Paul Chapman

Senior Portfolio Manager & Wealth Advisor

April 29, 2026

“I always say that my career wasn’t built on anything I thought of. It’s me working out who the smartest person is in the room, and then listening to them extremely carefully.” – Paul Sankey, founder of Sankey Research

Note that the contents of this memo are all my thoughts, and not the views of RBC Dominion Securities. As well, no part of this content was AI-assisted or created.

[YOU CAN LISTEN TO THE ABBREIVATED PODCAST VERSION OF THIS NOTE HERE]

Friends & Partners,

As we enter spring (finally), markets continue to confuse many – it is the most humbling machine known to man. March came along and brought the Iran war with it, which caught many investors offside as they worked to manage exposures through that. Then April came and brought with it a rebound to the upside that is almost unparalleled. The US market short back up 10% in 10 days off the lows, which is in the 99.7th percentile of all 10-day returns! This is why it pays to be patient, not emotional, and manage through the noise even when your gut tells you to sell into weak markets accompanied by scary headlines…

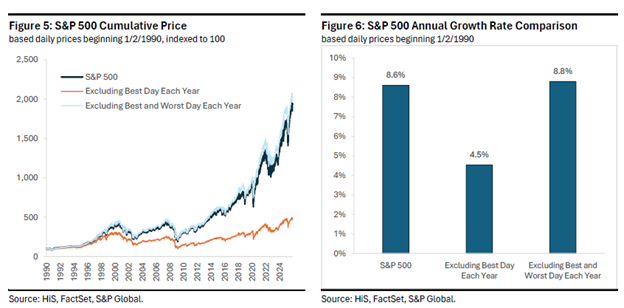

During times like these, many tend to sell (at the worst possible time when things ‘feel’ the worst) and then wait too long to reinvest once stocks begin to recover, which is a recipe for investment results disaster. We prepare, not predict, and avoid the impulse of trying to time the market. Successfully timing the market on a consistent basis is impossible. Even the slightest missteps can have a significant performance impact. Missing the worst days would be ideal, but that’s impossible - history has shown that most of these days tend to occur unexpectedly. More importantly, most of the single best performance days for the market occurred soon after some of the worst market days, and we saw it again in April. See the chart below showing that the S&P 500 has delivered an annual price return of 8.6% since 1990. Missing the single best day in each year from 1990 would drop the annualized price return to 4.5%. And even if an investor timed the market in a way to avoid both the single best and worst days, the annual price return would only be 0.2% higher than staying invested throughout the entire period. More on this in the first sub-section below (you should read it…).

Current markets are confusing many participants, with parallels being made to some ‘tops’ we’ve experienced in the past few decades. If you had told most folks that war would break out with Iran, the Strait would be closed, oil would rise above $100 and some infrastructure would be damaged, they would have expected a deeper and longer lasting correction. But many position for ‘bombs stop falling’ quickly after ‘bombs start falling’, and in recent years, investors have been conditioned not to sell into bad news (COVID, Liberation Day, etc).

Admittedly, this is not necessarily the type of environment where we would see stocks surging to new all-time highs and trading at multiples that are well above historical averages. But the fact is that markets being at all-time highs is not totally unreasonable, and there are some legitimate reasons for it.

First, remember that the worst-case scenario for markets, which was that oil would surge to $200/bbl on an extended conflict in the Middle East, has been largely eliminated. Oil at ~$85/bbl is not enough to derail the economy or to negatively impact corporate earnings. It was never about ‘elevated’ oil prices. It was about ‘spiking’ oil prices, and that simply does not look likely, despite the back and forth. Whether oil is $85/bbl or $65/bbl really isn’t that important for the market. What’s important is that it isn’t heading towards $200/bbl (which it likely isn’t, barring something extreme occurring from here).

Second, company earnings remain very strong, and this is what markets are trying to ultimately price in. The Q1 earnings season has been very solid (as of time of writing of this note a few days before month end), especially from the banks not just because of their financial results, but importantly due to their qualitative commentary. Banks know, as well as any company in the U.S. economy, how the consumer and businesses are doing, and there were virtually no words of warning from big bank CEOs. In addition, there were no major red flags about private credit becoming a systemic concern (as I’ve been noting!!). So, while it’s still a problem for some alternative asset managers, it does not look like a problem for the broader financial sector.

