Global Insight Special Report - Quantum computing and the next technology contest

Quantum computing and the next technology contest: AI has been all the rage, but quantum computing may be tech’s next big thing. While the timing of its commercial viability is uncertain, many governments see it as a cornerstone of long-term economic competitiveness and national security.

Quantum computing and the next technology contest: AI has been all the rage, but quantum computing may be tech’s next big thing. While the timing of its commercial viability is uncertain, many governments see it as a cornerstone of long-term economic competitiveness and national security.

Portfolio Advisory Group

May 22, 2026

Quantum computing and the next technology contest

Frédérique Carrier

Produced: May 18, 2026, 17:07 ET; Disseminated: May 20, 2026, 10:45 ET

All values in U.S. dollars and priced as of market close, May 8, 2026, unless otherwise stated. For important and required non-U.S. analyst disclosures, see page 13.

Investment and insurance products offered through RBC Wealth Management are not insured by the FDIC or any other federal government agency, are not deposits or other obligations of, or guaranteed by, a bank or any bank affiliate, and are subject to investment risks, including possible loss of the principal amount invested.

Special Report

Quantum computing and the next technology contest

AI has been all the rage, but quantum computing may be tech’s next big thing, with the potential to revolutionise diverse fields like science, logistics, finance, and medicine. While the timing of its commercial viability is uncertain, many governments see it as a cornerstone of long-term economic competitiveness and national security. We look at where the technology is today and why investors should pay attention to it.

Key points:

- Quantum computers enable the simultaneous exploration of multiple solutions, unlike AI, which excels at pattern recognition from large datasets.

- The possibility that quantum computing may break global encryption systems protecting the defence and finance industries has motivated governments to treat it as a strategic priority.

- The technology is not yet commercially viable as formidable technical barriers remain, though progress is being made.

- While still at the pre-commercial stage, the technology is shaping research ecosystems and geopolitical alignment, and it will likely present attractive investment opportunities in the decades ahead.

Quantum computing’s potential to undermine the encryption systems that secure global finance, communications, and defence—and the prospect that the technology can usher in breakthroughs in materials science, pharmaceuticals, and logistics—has propelled it into mainstream policy and boardroom discussions.

We review the technology’s fundamentals, contrast it with AI, and assess the remaining technical and commercial challenges before turning to the geopolitical competition shaping its development and considering why quantum computing warrants investor attention.

Quantum computing 101

Quantum computers are machines that use the properties of quantum physics—the laws that govern how particles behave at the atomic and subatomic levels—to store data and perform computations. A comparison to a traditional computer and using an analogy to a light switch can help clarify the concept.

A traditional computer works much like a very fast light switch. Each piece of information is stored as a basic unit of information, or a bit, that is either off (0) or on (1). Even the most powerful supercomputers are essentially performing massive numbers of these on/off calculations every second.

A quantum computer uses quantum bits, or qubits, as the basic building blocks to store and process information. But instead of simple on/off units of information, or just (0) or (1), qubits can exist in a combination of both at the same time, behaving more like a dimmer switch than a light switch. That is, in quantum mechanics, subatomic particles can exist in various states at the same time, a property called “superposition.”

In practice, qubits can be physically realised using various quantum systems such as: superconducting circuits on specialised chips, trapped ions (individual charged atoms trapped in electromagnetic fields), or photons (particles of light), each of which must be carefully controlled.

Thanks to superposition, a quantum computer can explore many possible solutions simultaneously, instead of checking them one by one. This enables the computer to coordinate calculations efficiently in ways traditional computers cannot.

That doesn’t mean that quantum computers are faster at every task. In fact, for everyday uses like spreadsheets they are not more useful. Rather, quantum computers are powerful explorers of possibilities. They are particularly adept at tackling specific problems where the number of possible answers is too large to test one by one, because they can explore many possible solutions simultaneously—for example, in optimising traffic flows or analysing security codes. Solving these types of problems overwhelm today’s computers even in the age of AI.

Potential benefits and risks of quantum technologies

Potential benefits: Quantum technologies may deliver significant productivity gains and competitive advantages across multiple sectors.

- Medicine and health care: Improved medical imaging for early tumour detection; accelerated DNA sequencing and drug discovery.

- Materials science: Enhanced defect detection and quality inspection; development of stronger, lighter materials.

- Energy and extractive industries: Better resource location and early fault identification for equipment; improved carbon-capture and grid operations.

- Chemistry: By simulating molecular reactions, a deeper understanding of molecular interactions can be achieved.

- Finance: Enhanced risk analysis, portfolio optimisation, and transaction settlement. Transportation and logistics: Solutions to routing and scheduling problems.

- Communications: Strengthened data security for critical infrastructure via secured quantum networks.

Potential risks: Quantum technologies pose a number of threats that need to be addressed.

- The undermining of current encryption standards: Quantum computers could compromise encryption methods that protect financial systems and critical infrastructure. In response, post-quantum cryptography standards are being developed.

- Increased surveillance: Quantum sensors could raise privacy concerns as they can bypass physical boundaries such as walls.

- National security: Advances in cryptanalysis and broader weapons and military sensing capabilities could undermine national security, prompting countries to accelerate the race to develop quantum technologies.

Source - RBC Wealth Management; OECD, “An overview of national strategies and policies for quantum technologies” (December 2025)

Quantum technology vs. AI

Today’s AI is very good at solving problems where there is a lot of data and clear patterns. AI can recognise images, understand language, predict trends, and recommend actions because it has learnt from millions of past examples.

Quantum computers, by contrast, are useful for searching through an enormous number of possible combinations, where there may not be a clear pattern to learn, and where testing each possibility one by one would take much too long—even for the fastest supercomputer.

AI and quantum computing can be complementary, rather than competing, tools. In practice, AI might help narrow down promising options, while a quantum computer could explore those options more efficiently.

Unlike modern AI development, which depends heavily on massive investments in specialised chips, cloud infrastructure, and large data centres, quantum technologies today are driven by scientific breakthroughs rather than by scale.

