Danielle Slavin and Brent Nichols

July 21, 2026

July 2026

The Global Insight 2026 Midyear Outlook is a lengthy document but we wanted to highlight a few of the items that we felt were important.

Strong earnings have supported equity prices this year but the conflict around the Strait of Hormuz could cause increased volatility in equities and bonds. In our view there isn’t an easy solution and this is why we are not extended in our positioning. We maintain a balanced equity approach not only to protect during times of weakness but also because there are “some investment opportunities built on structural forces powerful enough to transcend the noise of today’s investment environment”. While AI is one of the areas discussed starting on page 4 “The Unstoppables”, other areas include: the gray wave, electrification, renewables and also defense and medical devices.

An area of caution revolves around the US midterm elections. Page 17 highlights that “the S&P500 has experienced an average 21% correction surrounding midterm election years since 1934”. Corporate earnings have been strong enough to shake off some of these worries and as we start Q2 earnings, we will be looking for this trend to continue.

Central Banks at the start of the year were expected to drop interest rates but due to persistent inflation pressure, in large part because of the issues involving the Strait of Hormuz, RBC sees interest rates more likely to rise. See table on page 23. It is notable that the table shows that Canada could see the biggest increase in rates as tariffs with the US increase costs and add to uncertainty.

It is normal for the equity market to climb a wall of worry and we are monitoring these risks. As we have said, our positioning is not extended, we have been increasing the quality of the portfolios and our low volatility approach gives us the confidence to stay invested.

January 2026

The year has already started out with lots of worthy news items, so we thought we would share our thoughts on 2025 and expectations for 2026. The RBC Wealth Management Global Insight Weekly has a good review of how the US equity market did in 2025. Note for most accounts, we held 4 of the 7 most impactful stocks on the S&P 500 last year (see diagram on page 2). For 2026, RBC’s view around investment return expectations is aligned with ours…."We think a ‘positive’ rather than ‘above-average’ year is the outcome to plan for”. We believe continued improvement in market breadth and a positive economic environment in the US are tailwinds for equity markets.

We are determined to continue to manage any market volatility we expect this year in a prudent fashion and ensure there is a strong connection to your individual investment plan. As always, we would be pleased to discuss this in more detail personally.

November 2025

Hard to believe it’s November already and the holiday season will be upon us soon. As we approach the home stretch for 2025 in what has been a better year for equities than many expected at the April “liberation lows”, we wanted to share our thoughts on where we go from here.

Attached we include a Technical (using trends in market data to identify opportunities) report, Trend & Cycle: The Long View – November 2025. While some of you will like the detail and the charts included in this report, many of you are more interested in the bottom line. So with that in mind, the long term is still supportive of markets, however there are some reason for caution in the short term (you may recall that we have been counselling some caution in our past notes). This section from page 2 summarizes the current situation very well, in our minds.

The bottom line is that while historically high valuations and market concentration remain an understandable concern for fundamentally focused investors, we believe the current technical backdrop remains supportive of staying invested in equities with the caveat that a pause or pullback would not be surprising before year-end. Our recommendation continues to be for investors to use recent strength in equities to rebalance portfolios to maintain diversified equity exposure and to be cautious chasing the well-advanced leading stocks in fear of missing out.

This statement mirrors our positioning and strategy. Specifically, we have done the following in 2025:

- Reduced equity positioning slightly

- Maintained a balance of leading growth stocks with more defensive and dividend oriented stocks

- While we typically re-balance holdings annually, we decided to do a mid-year trimming of some stocks which had really moved up strongly

As always, please let us know if you would like to discuss anything in this report.

September 2025

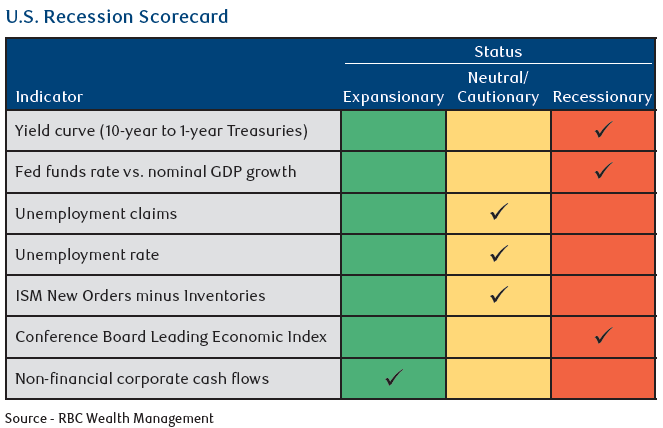

We hope everyone had a wonderful summer! With Fall fast approaching, we wanted to reach out and provide some thoughts on the markets and our strategic investment positioning. RBC’s US Recession Scorecard has been updated and is essentially unchanged from the last time we shared this with you. These findings give us confidence that maintaining our cautious approach is the best strategy for now. Despite this report being “inconclusive”, there are reasons to be more hopeful. In particular, the Central Banks in the US and Canada are now contemplating interest rate cuts this Fall, which should be supportive of Equity markets.

Should you have any questions about this report or our investment strategy, please reach out as we would welcome an opportunity to connect with you.

June 2025

Summer is fast approaching and we wanted to provide a couple of updates for you.

Firstly, Danielle is heading away with her family for a couple of weeks to Europe at the beginning of July (July 1st to 20th inclusive). This will be her first time away from the office for longer than a week in the past 10 years and it’s Kate’s first trip to Europe. Needless to say – we are all excited to explore the sites. First stop is to visit Harry Potter at the Warner Brothers Studio in London before heading to Legoland in Denmark and finally some hiking and exploring in Norway. In Danielle's absence, please contact Anita at anita.shin@rbc.com or by phone 604-257-3200. You may also contact Alison at alison.baker@rbc.com or 604-717-2127.

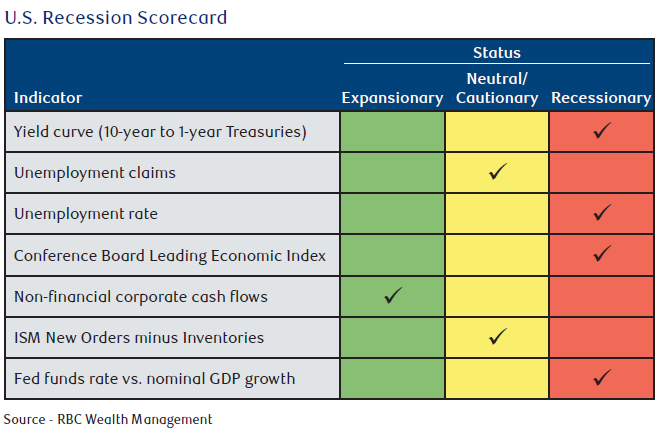

Secondly, the positioning of our investments under care became slightly more defensive earlier in the year. Obviously, tariff discussions have been considered but there is also a mix of other factors that have influenced us. While not all the news has been negative, the uncertainty of economic outcomes has risen this year, in our estimation. Thus we believe a little more caution remains warranted for now. The latest Global Insight Weekly features an updated U.S. Recession Scorecard. While there has been some improvement this month, it is still a mixed message. We would like to point out that the Yield Curve indicator is pointing towards expansionary economic conditions by most measures. While the Committee has kept the Yield Curve in the red for now to be prudent, it is important to emphasize that we are seeing some improvement there.

