Mike's Musings - June 5, 2026

Seemingly underwhelming Canadian economic data has attracted attention recently, but I think there are key nuances beneath the headlines. Below, I discuss the state of the Canadian economy and equity market in more detail below, alongside the ever-evolving geopolitical backdrop.

Seemingly underwhelming Canadian economic data has attracted attention recently, but I think there are key nuances beneath the headlines. Below, I discuss the state of the Canadian economy and equity market in more detail below, alongside the ever-evolving geopolitical backdrop.

Michael Wilkie

June 5, 2026

A Word from Mike

Hello,

Seemingly underwhelming Canadian economic data has attracted attention recently, but I think there are key nuances beneath the headlines. Below, I discuss the state of the Canadian economy and equity market in more detail below, alongside the ever-evolving geopolitical backdrop.

Geopolitics: Awaiting Confirmation

U.S. President Trump’s repeated assertions that a deal with Iran to reopen the Strait of Hormuz is “largely negotiated” have yet to produce a signed agreement. Prior to the conflict, the Strait facilitated roughly one-fifth of global oil shipments, and its continued closure has kept energy prices elevated. While the world economy has thus far demonstrated resilience, sustained commodity supply disruptions remain a significant risk to growth and inflation.

Against this backdrop, equity markets have recovered from their March correction and advanced further on the back of healthy corporate earnings and optimism of an eventual U.S.-Iran deal. Fixed income markets, however, have been more cautious. Bond yields remain well above where they started the year as markets consider the possibility that the energy shock could keep inflation pressures firmer for longer.

I am encouraged by the durability of the economy and corporate profitability but also recognize that recent gains in risk assets appear to reflect a high level of confidence regarding the timing of a U.S.-Iran deal. A finalized agreement that restores transit through the Strait may be needed to extend upward momentum. More importantly, it should help lower energy prices, ease inflation worries and create scope for bond yields to move lower.

Canadian Economy: Better Than the Headline

Canada’s latest GDP report generated headlines after economic output slipped 0.1% annualized in the first quarter, well below expectations and marking a second consecutive quarterly decline. While this met the common definition of a “technical recession,” I believe the underlying details were not as weak as implied by the headline figure.

Much of the downside surprise reflected a pullback in government defense spending after strong outlays in 2025. Business investment remained soft, but investment in equipment and intellectual property posted gains. Household spending continued to grow, suggesting resilient consumer demand. Demographic trends also make the data harder to interpret. Canada’s population fell for a second consecutive quarter as immigration slowed, meaning total economic output can understate underlying performance. In fact, real GDP per person rose 0.9% annualized during the quarter.

Overall, the report points to a sluggish and uneven economy, but not one experiencing a significant broad-based slowdown. Recent business surveys similarly indicate activity is expanding modestly, even as companies continue to navigate uncertainty and rising costs.

Trade policy remains the key near-term risk. My expectation is that the trade terms in the CUSMA treaty will remain broadly intact, but the review process is likely to bring unsettling headlines. The recently proposed 10% U.S. tariff illustrates how even limited measures can create complexity and weigh on business sentiment, even if CUSMA-compliant goods are likely to be exempt.

Banks Lead Canadian Earnings

Canada’s big banks kicked off Q2 earnings season with results that generally exceeded expectations. Strong equity markets, improving dealmaking and elevated trading activity helped drive healthy revenue and profit growth and offset softness in consumer lending.

Despite favourable earnings reports, share price reactions were mixed. Part of the explanation may lie in current valuations. Following a period of strong performance, Canadian banks’ valuations sit meaningfully above long-term averages, leaving less room for positive surprises to be rewarded.

Takeaways

Global risk assets continue to show resilience in the face of challenging crosscurrents. The Middle East conflict remains unresolved, while trade uncertainty continues to cloud the outlook for many Canadian businesses.

Reassuringly, corporate earnings are providing important fundamental support for equity markets, a reminder that macroeconomic trends and markets can diverge at times.

Uncertainty can be unsettling, but the central discipline of diversifying portfolios across sectors and asset classes remains a useful approach to withstand a wide range of market outcomes.

Highlights

China’s economy in a time of uncertainties

The country has seen a new driver of exports this year, and it has not yet been affected by the Middle East conflict to the extent of many other countries. This article assesses China's current economic performance and the equity market outlook for the remainder of 2026.

Regional developments: Canada per-capita GDP improves despite headline weakness; U.S. labour market remains stable despite surge in job openings; The UK and EU face new tariffs with the U.S. over forced labour enforcement, as the EU also navigates deteriorating relations with China; Bank of Japan could hike rates this month

Please take some time to review the Global Insight Weekly.