This is because the technology is still at a research-heavy stage. Progress remains constrained by fundamental scientific challenges such as keeping qubits stable, reducing error rates, and controlling and measuring quantum systems with sufficient precision. Currently, a breakthrough in physics or engineering is enough to improve the technology’s prospects. Small, highly specialised teams, academic laboratories, and startups can all be at the forefront of quantum research and development.

Challenges with quantum technology

Quantum computing technology is advancing rapidly, but several fundamental scientific, engineering, and ecosystem challenges remain before it can be deployed reliably.

The physics of it

Quantum systems are extremely fragile and sensitive to the most minute environmental disturbances such as tiny temperature fluctuations, the slightest vibration, and stray radiation. When disturbed, qubits lose their quantum properties.

To reduce this risk, quantum systems must operate in highly controlled environments, often at ultralow temperatures (-269 degrees Celsius or -452 Fahrenheit, levels close to absolute zero, the theoretical lowest possible temperature) and inside heavily shielded systems such as metal boxes and special lab environments. However, even under such conditions, maintaining stable qubits remains one of the key scientific challenges in quantum computing.

Scaling up

Even if scientists can make individual qubits stable, building large, reliable quantum computers introduces a new set of engineering and manufacturing challenges. Quantum calculations require not only many qubits, but also for those qubits to work together and remain stable long enough to complete a calculation. Today, qubits typically stay stable only for very short periods, which means errors can still occur frequently.

As researchers attempt to scale the technology by adding more qubits, the greater the challenge becomes because each additional qubit introduces new potential sources of interference.

To improve reliability, scientists use quantum error correction techniques, which involve combining many physical qubits together into a single logical qubit to detect and correct mistakes during calculations. This is a similar approach to that of the Global Positioning System (GPS), which utilises signals from a network of satellites to determine an accurate location, rather than relying on a single signal. While this improves reliability, it also increases the number of qubits required, making systems much larger and harder to engineer.

In addition, as quantum machines require sophisticated cooling systems, specialised materials, and highly controlled environments, moving from small experimental systems to machines that can be produced reliably at scale and at a reasonable cost is a significant challenge for the industry.

With many of these challenges not entirely resolved, there is no agreed winning architecture for quantum computers, much like the diverse, experimental nuclear reactor designs in the 1950s, or semiconductor materials in the 1960s. Despite recent breakthroughs, it remains unclear which approach will ultimately scale reliably, be it superconducting qubits, trapped ions, photonics, or other emerging technologies.

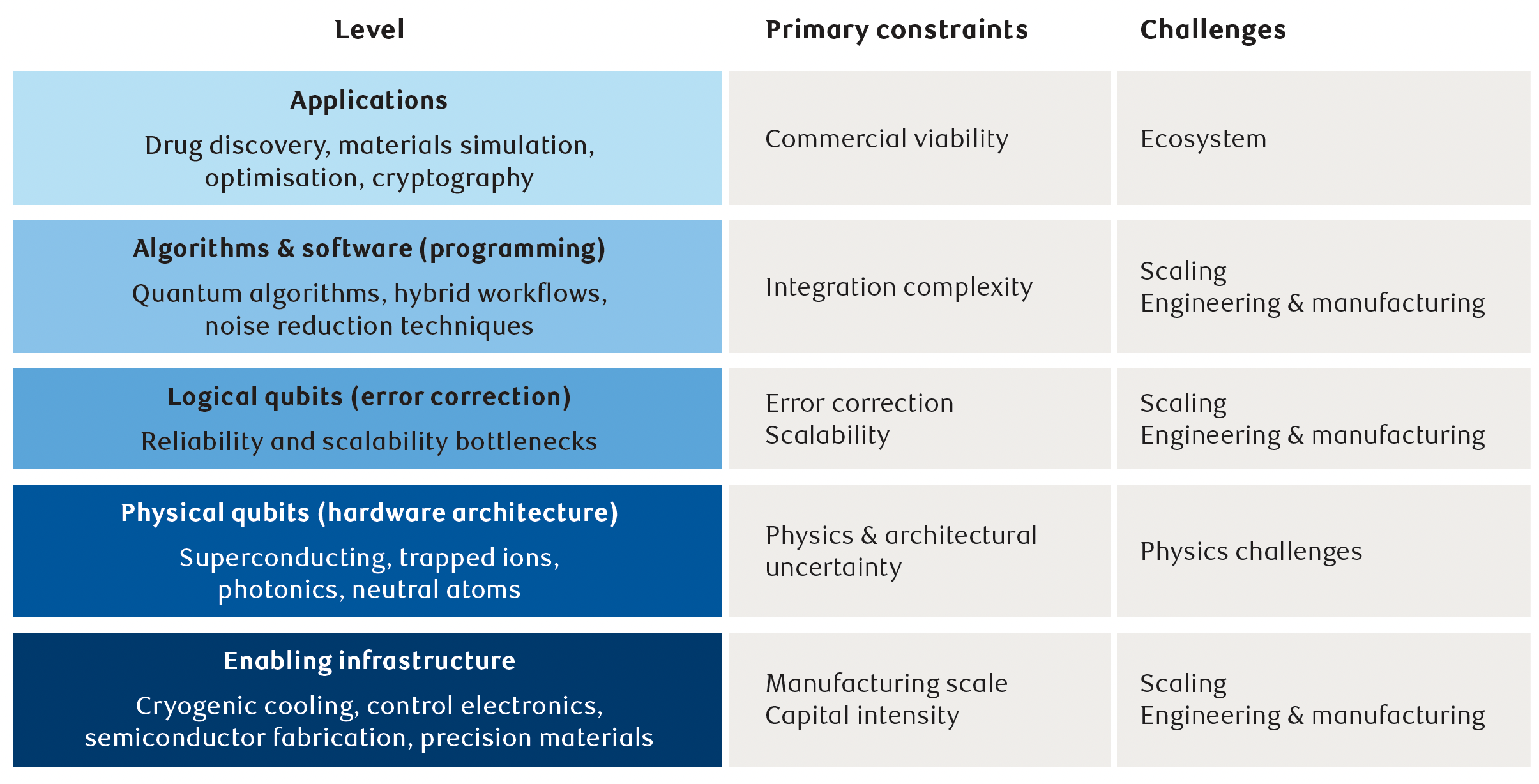

The quantum technology stack: constraints and challenges at every level

Hybrid workflows combine classical and quantum computing, with a classical computer managing most of the process while delegating specific subtasks to the quantum processor and integrating the results. Noise reduction employs software that uses statistical adjustments to reduce the impact of noise.