May 2025

The latest Global Insight Weekly has a really good article on the current challenge of the Federal Reserve (FED). Usually when there are concerns about the economy the Fed acts like the calvary and comes to the rescue. However, the Fed is somewhat boxed in by inflation concerns. This is why we have raised the amount of dry powder (cash) in client accounts and, where mandates allow, continued to overweight Alternative strategies, which can provide steady returns regardless of market directions. In our view, a more balanced investment strategy is prudent until we get more certainty on tariffs and the impact on the economy.

April 2025

So called “Liberation Day” did not feel that liberating, as stock markets responded negatively around the world. For over a month now we have increasingly viewed our positive expectations for markets to be in jeopardy. While we expected heightened volatility, Trump 2.0 seems more determined to play a longer game in his efforts to change US trade relations, regardless of who this impacts in the US and elsewhere. With this in mind, we have been incrementally increasing the defense in our client portfolios. Attached is the latest RBC Global Insight Weekly, which has some analysis and thoughts on the latest tariff announcements. As always, please reach out if you would like to discuss.

February 2025

Many investors are feeling nervous due to the ongoing headlines regarding US tariffs. In our last note, we referenced that we expected increased market volatility but remained constructive on the year ahead of us. The latest Global Insight Weekly goes a long way to explaining our comfort with our current investment positioning. What matters more for the market, Washington policy or plain vanilla corporate profit trends? While Washington, D.C. will likely capture a lot more business press headlines this year and policy developments could generate volatility, we think good old fashioned earnings trends will determine the U.S. equity market’s fate over the mid and long term. We look at the ongoing Q4 earnings season and the earnings outlook for the year.

Rest assured that we will continue to monitor the situation and will make adjustments if needed.

January 2025

Welcome to 2025! There is a lot of noise out there right now and divisiveness around politics continues. Despite all of that, the portfolios we manage are off to a good start and we wanted to share our thoughts for 2025.

We remain bullish and are not amending our asset allocation at this time. There are certainly things to be concerned about but as we know “the stock market climbs a wall of worry”. We have many Fundamental Analysts, including some that are exclusive to our firm, to help us with our investment decisions. We also use Technical Analysis as part of our process. We have discussed the slower recovery that we expected after the challenging market of 2022 and this did in fact come to pass. Now the question is: where do we go from here? Technical Analysis can help put where we are now into perspective and provide insights for the year to come.

The latest “Trend & Cycle: The Long View” from Robert Sluymer, Technical Strategist of our Portfolio Advisory Group shows that the market moves in long term bull and bear markets. We are currently in a secular bull market that could last into the next decade. Obviously, within these bull markets we can have significant corrections like we saw in 2020. It also shows that these corrections or cycle lows typically occur every 3-4 years. Therefore, based on this analysis, we remain positive on equity markets because we are in a secular bull market and still in the early stages of the shorter 4 year cycle. To us, this helps us remain confident in our positioning despite some high valuations among a few stocks. Valuation levels impact our stock selection but not necessarily our overall asset allocation decisions. The same goes for potential tariffs. It is influencing our stock selection and industry allocations, but not our view that markets will remain positive this year.

We trust you will find this helpful and please reach out if you would like to discuss.

December 2024

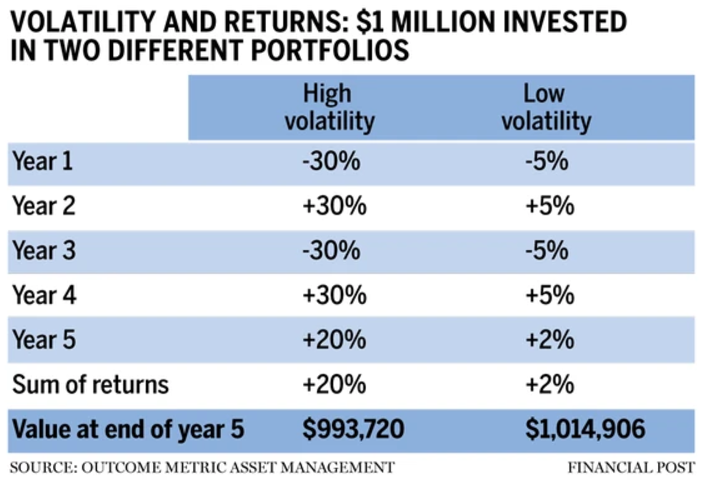

As we come to the close of another year we look back at our multi-year forecast of a “U” shaped recovery (slower recovery) and see that this is what has in fact transpired. Based on this forecast we have positioned portfolios for something different each year: 2022 - time for protection; 2023 - time for patience, 2024 - time for rewards. Indeed, as we look at our portfolio returns, we are pleased with the strong performance we are seeing this year. Our prudent investment style is to protect on the downside and be aware of the pattern of returns we deliver as this can be more important than total return; especially when drawing from the portfolio. We read an article this year that we could relate to, as it spoke to the benefits of protecting capital and not chasing returns. Our clients have seen us protect investments in times of market turmoil and this article does a good job of explaining why this is important. The below table from the article in particular quantifies the importance of managing volatility and the numbers may surprise some people.

Future notes to you will focus more on our thoughts for 2025, but in the meantime, enjoy this article and we look forward to connecting soon.

Wishing you health in happiness.

October 2024

The latest U.S. Recessionary Scorecard has not changed month over month and still strikes a cautionary tone about the U.S. economy. But, with respect to the equity markets, we remain bullish. While we expected the economy to slow this year, two things have kept us bullish: 1) the slowing economy would help lower inflation and allow the Federal Reserve to cut interest rates and 2) we felt the slowdown would result in a “soft landing” i.e. mild economic slowdown, which the equity markets had already priced in.

RBC has been more bearish on the economy than we have been this year but we see a couple of positives out of this report. Firstly, the Scorecard did not deteriorate further this month. Secondly, RBC writes that they can’t “…unequivocally rule out the possibility of a soft landing for the U.S. economy”. Ultimately, falling interest rates should help the Scorecard and supports the old adage: “Don’t fight the Fed”.

September 2024

The Federal Reserve (“Fed”) began its interest rate-cut cycle by announcing a 0.50% reduction this week. Prior to the announcement, markets were debating between a 0.25% or 0.50% cut. However, the Chair of the Fed suggested the 0.50% reduction was appropriate to ensure strength in the US labour market can be maintained in the context of more moderate economic growth. We view this positively for markets and surely, this gives Canada more leeway to be more aggressive with their rate cuts as well.

Aside from the Fed’s policy decisions, many of our clients are asking us for our thoughts on the US election and how it could influence markets. As such, we wanted to share the current RBC Global Insight Weekly, which offers an interesting comparison of Trump’s and Harris’ platform policies. Regardless of the policy differences, we would draw your attention to the section titled “Presidents don’t govern the stock market”. This report argues that non-political items such as the business cycle and the Fed’s monetary policy etc. will likely play a greater role in shaping markets than will the election outcome. Accordingly, we are not implementing any major investment changes based on an expected outcome of the US presidential election.

