Michael Wilkie

May 8, 2026

A Word from Mike

Hello,

Despite limited clarity around a resolution to the Middle East conflict, markets have remained relatively constructive. I provide some context around the factors supporting investor sentiment, along with recent developments from central banks.

A Delicate Balance

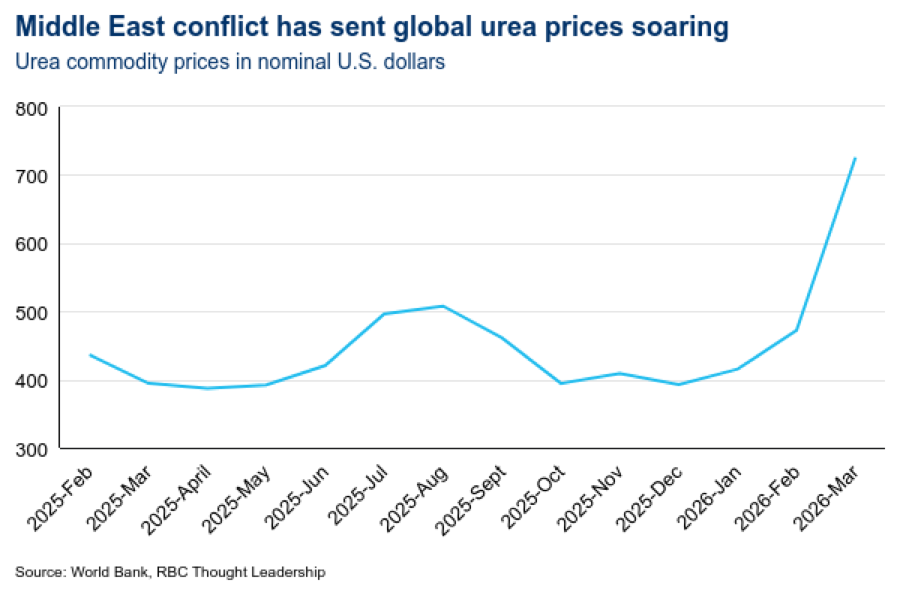

The U.S.-Iran ceasefire remains broadly intact, even as progress has been uneven. With diplomatic channels still active behind the scenes, a negotiated resolution that reopens the Strait of Hormuz remains a reasonable base case scenario, but markets appear to have already priced in much of this outcome.

Equity markets have pushed to new highs, supported by an economy that has demonstrated resilience despite elevated commodity prices. This strength reflects several reinforcing factors: strong corporate earnings, ongoing AI-driven business investment, consumers absorbing higher energy costs better than anticipated, and an economy that is structurally less oil-intensive than in prior decades.

Nevertheless, the current environment is best characterized as “tenuously stable”, with timing the key variable. The longer the Strait remains closed, the more strain builds beneath the surface. Temporary buffers—inventory drawdowns, strategic reserve releases, and logistical workarounds—have helped cushion the immediate oil supply disruption. As these buffers diminish, the supply-demand imbalances could become more acute, increasing the risk that elevated energy prices begin to weigh more meaningfully on economic activity.

AI Spending Meets Earnings Test

The latest round of Big Tech earnings was closely watched, given the group’s outsized influence on market performance and elevated profit growth expectations. Overall, results were constructive, with most companies continuing to deliver solid revenue expansion, healthy margins, and strong cash flows. Investor reactions, however, remained selective, with markets rewarding companies showing that heavy AI-related spending is translating into tangible earnings rather than simply higher capital intensity.

Upward earnings revisions have also helped improve the group’s valuation relative to expected growth, though I expect some degree of scrutiny to persist as AI-related spending, already sizeable, continues to scale higher. Reassuringly, earnings releases from semiconductor companies so far have reinforced confidence that AI infrastructure demand remains robust. I continue to view AI as a compelling long-term growth theme, while recognizing that concentrated market leadership and elevated expectations reinforce the importance of disciplined portfolio diversification.