Source - RBC Wealth Management

Immature ecosystem

The wider quantum computing ecosystem is still developing, with few people globally having the specialised skills needed to design, build, and operate quantum systems. At the same time, the number of proven realworld business applications remains limited, and software development is still catching up with hardware progress. As this uncertainty makes it difficult for private companies to be invested at a large scale, quantum computing is one of the few frontier technologies today where early progress is still strongly shaped by public research funding, even in countries like the U.S. where private sector investment is robust.

Despite these challenges, progress has been measurable. In 2024, Google reported that error rates can decline as logical qubits scale, an important step toward fault-tolerant systems, or systems that can detect and correct errors quickly enough so that they do not corrupt the final output. While these advances remain far from commercial deployment, they suggest that scientists are finding ways to make quantum computers more dependable.

Everyone’s race

Quantum computing has moved from laboratory curiosity to geopolitical priority. A 2025 report by the Organisation for Economic Co-operation and Development (OECD), a group of mostly wealthy nations, points out that the COVID-19 pandemic fundamentally reshaped the context for quantum strategy development due to heightened concerns about technological resilience and supply chain vulnerabilities. The pandemic also led to a worldwide wave of government investment to support economies, some of which was dedicated to quantum science and technology.

Governments increasingly view quantum research as a hedge against future vulnerability, given the technology’s potential to break widely used encryption systems that underpin global finance, communications, and defence infrastructure. They are therefore inclined to support the industry, with the aim of developing post-quantum cryptographic standards, a task which will take time as existing encryption systems are deeply embedded across key economic sectors.

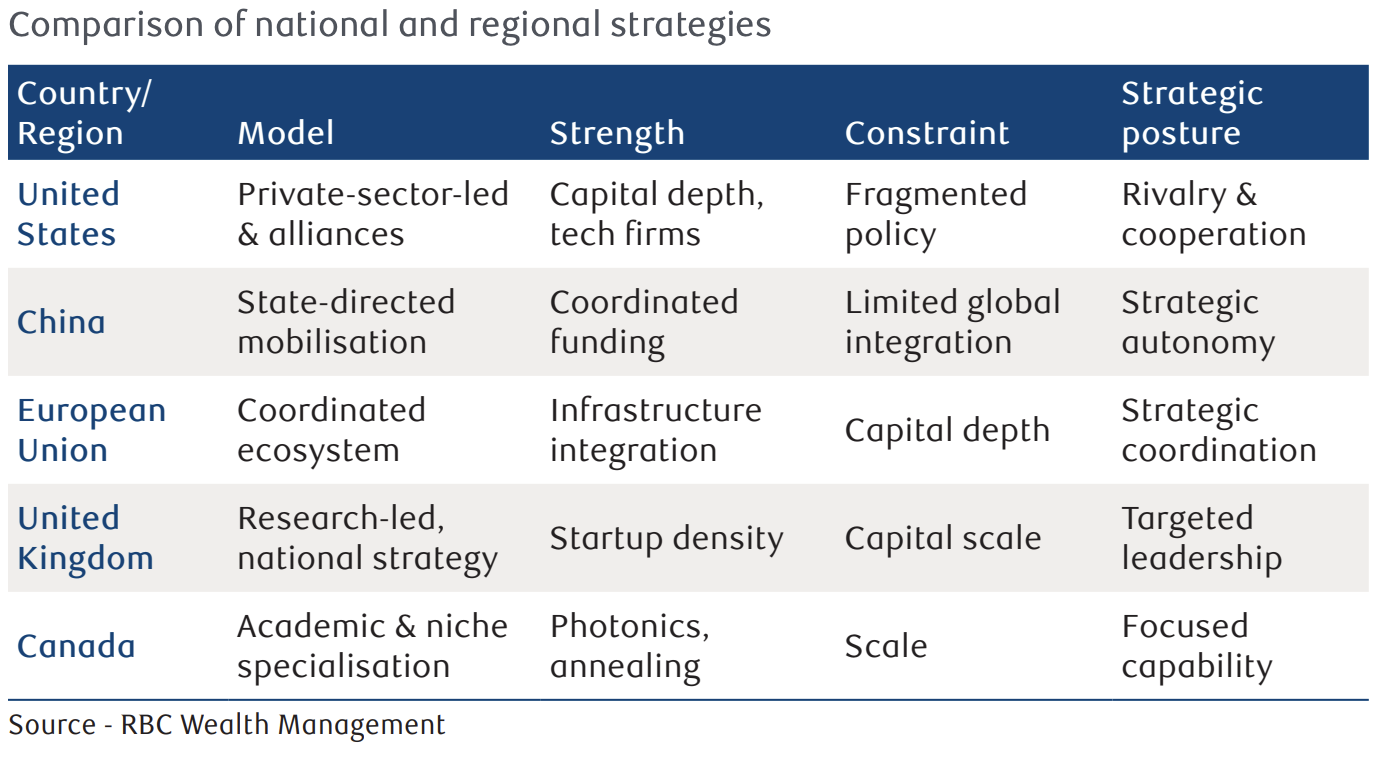

Strategic approaches shaped by institutions, capital, and policy

Yet despite this policy backing, quantum computing remains at a precommercial stage of development, with no country having crossed the threshold into large-scale, fault-tolerant machines.