August 2024

We wanted to share our current thoughts for the markets and our portfolio positioning. We have seen increased volatility of equity markets around the world recently; especially on Monday. We view this as normal ups and downs as “the stock market climbs a wall of worry” as commentators often say. US employment information has been softer and we believe the Federal Reserve (“FED”) will switch from focusing on inflation and move to supporting employment. This means that it is nearly certain that the Fed will start its process of cutting interest rates at their next meeting in September. Both bond and equity markets will find this comforting. From an investment perspective we remain optimistic and have positioned portfolios accordingly. These market adjustments are a good reminder to stay diversified as those who did will find the recent volatility more muted in their portfolios, which allows us to continue to buy into good companies at more favourable prices.

Hope everyone is enjoying their summer so far!

May 2024

We typically send comments out on macro-economic thoughts and how they relate to our future view of markets and portfolio positioning. As part of our commitment to develop high-impact expertise we also take advantage of the insights that technical analysis can provide. This helps us with short-term timing of trades. It also provides important information about longer term positioning; for example, our technical analysis has been showing that we are in a secular (longer-term) Bull market.

Robert Sluymer, our Technical Analyst at RBC Portfolio Advisory Group, provides regular commentary and weekly interactive discussions with us. A couple of items stood out for us in his latest report:

- The "S&P 500 Advance – Decline line" shows that since last November this has been increasingly positive, meaning the breadth of the market is improving and thus indicating a healthy, more sustainable equity market.

- The other graph that we thought was interesting was the graph on Copper and Gold prices. This confirms our positive view on Material stocks and while the steep recent run up in prices could lead to some volatility (like we saw last week), the analysis suggests that any weakness is expected to be short lived.

We welcome an opportunity to discuss this with you in more detail if you have any questions.

March 2024

We have some exciting news to share! Danielle was invited to be a guest on the Contractor Evolution Podcast to discuss risk mitigation strategies for business owners. Contractor Evolution provides weekly insight to over 40,000 developers and contractors through interviews with professionals and “people in the know”. This interesting and insightful discussion will be helpful even if you are not a contractor or developer, as there are common threads that transcend different industries and family situations.

To quote Contractor Evolution, it's a good reminder that "the affluent business person you want to become doesn't get there simply by always making successful bets. The part you don't see is the huge losses they avoided". It was incredible for us to have Danielle included in a conversation that so closely mirrors our beliefs around investment management, namely that protecting on the downside is an integral component to pursuing long-term compounded growth.

We are pleased to share this podcast with you! Enjoy and please share with anybody you think could find this helpful:

March 2024

After a strong finish to 2023, markets are currently inclined to embrace a risk-on bias as per the Global Insight Weekly. At the beginning of the year the US bond markets were pricing in seven 25 bps interest rate cuts from the Federal Reserve. Interestingly, at the same time, EPS (earnings per share) estimates for the S&P 500 stock index were pricing in healthy double digit percentage gains. Hmmmm, we thought…how could you get both?! If EPS growth is strong because the economy is good, what would the incentive be for the Fed to cut rates and risk inflation coming back? As we said last summer in one of our notes, we are feeling more positive about the US economy and it is likely that a recession can be avoided or delayed for now. Therefore, we felt the estimate of six rate cuts this year was optimistic. See graph titled: “Interest Rate Expectations Have Been Pushed Back”.

This recalibration of interest rate expectations has challenged most bond sectors year to date. Our base strategy is to underweight bonds and be neutral equities. So far this tactical strategy has been beneficial. Looking forward, the general consensus across various managers, analysts etc., has been for modest equity returns with some weakness in the first half of this year. In fact, it was very hard to find anyone with a strongly positive view of equity markets. In our experience, when everybody has the same view, it is better to go in the opposite direction. Given the better equity breadth and good employment picture, we would view any sustained selling pressure as an opportunity to add to our equity positions.

November 2023

Markets had a positive start to November, which is seasonally a better period for equities, typically. After a difficult spell in September and October, we were pleased to see a good week! The attached Global Insight Weekly starts with a good discussion on the news that supported the recent drop in interest rates, which resulted in nice price gains for bonds. The good news didn’t stop there as lower yields also helped equities.

North American economies showed some signs of slowing this week, but since markets have been expecting this we ultimately see this as good news. Softer economic indicators take pressure off of interest rates thus supporting bond and stock prices. As we work through the “U” shaped recovery (as opposed to a quick “V” type recovery) our message and investment strategies have shifted. Protection was our strategy in 2022, this year our message was patience as we incrementally prepared portfolios for better times and heading into 2024 we believe better returns will be available from bonds and stocks.

July 2023

This year, we've noticed some frustration among investors due to Central Banks' ongoing interest rate hikes and lingering uncertainty about the economy's direction. Such reactions are typical during a "U" shaped recovery in the markets, where corrections take longer compared to the swift "V" shaped recoveries we've experienced in the past. What sets this period apart is that Central Banks are not coming to the rescue; rather, they are intentionally presenting additional challenges.

In our initial note at the start of the year, we emphasized the importance of patience and seizing opportunities to transition from defensive to offensive strategies. In the first half of the year, we successfully adjusted the portfolio by unwinding some of our overweight to cash and investing in more bonds and equities.

Looking ahead, we have several reasons to be optimistic:

- Attractive Bond Yields: Bond yields are currently more appealing than they have been in over a decade. For instance, High Yield bonds are offering returns in the 10% range.

- Potential End to Rate Hiking Cycle: Central Banks may be nearing the end of their rate hiking cycle, which could have positive implications for markets.

- Soft Landing Likely: There is an increased likelihood of a soft landing for the economy in North America as opposed to a more severe downturn.

- Positive Portfolio Returns: Our portfolio has already yielded positive returns year-to-date, indicating progress in the recovery.

- Broadening Stock Market Performance: The stock market is showing improved breadth with more diverse stocks performing well, rather than relying on a handful of technology stocks.

While we anticipate some market volatility to persist, we continue to believe investors will be rewarded for their patience. We are increasingly hopeful about the future and believe that the current environment presents opportunities for growth.

As always, we are here to address any questions or discuss these matters in greater detail. Please don't hesitate to reach out to us.

