaos is also a reminder of a familiar pattern: headlines hit fast and market reactions are often exaggerated to the downside, while the true outcomes take longer to develop and often land somewhere far less extreme (usually revising upwards). Our objective is not to speculate on political outcomes, but to provide practical insight and portfolio positioning to minimize downside, volatility and capture tactical opportunities as markets recalibrate from chaos back toward fundamentals.

Other Interesting Things To Highlight

On March 3rd at 1pm ET, we are hosting a virtual event entitled "Private credit – Canary in the coal mine or opportunity?". We will be featuring two experts in the field of private credit – a senior Managing Director from Oaktree Capital Management (one of the leaders in the space), and the CEO & Chief Investment Officer of Accelerate, another expert in this space. Given the headlines out there on this sector, this is a timely one. Please RSVP to chapmanwealth@rbc.com to receive the Webinar link.

I am proud to be supporting My Friend’s House again this year. My Friend’s House is a non-profit agency offering support for abused women and children living in the Georgian Triangle. Since opening in 1991, My Friend’s House has helped thousands of women get the safety and support they need to rebuild their lives, and serves 600 women and their children each year. This is an important one to support.

Save the date for their East Coast Kitchen Party on May 20th, once again at Harbour St Fish Bar in Collingwood. Tickets go on sale March 10th.

Understanding AI’s Implications & Threats

I need to highlight a wonderful article from some at ‘ground zero’ showing how AI is really going to affect the world and people around you, it is certainly worth the quick read: Something Big Is Happening — matt shumer.

This was a piece from Citrini that was scaring many in the markets recently– THE 2028 GLOBAL INTELLIGENCE CRISIS - A Thought Exercise in Financial History, From the Future. But, you have to also read the positive take on things, a rebuttal piece - THE 2028 GLOBAL INTELLIGENCE BOOM which is just as compelling. This shows that nobody really knows. One of my colleagues on the desk pointed out that analysis here “favours technology optimism - The 200-year record is undefeated: Luddites, Malthusians, 1960s automation panic, 1990s ‘end of work’ discourse – wrong every time. Betting against technology-driven deflation improving living standards has a 0% hit rate over two centuries. That's an overwhelming prior.” You be the judge.

Interestingly, JP Morgan has a more optimistic view than some. They note that in recent weeks, the software selloff has been broad and indiscriminate between AI-resilient firms with strong fundamentals and more speculative growth names. In their view, the market is pricing in imminent, worst-case AI disruption, which is likely too pessimistic in their view. When it comes to quality companies, JPM still sees potential for existing platforms to be enhanced, enabling them to raise prices, though much uncertainty around AI's impact remains longer-term. Further, the revenue of established software companies is resilient due to the nature of enterprise software: high switching costs and long-term contracts. I think we can expect volatility in AI-related names to continue as new companies and innovations emerge and investors debate the potential winners and losers. Even though the software selloff is potetnially overdone, it serves as a reminder of the importance of maintaining defensive and diversified exposures.

Is This An Unhealthy Market? Highlighting The Risks Out There

Many are fearful for a myriad of reasons, but some of the more notable ones are that sentiment remains overly optimistic (too optimistic), the market ‘internals’ are behaving oddly, valuations are still high, the jury is still out on a potential recession, leverage abounds, and insiders are selling. To name a few.

One argument is that markets are acting a bit like they did during the tech crash in the dotcom bubble – tech names got creamed, while some sectors did quite well. We’re seeing that a bit currently. . Could we see a similar situation where the MAG7 stocks come off the boil to a more reasonable valuation level, while others continue to perform well? This has been happening, but is difficult to say if it will continue.