Researchers at the Harvard Kennedy School, the graduate school of public policy of Harvard University, have attempted to assess which countries lead in quantum technologies, ranking 25 countries according to their Critical and Emerging Technologies Index, with 100 being most developed. The U.S. dominates with a score of 84, followed closely by China at 76 and Europe (the UK, France, Germany, Italy, the Netherlands, and Spain) at 74. The UK on its own lags at 48 and Canada is at 41, ranking fourth and sixth, respectively.

Each region has developed a different strategic approach shaped by their institutional strengths, capital structures, and policy priorities. (These are explored in more detail in the Appendix, which includes some publicly traded companies that are involved.)

Overall, the U.S. has the strongest capital intensity, China the most aggressive strategic state direction, Canada and the UK both enjoy a high level of research density per capita, while Europe is strong in infrastructure coordination.

As is the case with semiconductors, quantum technology is now embedded in broader geopolitical competition and forms part of a broader contest over advanced technologies and supply chains. Both the U.S. and China

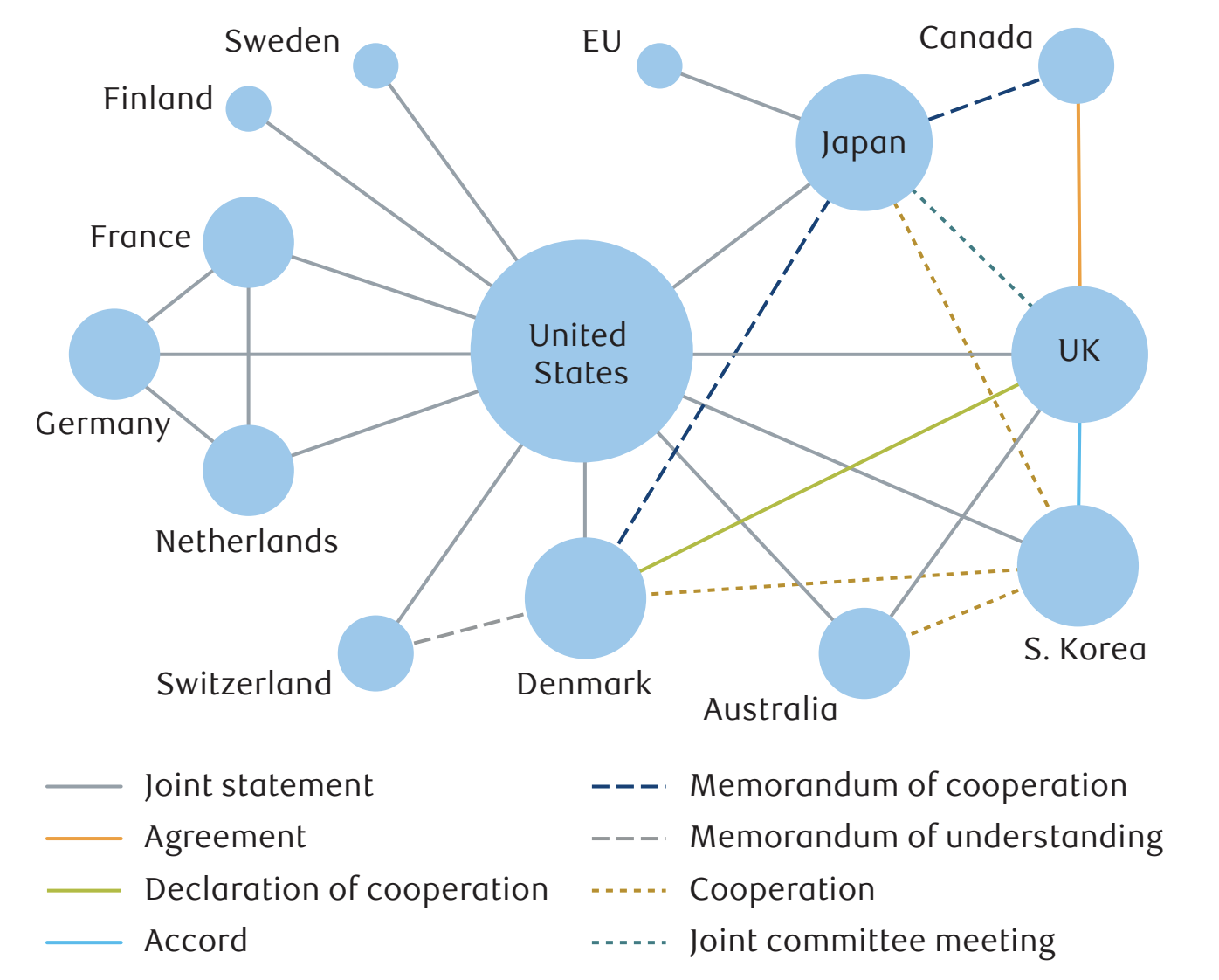

Cooperation among allies

A representation of over 20 bilateral agreements related to quantum science and technology

Each node represents a country and the lines between countries represent bilateral agreements. The size of the node corresponds to the number of bilateral cooperation statements, accords, memoranda, or declarations related to the country.

Source - OECD, “An overview of national strategies and policies for quantum technologies” (December 2025).

now treat quantum technologies as strategic assets, restricting foreign access to critical capabilities. China limits exports of certain high-end materials and technologies, while the U.S. has introduced outbound investment controls covering quantum technologies and imposed export controls on high-performance cooling systems and other quantum components as part of its national security policy.

At the same time, the U.S. approach differs from China’s in one important respect. OECD mapping identifies more than 20 formal bilateral agreements related to quantum science and technology involving the U.S., spanning research collaboration, funding partnerships, talent mobility, and policy coordination. China, by contrast, has tended to pursue more targeted state-led partnerships, particularly in quantum communications, including collaborations with Russia and South Africa.