May 2023

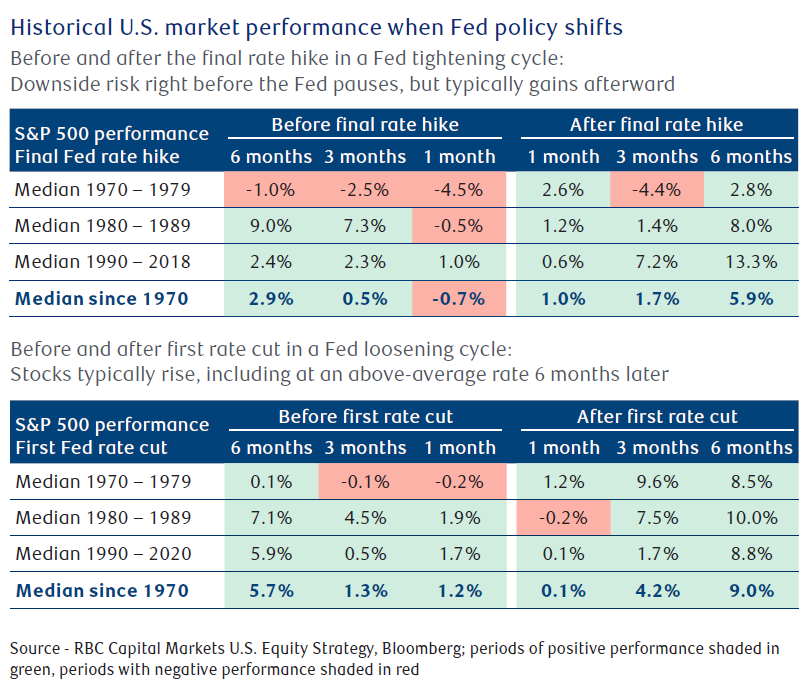

After a decent, yet volatile, start to the year for markets, the news cycle pushes on with an air of pessimism for what lies ahead. For clients, we remain conservatively positioned as we are monitoring the US regional banking system stresses, the US debt ceiling discussions and the increasing likelihood of a recession. While this means we are being patient and making sure we are getting good income from interest and dividends, we are also alert for opportunities to become less conservative and position ourselves for more growth. This is because there are a couple of silver linings as per the most recent Global Insight Weekly. Specifically: “(1) The S&P 500 typically bottoms well before economic conditions improve, and often when headlines and investor sentiment are still rather negative, and (2) a shift in Fed policy could support the market overtime.” The below chart shows that the median return on the S&P 500 since 1970, 6 months after the last Federal Reserve interest rate hike, is 5.9%; thus supporting our view that despite the pessimistic news cycle, there are opportunities to position client portfolios well for a recovery.

March 2023

Given the failure recently of some US regional banks, we wanted to share a market update: The SVB collapse: Reverberations & reactions. As a quick summary the second paragraph and the last paragraph are the most important to investors.

“In the opinion of RBC Capital Markets, LLC’s lead U.S. bank analyst Gerard Cassidy, the joint action of regulators on Sunday regarding SVB and their other decisions to support the banking system ‘reduces any contagion risk from the Silicon Valley Bank failure.’”

“The Fed likes to state that it is ‘data dependent’ when it comes to making interest rate decisions. We think the SVB crisis is a big data point that the Fed can’t and won’t ignore. In our view, it argues that the Fed should pause its rate hike cycle sooner rather than later, so as to let the financial system and economy absorb the significant hikes it has already implemented.”

We remain conservatively positioned at this time. We did see an attractive entry point to add to our bond positions in client portfolios a couple of weeks ago. This move did an excellent job of offsetting some of the recent equity volatility.

December 2022

As we are approaching the end of a volatile year in markets in 2022, we thought we’d share RBC’s 2023 Outlook to provide an indication of what to expect for the year to come. This document is 40 pages but the first section written by our esteemed and very experienced colleague, Jim Allworth, Investment Strategist and Co-Chair of our Global Portfolio Advisory Committee, is always worth paying attention to. Essentially the view is that the US recession will come mid-way through 2023. For Investors it’s important to know that we are likely closer to the end than the beginning of these trying equity results, as markets typically start moving up 3 to 5 months prior to the end of a recession.

For our clients we continue to remain tilted to a defensive positioning and acknowledge that the first half of 2023 will most likely remain volatile.

Best wishes for 2023 and thank you for entrusting us with your investments. We never take that trust for granted.

October 2022

For this month’s commentary we thought we’d share another audio file featuring Jim Allworth, Co-chair of RBC’s Global Portfolio Advisory Committee, in which Jim shares his views on the continued market volatility, and why investors should remain mindful of the longer-term drivers of investment returns. In our view this commentary is timely and touches on a number of important questions that we believe are top of mind for a lot of our clients – specifically: how do the heightened recession fears and the more challenging outlook for markets in the short-term impact the long-term nature of investing?

The audio file is broken down into three sections. We’ve provided time stamps for the themes discussed should you wish to click ahead to a specific topic:

- Introduction – 0:00

- Inflationary pressures and the current recession risk – 0:38

- Recent behaviours within bond and equity markets – 5:45

- Short-term versus long-term focus – 14:32

We continue to be overweight cash in client portfolios while we monitor market and economic conditions for signals to redeploy cash into other asset classes.

As always, please let us know if you’d like to discuss this in more detail.

July 2022

Summer has finally arrived, and we hope everyone is getting out and enjoying the sunshine and good weather.

As markets transition into the second half of the year, we wanted to share the midyear outlook from Jim Allworth. It provides a summary of what has occurred over the first half of 2022, but more importantly it discusses what the path ahead might look like. The article outlines two possible scenarios and unsurprisingly, inflation is still at front and center.

The first scenario is one in which inflation remains stubbornly elevated, forcing central banks to continue to tighten financial conditions. In the second and more ideal scenario, inflation recedes, the economy slows, and the need for more tightening declines, thus leading to the possibility of a soft landing. Which is more likely?

“In our view, it could take six months or more to determine whether the economy islanding softly or heading into a recession”. Until a catalyst emerges, such as softer inflation readings, both outcomes are plausible and “the most likely path for equity prices through the remainder of this year will be generally sideways”.

As we continue to focus on economic and inflationary data that is released monthly, we are at a point where bad news is good news for markets. As counterintuitive as this might sound, a slowing of the economy (i.e. bad news) may cause the Fed to increase rates at a slower pace, a lower magnitude, or both (i.e. this could be good news for markets).

In the meantime we continue to be positioned defensively in client portfolios with an overweight to cash.

May 2022

April was a particularly difficult month for both bonds and equities as markets adjusted to higher interest rates. We have seen a dramatic move in interest rates since the pandemic started. In 2020 the 10 Year US Treasury yield dropped to about 0.50% and most recently it touched 3.00%, with a lot of that increase coming this year. Remember last year when the Fed was saying that inflation was just transitory and don’t be worried…?

In terms of client portfolios, we have made some moves to reduce risk and add defense this year, and we continue to be underweight bonds as has been the case for some time now. So where do we go from here? We have highlighted some quotes from the recent Global Insight Weekly that we think are important considerations in terms of the short-term outlook for markets:

We continue to believe the S&P 500 has the potential to be higher than current levels in the next 12 months primarily because U.S. recession risks are no worse than moderate as things stand, a number of economic indicators are sturdy, and earnings trends are still generally good. As long as the end result is an economic “growth scare” instead of a full-blown recession, and Russia and NATO avoid direct clashes, we think any further market downside should be limited.

From a technical perspective:

RBC Wealth Management Inc. Technical Strategist Rob Sluymer notes two lines in the sand that are coming into sharper focus. The first concerns the S&P 500 Index. He believes this measure of the broad U.S. stock market must hold at the critical support band between 4,100 and 4,200, near its year-to-date lows. A break below this band would, by definition, confirm a new downtrend for the market.

The second relates to the benchmark 10-year U.S. Treasury bond interest rate. If this yield pushes above technical resistance near the recent cycle high between 3.00% and3.25%, it would likely trigger additional risk-off behavior, according to Sluymer. Recently, bond yields have tempered their rise; if the pause continues, it may prove to be an important reprieve for equities.