As an aside on private credit, I believe we will look back on the private credit pandemonium attributable to nothing systemically substantive other than media headlines that drove a herd of retail redemption. I am sure we’ll see more volatility there, but price discovery will always center back around fundamentals versus short-term sentiment.

Third, economic growth remains resilient. Fears that the U.S./Iran war would create a wave of stagflation (rising inflation combined with a slowing economy = very bad combo) across the global economy have, so far, gone unfulfilled. While it is still early, the initial data is good as inflation metrics are up, but outside of energy and commodities, they are relatively stable. Additionally, economic growth is not slowing. So, fears of stagflation appear for now to be overdone.

Finally, there are technical reasons for the market’s torrid race to new highs. Much of the torrid 10% rally in stocks over the past few weeks has been driven by funds chasing stock exposure.

This move back higher is not being driven by a fundamental evolution of the outlook necessarily. Instead, it has been driven by a series of events: 1) not being a worst case scenario, 2) reminders from data of the resiliency of corporate earnings and the economy, and 3) funds that got too under-weight too quickly, and then had to chase the market higher to add exposure as the worst-case scenarios, yet again, did not prove true.

That said, this is not a perfect environment by any means, and still-high valuations (though off the peaks) and momentum have left this market vulnerable. The key is to be positioned defensively and opportunistically for the volatility, not be held hostage to it.

As always, remember that there are a number positive underpinnings driving this robust recovery in markets that could prove sustainable: earnings growth is double digits, margins are at all-time highs, tax refunds were up 28% over last year, bank capital requirements are being reduced, GDP is positive, productivity is advancing, and both services and manufacturing are in expansion territory. The offset is volatile geopolitics, elevated inflation and whether the labour market continues to perform. Markets climb the wall of worry as they often do…

But the TSX isn't a diversified index at the best of times, and this year it has been a two-sector trade. Energy (45%) and Materials (43%) account for ~87% of the entire TSX year-to-date return. Luckily, we went well overweight those sectors in December in our client’s portfolios, even though few were positioned that way at the time.

It is important to remain disciplined and focus on the best and ‘real’ information – we get fed so much noise that can affect our judgement. Not good for investing. There is so much noise to signal – remember that economic/financial article authors aren’t paid on the quality of their analysis, or if the idea works out; they are paid based on the number of people who read it. So nobody is going to write about something ‘boring’ (boring is usually good when it comes to investing). It is all going to be high growth, exciting glam stocks. Topic selection is skewed by economics – the algos feed this as more extreme stories get read more, which triggers other algos to distribute more widely.

Markets like this illustrate why our portfolios are structured the way they are, with a “hope for the best and plan for the worst” investment process that prioritizes risk management, broad diversification and an institutional construct. When bad things happen in the world and markets, we want to ensure make sure that we are always well invested and emerge from the storm to be stronger. I will leave this story for you with this to ponder, from my friend and CIO of Outcome Asset Mgmt, Noah Solomon:

“Legendary investor Howard Marks once recalled a discussion he had in 1990 with the director of a major mid-West pension plan. During the conversation, he learned that the plan's stock portfolio had far outperformed the S&P 500 Index over the past 14 years. Even more striking than its headline performance was the path that it had followed to achieve it.

Notwithstanding that the plan’s returns in any given year had never placed below the 47th percentile or above the 27th percentile, its portfolio’s performance over the entire fourteen-year period placed it in the 4th percentile.

The proverbial moral of the story is that if you swing for the fences and attempt to be in the top 5% or 10% every year, you will fall victim to the double-edged sword, delivering long-term returns that are (at best) mediocre and that are accompanied by high volatility. In contrast, if you deliver performance which is slightly above average on a realistically consistent basis with particular emphasis on outperforming in bear markets, (1) your long-term outperformance will be substantially better than average, and (2) you will be subject to lower volatility and shallower losses in challenging markets.”