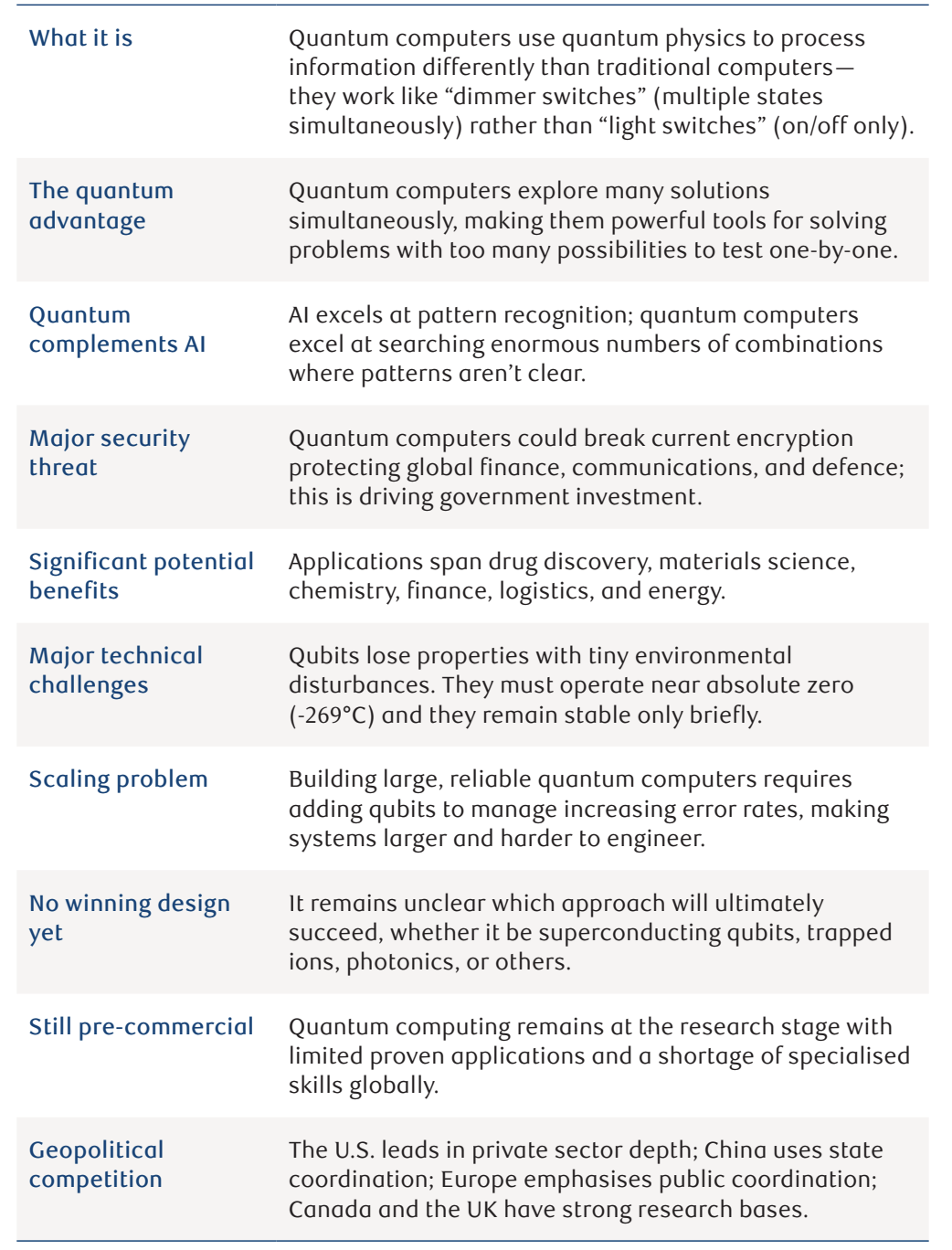

Ten key points about quantum computing

A technology to watch

Quantum computing remains a scientifically validated but commercially immature technology. Yet many governments view quantum technologies as part of long-term sovereign capabilities, embedding them within industrial policy, national security planning, and research strategy.

For investors, the relevance is in understanding how quantum development shapes supply chains, research ecosystems, and geopolitical alignment, rather than focusing on immediate commercial deployment. The technology’s strategic importance is already influencing capital allocation and policy direction.

Quantum computing should therefore be monitored as it will increasingly have long-term implications for advanced manufacturing, materials science, semiconductors, and high-performance computing infrastructure. We expect it will be a rich source of attractive investment opportunities over the next two decades.

Appendix

Regional quantum strategies: A comparative analysis

United States

The U.S. is characterised by the leadership of its large technology firms, such as Google, IBM, Intel, and Microsoft, while startups benefit from venture capital depth. A strong university-to-industry pipeline is a real asset to innovation that emphasises error correction and scalable architecture. The industry benefits from federal support through the National Quantum Initiative, but the ecosystem is driven by private capital.

Overall, the U.S. leads in commercial ecosystem depth and logical qubit progress. Private sector competition fosters innovation.

China

The quantum effort in China is heavily supported by the state to the extent that Alibaba and Baidu, two tech behemoths, have handed their research in the field as well as equipment and facilities over to the government. Both retain a peripheral presence in the space. Quantum research takes place mostly at state-run universities, with startups either controlled or financed by the government, pointing to strategic coordination. China may thus have an advantage in developing a large-scale supply chain for a technology that still has an unclear time horizon and payoff. However, government coordination suggests the authorities will focus on the approach they think will succeed—an approach that can carry the risk of not making the right choice.

The country’s strength is not only in quantum computing but also in quantum communications, where using qubits is ultra secure, attracting interest from the military and intelligence industries.

China treats quantum as strategic infrastructure, not merely commercial technology.

European Union

Europe has taken a coordinated, public sector-led approach to quantum development. It is anchored by the EU’s Quantum Flagship, a largescale research and innovation programme designed to accelerate the development of quantum technologies across Europe, and linked to the European High Performance Computing Joint Undertaking, an initiative to build and coordinate a network of world-class supercomputers across the region.

Europe’s emphasis has been on building shared infrastructure, supporting startups across member states, and linking research excellence with industrial applications. Countries including France, Germany, Finland, and the Netherlands host significant hardware ventures, while EU funding aims to reduce fragmentation.