While it appears that a lot of the bad news has now been “priced in”, we remain cautious in light of Rob Sluymer’s lines in the sand as mentioned above.

April 2022

The primary article in this week’s Global Insight Weekly discusses the war in Ukraine and how equity markets have essentially already moved pass them. They also note that Canada and the US are well insulated from possible economic fallout versus say Europe. For clients that had Emerging Market exposure we sold this off before the Russian invasion of Ukraine as we were worried about bigger possible economic fallout in those regions and to ensure we didn’t have any Russian exposure.

As heartbreaking as this war is and the massive amount of media attention that it is garnering, there is something much more mundane that we are watching closely from an investment strategy perspective. Developments in the bond market have been noteworthy fora couple of reasons:

Firstly, bond yields have moved up sharply due to inflation and anticipated central bank actions. This has had an impact on interest sensitive investments. For example, the US Aggregate Bond index was down 3.1% in the month. While this means better opportunities for bonds down the road, it was a painful adjustment in bond prices. For clients, our practice has been to underweight bond exposure, as we felt inflation and ultimately interest rates would be increasing.

Secondly, the shape of the yield curve is a good predictor of future economic activity. If shorter rates start to yield more than longer rates, it could mean that a recession is coming in the next 6-12 months. "While we believe the flattening yield curve is worth keeping an eye on, we note that the spread between the 1-year and 10-year yields, which the Global Portfolio Advisory Committee monitors as part of its U.S. recession scorecard, has not inverted. This leads us to believe recession speculation is likely premature”. While it may be premature, the yield curve has been flattening and we are factoring this in to our portfolio decisions.

As always, we are happy to discuss this with you in more detail.

March 2022

Happy International Women’s Day to all the amazing women in our lives! Danielle was interviewed this week by Charitable Impact regarding her experiences as a woman in the industry as well as how the team supports clients with their charitable intentions. One interesting fact is that Danielle was heavily influenced by her own mother’s involvement in various charities and board work. Regarding charitable giving as a family event, Danielle says, “The really fascinating thing about charitable giving is how well it can act as an education tool for many family and financial matters. A real life-lesson in gratitude”.

If you are curious to read the article, please click here.

March 2022

The situation in Ukraine is nothing short of devastating. The human impact has been heartbreaking and as fellow parents, difficult to watch and imagine what families are experiencing. In light of events and within our role as Portfolio Managers, we wanted to share an audio commentary

by Janet Engels, Head of the Portfolio Advisory Group – U.S., to explore the economic aspect of the crisis. Specifically, how the economic sanctions and expanding supply chain issues will impact businesses and our outlook/positioning for this year.

The audio file is short (about 11 minutes), but informative. Janet makes quick reference to the global reliance on Russia for oil but also commodities in general. Within the portfolio, you may recall that we have been adding some commodity exposure over the past year or so. Adding mining exposure required research to ensure we were comfortable with the environmental impact of the companies we were investing in.

Janet makes a good case to stay invested. She quotes that the time for markets to recover from past acts of war was “remarkably similar, four or five months to get back to even, and if we look past that, six to twelve months after, the average recovery was 24 to 30% higher”. We have repositioned portfolios this year to remove Emerging Market exposure and build up cash reserves, but we believe Janet’s wisdom is correct and that the economic strength we are expecting for 2022 will materialize and ultimately result in higher stock prices.

If you have any questions or concerns, please don't hesitate to reach out.

February 2022

Given the volatile start to the year, we thought it would be timely to share an audio commentary by Janet Engels, Head of the Portfolio Advisory Group – U.S., where she talks about what’s causing the recent volatility and whether that has changed her group’s outlook and positioning for the year.

You may recall from our March 2021 commentary that we were expecting inflation to be more sticky and not as transitory as many initially thought. With this view we positioned portfolios accordingly and it factored into our trade decisions throughout last year. Specifically, our decision to generally underweight fixed income and shorten duration within our bond positioning (lower the interest rate sensitivity) has worked well given that rising rates have put pressure on bond prices. On the equity side, our decision to reduce growth areas such as small cap and technology, and increase the allocation to commodities and bank stocks as an inflation hedge has also proven to be very effective.

Going forward, we expect markets to gradually settle into the understanding that stimulus is being reduced from the system on the basis of very strong economic background. However, there is a big difference between the Federal Reserve starting to tighten the supply of money, and actually decreasing the supply. This is not something that will happen overnight and it will likely take years for the economy to revert to just average growth. Until then, we expect the economy to continue to expand, and both profits and asset prices to continue to climb, with stocks outperforming bonds again in 2022 (albeit with a more muted gap between the two asset classes than we’ve seen in recent years).

As always, if you have any questions, we would be more than happy to connect.

December 2021

To wrap up the year, we did an interview with Jim Allworth, Portfolio Strategist at RBC Dominion Securities, who provided his expectations for financial markets as well as some guidance around portfolio positioning.

Our bottom line takeaway is that while there are always risks in the short term, we feel comfortable with the economy and financial markets moving into 2022. One caveat is that we feel equity returns will be more subdued in 2022 following what has been three fairly strong years. In terms of positioning, as a reminder, we have been increasing exposure to growth stocks in client portfolios since March 2020 in order to complement our core dividend-paying holdings. This “barbell” strategy has helped diversify the portfolio between the two styles, with each outperforming the other at various points this year. More recently, we have been taking profits on some of the growth we added in 2020 and will continue to look at opportunities to rebalance throughout next year.

October 2021

We hope everyone is settling into Fall and for those with children and grandchildren in their lives, we hope the transition to school has been smooth. In our household, Kate started preschool. So far she is loving it and bringing home an assortment of crafts and germs each week.

Markets experienced their own flu-like symptoms in September too. Accordingly, the start of this week’s Global Insight Weekly provides a good overview of the diagnosis and expected path for recovery: "Given the tear it’s been on since the pandemic lows, it shouldn’t come as a surprise that the stock market would take a much-needed rest, even more so as it’s navigating through some challenges. And while there could be more volatility ahead, we think the bull market can work through the headwinds and ultimately move higher.”

The support for a continued bull market at this point shows up in a couple other areas of this commentary. The last paragraph on page 2 says "Despite the unique COVID-related headwinds, leading economic indicators are still signaling that recession risks are nearly nonexistent, household fundamentals remain strong, and earnings growth should persist, at least at a moderate pace”. Under the Market Scorecard on page 5 under Fixed income (returns), it shows that U.S. High-Yield Corp bonds performed better than investment grade bonds for the month of September, which is a sign that the bond market is not worried about a significant slowdown in the economy.

When in doubt, trust the bond market doctors. We take great comfort in the signals we are seeing from the credit environment that the recent volatility is a common seasonal cold with an expected recovery to be relatively quick.

