October 2024 Market Commentary

After posting five consecutive months of gains, the S&P 500 slightly pulled back in October. The resource-rich Canadian S&P TSX returned +0.9%, outpacing its American counterparts. A return attribution of major equity indices shows the S&P TSX energy sector returned +4.8% during the month, which was the catalyst in overall relative outperformance.

After posting five consecutive months of gains, the S&P 500 slightly pulled back in October. The resource-rich Canadian S&P TSX returned +0.9%, outpacing its American counterparts. A return attribution of major equity indices shows the S&P TSX energy sector returned +4.8% during the month, which was the catalyst in overall relative outperformance.

Troy Private Wealth Partners

October 30, 2024

After posting five consecutive months of gains, the S&P 500 slightly pulled back in October. The resource-rich Canadian S&P TSX returned +0.9%, outpacing its American counterparts. A return attribution of major equity indices shows the S&P TSX energy sector returned +4.8% during the month, which was the catalyst in overall relative outperformance.

Index | October | 3-Month Trailing | YTD Return |

|---|---|---|---|

S&P TSX | 0.9% | 5.3% | 18.2% |

S&P 500 | -0.9% | 3.7% | 21.0% |

Nasdaq | -0.5% | 2.8% | 20.5% |

WTI Oil | 1.2% | -12.3% | -3.2% |

Natural Gas | -7.4% | 33.0% | 7.7% |

10-Year US Treasury Bond | -3.7% | -1.1% | 0.1% |

USD/CAD FX | 3.0% | 0.9% | 5.2% |

Source: FactSet

Former President Donald Trump won both the electoral college and popular vote to win his second non-consecutive term in the White House. This feat has only happened once before in American history when Grover Cleveland won a non-consecutive term in 1893. With the U.S. Presidential election finally behind us, are there broader-ranging implications on your portfolio? The answer is most certainly, yes.

Not only did Trump win the White House, he did so resoundingly. He won each of the seven battleground states (Pennsylvania, Michigan, North Carolina, Georgia, Wisconsin, Arizona, and Nevada), the Senate flipped to Republican control, and the House of Representatives remained Republican. With Trump in power, a Republican majority is a significant development - A fair chunk of his policies could ultimately pass congress.

When Republicans have controlled all branches of government the S&P 500 has returned +13% on average (since 1932). History does not always repeat itself, but investors should find solace in knowing we have been here before. The last time the Republicans held the majority in both chambers of the U.S. Congress was from 2017 to 2019 (the first two years of President Trump’s first term). From inauguration on January 20, 2017 to January 20, 2019, the S&P 500 posted a net gain of roughly +9% annualized. The index returned +21.8% in 2017 (coined the “Trump Bump”) but fell -4.4% in 2018 primarily due to a sharp fourth quarter sell-off over concerns about rising interest rates and trade tensions.