The EU has committed to supporting quantum technologies through a dedicated European Quantum Act, building on the European Commission’s Quantum Europe Strategy published in July 2025, with adoption expected in 2027.

Europe’s strength lies in ecosystem coordination, but scale and capital remain constraints.

United Kingdom

The UK was early in establishing the National Quantum Technologies Programme in 2014. At the time, it was the first coordinated national initiative in the world to support the technology. This and a strong research base in the field enables the UK to be home to 64 of the world’s 513 companies that focus exclusively on quantum technologies, ranking second globally behind the U.S., which has 148 such firms according to a 2025 report by the Tony Blair Institute for Global Change. Most of these companies are privately held, such as Oxford Quantum Circuits, an Oxford university spinout, or Riverlane, a Cambridge-based quantum error correction software firm. Of the rare publicly listed names, Arqit Quantum is a London-based quantum encryption company listed on Nasdaq, while Quantinuum (majority owned by Honeywell) recently filed for a U.S. IPO.

The UK has leadership in photonics, an approach that uses light to perform quantum computations, as well as in quantum sensing, and is strong in early-stage commercial ecosystem development. Moreover, the report notes that the country has firms across the quantum ecosystem, from error correction systems to algorithms and hardware manufacturing. It highlights vulnerabilities such as too few suppliers of certain types of hardware like lasers and photonics, reliance on foreign providers of ultra-cold refrigerators, and a lack of domestic capacity for quantum chip packaging.

Canada

In contrast to the U.S.’s scale-driven corporate ecosystem and the EU’s coordinated public sector strategy, Canada’s quantum ecosystem is rooted in academic depth and specialised firms. The University of Waterloo is the anchor of Canada’s quantum ecosystem, with the University of Toronto and Simon Fraser University in British Columbia also playing key roles. Moreover, Canada is home to globally recognised quantum firms such as D-Wave Quantum and Xanadu Quantum Technologies, as well as software specialist 1QBit, reflecting both hardware and software expertise.

The country has also developed particular strength in photonics and is widely recognised for punching above its weight in research and specialised niches.

Research resources

This document is produced by the Global Portfolio Advisory Committee within RBC Wealth Management’s Portfolio Advisory Group. The RBC Wealth Management Portfolio Advisory Group provides support related to asset allocation and portfolio construction for the firm’s investment advisors / financial advisors who are engaged in assembling portfolios incorporating individual marketable securities.

The Global Portfolio Advisory Committee leverages the broad market outlook as developed by the RBC Investment Strategy Committee (RISC), providing additional tactical and thematic support utilizing research from the RISC, RBC Capital Markets, and third-party resources.

The RISC consists of senior investment professionals drawn from individual, client-focused business units within RBC, including the Portfolio Advisory Group. The RISC builds a broad global investment outlook and develops specific guidelines that can be used to manage portfolios.

Global Portfolio Advisory Committee members

Jim Allworth – Co-chair Investment Strategist, RBC Dominion Securities Inc.

Kelly Bogdanova – Co-chair Portfolio Analyst, RBC Wealth Management Portfolio Advisory Group U.S., RBC Capital Markets, LLC

Frédérique Carrier – Co-chair Managing Director & Head of Investment Strategy, RBC Europe Limited

Jasmine Duan – Co-chair Senior Investment Strategist, RBC Investment Services (Asia) Limited

Luis Castillo – Head, Fixed Income Strategies, RBC Wealth Management Portfolio Advisory Group, RBC Dominion Securities Inc.

Rufaro Chiriseri, CFA – Director & Head of Fixed Income, British Isles, RBC Europe Limited

Janet Engels – Vice President & Head, Global Investments, RBC Wealth Management, RBC Capital Markets, LLC

Thomas Garretson, CFA – Fixed Income Senior Portfolio Strategist, RBC Wealth Management Portfolio Advisory Group, RBC Capital Markets, LLC

Patrick McAllister, CFA – Manager, Equity Advisory & Portfolio Management, RBC Wealth Management Portfolio Advisory Group, RBC Dominion Securities Inc.

Sean Naughton, CFA – Head, RBC Wealth Management Portfolio Advisory Group U.S., RBC Capital Markets, LLC

Alan Robinson – Senior Portfolio Advisor, RBC Wealth Management Portfolio Advisory Group – U.S. Equities, RBC Capital Markets, LLC

Michael Schuette, CFA – Multi-Asset Portfolio Strategist, RBC Wealth Management Portfolio Advisory Group – U.S., RBC Capital Markets, LLC

David Storm, CFA, CAIA – Chief Investment Officer, British Isles & Asia, RBC Europe Limited

Yuh Harn Tan – Head of Discretionary Portfolio Management & UHNW Solutions, Royal Bank of Canada, Singapore Branch

Joseph Wu, CFA – Portfolio Manager, Multi-Asset Strategy, RBC Dominion Securities Inc.

Required disclosures

Analyst Certification

All of the views expressed in this report accurately reflect the personal views of the responsible analyst(s) about any and all of the subject securities or issuers. No part of the compensation of the responsible analyst(s) named herein is, or will be, directly or indirectly, related to the specific recommendations or views expressed by the responsible analyst(s) in this report.

Important Disclosures

In the U.S., RBC Wealth Management operates as a division of RBC Capital Markets, LLC. In Canada, RBC Wealth Management includes, without limitation, RBC Dominion Securities Inc., which is a foreign affiliate of RBC Capital Markets. This report has been prepared by RBC Capital Markets which is an indirect wholly-owned subsidiary of the Royal Bank of Canada and, as such, is a related issuer of Royal Bank of Canada.

Non-U.S. Analyst Disclosure

One or more research analysts involved in the preparation of this report (i) may not be registered/qualified as research analysts with the NYSE and/or FINRA and (ii) may not be associated persons of the RBC Wealth Management and therefore may not be subject to FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

In the event that this is a compendium report (covers six or more companies), RBC Wealth Management may choose to provide important disclosure information by reference. To access current disclosures, clients should refer to https://www.rbccm.com/GLDisclosure/PublicWeb/DisclosureLookup.aspx?EntityID=2 to view disclosures regarding RBC Wealth Management and its affiliated firms. Such information is also available upon request to RBC Wealth Management Publishing, 250 Nicollet Mall, Suite 1800, Minneapolis, MN 55401-1931.