August 2021

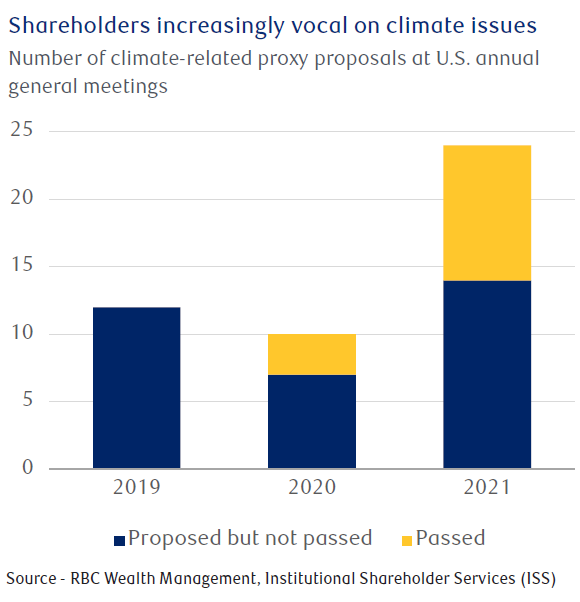

Maybe it’s the hot weather and forest fires we are seeing in the West this summer, but there was a brief comment in the Global Insight Weekly that caught our eye. Specifically the below graph showing the rise in climate-related board proxies. Not only was the increase in the last three years interesting, but in 2021 thus far, some of these are actually being passed at the AGMs whereas none were voted favourably upon in 2019.

Our view is that this is not a blip and is likely sustainable...pun intended. Our fundamental belief is that for companies to succeed and excel in the future, they too need to be conscious of their broader impact on our community and humanity in general. It is a business risk and ultimately an investment risk not to. This is why we use ratings from Sustainalytics and other sources as part of our investment process to analyze management quality and environmental exposure as a further level of risk mitigation.

Enjoy the rest of the summer!

July 2021

We hope everyone is well underway to receiving their second vaccine dose and is enjoying some new freedom to get out more. Local small businesses are eagerly awaiting our return especially while borders remain closed. Any support and spending you can give is surely appreciated.

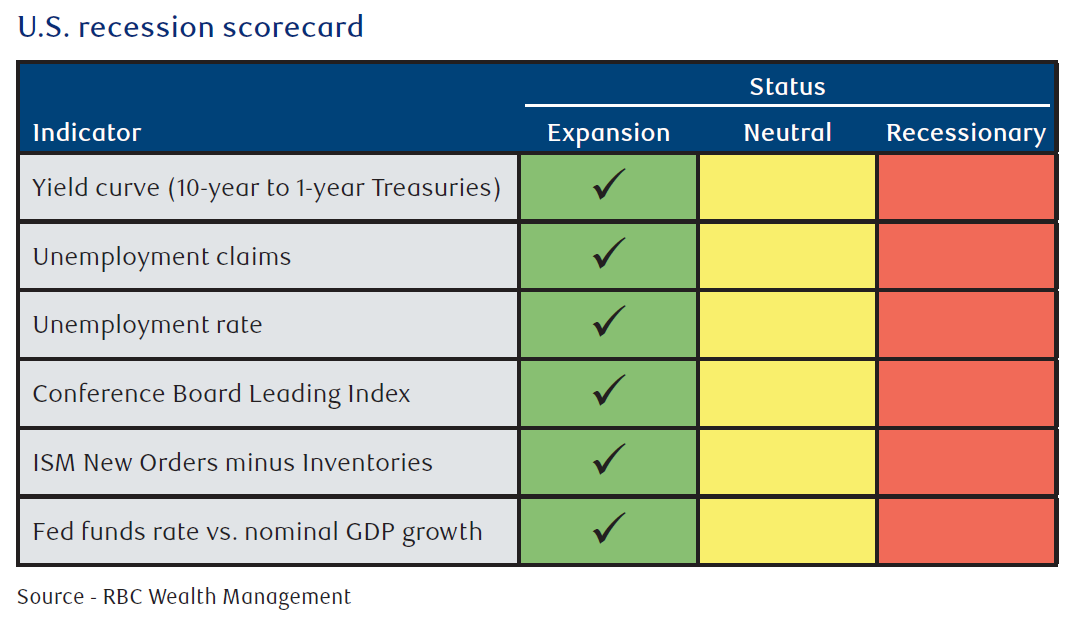

Within public markets, we want to share the latest “U.S. recession scorecard” from RBC's Midyear Outlook. Note that all indicators are pointing towards Expansion, which is supportive of equities. We follow this scorecard regularly and there have been times when the trend started to weaken or when the indicators were mixed. This is clearly not the case now. So while this is of course no guarantee, there doesn’t appear to be a recession on the horizon.

June 2021

What a change a month has made to the vaccine rollout! Early May saw people in their 50s and 60s receiving their long awaited first dose, and by the end of the month, people in their 20s were being vaccinated as well. We hope you are staying safe and that you and your loved ones have had the opportunity to be vaccinated too. Meanwhile, markets have mostly continued to climb higher in anticipation of a successful vaccine rollout and economic recovery.

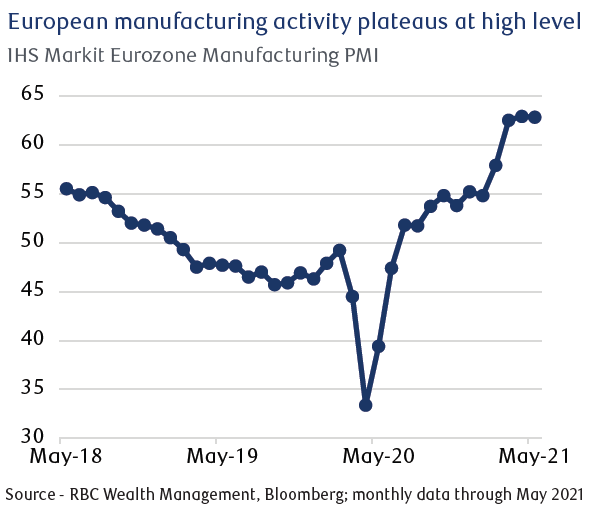

For this month, RBC’s Global Portfolio Advisory Committee featured an article on the positive European recovery (see graph below). With much of the world seeing good economic recoveries, our minds turn to interest rates and whether we could see some lasting inflation and therefore more increases in bond yields. The European Central Bank seems aligned with North America in that “the consensus sees the ECB waiting until around mid-2023 to raise its deposit rate”. So clearly, central banks in developed countries will favour growth at the risk of inflation. We will continue to monitor signs that could indicate rising rates and inflation, however, this shouldn’t materially impact our positive equity expectations in the near term and we continue to be overweight equities in client portfolios.

March 2021

The latest edition of the Global Insight Weekly focuses on the rise in bond yields. The 10Y US Treasury yields (interest rates) have increased about 70% this year. This is a fairly big move and has put pressure recently on both bond and stock prices. The article goes through a number of reasons why they don’t expect this to continue, however, in our view it would be prudent to consider rising yields as a significant risk to our favourable market forecast. If inflation rises more than expected or governments have trouble finding investors for their expanding need for bonds, then rates will increase and challenge bond and stock prices. We are factoring this into our security selection and asset allocation decisions to avoid or manage the more interest sensitive areas.