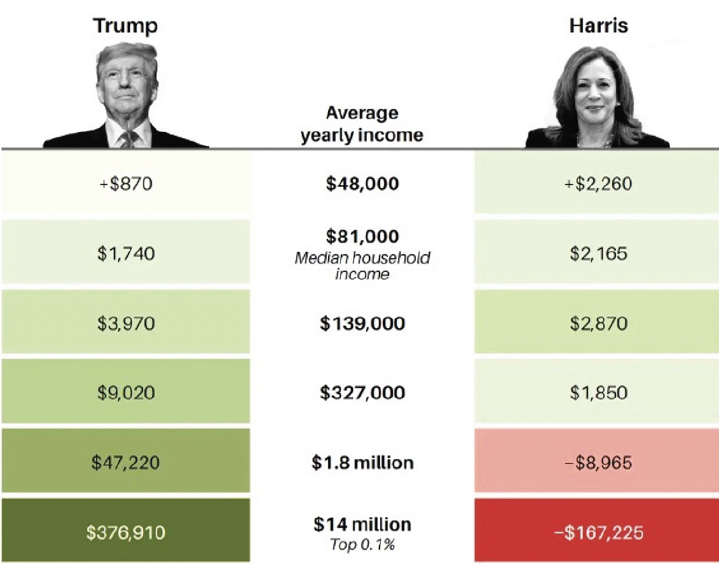

Chart 1: Individual tax policy gain or loss at key income levels

Source: Wharton Business School, U.S. Census Data

With an increased likelihood of Trump successfully passing a fair amount of his agenda through congress, let’s examine the potential impact on your portfolio. RBC Capital Markets published a recent study on the potential policy changes we could see under a Trump 2.0 administration (Chart 2). Even though Trump has a goal of keeping inflation low, we view most of his core policies as inflationary. Maintaining or cutting corporate and individual taxes, increasing tariffs on foreign goods, increasing the budget deficit, and deporting illegal immigrants is highly inflationary (Chart 1,2). U.S. 10-Year bond yields act as a bit of a barometer in terms of future economic prosperity. Broadly speaking, if long-term yields are rising the bond market is telling us there is rising confidence in the economy which likely leads to higher inflation. In mid-September the U.S. 10-Year was ~ 3.65% but as the odds of a Trump victory kept climbing, so did yields. There has been a substantial move in short order since then, with the U.S. 10-Year climbing 78 bps (sitting at ~ 4.43%).

Despite Trump stating there will be low or even no inflation, the actions we have seen in the bond market suggest otherwise.