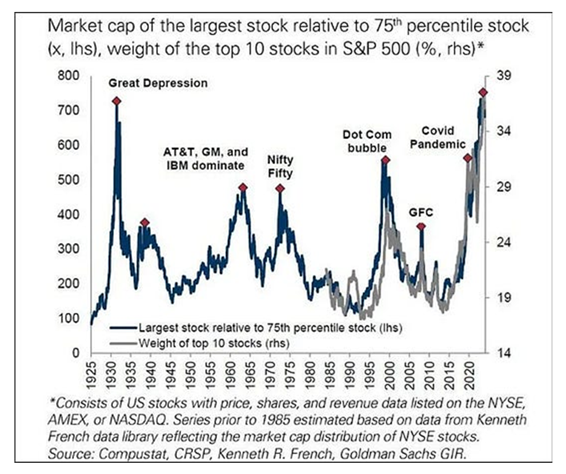

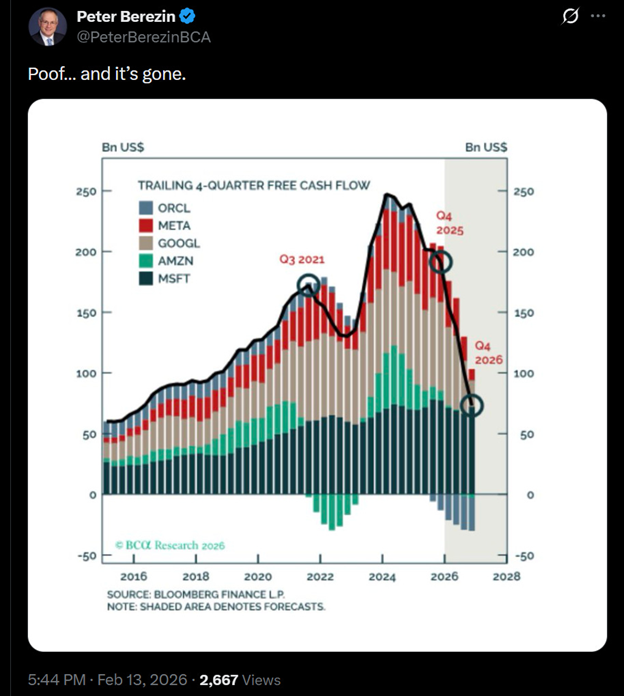

And everyone knows this isn’t healthy – the market is driven by the big tech names still:

These large tech companies are pouring billions into AI, hoovering up all of their free cash flow for now. It had better pay off!

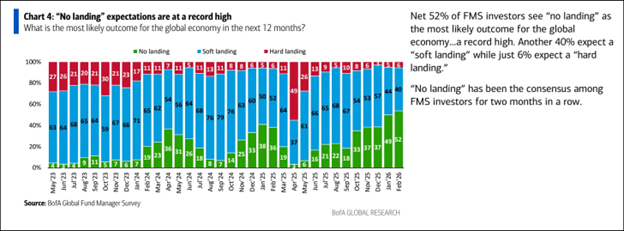

Everyone thinks the chance of recession is too low – look how many are now saying ‘no landing’:

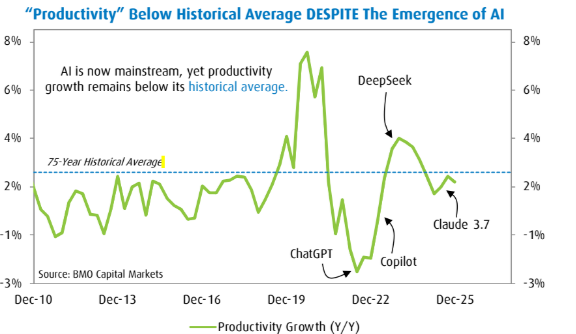

And US productivity doesn’t seem to be picking up, even with the advent of AI:

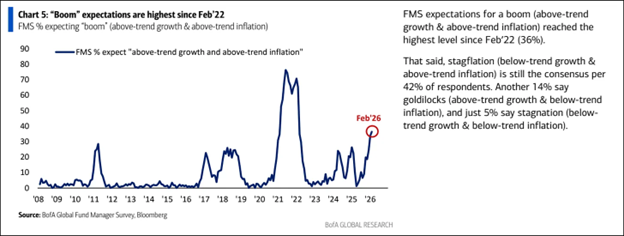

All the while, fund managers are more bullish than they have been in a long time:

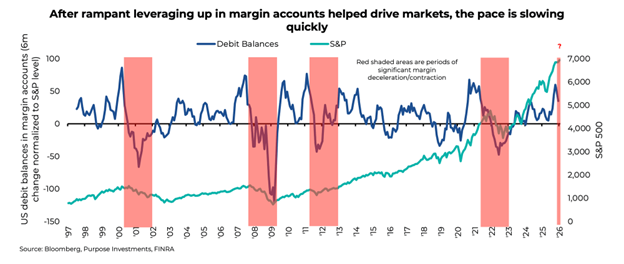

We have to keep an eye on leverage by investors. leverage. This is one thing that helped markets post strong returns in the second half of 2025. The chart below is the six-month change in debit balances, adjusted for the level of the S&P. Late last year, there was a pretty big increase in debit balances and stock ownership in margin accounts, as investors took on more leverage. The key is that when this reverses or loses upward momentum, a market reversal often follows as well. And based on the latest data point (December), the pace of margin growth has slowed.