February 2021

The February Global Insight Weekly discusses concerns around a potential bubble in some markets. Certainly there have been some signs – for example Bitcoin and GameStop – but the broader market still has reasonable valuations and the backdrop is supportive of equities due to low interest rates and government spending. The last paragraph of the article talks about a recommended strategy that is aligned with our thinking:

"How to position? We maintain our Overweight stance in global equities, and we are willing to withstand possible volatility as we think equities will eventually move slowly higher over the course of the year. We expect the sector rotation into cyclicals that started in November 2020 to continue as the economy approaches a reopening. We would continue to look for exposure to more attractively valued cyclicals, without neglecting exposure to resilient defensive stocks."

As always, please reach out to us if you would like to discuss in more detail.

December 2020

Here is a comprehensive forecast that covers a number of questions clients have posed to us this year. Topics include capital market expectations, impact of rising government debt, higher inflation etc. This is worth a read for those that have the time to go through it.

For those that would like a quick summary we have highlighted a few items from page 2 of the document that were important to us:

- “The pandemic has marked the start of a new economic era – one where old rules are swept away. World governments are racking up massive borrowing, money is being printed to buy government debt at an unprecedented pace, and governments’ role as capital allocator has grown markedly.”

- “We expect worthwhile equity returns and strong earnings growth as COVID-19 economic headwinds diminish. The persistence of ultralow interest rates should support above average valuations and make equities the asset class of choice in 2021.”

- “With high debt levels and low inflation enabling central banks to keep interest rate slower for much longer, what worked in the past for fixed income investors may not work in the future. Investors should look to split the roles of safety and income generation in portfolios.”

We are generally aligned with RBC’s analysis. In particular, the last quote from the forecast document is the most important as low interest rates have an impact on portfolio construction. Client portfolios have gradually been amended to find other ways to deal with the issues of income generation while still maintaining our core belief of managing portfolio volatility. We would be happy to discuss this with you at your convenience, but please know that we are focused on finding solutions to the low interest rate environment we are in.

Happy Holidays and best wishes for 2021!

November 2020

With US elections mostly over, markets have turned back to focusing on the COVID-19 implications for the economy. The latest RBC Global Insight Weekly discusses the vaccines being developed and the timing of their availability. Markets tend to look forward 6-9 months when pricing stocks, so some of this good news is working its way into bond and stock prices this month. This helps support our strategy to maintain current equity allocations. Page 5 shows the month-to-date returns on various market benchmarks. Note that the S&P 500 is up an incredible 8.2% this month and the S&P TSX is up 6.4%.

As always, please reach out to us if you have any questions.

