Buy-sell agreements

A private corporation held by more than one shareholder often has an agreement in place to deal with the death, disability or retirement of one of its shareholders, conflict among its shareholders or other special circumstances. This agreement, known as a "buy-sell agreement," generally provides for the sale of shares by an existing shareholder and the acquisition of those shares by one or more of the remaining shareholders, the corporation or third parties.

A private corporation held by more than one shareholder often has an agreement in place to deal with the death, disability or retirement of one of its shareholders, conflict among its shareholders or other special circumstances. This agreement, known as a "buy-sell agreement," generally provides for the sale of shares by an existing shareholder and the acquisition of those shares by one or more of the remaining shareholders, the corporation or third parties.

Family Office Services

February 14, 2026

Buy-sell Agreements

A private corporation held by more than one shareholder often has an agreement in place to deal with the death, disability or retirement of one of its shareholders, conflict among its shareholders or other special circumstances, such as a shareholder facing a marriage breakdown. This agreement, known as a "buy-sell agreement," generally provides for the sale of shares by an existing shareholder and the acquisition of those shares by one or more of the remaining shareholders, the corporation or third parties.

This article is intended to provide an overview of some common triggering events that may be dealt with in a buy-sell agreement and the considerations involved with share valuations. As well, the article will provide an overview of funding options and other considerations for a buy-sell agreement.

Any reference to a spouse includes a common-law partner.

What is a Buy-sell Agreement?

Buy-sell agreements are a crucial part of a business succession plan, and it is important to have the specific clauses drafted to meet the intentions of all parties entering into the agreement. Buy-sell agreements are generally designed to provide a mechanism for transferring share ownership upon the occurrence of certain triggering events that may cause adverse circumstances. The ultimate purpose of the agreement is often to ensure the smooth transfer of shares from a departing shareholder, while avoiding any disputes and without jeopardizing the financial well-being of the departing shareholder or the corporation. For smaller corporations, a buy-sell agreement may provide a degree of liquidity for shares that are normally illiquid. In circumstances where the shareholders are a tight knit group of individuals, a buy-sell agreement might help prevent or reduce the possibility of a shareholder selling their shares to an unknown third party. This enables the remaining shareholders to decide whether there will be a new shareholder and, if so, who the next shareholder will be.

A buy-sell agreement can be a separate standalone document. It can also be part of a more comprehensive shareholder agreement that outlines, among other things, the interests and obligations of the shareholders, share transfer restrictions, as well as any steps to remedy shareholder disputes.

A buy-sell agreement (or buy-sell provisions in a shareholder agreement) will outline the parameters for the sale of shares by a departing shareholder and the acquisition of those shares by the remaining shareholders, the corporation or third parties. The buy-sell agreement is generally initiated by a triggering event which will result in a specific sequence of predetermined actions by the shareholders and, in certain instances, the corporation. The result is that the departing shareholder will receive proceeds in accordance with a share valuation method set out in the agreement.

Elements of a Buy-Sell Agreement

While buy-sell agreements can vary due to the complexity of the corporate structure or the needs of the shareholders, the common elements found in all buy-sell agreements are:

• A triggering event

• A share valuation method

• A manner of financing the share purchase

Triggering Event

Buy-sell agreements will generally identify certain events, known as "triggering events," that may result or require the transfer or disposition of a shareholder's shares and address how this transfer or disposition should be dealt with.

It's important to note that in any of the following cases, where there are multiple remaining shareholders who may want to exercise a right to purchase a departing shareholder's shares, the agreement can be drafted so the purchase is done on a pro-rata basis. This helps ensure the relative ownership stakes remain the same between the remaining shareholders.

Death of a Shareholder

On the death of a shareholder, all of their assets, including their directly held private company shares, fall into their estate to be distributed to their beneficiaries in accordance with their Will, or, if they have no Will, provincial intestacy laws. It's easy to imagine scenarios where beneficiaries with no business experience may not want to participate in the business, or where remaining shareholders may not want the beneficiaries to be involved in the business. A typical "transfer at death provision" that may be included in a buy-sell agreement would provide surviving shareholders with a right of first refusal to purchase the shares on the death of a shareholder followed by an option for the corporation to redeem the shares if all surviving shareholders refuse to purchase the shares. An important element of this provision is that the personal representative of the deceased shareholder is obliged to abide by the buy-sell agreement.