Other Interesting Things To Highlight

We are hiring! We need an exceptional addition for an exceptional team. We are blessed to have one of the fastest growing wealth management businesses in the industry, and need more hands on deck. This is an amazing opportunity for someone to join a dynamic and tight-knit team, with a keen focus on our clients, our culture, processes, and service model. This is an entry to a great career in wealth management, and getting to join one of the leading teams on this front. This position is based in Collingwood, Ontario. Please let me know if you have any exceptional candidates to refer us.

We will be hosting the one and only Brian Belski in Collingwood on May 27th at 5-6:30pm at Craigleith Ski Club. Getting Brian to Collingwood in Canada took some coordination given his busy schedule, and we’re excited to be able to host him – this will prove to be a very insightful and fun evening without question. Brian is a former colleague of mine and is one of the leading investment strategists on the planet. He is a very frequent contributor to CNBC, Bloomberg, Fox Business News, and BNN, where his market calls are closely followed by investors globally. Brian served as the Chief Investment Strategist at BMO Capital Markets for many years, where he guided portfolio strategy for some of the world’s largest institutional investors and private wealth clients. In his more than 35-year investment career, Brian has held senior strategy and research positions at BMO, Oppenheimer & Company, Merrill Lynch, and Piper Jaffray, where his consistency in messaging, coupled with process-driven conclusions, helped shape stock market and investment views for decades. Brian has most recently founded an independent investment firm Humilis Investment Strategies. Light food and drinks will be served. To RSVP please click HERE.

We hosted part 3 of our Family Office event series in Toronto recently, with this instalment entitled “Investing In an Era of Turbulence: the state of markets today and perspectives on investing through volatility and change”. It was another packed house, with many of Canada’s leading family offices in attendance to hear from an all-star cast. We hosted panels of thought leaders speaking on the state of the markets and economy, and alternative managers who have managed multiple volatile cycles. By examining their contrasting approaches—ranging from high-conviction equity long/short to sophisticated arbitrage trades—we explored how these diverse strategies navigate a challenging environment. Thank you again to our speakers Eric Lascelles, Chief Economist and Head of Investment Strategy Research at RBC Global Asset Management, Brian D’Costa, Founding Partner & Chief Strategy and Risk Officer at Algonquin, Jamie Wise, Co-Founder & Chief Executive Officer at Periscope Capital, Peter Hatziioannou, Co-Founder, President at XIB Asset Management, Adam Mitchell, Portfolio Manager at NewGen Asset Management, and Robert Fournier, Managing Director/PM of U.S. Equities at ONEX Corporation.

A new private equity fund strategy/manager to assess is the CVC Private Equity Fund. On Tuesday, May 12 at 2:00 p.m. – 3:00 p.m. ET, join the Head of Alternatives at RBC Wealth Management Mikhial Pasic for a timely discussion with Rolly van Rappard, Co-Founder and Non-Executive Chair of the Board of the private equity firm CVC Capital Partners, and Nick Clarry, Managing Partner at CVC and Head of Sports, Media and Entertainment for CVC globally. Together, they will introduce the CVC Private Equity Fund – a new investment opportunity (but longstanding manager) that provides high-quality European mid-market access, exclusively available in the Canadian market through RBC Wealth Management. During this session, insights will be shared on:

- How CVC's regional specialization allows for differentiated deal sourcing and localized operational value-add across multiple European markets, providing diversification to North American private equity investments.

- How the fund offers sector diversification through its access to sports, media and entertainment deals, and a notable underweight exposure to technology.

- How this strategy may complement a traditional investment portfolio.

- With over 40 years of experience, CVC is a global firm ranking among the top private equity managers in Europe.

You can register for this event HERE.

I wanted to highlight an interesting charity initiative started by one of our clients: Alaboo Charity is a registered Canadian charity based in Thornbury, Ontario, dedicated to supporting a growing community in Kenya. What began as a small preschool for 40 children has grown into a thriving school serving 240 students from Kindergarten through Grade 7. Their mission is to provide access to quality education and essential resources for children in underserved communities. They are currently seeking support to expand their school to include Grades 8–12, allowing students to continue their education and build brighter futures. In addition, many of the students walk long distances from surrounding villages, and the community has requested support to build a well that would provide clean drinking water to over 3,000 people. To learn more about our work and how you can get involved, please visit our website https://www.alaboo.com

Resisting That Urge To Sell… Think You Can Time The Market?