October 2020

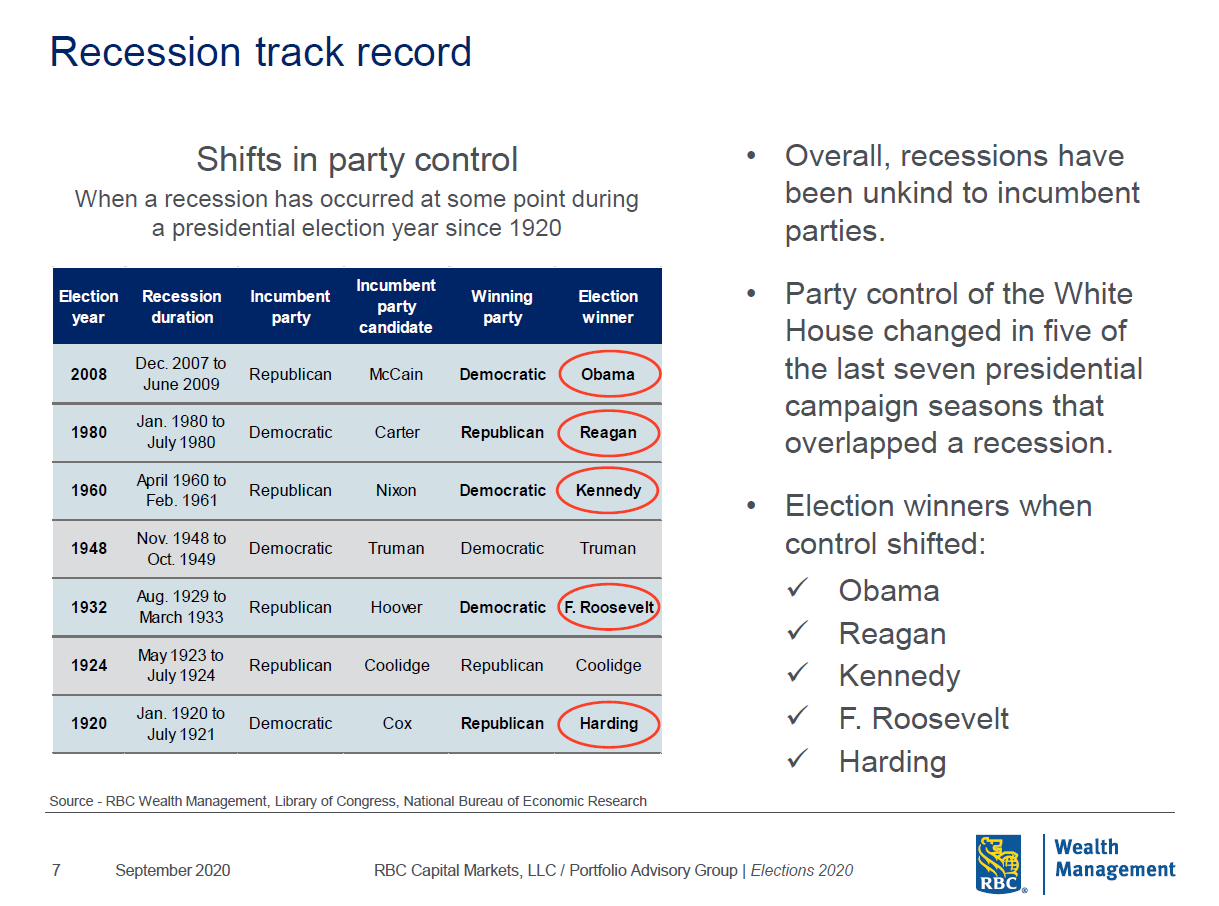

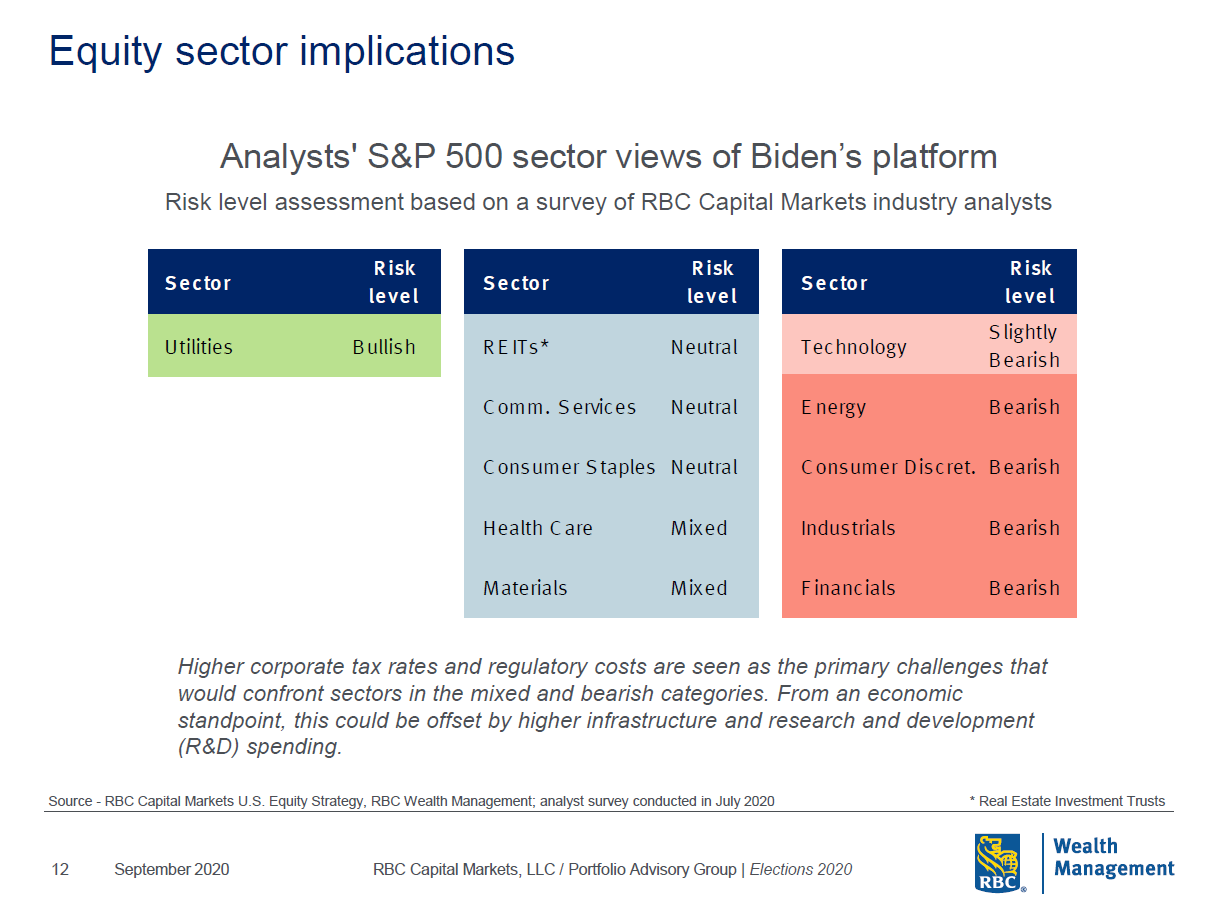

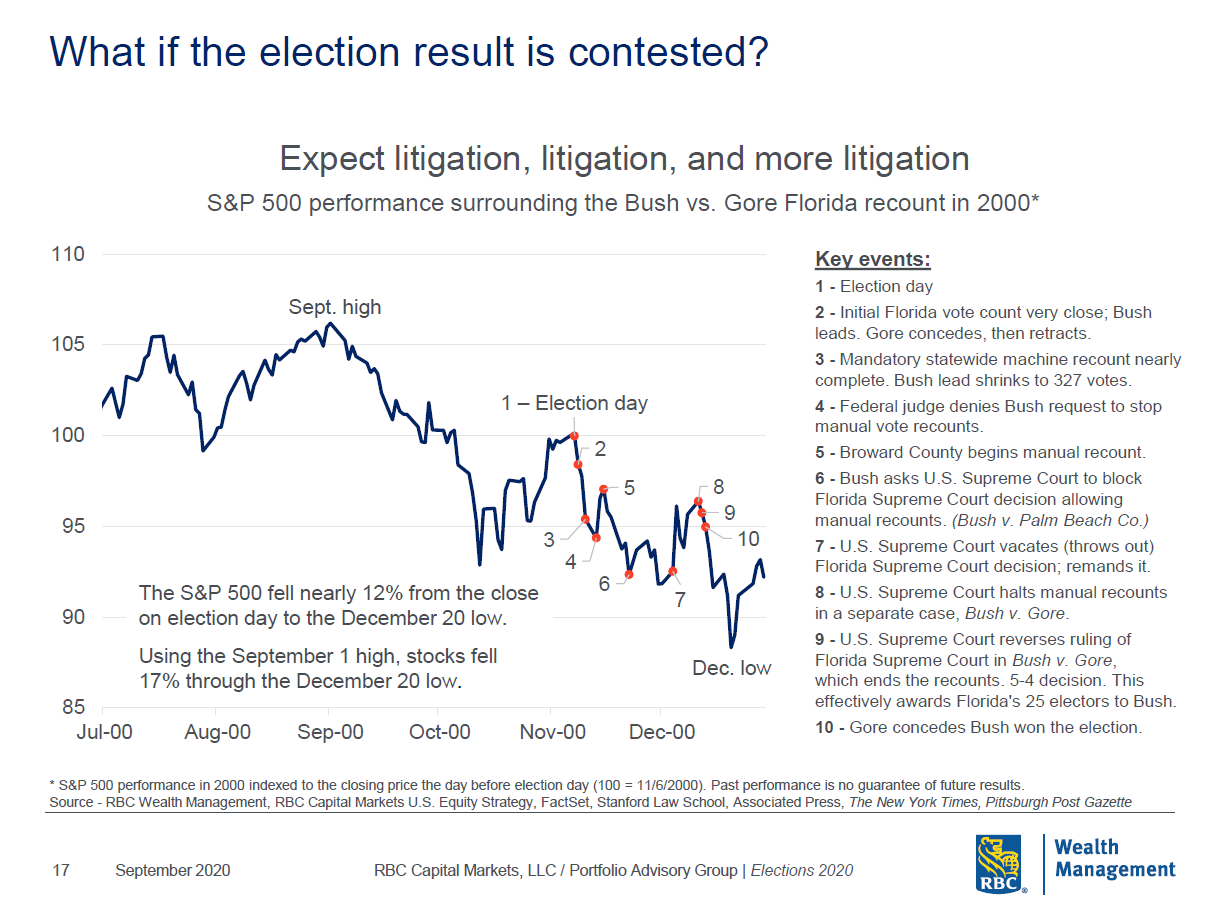

The US election seems to be on everybody’s minds right now, so we wanted to share our thoughts on the topic. We have included three slides with key points about the election and have added some comments for each below:

Who is likely to win? Slide 1 shows that incumbents are vulnerable if there is a recession. Given that we have had a recession this year, it would suggest a higher probability of a Biden victory.

What sectors of the US market are most vulnerable to the likely outcome? Slide 2 discusses the likely reaction by each equity sector if Mr. Biden does become President. We are probably better positioned if Mr. Biden wins as we are underweight to energy and financials (two of the key areas with bearish/negative outlooks under a Biden victory).

What if the election outcome is contested? Slide 3 shows what happened when there was a contested election in 2000 and the results were not good for the equity markets. However, if this were to happen in 2020, the reaction could be quite different as it wouldn’t be a surprise the way it was in 2000. The latest Weekly Market Insight analyzes the potential results, and the end result is that we would probably see some short-term volatility but nothing as dramatic as what we saw in 2000. Essentially, the market anticipates some controversy in the election results.

As always, please let us know if you have any questions.

Disclaimer: RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. â / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © RBC Dominion Securities Inc. (insert applicable year). All rights reserved. This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.