Valuations do not bode well for future returns in general equities, so you need to pick your exposures wisely:

Another negative data point for US equities generally: Foreign investors, perhaps most sensitive to the costs born by the currency as a result of weakening Fed independence are massively overweight US equities. “A weaker dollar will reduce the weight of American assets in global indices, forcing benchmark-hugging investors to sell them. That will further weaken the greenback, feeding a vicious cycle,” notes The Economist.

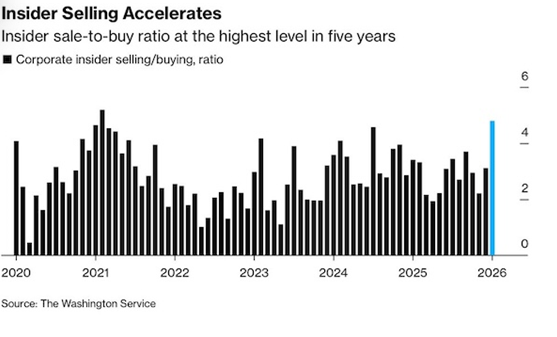

Finally, elevated insider selling is never a good sign:

Is There Still Opportunity? The Revenge Of The Old Economy!

There is always opportunity in markets.

Call this the ‘revenge of the old economy’. Since October of last year, technology (or ‘new economy’) shares are down 5-10%, while ‘old economy’ shares like energy, metals, and mining are up 30-50%.

Whether you want to call it an ‘old economy’ or ‘asset-heavy’ boom or even a ‘commodity super-cycle’ in the end it is simply a capex cycle in which physical constraints on growth create physical pricing pressures. It’s no coincidence that the last two commodity super-cycles corresponded nearly precisely to the two largest global capex cycles of the last 70 years.

I continue to believe that we are in the early stages of a physical capex super-cycle driven by electrification, deglobalization requiring new and deeper supply chains, defense spending and replacing aging infrastructure. Given the capacity constraints many commodity markets face today, which are made worse by the “weaponization” of the periodic table. The global economy will continue to grind against physical constraints and prices should continue to rise over time.

Tthis will drive certain sectors and markets – it has served our portfolios well, and should continue to.

Markets are grouping stocks and sectors by their perceived AI immunity or vulnerability. Hard asset and 'old economy' areas such as Commodities, Industrials, Materials, Healthcare and Consumer Goods are being treated as AI immune, while many Consumer or Commercial Services and Technology related industries, typically with high margins, are being viewed as vulnerable. The AI losers narrative, which began last year with segments like Media and Business Services, then broadened into Software and now into Financial Services, Logistics and commercial real estate.

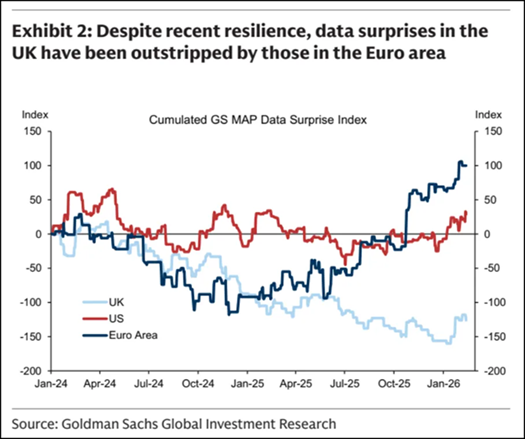

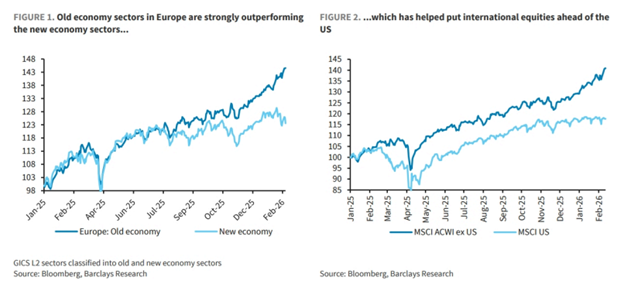

Geographically, cheaper valuations and greater exposure to old economy sectors have also helped the relative outperformance of non-US equities (where we have been overweight for some time!). International stocks were left for dead not long ago. But they’ve been crushing the US market performance:

Even though everyone has been bearish on Europe’s economy, they keep surprising on the upside: