The Clarity of Time

Investing is unique in that the range of potential outcomes narrows the further into the future you look. It’s an important reminder that staying invested with a consistent, repeatable process is far more important than picking any one winning stock or trying to time the market.

Investing is unique in that the range of potential outcomes narrows the further into the future you look. It’s an important reminder that staying invested with a consistent, repeatable process is far more important than picking any one winning stock or trying to time the market.

Ryan Harder

Associate Portfolio Manager & Lead Strategist

May 4, 2026

Life can only be understood backwards, but it must be lived forwards – Soren Kierkegaard

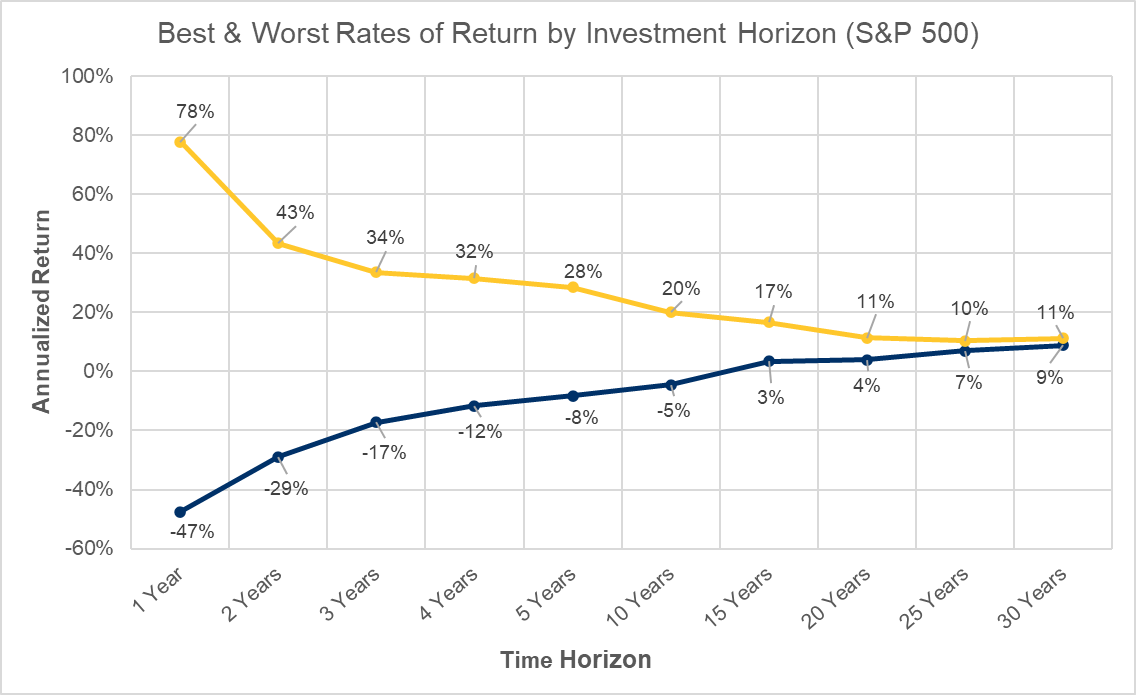

Our perception is often that the longer into the future we look, the more uncertain the final outcome will be. But when looking at the history of investing, I would argue the opposite is true in at least one important way.

To show this I compiled returns for the S&P 500 over the last century, and filtered for the best and worst annualized returns over a variety of different time frames. The result is that the widest dispersion of potential returns occurs over the shortest time frames, and this dispersion narrows dramatically over time. In fact the worst 30-year period in the S&P 500’s history is only 2% worse per year than the best ever 30-year period: rather than diverging, investment returns converge over long time frames. We can see the distant future with more clarity than the near future. This doesn’t mean that investment choices don’t matter (on the contrary), but it does indicate that the time you spend invested is more important than trying to time the market itself.

To be fair, it’s true that a 2% annualized difference would result in a very large dollar difference over multiple decades, and yes the starting point still makes a difference, and no the future won’t necessarily mirror the past. Nonetheless, there are a couple of important takeaways here.

The first is to always focus on the long term for funds that are invested for the long term; the key is to have the market agree with us later, not today. Or as Warren Buffett puts it, the market is a voting machine in the short run and a weighing machine in the long run. The key for portfolio managers is to invest based on the weighing machine and not allow the market’s tendency to oscillate between euphoria and panic to distract from investments with superior long-term value.

Take the price of gold for example: I have a great deal of conviction about where gold is headed over the next decade (higher), but none whatsoever about where it’s headed in the next few hours, days, weeks, or months, even if I think there are strong trends in place today to push the price higher (fiscal deficits, geopolitical conflict, central bank buying, unipolar to multi-polar shift in global power dynamics, etc). There’s a fog that is completely opaque in the near term (outside of inside information or front-running), but much clearer in the long term. This is why even the most legendary investors have no edge whatsoever over short timeframes.

We know that the act of investing means assuming risk in the pursuit of increasing the value of invested capital over time. The risk that your capital declines is how we almost always think of investment risk. But the reverse is true over long time frames—the risk is in not being invested, and instead watching the purchasing power of your capital decline.

In our role as portfolio managers, this exercise is a reminder that a solid investment process is far more important than picking any one specific winning stock. A process that can generate small, incremental, repeatable wins (tax & trading efficiencies, liquidity management, investment strategy that focuses on business fundamentals over hype/momentum) is the only way to reliably generate superior outcomes over long time frames. And while we must always remain nimble and responsive to changing economic realities, we should also remember to step back and focus on the clarity that only time and patience can provide.