Well, you can’t. As enticing as it seems.

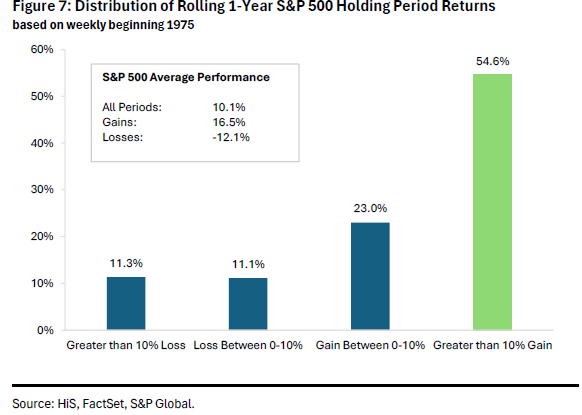

It is important know that one-year S&P 500 returns have been positive nearly 80% of the time over the past 50 years, which is a huge hit rate. Yes, Brian Belski notes that average losses within this period have been steep at -12.1%, but to avoid “big mistakes” investors need to remember that sometimes it is ok to endure some losses because those with a longer-term focus have been rewarded time and time again given the 10.1% average return for entire period. In fact, big gains have outnumbered big losses by nearly a 5 to 1 ratio, which is why it is so important for investors to maintain their discipline (e.g., avoid panic selling) during any periods of market weakness.

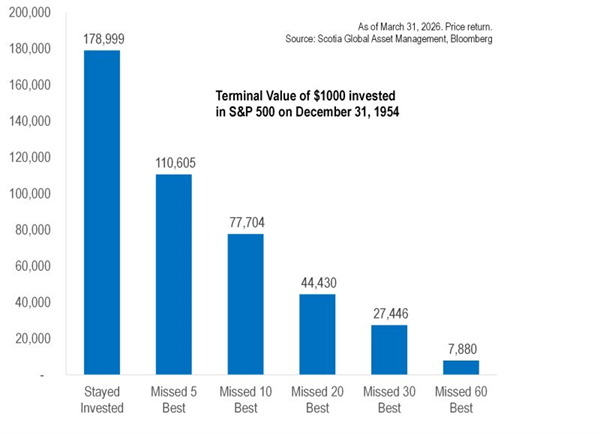

Let’s look at this from another angle – if you had invested $1000 in the S&P 500 at index inception in the 1950s, it would be worth $178,999 dollars today. Yet, missing the five best performance days since that time would cut your total gains down to $110,605 dollars. Missing the 10 best days would have resulted in a terminal value of $77,704 which is less than half of the wealth accrued by remaining invested. Remember, those days come during the worst noise.

The key takeaway is that a very few number of days is what makes all the difference to an equity investor’s terminal wealth. It is also important to understand that volatility clusters. Eight of the ten best up days over this period landed within five business days of the ten worst performance days. Said differently, those big up days usually happen just after an investor ‘panic sells’ in response to a very bad down day.

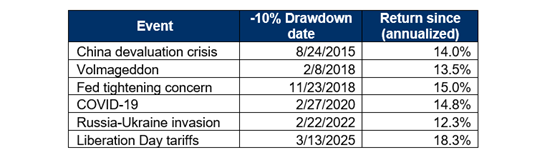

Even since 2015, the S&P 500 has weathered six distinct drawdowns of at least -10%. Each event triggered fear and uncertainty. Yet, looking back, the data tells a different story. The average annualized return following these -10% dips was 14.7%. Compare that to the S&P 500’s overall annual return of 12.9% since 2015, and the pattern becomes clear: pullbacks aren’t just bumps in the road, they’re potential entry points for improved long-term gains.

Source: Source: RBC GAM, Morningstar.

Importantly, pullbacks aren’t usually a signal that something is fundamentally broken longer term, it’s a reminder that markets don’t move in straight lines. Periods of volatility are not only common, they are an essential part of long-term performance generation.