Chart 2: President Trump’s policy goals are ambitious, and unrealistic

Topic | Goals |

General |

|

Corporate & Individual Taxes |

|

Safety Nets |

|

Education |

|

Energy & Climate |

|

Health Care |

|

Technology |

|

Housing |

|

Regulation |

|

Trade |

|

Immigration |

|

Source: RBC Capital Markets

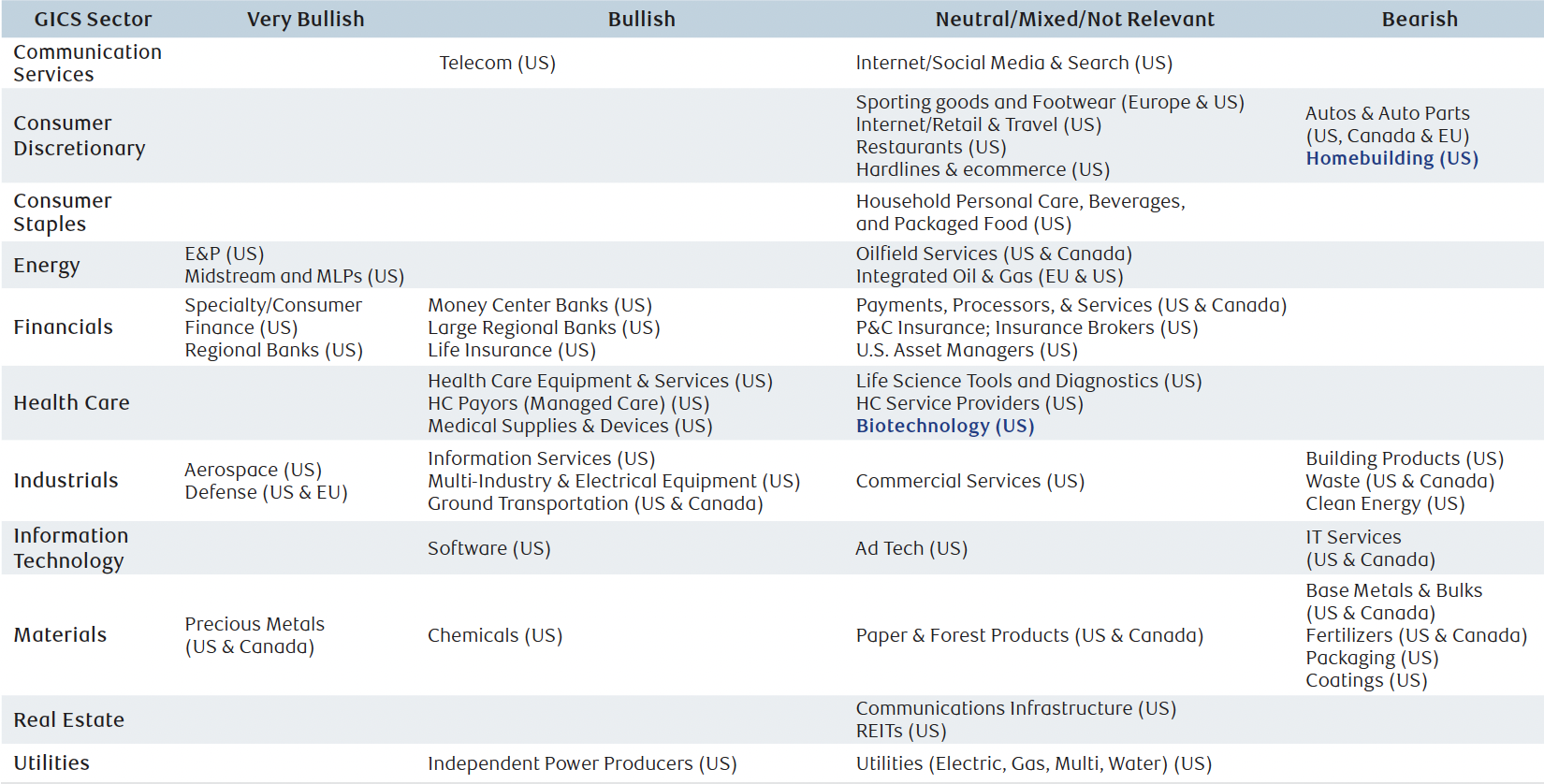

Sentiment amongst internal equity research analysts was positive, with many sharing they would revise their earnings estimates higher due to policy tailwinds from deregulation and taxes. Further, they also believe that non-U.S. equity investors will want to stay overweight U.S. if Trump did win, due to his trade and foreign policy. This is especially true when it comes to European money managers given Trump’s approach to NATO and the risks that is poses to Europe. Why might markets not do well in this Republican sweep scenario? With U.S. equities not too far below their all-time highs, it’s possible this outcome was already baked into the market. Additionally, long-only investors have relayed a bit of concern over Trump’s tariff views and protectionist stance. Lastly, our analysts do see climbing long-term bond yields as a headwind to equities. Why is this the case? When bond yields rise, investors may shift capital from stocks to bonds. The opportunity cost of holding equities increases as the yields from bonds rise, making bonds a more appealing alternative. Also, the value of stocks is heavily influenced by the future value of cash flows. The value of a dollar today is worth more than a dollar tomorrow and if interest rates are increasing, the present value of those future cash flows are worth less. Lastly, we would see higher borrowing costs for individuals and companies, which would tamper growth. Higher borrowing costs can narrow profit margins and reduce investment in growth and expansion. In terms of sectors, our analysts in a Republican sweep scenario are very bullish on the Financials, Energy, Precious Metals and Industrials sectors (Chart 3). Areas where the group was less positive on included Healthcare (due to RFK Jr’s involvement), clean energy, and homebuilding (rate sensitive) to name a few.

From a positioning standpoint, we are doing research around the opportunity that is growing in small-cap stocks. Small-cap stocks are publicly traded companies with a relatively small market capitalization. Typically, smaller-cap companies have a market cap of around $2 billion, which is much smaller in size than companies such as Brookfield Corporation ($121 billion in size). Small-cap positioning surged in 2016, 2017, and 2018 on economic optimism around Trump’s victory. The tax cuts and deregulation benefitted the group more than the large-caps and we saw major institutional flows into the Russell 2000 (widely regarded as the small-cap index). Additionally, if the federal reserve continues to cut rates, small-cap stocks that are often more sensitive to borrowing costs could benefit disproportionately. The growth potential in this segment of the market is certainly compelling in the current environment, and perhaps investors will return to that playbook in the near to medium-term.