Central Banks Hold Steady

Recent central bank decisions were largely in line with expectations, with both the Bank of Canada (BoC) and the Federal Reserve (Fed) holding policy rates steady. Long-term inflation expectations remain well anchored, giving policymakers flexibility to remain patient as they assess how the Middle East conflict may affect prices, consumer spending, and business sentiment. Since the onset of the U.S.-Iran war, markets have pared back expectations for lower interest rates, with investors now anticipating both the Fed and BoC to remain on hold through the next several meetings.

The latest Fed meeting also marked Jerome Powell’s final meeting at the helm. Powell indicated he plans to remain on the rate-setting committee as a governor for a period "to be determined," delaying the need for the Trump administration to nominate another board member. As Kevin Warsh’s nomination to succeed him as chair continues to advance through the Senate confirmation process, attention could shift toward the leadership transition at the central bank. While the Fed’s monetary policy framework tends to evolve gradually, shifts in communication styles and policy “reaction functions” to macro developments can occasionally introduce short-term market volatility as investors adjust to a new leadership regime.

Takeaway

Geopolitical headlines will likely remain noisy with the U.S. and Iran conflict locked in a negotiating phase. Recent strength in equities has been fundamentally supported by sturdy profit growth, but I am mindful that markets have largely embraced the narrative of a timely resolution. This leaves the outlook more sensitive to delays, as the cumulative effects of high commodity prices could become more pronounced over time. Keeping a long-term perspective, combined with an awareness of evolving risks, remains a useful approach for navigating the near-term uncertainty.

Highlights

The delicate shift toward an efficiency-driven economy

U.S. equity markets are at record levels, supported by resilient corporate earnings and a willingness from investors to look through ongoing geopolitical risks in the Middle East. However, a widening gap is emerging between asset prices and underlying economic conditions.

Regional developments: Alphabet issued its first loonie-denominated bond, the largest Canadian corporate bond deal on record; U.S. equity markets shrugged off geopolitical concerns as AI investment took center stage; Europe fighting inflation, but secondary effects seem limited; New inflation risks emerging in India.

Please take some time to review the Global Insight Weekly.

Global Insight Monthly

May 2026 edition

I am pleased to share the latest investment strategy report from RBC Wealth Management—Global Insight, which provides our current thoughts on asset classes, the economy, and timely issues that impact investment strategy.

Full report: Global Insight

This month’s highlights:

Midterms, the market, and what matters

The U.S. midterm election in November is shaping up to be a referendum on Trump 2.0. Independent voters and views on the economy could tip the scales. We examine historical equity market performance surrounding midterm elections, and what this might—or might not—be suggesting for this year and next.

Global equity: Was that all there is?

The outlook for equity markets, already faced with the historical challenges of a midterm election year, is now additionally dependent on how soon the Strait of Hormuz can reopen.

Global fixed income: Central banks have seen enough

After biding their time, we now see some major global central banks pivoting to rate hikes in the months ahead.

U.S. Recession Scorecard: A more constructive picture

After years of slowly edging toward a recessionary red complexion, the Scorecard looks to have reversed course and is slowly shifting toward expansionary green, a positive for the equities outlook.

Canada launched its first national sovereign wealth fund

The Canada Strong Fund will be seeded with $25 billion in capital over three years and support major new projects, alongside private and foreign investors. Canadian citizens will be able to invest in the fund with their initial invested capital protected. The fund will be run as an arms-length Crown corporation, focusing on domestic assets and projects and reporting to Parliament, the government said.

Ottawa is projecting a smaller deficit despite more spending

Finance Minister François-Philippe Champagne's spring fiscal update projected an estimated deficit of $66.9 billion for the 2025-26 fiscal year, an $11.5-billion improvement over what the government had forecast in its November budget. New spending includes recent multi-billion-dollar announcements such as GST credit and gas tax breaks and $6 billion over five years to boost skilled traded. Canadian workers and employers will also get a break on Canada Pension Plan premiums, with base contributions dropping to 9.5% from 9.9% from 2027.

