Nick Milau

March 19, 2026

Weekly Wrap

Global stock markets faced a challenging and volatile week as geopolitical tensions in the Middle East and a "central bank blitz" dominated investor sentiment. In the United States, the major indices are on track for their fourth consecutive weekly loss. As of writing, the S&P 500 has fallen 2% for the week, while the Nasdaq Composite—sensitive to the rising bond yields that accompanied inflation fears—has slipped 2.4%. The Dow Jones Industrial Average has also trended lower, shedding 2%. These declines were catalyzed by the ongoing conflict involving Iran, which has severely disrupted shipping through the Strait of Hormuz. While a mid-week dip in oil prices toward $93 per barrel provided temporary relief, Middle East escalation has since sent the price of oil soaring prompting a spike in searches for EVs at online car marketplaces according to Business Insider.

In Canada, the S&P/TSX Composite also headed south as gold and material stocks tumbled with gold itself shedding around 9%. Currently the TSX is down over 3.35%. International markets were equally unsettled. Developed overseas markets slid more than 2% over the week. European and Asian markets remained particularly vulnerable to energy supply shocks. European shares had slight corrective bounce this morning before joining the other developed markets finishing lower today and for the week. Like all other markets, the Emerging Markets also declined but slightly more with the double shock of current events and a strengthening US dollar. Driving these global moves was a heavy calendar of central bank decisions; the Federal Reserve, Bank of Canada, and ECB all held rates steady but adopted a "hawkish hold" stance. This signaled that while inflation is slowing, the recent energy spike might delay anticipated rate cuts, keeping global borrowing costs high and equity valuations under pressure. Much of this resulted in a yield surge with the US 10-year treasury yield reaching 4.37% today. In Canada, long-term yields drifted higher with the Canada 10-year benchmark yield climbing back towards 3.5%. US money market assets have surged to record levels, approaching an estimated $8 trillion due to the uncertainty of the conflict and its inflationary pressures. These elevated cash allocations carry reinvestment risk as investors would then require careful timing when rotating back into higher-risk assets as conditions stabilize.

Market Insights

Geopolitical Conflicts and Market Resilience: Historical Lessons for Today

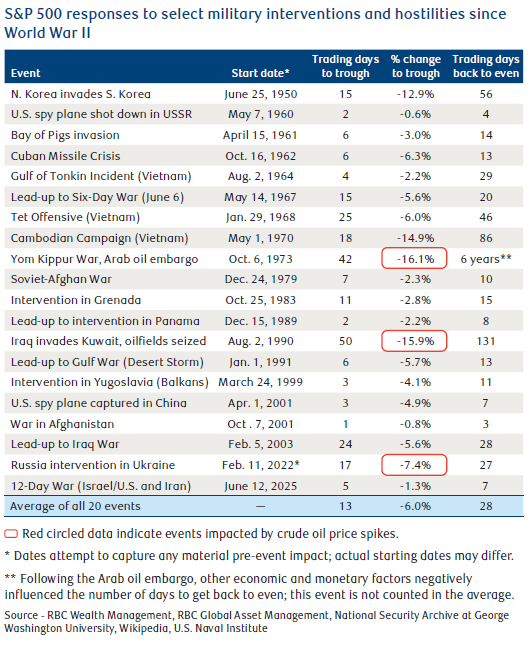

History offers a reassuring perspective on military conflicts and equity markets. RBC's analysis of 20 major post-World War II military interventions reveals that the S&P 500 averaged a six percent decline from initial market impact to the trough, with markets recovering to pre-conflict levels within just 28 days in 19 of the 20 events studied. Importantly, the duration of conflict has historically had little bearing on recovery timelines—suggesting that temporary volatility is par for the course, even as longer-term fundamentals remain intact. The current Middle East situation does warrant attention given the region's role in global energy supplies. With crude oil now above $100 per barrel and costs increasing amid ongoing escalation, this represents a material shift from recent price levels. Such energy price movements could influence economic activity and market sentiment in the near term.

Looking at historical precedent, markets have proven most resilient when geopolitical tensions don't disrupt energy supplies. Russia's 2022 intervention in Ukraine saw the S&P 500 decline 7.4 percent—relatively modest because crude supplies remained stable. Today's U.S. economy is far less energy-dependent than decades past, and leading economic indicators remain solid, pointing to underlying economic strength. While investors should anticipate market volatility, the broader picture suggests economies and markets remain well-positioned to weather near-term uncertainty. Historical evidence supports maintaining a long-term investment perspective through these inevitable market cycles.

Portfolio Update

No portfolio updates this week.

Planning On

CRA and TFSA’s

Tax-Free Savings Account or TFSA’s have been around since 2009. It was much easier to keep track of contribution back then and even for the first number of years, but it has become increasingly difficult with contribution rates increasing. It can be further complicated by withdrawals especially if you make them regularly. Side note: we encourage you to think of these accounts as your ultra long-term money allowing you to take maximum advantage of the tax-sheltered nature of these accounts. A high percentage of our clients are maxed out, making calculation of contribution room easy even after all these years of changing contribution room (remember when the Conservative government increased it to $10,000?), but that is not always the case.

The formula to determine your room is as follows:

1. TFSA contribution room as of January 1st of the previous year minus total contributions made in the previous year.

2. To that number add Unused TFSA contributions at the end of the previous year.

3. Add Total withdrawals made in the previous year.

4. Finally, add the TFSA contribution room on January 1st of the current year.

Seems simple enough providing you have records of everything you have done in all the years that you have had a TFSA. But who keeps records of all of that? Well, CRA is supposed to providing that financial institutions are accurately submitting the information. And that is key to know when accessing CRA’s My Account. It does take a while for the information to be updated. All financial institutions are required to submit the total of contributions and withdrawals made for every Tax-Free Savings Account. They don’t do that, however, until the calendar year turns and then it takes CRA a while to upload all the information for each individual with a Social Insurance Number (and who is eligible to open one). Well, it appears that My Account is now updated. A few of us in the office have had a look and the contribution room indicated for 2026 is accurate, including the activities that took place in 2025. So, if you are looking to max out and have been waiting on CRA, have a look to see if it all reconciles with your information. You can access My Account via your online banking credentials through the link below:

https://www.canada.ca/en/revenue-agency/services/e-services/cra-login-services.html

If we can help you with your strategies to make the best use of these accounts, please let us know.

This information is not intended to provide legal, tax, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified lawyer or accountant, as applicable, before acting on any of the information.

Charts of the Week

Spare Time Updates

The 1 Small Change That Can Reset Your Sleep

Waking up is hard enough. Waking up at the exact same time every day can feel borderline unreasonable. Yet a consistent sleep schedule seven days a week is one of the most powerful ways to improve your sleep quality and, in turn, your overall well-being.

'We’re constantly surprised': The strange deep-sea creatures that eat whales

From bone-eating snot-flowers to snowboarding scale worms, when a whale dies it becomes a colossal island of nutrients – attracting weird and wonderful creatures to feast.