Large-scale data centres will feature in Canada’s new AI strategy

The federal government strategy identified health and life sciences, energy and natural resources, transportation, agriculture, and manufacturing and robotics, and intends to spend $2.3 billion for training, adoption and startups. Canadian data will be considered a "strategic national asset" for use by AI innovators, with guardrails around Canadian privacy and safeguarding democracy. The government will also pursue deals with the private sector for as much as 830 megawatts of computing capacity by 2030, scaling up to 2.3 gigawatts eventually.

Canadian energy exports to non-U.S. markets ramped up

Natural gas production rose 5.6% in March, led by British Columbia’s 13.8% increase, according to Statistics Canada, as the Middle East conflict compelled many energy importers to tap Canadian fossil fuels. Canadian oil exports also rose 4.2% year-on-year, with shipments to non-U.S. markets (up 25.4%) growing faster than to the U.S. (5.9%). Still, America remains the biggest market for Canadian natural gas and crude oil. Production and exports of finished petroleum products set records for March.

Canada Advances Trade Proposals Ahead of USMCA Review

Canada has submitted new, more detailed trade proposals to the U.S. after recent negotiating progress. The substance of the proposals has yet to be shared. Canada is focused on easing U.S. sectoral tariffs affecting autos, steel, aluminum and softwood lumber, while also preparing for possible new U.S. measures tied to trade investigations. Mark Carney confirmed that Washington is pushing for a 50% U.S.-content threshold for vehicles, a standard he said most Canadian autos already meet, on average. In a recent statement, the Office of the U.S. Trade Representative proposed a tariff of at least 10% on imports from 60 trading partners, including Canada, after a Section 301 investigation into whether countries adequately block goods tied to forced labour. The measures are not finalized and will undergo review and public feedback over the next month or so. For Canada, the broader issue remains the upcoming USMCA renegotiation, since the agreement still allows most goods to flow tariff-free. However, if implemented, these new duties could still add costs and uncertainty for certain Canadian exporters already facing strain under current levies.

U.S. inflation hit a three-year high

Inflation jumped to 3.8% in April, from 3.5% in March, to levels last seen in May 2023, the Commerce Department reported. Gas prices have jumped 50% since the Middle East conflict began, but the U.S. government has dismissed the spike as “transitory.” Excluding food and energy, core inflation rose to 3.3% in April from 3.2% the previous month. The economy also grew at a modest 1.6% pace in the first quarter, with a slowdown in growth of consumer spending offset by higher business investment.

U.S. oil stockpile has dwindled as the Middle East conflict drags on

Petroleum inventories fell for a 10th straight week to levels last seen in 2004, according to the government data. The global oil market was in a state of glut before the Strait of Hormuz was blocked, but now global and U.S. stockpiles are below seasonal norms, according to Vitol Group, the world’s largest energy trader. With hurricane season approaching on the Gulf Coast—a key refinery hub—analysts believe a major storm could ripple across global energy market.

The OECD lowered its global GDP growth forecast

The organization now expects global economic growth to ease to 2.8% in 2026 compared to 3.4% before, assuming the Strait of Hormuz crisis is a “time-limited disruption.” A prolonged disruption could see growth slow to 2.1% this year and sink to 1.8% in 2027. Average G20 economic growth is projected at 3% in 2026, with Canada at around 1.2%. Energy stockpiles are helping countries manage the crisis, but developing countries are especially exposed, said Stefano Scarpetta, the OECD’s chief economist.

Japan’s population decreased by three million in five years

New census data revealed that the country of 123 million people is the same size today as it was in 1989—with the population projected to fall to 87 million by 2070. An aging population and low birth rate—there are two deaths for every birth in Japan—are constricting GDP growth, causing labour shortages, and putting pressure on the health care system. The demographic challenge is one that many developed countries will face in the years ahead.