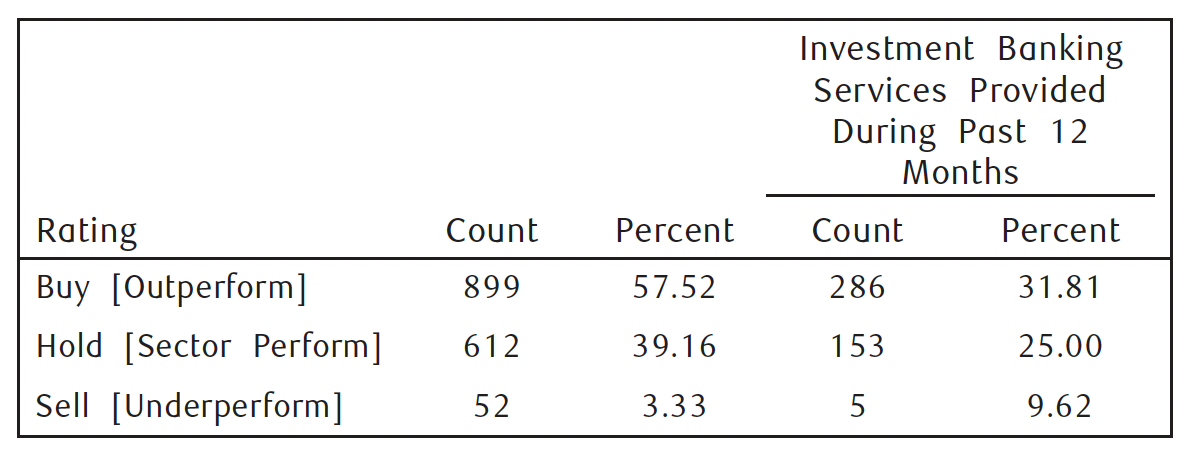

RBC Capital Markets Distribution of Ratings

For the purpose of ratings distributions, regulatory rules require member firms to assign ratings to one of three rating categories – Buy, Hold/Neutral, or Sell – regardless of a firm’s own rating categories. Although RBC Capital Markets’ ratings of Outperform (O), Sector Perform (SP), and Underperform (U) most closely correspond to Buy, Hold/Neutral and Sell, respectively, the meanings are not the same because RBC Capital Markets’ ratings are determined on a relative basis.

Distribution of ratings – RBC Capital Markets Equity Research

As of March 31, 2026

Explanation of RBC Capital Markets Equity Rating System

An analyst’s “sector” is the universe of companies for which the analyst provides research coverage. Accordingly, the rating assigned to a particular stock represents solely the analyst’s view of how that stock will perform over the next 12 months relative to the analyst’s sector average.

Outperform (O): Expected to materially outperform sector average over 12 months. Sector Perform (SP): Returns expected to be in line with sector average over 12 months. Underperform (U): Returns expected to be materially below sector average over 12 months. Restricted (R): RBC policy precludes certain types of communications, including an investment recommendation, when RBC is acting as an advisor in certain merger or other strategic transactions and in certain other circumstances. Not Rated (NR): The rating, price targets and estimates have been removed due to applicable legal, regulatory or policy constraints which may include when RBC Capital Markets is acting in an advisory capacity involving the company.

Risk Rating: The Speculative risk rating reflects a security’s lower level of financial or operating predictability, illiquid share trading volumes, high balance sheet leverage, or limited operating history that result in a higher expectation of financial and/or stock price volatility.

Valuation and Risks to Rating and Price Target

When RBC Capital Markets assigns a value to a company in a research report, FINRA Rules and NYSE Rules (as incorporated into the FINRA Rulebook) require that the basis for the valuation and the impediments to obtaining that valuation be described. Where applicable, this information is included in the text of our research in the sections entitled “Valuation” and “Risks to Rating and Price Target”, respectively.

The analyst(s) responsible for preparing this research report have received (or will receive) compensation that is based upon various factors, including total revenues of RBC Capital Markets, and its affiliates, a portion of which are or have been generated by investment banking activities of RBC Capital Markets and its affiliates.

Other Disclosures

Prepared with the assistance of our national research sources. RBC Wealth Management prepared this report and takes sole responsibility for its content and distribution. The content may have been based, at least in part, on material provided by our third-party correspondent research services. Our third-party correspondent has given RBC Wealth Management general permission to use its research reports as source materials, but has not reviewed or approved this report, nor has it been informed of its publication. Our third-party correspondent may from time to time have long or short positions in, effect transactions in, and make markets in securities referred to herein. Our third-party correspondent may from time to time perform investment banking or other services for, or solicit investment banking or other business from, any company mentioned in this report.

RBC Wealth Management endeavors to make all reasonable efforts to provide research simultaneously to all eligible clients, having regard to local time zones in overseas jurisdictions. In certain investment advisory accounts, RBC Wealth Management or a designated third party will act as overlay manager for our clients and will initiate transactions in the securities referenced herein for those accounts upon receipt of this report. These transactions may occur before or after your receipt of this report and may have a short-term impact on the market price of the securities in which transactions occur. RBC Wealth Management research is posted to our proprietary Web sites to ensure eligible clients receive coverage initiations and changes in rating, targets, and opinions in a timely manner. Additional distribution may be done by sales personnel via e-mail, fax, or regular mail. Clients may also receive our research via third-party vendors. Please contact your RBC Wealth Management Financial Advisor for more information regarding RBC Wealth Management research.