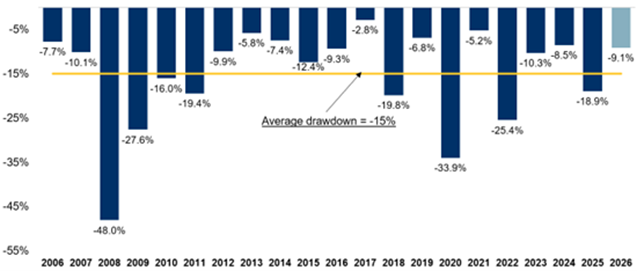

Here are the annual drawdowns in the S&P500 since 2006:

Source: Bloomberg

The data tells us that drawdowns are normal.

- Each year (with the exception of 2017) experienced a drawdown greater than -5%, even in years when returns ultimately finish positive. In fact, markets were positive in 17 of the last 20 years, returning on average 12.4% in each calendar year.

- Larger declines (-20%+) tend to occur during major economic or financial shocks, such as the 2008 Global Financial Crisis, or the Covid-19 pandemic.

Trying to time the market bottom is a function of chance, and rarely pans out...

More Warning Signs

There are lots of warning signs to consider as part of assessing things. The potential paths and outcomes from here on the geopolitical front are too many to list, other than to say we don’t know how things will evolve. If you don’t like the news, wait a few hours and things will change…

This rebound has come with limited trading volume, which may equal limited conviction. Charles Dow’s first law: volume must confirm price. This recent breakout to record highs occurred on the lowest volume of the year…

There are many making parallels to the bubble markets we’ve seen in the past few decades, such as 2000 and 2007 market crashed. overlays the 2026 S&P 500 price trajectory against identical ∼9–10% pullbacks that occurred in both H1’2000 and H2’2007. In both cases, the recovery to new all-time highs — on fading volume — proved to be the lasting market top before cyclical bear markets. The correlation is uncomfortably tight.

If you backtest all the times in history that the stock market recovered from greater than a 10% pullback in less than three months and closed at a new high with less than 3% of stocks at net new highs and less than 60% above the 50- and 200-day moving averages (similar to today!), you get March of 2000… And that was followed by the tech wreck.

There are differences today of course, but there are similarities – we’re arguably in an AI bubble as we’ve seen some companies now (like shoe companies!) pivoting to AI models which is insane.

We are watching a similar technical setup that preceded both the 2000 Tech Bubble collapse, and the 2008 Great Financial Crisis could be unfolding:

- Yield curve Bull-Steepening following a prolonged inversion — a 100% historically accurate pre-recession signal.

- Credit spreads holding well off cycle “tights” despite new stock market records — a noteworthy cross-asset non-confirmation.

- Market breadth lagging price — the % of S&P 500 stocks above their 50-, 100-, and 200-day moving averages have all failed to reach new YTD highs despite the index’s breakout

- Stagflation signals building — Empire and Philly Fed surveys both showed strong headline demand paired with surging price indices; Core PPI running above estimates.

- The Fed is now expected to cut by year-end — but with growth appearing solid and inflation risks simmering, the most likely reason is that recession risks are quietly being priced in

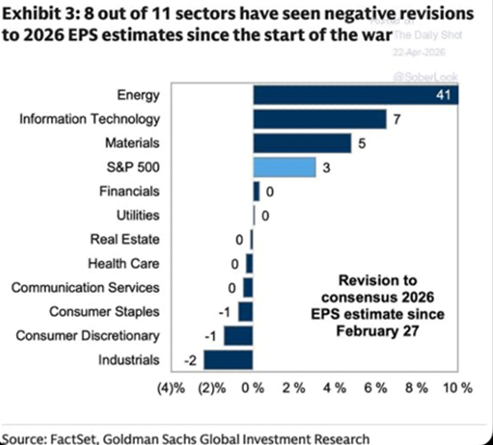

Corporate earnings have been good, but much of the boost in forward estimates is coming from commodity shortages and compute/memory shortages, while much of the rest in the real economy isn’t as strong. 8 of the 121 sectors have actually seen negative revisions to 2026 EPS estimates since March:

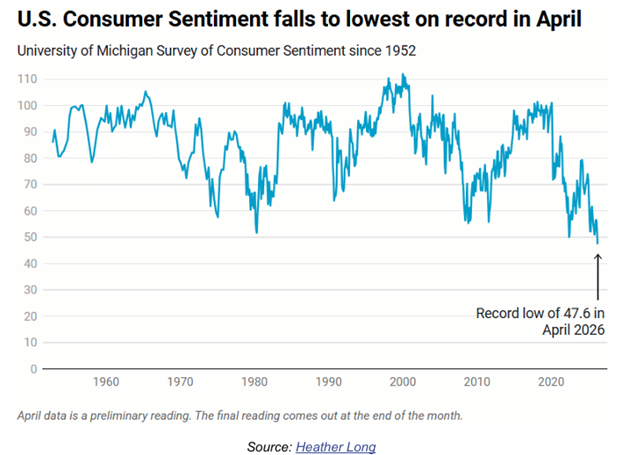

And finally, consumers aren’t happy. Below is the University of Michigan’s consumer sentiment index going back to 1952. This month it touched an all-time low, according to preliminary data. That’s remarkable because Americans saw some truly awful economic times over these years – far worse than today, by many benchmarks. Yet they are unhappier than ever. The aforementioned inflation and gasoline prices certainly don’t help, but sentiment was already deteriorating. A chunk of this is the partisan culture in the US that has been forming, however.

How Markets Could Continue To Rally Moving Forward

There are lots of tailwinds out there as well we have to balance along with the cautious data points. This is why I always include these for consideration – we need the signal, not the noise.

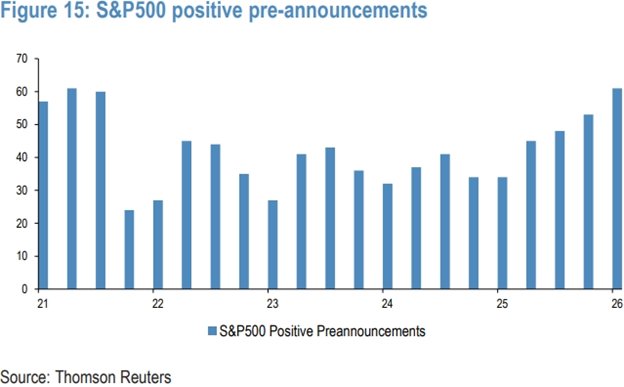

Company earnings are still doing very well. Despite geopolitical stress, the number of S&P 500 companies releasing positive preannouncements is the highest in 5 years:

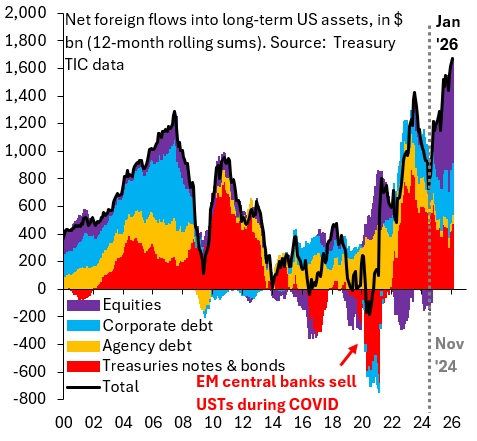

Has there really been a ‘sell America’ dynamic going on? Apparently not. Markets ignore much of the political volatility and continue to see the U.S. as the single best growth story out there. Foreign portfolio inflows into U.S. Treasuries, corporate debt and equities are the strongest in over 25 years:

Source: Brooks

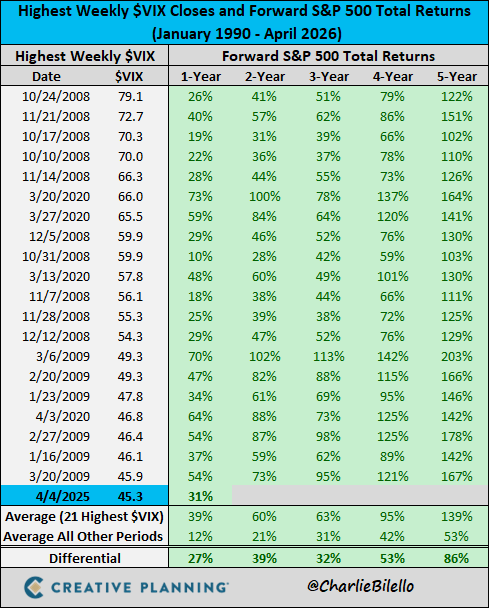

A year or so ago in April, on the back of Trump’s tariffs, the volatility index (VIX) ended the week at 45.3, one of its highest weekly closes in history. This is usually a big warning sign, but the S&P 500 has rallied 31% since then, adding to the list of times when it paid to be greedy when others were fearful.

