When bonds fail: Rethinking portfolio protection strategies

For decades, Canadian investors relied on long-term bonds to balance risk in portfolios. Since the inflation and interest rate shifts of 2022, that traditional stock-bond relationship has broken down, leaving portfolios vulnerable during market downturns. Interestingly, the Canadian dollar has also decoupled from oil prices, meaning energy rallies no longer provide a built-in lift for the loonie. Instead, the ultimate stabilizer for Canadian portfolios has become the US dollar, which aside from providing diversification into equity themes unavailable on the TSX also tends to ballast volatility during flight to safety events.

For decades, Canadian investors relied on long-term bonds to balance risk in portfolios. Since the inflation and interest rate shifts of 2022, that traditional stock-bond relationship has broken down, leaving portfolios vulnerable during market downturns. Interestingly, the Canadian dollar has also decoupled from oil prices, meaning energy rallies no longer provide a built-in lift for the loonie. Instead, the ultimate stabilizer for Canadian portfolios has become the US dollar, which aside from providing diversification into equity themes unavailable on the TSX also tends to ballast volatility during flight to safety events.

Robin Gullason

Associate Portfolio Manager & Lead Strategist

May 29, 2026

Executive Summary

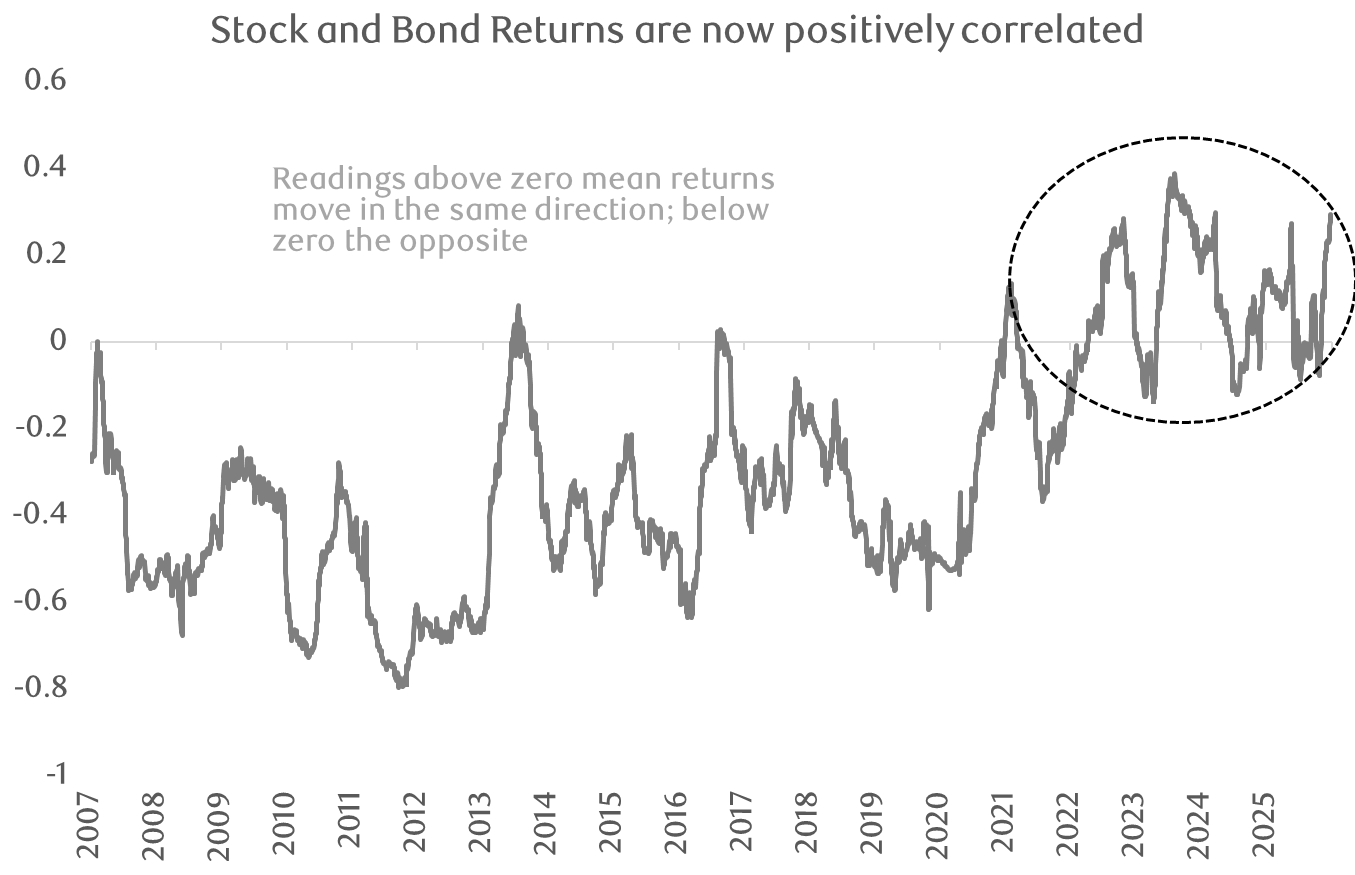

- The historical negative correlation between stocks and bonds has reversed since 2022. We have seen multiple episodes of bond prices falling alongside equities during market corrections, limiting their role as a portfolio hedge.

- The Canadian dollar has structurally decoupled from crude oil prices, reducing the risk of a spike in the loonie (which depresses returns of USD holdings) when oil prices rise, as seen in March of this year.

- During market corrections, the US dollar appreciates versus the Canadian dollar more often than not, and with bonds out of the picture for now, it remains one of the best volatility dampeners available to Canadian investors.

- Despite concerns over the U.S. stepping back from its dominant global role geopolitically, we have yet to see any other currency ready to become the next reserve currency, and recent price action confirms the U.S. dollar’s dominance.