Charts of the day

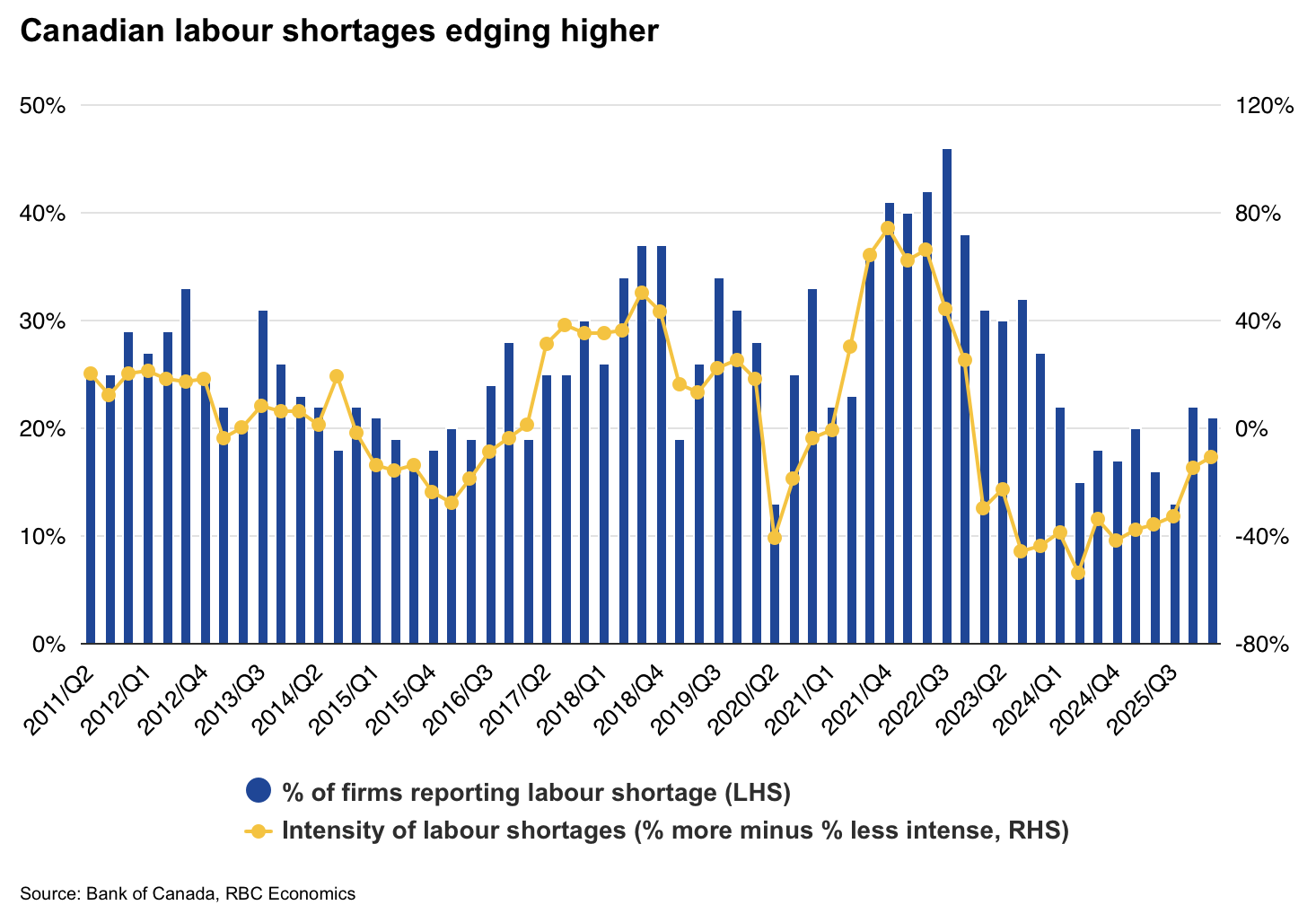

Canada's looming labour squeeze: The impact of retirements and immigration policy