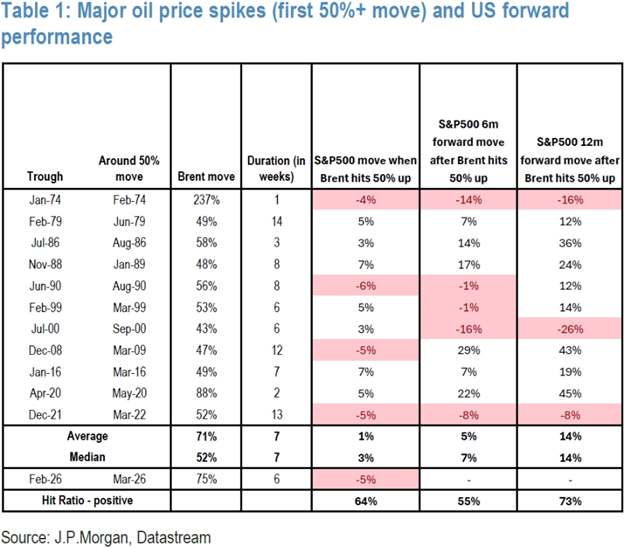

Market can do ok after oil spikes too. Below are the S&P 500 returns after major oil price spikes. Looking at all past instances of oil advancing at least 50-60% in a short space of time, equities on average delivered a +1% move during these periods, and the 6-month and 12-month forward equity returns were +7% and +14% for S&P500, with a 73% hit ratio over 12 months. So, the question is – is today similar to the few episodes where equities were down? - 1974, 2000, and 2022 - all of those had significant differences to the present environment I would contend.

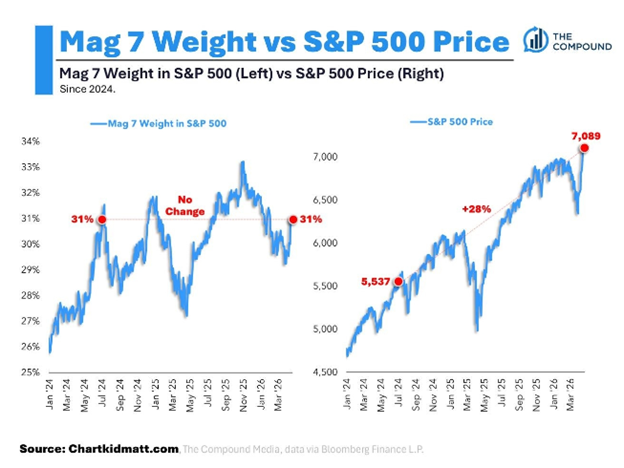

Unlike Canada, the US market is finally broadening out as well, it’s not just a story of the ‘Magnificent 7’ growth stock pulling everything higher. The Mag 7’s weight in the S&P 500 since July 2024 is unchanged and yet the index has rallied ~30%. The rest of the market is pulling its weight:

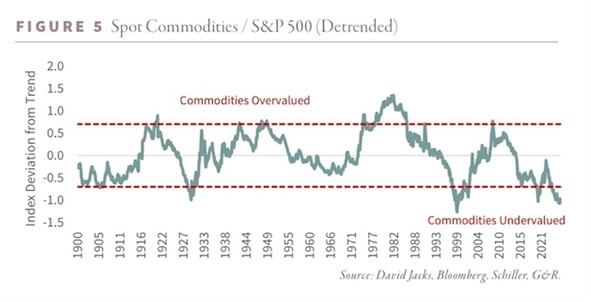

Even with the run in gold, oil and some materials, the commodity trade may still be in the early innings (we believe so, and are positioned as such):