- If we exit the current regime of persistently high inflation and large fiscal deficits, bonds may once again prove to be the effective diversification force they had been. Until then, we are happy to have the U.S. dollar available to serve that role.

For more than a generation, one of the key tenets of portfolio management rested on a comfortable, predictable foundation: the classic balanced portfolio. When economic growth was favourable, equities carried the day and bonds underperformed. When equity markets stumbled or worse, high-quality bonds more often than not acted as the ultimate portfolio ballast, rising in price as interest rates fell and investors sought safety. The negative correlation between stock and bond returns held strong for decades, but appears to have fractured in 2022.

Source: The Harbour Group; Bloomberg

Bonds are not enough to protect portfolios

As central banks aggressively raised interest rates to combat post-COVID inflation, investors witnessed a rare and painful phenomenon as stocks and fixed-income assets declined in tandem. In an instant, the protective shield historically provided by bonds vanished. Even as markets moved through subsequent cycles, the stock-bond correlation has remained stubbornly positive during periods of macroeconomic volatility including surrounding “Liberation Day” in 2025 and once again this year as oil prices have stayed stubbornly high. When inflation risks or fiscal deficits loom large, bonds now compound the volatility in portfolios instead of offset it. This rupture in an age-old relationship means that traditional diversification is no longer functioning when it is needed most and bond maturities are best kept to the shorter-term variety which are less susceptible to volatility and provide liquidity in times of need.

Never say never, but in the meantime we need alternative sources of protection

Longer-term bonds currently are failing to provide their historical buffer, and this can change should budget or inflation dynamics become more benign, but we are not holding our breath. In the meantime, Canadian investors must look elsewhere for true portfolio stabilization, and as Canadians we are in a unique global position. Our local currency happens to be what market participants call a “risk on” currency, meaning that it is typically stronger versus the U.S. dollar when markets are going up, but it tends to go down when markets are challenged. The corollary of this is that in Canadian dollar terms, the U.S. dollar tends to go up when everything else is going down.