Chart 3: Potential Republican sweep sector implications

Source: RBC Capital Markets

Company Highlight

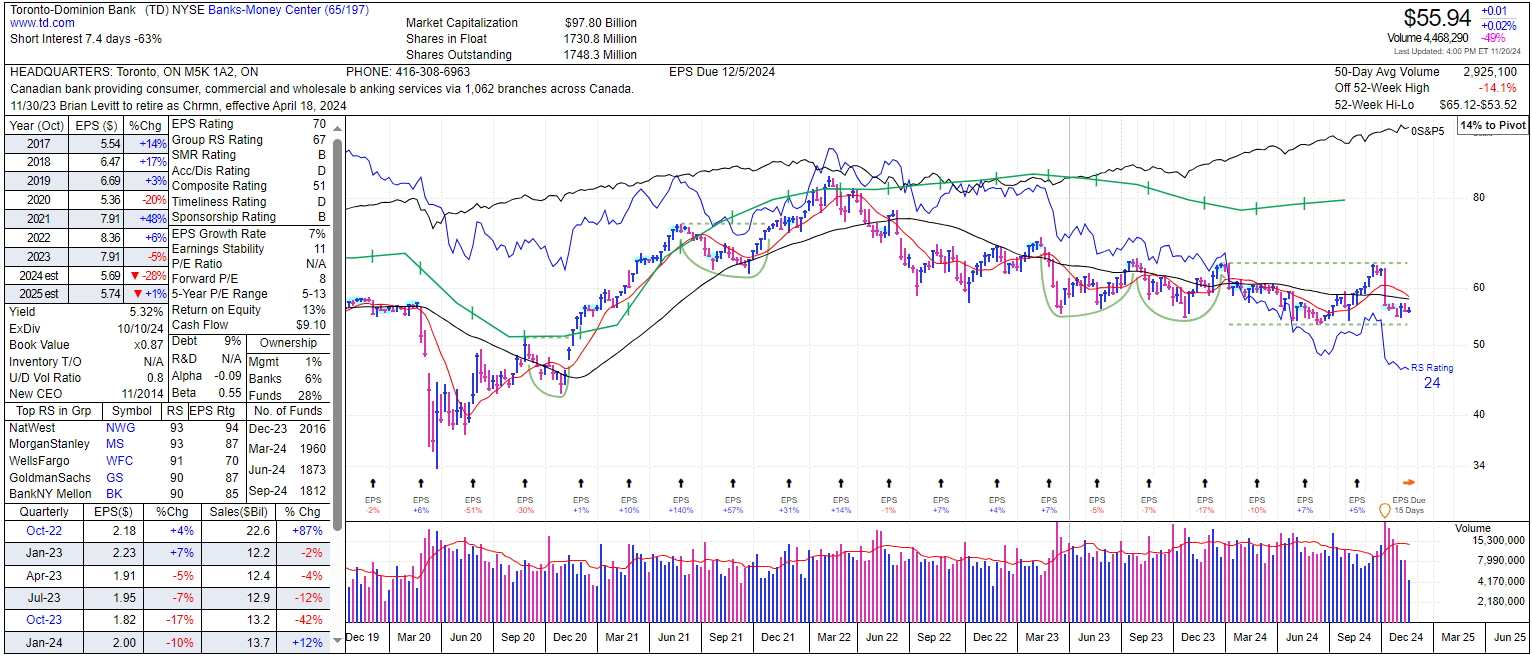

At the end of October, we added more TD Bank (TD-T) exposure to our client portfolios. TD is the second largest Canadian bank by market cap and engages in personal and commercial banking, wealth management, insurance, and capital markets. For those unfamiliar, TD has been under scrutiny with U.S. regulators due to significant failures in its anti-money laundering (AML) program. These deficiencies allowed criminal organizations to launder substantial sums of money through the bank over several years and this scandal has been an overhang on the stock for quite some time now. On September 19, TD announced that President and CEO Bharat Masrani would step down and retire, naming Raymond Chun as his successor effective November 1, 2024. Then on October 10, TD announced that it reached a resolution related to issues surrounding its U.S. Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) compliance programs with the OCC, U.S. Federal Reserve Board, FinCEN, and U.S. Department of Justice. This resolution entails a fine of USD $3.09 billion, an indefinite asset cap (loan growth restriction) on TD’s two U.S. banking subsidiaries, and a complete remediation of its AML program.

With so much bad news baked into the stock over the last few months, we see TD as having the ability to potentially reset and re-rate over the medium to longer-term. The AML deficiencies will be addressed, a change in leadership was needed, and we were able to add more shares at a ~ 5.5% dividend yield, which we view as highly attractive.

Chart 4: Plenty of bad news has been baked into TD (U.S. listed chart)

As we reflect on the past year and begin to look ahead to the next, we remain focused on navigating the ever-evolving financial landscape. Your long-term goals are always at the heart of what we do, and we are here to provide guidance and support every step of the way. We thank you for your continued trust, and don’t hesitate to reach out anytime as questions arise.