Nick Milau

April 23, 2026

Weekly Wrap

Global stock markets experienced a week of high volatility and record-breaking milestones, primarily fueled by shifting geopolitical headlines and the onset of the Q1 earnings season. The week was defined by a transition from ‘risk off’ to ‘risk on’ sentiment as investors reacted to potential de-escalation in the Middle East and cooling inflation data. US indices reached historic levels earlier in the week with the S&P 500 crossing the 7,100 threshold and the NASDAQ achieving its longest winning streak since 1992. As of writing, the Nasdaq is up almost 1.5% for the week, with S&P 500 green to the tune of .7% while the Dow seeped into the red by about .5%. The TSX is currently down about 1.15%. The Canadian index was heavily influenced by crude oil volatility. Brent crude surged to nearly $95.50 by midweek and fears of a continued blockade in the Strait of Hormuz provided a tailwind for Canadian energy producers. Market activity was further driven by a “Build Canada” investment cycle with significant capital flowing into infrastructure defense and power grid projects to support new data center build outs. Emerging Markets showed resilience, with the MSCI Emerging Markets Index gaining momentum toward the end of the week. Gains were largely spearheaded by Taiwan semiconductor and Samsung which benefited from the same global AI driven demand that lifted the NASDAQ. Gold, which had been experiencing some positive correlation to the equity markets recently, headed south this week. As geopolitical tensions eased somewhat, gold saw significant profit-taking. With US inflation data (PPI brackets) coming in lower than expected, there is a renewed focus on real interest rates. Historically, gold maintains a negative correlation with real rates; As the outlook for the economy stabilizes and stocks rally, the opportunity cost of holding non-yielding gold increases.

Market Insights

Checking in on the Canadian macro landscape. Canada is showing tentative signs of stabilization after a challenging start to the year. Real GDP growth reached 0.1% month-over-month in January, with February posting a 0.2% gain—tracking toward approximately 1.5% annualized growth in Q1. This modest rebound should help the country avoid a technical recession following Q4's contraction. On labour market and employment, March saw employment rise by 14,100 positions, partially offsetting the 109,000 combined decline in January-February. While recovery remains gradual, modest positive employment growth is expected throughout the year, which should help ease labour market slack over time. The housing sector continues to soften. Single-family home prices fell 0.3% month-over-month in March, with apartment prices declining more sharply at 0.9%. Excess supply indicators suggest annual house price declines of around -5% will likely persist through 2026. Headline inflation rose to 2.4% in March, partly driven by a 21% jump in gasoline prices. Core inflation measures remain broadly aligned with the Bank of Canada's target. Market expectations suggest interest rate hikes are unlikely this year given moderate growth and contained inflation pressures. While the Business Outlook Survey showed stronger sales expectations pre-conflict, sentiment has since turned cautious amid uncertainty. The newly secured Liberal majority is expected to have limited fiscal implications, though it may facilitate initiatives around natural resource exports, defense spending, and infrastructure approvals. Bottom Line: Canada's economy is stabilizing, but growth remains modest and uneven across sectors.

Asia-Pacific Markets & Green Technology Trends. South Korea is leading regional performance, with the KOSPI Index rebounding nearly 30% this month to reach all-time highs. Memory chip stocks are driving this rally, particularly SK Hynix, which reported exceptional results: revenue nearly tripled year-over-year to exceed 50 trillion won (US$35.6 billion) quarterly, while operating profit increased fivefold. Strong AI infrastructure investments sustained robust demand despite typical Q1 seasonality. Semiconductor export strength has bolstered South Korea's economy significantly. Q1 2026 GDP grew 1.7% quarter-over-quarter and 3.6% year-over-year—the fastest quarterly expansion since Q3 2020 and well ahead of consensus estimates. This reverses Q4 2025's slight contraction. However, the Bank of Korea remains cautious, projecting full-year growth may underperform earlier forecasts due to Middle East conflict uncertainties. China's green technology exports hit record levels in March, with electric vehicles, solar panels, and lithium-ion batteries surging 68% year-over-year. While U.S. trade barriers limit American market penetration, exports to most other regions performed strongly. Interestingly, the Middle East conflict may benefit China by increasing global demand for affordable renewable solutions. "New energy vehicle" registrations—including electric vehicles and plug-in hybrids—more than doubled year-over-year in Japan, South Korea, and New Zealand, while increasing over 50% in India, Australia, and numerous European markets. Asia-Pacific demonstrates robust tech-driven growth and accelerating green energy adoption globally.

Portfolio Update

No portfolio updates this week.

Planning On

Paying your tax bill

As we head into home stretch of the tax season, some of you may be facing a tax bill from capital gains realized in your non-registered accounts this year. Here's a friendly reminder: you don't need to drain your cash flow to cover it.

Consider funding your tax bill directly from the account itself. Since the gains that triggered the tax liability are already sitting in your portfolio, using those proceeds to pay CRA creates an efficient, self-contained solution, allowing you to maintain your cash position for other things that are important to you.

This approach works particularly well if we are holding some cash in these accounts or have recently trimmed positions. It's a straightforward way to let your investments "pay their own way" when it comes to taxes.

REMINDER:

In early December, we send each client who a holds non-registered account an email asking if they would like a preliminary gains/loss report. Simply respond with a “Yes, please!” and we will send one immediately. Armed with that information, you have time to implement tax minimization strategies before year-end if desired. Some strategies to consider include:

• Tax-loss harvesting – offset gains with realized losses (assuming your portfolio has some).

• Donating securities in-kind – support causes you care about while avoiding capital gains tax.

• RRSP contributions – reduce taxable income and boost retirement savings.

• Spousal RRSP contributions – optimize household income splitting and can be made even if you are over 72 if your spouse or common-law partner is still 71 or younger.

If you'd like to discuss how this might work within your specific situation, we're here to help.

This information is not intended to provide legal, tax, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified lawyer or accountant, as applicable, before acting on any of the information.

Message from the Admin Team

A quick note regarding client parking

Clients are welcome to park in any available stalls; however, please be mindful of the 2-hour time limit. Reserved Parking is available in stalls #7, #8, and #9 marked 'Reserved for RBC.' These stalls are located in the parking area facing Croydon, immediately to the left when you pull into the lot and have no time limit.

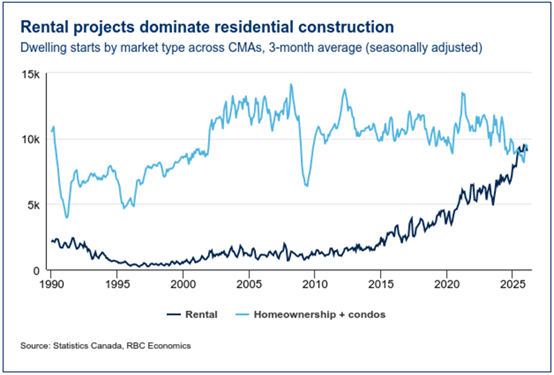

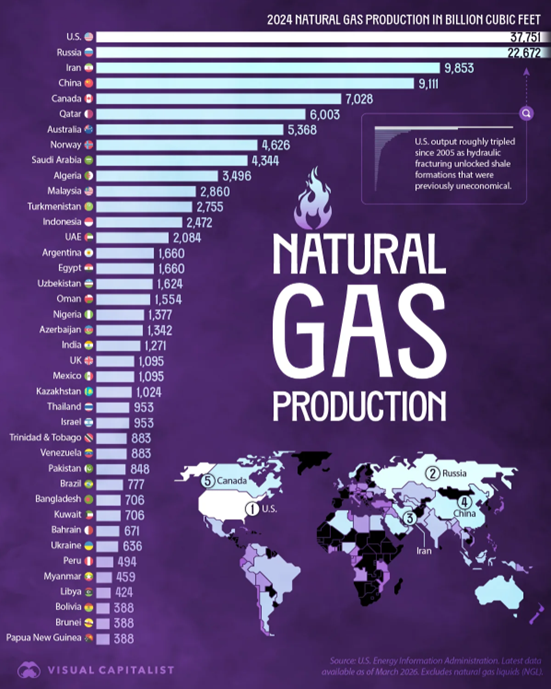

Charts of the Week

Spare Time Updates

At Merton College in Oxford, there is an antique chest. In the Middle Ages, three key-holders had to be summoned to reveal the riches within. But this treasure wasn't gold or jewels. It was books.

9 Myths About the 'Stress Hormone' Cortisol

Cortisol surges in the early hours, nudging your blood pressure up, helping your body tap into its energy reserves, and preparing your immune system for whatever the day will bring.

Feel free to pass on this email to anyone you think would benefit from its information or see some value in it.

Thank you very much for reading through our commentary. Feedback is welcome!

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. â / ™ Trademark(s) of Royal Bank of Canada. Used under license. © RBC Dominion Securities Inc. 2026. All rights reserved. This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. This publication is for information purposes only. Graphs and charts are used for illustrative purposes only and do not reflect future values or changes. Past performance is not indicative of future returns. This commentary is based on information that is believed to be accurate at the time of writing and is subject to change. All opinions and estimates contained in this report constitute RBC Dominion Securities Inc.'s judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. Interest rates, market conditions and other investment factors are subject to change. Past performance may not be repeated. The information provided is intended only to illustrate certain historical returns and is not intended to reflect future values or returns. This publication is not intended as nor does it constitute tax or legal advice. Readers should consult their own lawyer, accountant or other professional advisor when planning to implement a strategy.

RBC Dominion Securities Inc.