Bankruptcy or Default of a Shareholder

Identifying bankruptcy or defining another form of default as a triggering event may help protect the corporation from an involuntary liquidation of assets to satisfy a shareholder's creditor claims. Shareholders of a corporation will generally want to protect the corporation from the personal creditors of each shareholder. If a shareholder becomes insolvent, it may be possible for a creditor to encumber or seize their shares. A creditor that seizes shares may not be subject to the same transfer restrictions as ordinary shareholders since they were not a party to a buy-sell agreement. This means existing shareholders may have little protection from the sale of the shares on the open market to an unknown third party. Accordingly, if a shareholder declares bankruptcy or becomes insolvent, the corporation or the remaining shareholders may wish to have the right to purchase their shares to prevent their distribution to creditors.

Disability

If a shareholder becomes disabled, they may want to exit the business and realize the fair market value of their interest in the corporation to pay for their care. Alternatively, a shareholder may no longer be able to participate in the business due to a loss of mental capacity, and the other shareholders may not want that shareholder's personal representative to step into their shoes and vote on their shares. In either circumstance, it's important to identify the definition of disability and the duration of the disability that would trigger the event of purchasing the disabled shareholder's shares.

Termination of Employment

When a shareholder actively involved in the business is terminated, the remaining shareholders may not want the departing shareholder to have any interest in or influence over the corporation. Identifying the termination of employment from the corporation as a triggering event provides an opportunity for remaining shareholders to maintain control among those still active in the business.

Marriage Breakdown

Without a domestic contract in place, it's possible for a shareholder's interest in a business to be subject to division-of-property regimes under provincial family law legislation. Buy-sell agreements are typically structured to prevent the spouse of a shareholder from obtaining ownership of the shares of the company. It's possible to include a provision in the buy-sell agreement to require each shareholder to enter into a marriage or domestic contract with their non-shareholder spouse, which would exclude the shares from division on separation or divorce. Alternatively, it's possible to provide the remaining shareholders with the right to buy out the shareholder who's separating or divorcing their spouse. This right can be exercised before the shares are awarded to their spouse under the division of property regime, or from the shareholder's former spouse, should shares be given to them as part of the division of assets.

Common Buy-out Clauses

In addition to the triggering events mentioned, there may be circumstances where a shareholder desires to sell their shares because they want to exit the business. The reasons for the shareholder's desire to sell may be due to a conflict with other shareholders. Alternatively, they may have been approached with an offer to buy their shares. To address this situation, these clauses are also typically included as part of a buy-sell agreement:

- Shotgun Clause: This clause is often included in a buy-sell agreement as a means of immediate dispute resolution where there has been a breakdown in the relationship among shareholders or groups of shareholders that can't be resolved. This remedy is generally used in cases involving two 50/50 shareholders. Where there are more than two shareholders, it's important that this clause be carefully drafted, as the situation is more complex.

When a shotgun clause is invoked, the initiating shareholder will set a specified price at which they're prepared to buy the other shareholder's interest in the business or sell their own interest. The responding shareholder may choose the option they prefer within a specified timeline. If the responding shareholder doesn't respond within the stipulated timeframe, then the initiating shareholder can often force the sale of the responding shareholder's shares to themselves. The expectation is that the offer would be reasonable due to the possibility of the responding shareholder buying out the initiating shareholder.

- Shareholder Offering (i.e. right of first opportunity): A buy-sell agreement may require a shareholder who wishes to sell their shares to offer the shares to all other shareholders prior to offering the shares to third parties. The selling shareholder would set a price and terms of the sale and provide existing shareholders notice of an offer to sell. Only after the other shareholders of the corporation have refused to purchase the shares may the selling shareholder offer the shares to a third-party purchaser at the same specified price and terms. This may be a simpler and less costly option for selling shareholders.

- Third-party Solicitation: These clauses are typically included in a buy-sell agreement for a closely held corporation. To prevent an unknown third party from entering the business, a buy-sell agreement may require a shareholder to bring any third-party offer to purchase shares to the attention of other shareholders. There are typically three options to mitigate this scenario:

- Right of First Refusal – This clause is used when a shareholder receives an offer from a third party to purchase their shares. The selling shareholder would be required to offer to sell their shares to the other shareholders on the exact same terms before accepting the third party's offer. This gives the remaining shareholders control over who purchases the shares and may provide an indication of the market value of their shares.