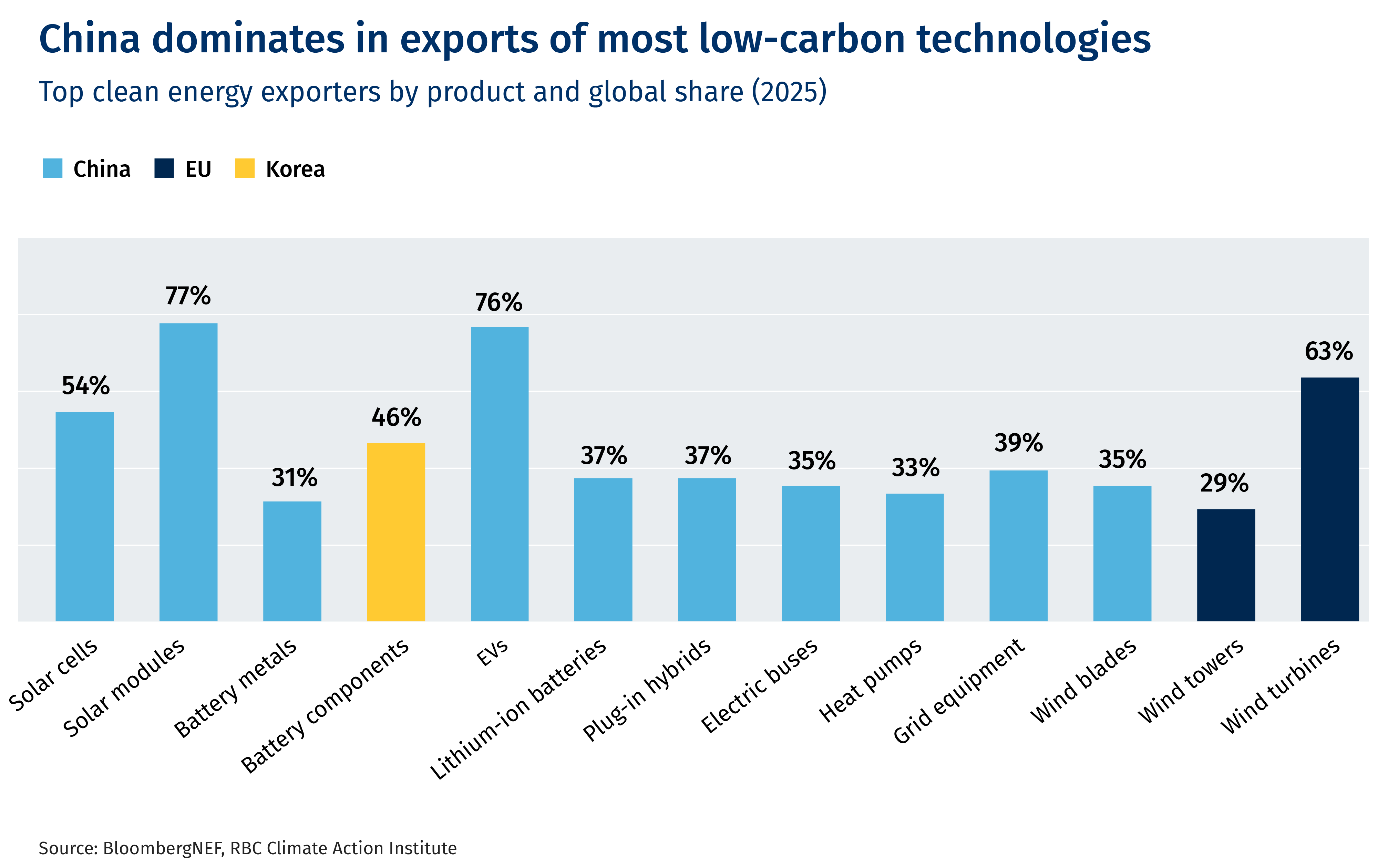

How the Hormuz crisis is accelerating China’s clean-tech dominance

Interesting tidbits

- Flipping burgers on the grill will be a costly affair this summer. Beef prices are up 62.6% since 2021 as droughts, shrinking cattle herds, and higher production costs drive up prices. While some farms are looking to boost their cattle numbers, the rising cost of diesel fuel and dry conditions, especially across the Prairies, present obstacles. Some producers are also taking advantage of high prices to liquidate their herds and retire. Fresh or frozen pork is also up 23.7%, while fresh or frozen chicken has shot up 25.7% during the period.

- US$30 million. The record estimate for a 67-million-year-old Tyrannosaurus rex fossil that will be auctioned by Sotheby's in July. The auction house claims it's the most complete skeleton ever discovered.

- Drones are helping protect animals from poachers. Icarus, an US$83-million project backed by the EU, will see the launch of six satellites by mid-2027 and process real-time data on animal movements worldwide. Dubbed the “Internet of Animals,” the satellites can detect “patterns of panic” among animals, potentially saving endangered species—and track down the poachers. The technology is backed by advances in tagging chips that are now small enough to be embedded in butterflies. Project lead and ornithologist Martin Wikeski is hoping to tag 100,000 animals globally by 2030.

- 1 in 5. The number of landlords in Canada offering tenants incentives such as reduced parking fees, gift cards and cash bonuses, Rentals.ca and Urbanation data shows. The market has seen 19 consecutive months of rent declines.

Today's funny

REMINDER: Most of my new clients come to me via word of mouth as I don’t advertise or engage in marketing programs. Please keep my team in mind if you hear of anyone with over $1 million in investable assets who is in need of wealth management services.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.