Hugh Connor

Senior Portfolio Manager & Wealth Advisor

April 14, 2026

Will 2026 end up being a good year for investors?

The challenge with this quarterly newsletter is that by the time it is finalized and distributed the narrative could have shifted dramatically and the commentary could be out of date! Things are changing daily (sometimes intraday!) However, we always need to look past any current headlines and volatility and maintain an informed longer-term perspective.

After a strong 2025 and equally positive start to 2026 the war in Iran has injected significant uncertainty into the outlook and widened the range of potential outcomes for the economy and financial markets. RBC Global Asset Management still believes the economy will continue to grow and maintains a positive outlook on stock market performance:

Economy:

- The war in Iran and concerns around artificial intelligence (AI) are unlikely to be killer blows: oil prices should drop back in coming months, and the positive AI scenarios outweigh the negative ones.

- Last year’s interest-rate cuts, fiscal support, and AI-related capital expenditures are still providing tailwinds.

- Progress on inflation should resume and energy-linked inflation should unwind once energy begins flowing normally again from the Middle East.

Stock Markets:

- Despite heightened uncertainty, corporate profit estimates in Canada and the U.S. have continued to move higher. Management guidance on business conditions and consumer demand will provide valuable signals on whether the current trajectory in earnings is sustainable and whether it can provide fundamental support for equity markets.

- The positive impulse of 175 basis points (bps) of U.S. Federal Reserve (Fed) rate cuts over the past 17 months will go on providing useful stimulus for some months to come, as will the estimated USD$50 billion of additional tax refunds arriving this spring.

- U.S. GDP growth estimates are now sitting comfortably in the 2 percent and 3 percent range, a pace of economic growth which has typically delivered low double-digit S&P500 returns. The Canadian economy is faced with many of the same challenges as the U.S. and then some including trade and tariff uncertainty. However, interest rates are lower in Canada and our balance sheet is better positioned for long-term fiscal and policy support.

- One item to watch out for is that it is midterm election year in the U.S. In the 23 midterm election years since 1934, markets have experienced noteworthy downturns but robust rebounds typically follow and the market goes on to new highs.

Therefore, we can likely expect continued volatility and potentially an extended market pullback at some point due to the mid-term election. However, recessions seem unlikely and assuming the Iran conflict does not evolve into a longer U.S. military commitment the pull-back is likely part of the roadmap for stock markets to set more highs later this year.

Volatility is so uncomfortable, but it is completely normal

It seems impossible to go even one day without seeing a panic-inducing headline – geopolitical tensions, inflation fears, AI disruption etc. It’s only human nature for fear to take hold in uncertain times. Even the most seasoned investor can find it difficult to maintain investment discipline when emotions run high. As clients you are well aware how The Connor Group has an extremely disciplined and data driven approach to our investment models and portfolio construction. We are by no means dismissing the human element in decision making but we admittedly attempt to minimize it. The same goes with dealing with investor psychology. We are not dismissing feelings and ignoring humanitarian consequences of world events but we are using data to formulate our strategies and responses:

Geopolitical shocks have on average had a surprisingly muted and short-lived impact on markets.

An analysis of 41 major geopolitical shocks since World War II shows that the S&P 500 has a median recovery time of just two weeks following acts of war. The median peak-to-trough decline is a modest -3%. Each situation is different and this Middle East conflict may take longer to resolve but markets tend to bounce back faster than fear suggests.

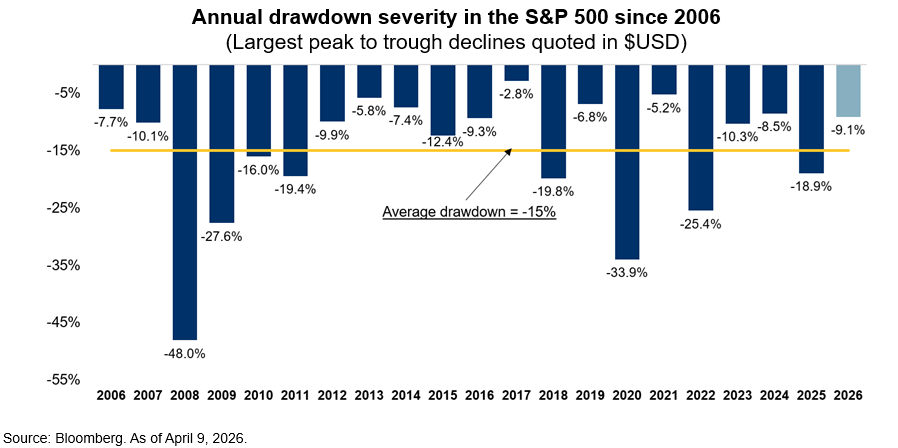

The data shows that most war-related market declines are short-lived.

Market drawdowns or corrections are very normal. The S&P500 declined almost 10% from its peak earlier in the year. Drawdowns like this year happen….every year. Markets don’t move in straight lines. Periods of volatility are common. Even with these drawdowns the markets were positive in 17 of the last 20 years. Historically, strong market rebounds often occur close to periods of weakness. Long-term returns are achieved not by avoiding drawdowns but by being disciplined through them.