The Canadian economy grew for a fourth straight month

The 0.2% gain in February was led by a 1.8% increase in the manufacturing sector. Looking ahead, the advance estimate for March GDP was “essentially unchanged,” Statistics Canada stated. On a quarterly basis, activity remains broadly consistent with RBC Economics’ base case for moderate expansion, with Q1 GDP tracking slightly higher than its own forecast of 1.3%. Across the border, the U.S. economy grew 2% in the first quarter, remaining resilient in the face of compounding shocks, such as higher gas prices.

Canada is offering a $1.5 billion in support to tariff-hit sectors

Steel, aluminum and copper sectors can tap a new billion-dollar Business Development Bank of Canada program, plus $500 million in additional funding. In April, the U.S. began levying a 25% tariff on the entire value of imported “derivative” goods made of steel, aluminum and copper. The Canadian industry has argued that higher tariffs are hurting American businesses, with Ford Motors reporting that the company's commodity costs have doubled to US$2 billion, largely due to rising aluminum costs.

Corporate America is raking in revenues and profits

With just over a quarter of S&P 500 companies reporting results for the first quarter, major U.S. companies are projected to post healthy results. Year-over-year growth in earnings per share in Q1 could exceed 13% for the sixth quarter running, data firm LSEG estimates. Tech firms are expected to lead, with a 48% jump in earnings per share, while materials (32.2%) are also expected to outpace the broader market. The upbeat assessment contrasts with U.S. consumer sentiment which hit a record low in April.

Donald Trump’s 10% global tariffs are unlawful

The ruling by the U.S. Court of International Trade is another blow to the U.S. president’s push for sweeping levies under his aggressive trade agenda. The tariffs were meant to replace earlier levies the U.S. Supreme Court had deemed illegal. But the CIT only blocked enforcement against the two companies and Washington State that filed the case, making clear it was not issuing a so-called “universal injunction.”

Saudi Arabia’s Red Sea Coast is emerging as a new Middle East port hub

The port of Neom, originally built as an anchor for a new residential, tourism and business developments on the kingdom’s west coast, has gained strategic importance as the country seeks alternative the Strait of Hormuz which is caught in the U.S.-Iran standoff. Airlines from Kuwait and Bahrain are also temporarily moving some operations to Saudi airports, while the government also launched five new “logistics corridors” this month that link ports on the Gulf with the Red Sea.

Charts of the day

Trade Zone: A perfect storm rippling across the world's food supply chains

A New Blueprint: How Modern Methods of Construction can help solve Canada’s housing crisis

Interesting tidbits

Windsor, Ontario, is Canada’s allergy capital. That’s the finding of the Aerobiology Research Laboratories report, noting that “annual pollen loads across Canada show a clear overall upward trend despite year-to-year variability.” Apart from Windsor, Ontario cities Hamilton, Barrie and Kingston, and Victoria in British Columbia are the other cities most challenged by seasonal pollen allergies, the report found. Climate change is the main “catalyst” for the doubling in pollen over the past 25 years given their propensity to thrive in warmer weather and milder winters.

US$22 trillion. The current combined valuation of the Magnificent Seven U.S. tech stocks—Apple, Alphabet, Amazon, Meta, Microsoft, Nvidia, and Tesla. That’s as much as the total market cap of all developed stock markets (outside the U.S.)

$500. The fine Canadians will have to pay if they don’t fill out the census, to be released by Statistics Canada next week. The agency collects demographic, social, and economic information for the Census of Population from every household every five years.

Today’s funny

“Frankly, he’s so loud I think he must be compensating for something.”

REMINDER: Most of my new clients come to me via word of mouth as I don’t advertise or engage in marketing programs. Please keep my team in mind if you hear of anyone with over $1 million in investable assets who is in need of wealth management services.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.