Conflicts Disclosure: RBC Wealth Management is registered with the Securities and Exchange Commission as a broker/dealer and an investment adviser, offering both brokerage and investment advisory services. RBC Wealth Management’s Policy for Managing Conflicts of Interest in Relation to Investment Research is available from us on our website at https://www.rbccm.com/GLDisclosure/PublicWeb/DisclosureLookup.aspx?EntityID=2. Conflicts of interests related to our investment advisory business can be found in Part 2A Appendix 1 of the Firm’s Form ADV or the RBC Advisory Programs Disclosure Document. Copies of any of these documents are available upon request through your Financial Advisor. We reserve the right to amend or supplement this policy, Part 2A Appendix 1 of the Form ADV, or the RBC Advisory Programs Disclosure Document at any time.

The authors are employed by one of the following entities: RBC Wealth Management USA, a division of RBC Capital Markets, LLC, a securities broker-dealer with principal offices located in Minnesota and New York, USA; RBC Dominion Securities Inc., a securities broker-dealer with principal offices located in Toronto, Canada; Royal Bank of Canada, Hong Kong Branch, which is regulated by the Hong Kong Monetary Authority and the Securities and Futures Commission (“SFC”); Royal Bank of Canada, Singapore Branch, a licensed wholesale bank with its principal office located in Singapore; and RBC Europe Limited, a licensed bank with principal offices located in London, United Kingdom.

Third-party Disclaimers

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”) and is licensed for use by RBC. Neither MSCI, S&P, nor any other party involved in making or compiling the GICS or any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability and fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

Disclaimer

The information contained in this report has been compiled by RBC Wealth Management, a division of RBC Capital Markets, LLC, from sources believed to be reliable, but no representation or warranty, express or implied, is made by Royal Bank of Canada, RBC Wealth Management, its affiliates or any other person as to its accuracy, completeness or correctness. All opinions and estimates contained in this report constitute RBC Wealth Management’s judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Every province in Canada, state in the U.S., and most countries throughout the world have their own laws regulating the types of securities and other investment products which may be offered to their residents, as well as the process for doing so. As a result, the securities discussed in this report may not be eligible for sale in some jurisdictions. This report is not, and under no circumstances should be construed as, a solicitation to act as securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on the business of a securities broker or dealer in that jurisdiction. Nothing in this report constitutes legal, accounting or tax advice or individually tailored investment advice. This material is prepared for general circulation to clients, including clients who are affiliates of Royal Bank of Canada, and does not have regard to the particular circumstances or needs of any specific person who may read it. The investments or services contained in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about the suitability of such investments or services. To the full extent permitted by law neither Royal Bank of Canada nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct, indirect or consequential loss arising from, or in connection with, any use of this report or the information contained herein. No matter contained in this document may be reproduced or copied by any means without the prior written consent of Royal Bank of Canada in each instance. In the U.S., RBC Wealth Management operates as a division of RBC Capital Markets, LLC. In Canada, RBC Wealth Management includes, without limitation, RBC Dominion LLC. This report has been prepared by RBC Capital Markets, LLC. Additional information is available upon request.

To U.S. Residents: This publication has been approved by RBC Capital Markets, LLC, Member NYSE/FINRA/SIPC, which is a U.S. registered broker-dealer and which accepts responsibility for this report and its dissemination in the United States. RBC Capital Markets, LLC, is an indirect wholly-owned subsidiary of the Royal Bank of Canada and, as such, is a related issuer of Royal Bank of Canada. Any U.S. recipient of this report that is not a registered broker-dealer or a bank acting in a broker or dealer capacity and that wishes further information regarding, or to effect any transaction in, any of the securities discussed in this report, should contact and place orders with RBC Capital Markets, LLC. International investing involves risks not typically associated with U.S. investing, including currency fluctuation, foreign taxation, political instability and different accounting standards.

To Canadian Residents: This publication has been approved by RBC Dominion Securities Inc. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. * Member Canadian Investor Protection Fund. ® Registered trademark of Royal Bank of Canada. Used under license. RBC Wealth Management is a registered trademark of Royal Bank of Canada. Used under license.

RBC Wealth Management (British Isles): This publication is distributed by RBC Europe Limited and Royal Bank of Canada (Channel Islands) Limited. RBC Europe Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority (FCA registration number: 124543). Registered office: 100 Bishopsgate, London, EC2N 4AA, UK. Royal Bank of Canada (Channel Islands) Limited is regulated by the Jersey Financial Services Commission in the conduct of investment business in Jersey. Registered office: Gaspé House, 66-72 Esplanade, St Helier, Jersey JE2 3QT, Channel Islands.

To persons receiving this from Royal Bank of Canada, Hong Kong Branch: This document is distributed in Hong Kong by Royal Bank of Canada, Hong Kong Branch which is regulated by the Hong Kong Monetary Authority and the SFC. This document is not for distribution in Hong Kong, to investors who are not “professional investors”, as defined in the Securities and Futures Ordinance (Cap. 571 of Hong Kong) and any rules made under that Ordinance. This document has been prepared for general circulation and does not take into account the objectives, financial situation, or needs of any recipient. Past performance is not indicative of future performance. WARNING: The contents of this document have not been reviewed by any regulatory authority in Hong Kong. Investors are advised to exercise caution in relation to the investment. If you are in doubt about any of the contents of this document, you should obtain independent professional advice.

To persons receiving this from Royal Bank of Canada, Singapore Branch: This publication is distributed in Singapore by the Royal Bank of Canada, Singapore Branch, a registered entity licensed by the Monetary Authority of Singapore. This publication is not for distribution in Singapore, to investors who are not “accredited investors” and “institutional investors”, as defined in the Securities and Futures Act 2001 of Singapore. This publication has been prepared for general circulation and does not take into account the objectives, financial situation, or needs of any recipient. You are advised to seek independent advice from a financial adviser before purchasing any product. If you do not obtain independent advice, you should consider whether the product is suitable for you. Past performance is not indicative of future performance. If you have any questions related to this publication, please contact the Royal Bank of Canada, Singapore Branch.

© 2026 RBC Capital Markets, LLC – Member NYSE/FINRA/SIPC © 2026 RBC Dominion Securities Inc. – Member Canadian Investor Protection Fund © 2026 RBC Europe Limited © 2026 Royal Bank of Canada All rights reserved RBC1524