The data tells us that drawdowns are normal.

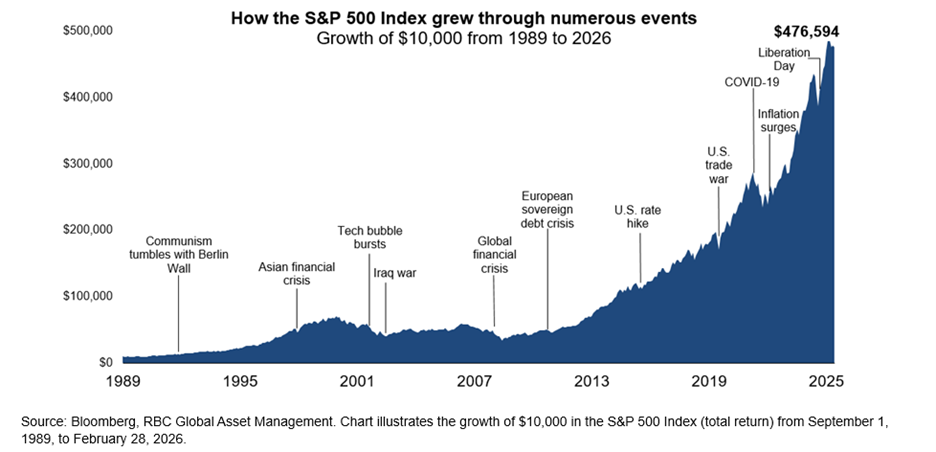

Focusing on the long-term and your plan provides a more rational perspective. There have always been compelling reasons to sit on the sidelines and wait for a better time to invest. The below chart will remind you of many events that undoubtedly were very unsettling at the time.

The data shows how resilient the market is over the long term.

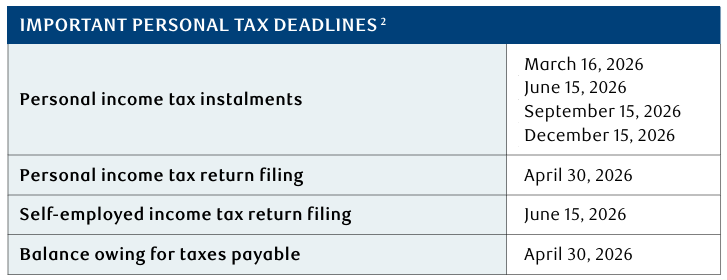

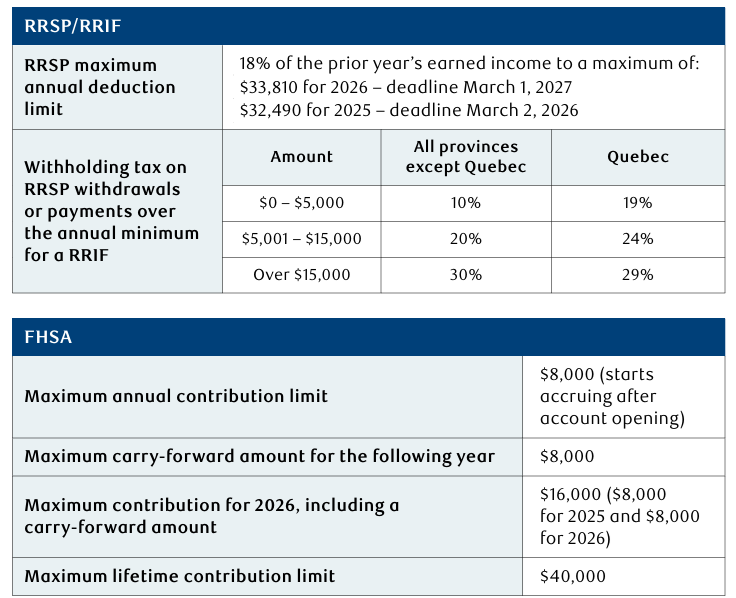

Some Financial Planning Reminders

Your Quarterly Smile 😊

He who has never learned to obey cannot be a good commander – Aristotle

Interesting how an ancient quote can seem so relevant today.

Thank you

Hugh, Ryan and Diane

Securities or investment strategies mentioned in this newsletter may not be suitable for all investors or portfolios. The information contained in this newsletter is not intended as a

recommendation directed to a particular investor or class of investors and is not intended as a recommendation in view of the particular circumstances of a specific investor, class of investors or a specific portfolio. You should not take any action with respect to any securities or investment strategy mentioned in this newsletter without first consulting your own investment advisor in order to ascertain whether the securities or investment strategy mentioned are suitable in your particular circumstances. This information is not a substitute for obtaining professional advice from your Investment Advisor. The commentary, opinions and conclusions, if any, included in this newsletter represent the personal and subjective view of the investment advisor, Hugh Connor, who is not employed as an analyst and do not purport to represent the views of RBC Dominion Securities Inc.

The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or

information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof.

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © RBC Dominion Securities Inc. 2025. All rights reserved.