Petro Loonie has flown south…

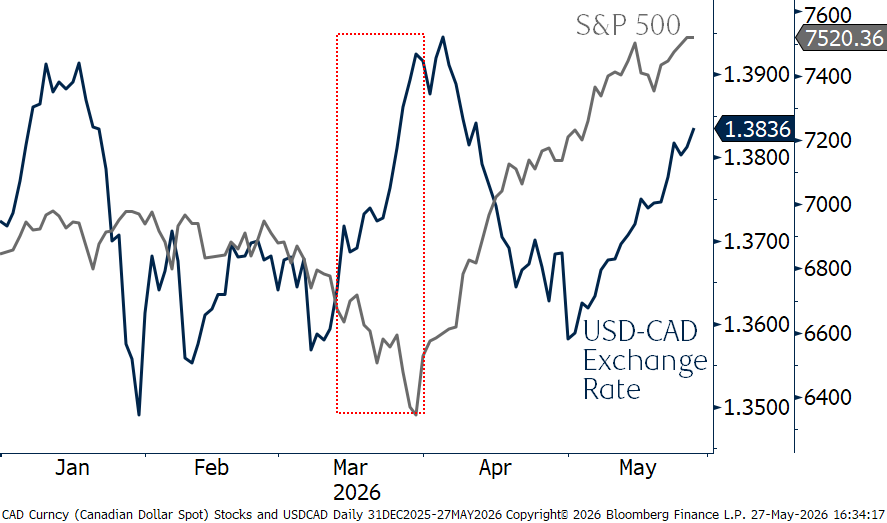

Historically, the Canadian dollar was known as a "petro-currency," tightly bound to the global price of crude oil. When global markets faced geopolitical tension or supply shocks, oil prices would spike, dragging the loonie upward in the process. It seems that relationship has faded in the past decade or so, and frankly it feels like the only time the loonie has a strong correlation with oil prices is when both are going down! Look no further than recent market behavior which saw oil prices rise sharply, yet the Canadian dollar has failed to catch its traditional tailwind. In fact, the U.S. dollar gained 2% versus the Canadian dollar in the month of March, highlighted below. Since then, oil prices have fallen as Mideast tensions have eased somewhat, and the U.S. dollar is gaining steam once again.

… and may not be back for a while

The reason for this decoupling is structural, not temporary. Over the past decade, foreign capital investment in the Canadian oil sands has declined. Without massive inflows of foreign capital entering the country to fund massive energy infrastructure projects, the direct pipeline between rising oil prices and a strengthening Canadian dollar has broken down. The loonie is now far more sensitive to global risk-off sentiment and interest rate differentials than it is to a barrel of Western Canadian Select. When global markets panic, foreign capital leaves Canada, causing the Canadian dollar to drop regardless of what is happening at the oil pumps.

The ultimate “flight” to safety

As we navigate an era characterized by shifting correlations and structural macro volatility, the old rules of portfolio construction are evolving. With bonds turning unreliable and other historically favoured volatility dampeners such as gold posting a mixed track record, it is comforting that we have access to the world’s reserve currency and the benefits exposure provides. While we primarily have U.S. exposure as a result of investing in the global champions available in their market but not ours, the “hedging” properties of the U.S. dollar have been incredibly beneficial to portfolios over the last decade-plus. As we have seen with bonds, there is no guarantee that these relationships will last forever, but for the time being we have a powerful risk management tool available to us and it is incumbent on us to monitor its effectiveness and seek out alternatives should the regime shift.

The Harbour Group - 416-842-2300

Putting you first, every time, to help you navigate the complexities of managing your wealth. All of our team members, all of our resources, all of our collective insight: ALL FOR ONE: YOU™.

The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc. and its affiliates may have an investment banking or other relationship with some or all of the issuers mentioned herein and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. RBC Dominion Securities Inc. and its affiliates also may issue options on securities mentioned herein and may trade in options issued by others. Accordingly, RBC Dominion Securities Inc. or its affiliates may at any time have a long or short position in any such security or option thereon. Mutual funds are sold by RBC Dominion Securities Inc. There may be commissions, trailing commissions, management fees and expenses associated with mutual fund investments. Read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member CIPF. ®Registered Trademark of Royal Bank of Canada. Used under licence. RBC Dominion Securities is a registered trademark of Royal Bank of Canada. Used under licence. ©Copyright 2019. All rights reserved.