- Tag-along Provision – In a situation where a third party has made an offer to purchase the shares of the majority shareholder, this clause provides the non-selling minority shareholders the opportunity to force the purchaser to acquire their shares as well. This usually provides protection and liquidity to minority shareholders if the majority shareholder's shares are being sold to an incompatible third party.

- Drag-along Provision – In a situation where a third party makes an offer to purchase the shares of the majority shareholder, this clause forces the minority shareholder(s) to also sell their shares on the same terms and conditions accepted by the majority shareholder. This allows the majority shareholder to negotiate and sell the business as a whole.

- Right of First Refusal – This clause is used when a shareholder receives an offer from a third party to purchase their shares. The selling shareholder would be required to offer to sell their shares to the other shareholders on the exact same terms before accepting the third party's offer. This gives the remaining shareholders control over who purchases the shares and may provide an indication of the market value of their shares.

Valuation

A buy-sell agreement will typically address which valuation mechanism is to be used to determine the purchase price of the shares when a triggering event occurs. Some agreements use a fixed price method, where the price is fixed at the outset and then adjusted periodically. The agreement may require that the shareholders meet annually to value the company, with each owner signing off on the agreed annual valuation. While this works to ensure a current and realistic business value is used, it's easy to potentially forget to update this annual price setting and before long, the figure may become outdated.

Alternatively, some agreements provide for a formula or rule-of-thumb approach to a business valuation. Some formulas will start with the book value and make adjustments for the appraised fair market values of specific assets, such as real estate, equipment and fixtures, and goodwill. Other formulas may determine the value of a business by applying a specified multiplier to either revenues or earnings. One of the disadvantages of the formula approach is that what seems to apply best at one point in time may be inadequate or inapplicable when the time to apply the formula occurs. As a result, the formula approach may provide a figure that doesn't represent the true value of the business. For this reason, many buy-sell agreements typically call for an independent valuator to determine the fair market value of the business. The valuation method employed would generally depend on the type of business. For example, companies with no active business (such as a holding company) would generally be valued using an asset-based approach while active businesses could be valued using a cash-flow method. One issue with using an independent valuator is that the purchase price may not be known until the exit has been triggered. This may create some uncertainty in financing the purchase.

Funding Options for the Buy-sell Agreement

Once the triggering event has occurred and the shares have been valued, sufficient liquidity is typically required to complete the transaction pursuant to the buy-sell agreement. Planning for adequate funding is crucial to the buy-sell agreement. It's common for shareholders to contemplate the funding options available to them when negotiating buy-sell agreements. In choosing an appropriate funding method, shareholders must consider the timing of the triggering event (i.e. during the lifetime or on the death of the shareholder), how the purchase will be structured, tax implications associated with the different purchase and funding options, and the financial resources that may be available to individual shareholders or the corporation.

Some examples of funding options include:

- Establishing a Sinking Fund Within the Corporation – A sinking fund is simply a pool of retained earnings a corporation sets aside for a specific purpose — in this case, to purchase any shares of an outgoing shareholder. Very few businesses have the cash flow available to establish a sinking fund, and business owners may want to invest excess cash into their business instead. Also, the amount of the fund may be inadequate if the departing shareholder leaves prematurely.

- Obtaining a Loan from a Financial Institution – The remaining shareholder(s) or corporation may consider obtaining a loan to fund the purchase shares of the departing shareholder. A shareholder may need to ensure they have sufficient assets to use as collateral for the loan. If the corporation is the one to borrow funds, there may be debt covenants included as part of the financing arrangement that may restrict the ability of the company to use its assets, or to pay dividends. Additionally, financial institutions may not be willing to lend to a company where the departing shareholder is also a key person to the company's success. This financing option also dilutes the value of the other shareholders' shares until the loan is repaid.

- Purchasing Shares of a Departing Shareholder Via Instalments – This option may provide the corporation with the liquidity necessary to complete the transaction, as they don't need to provide all the funds at once upon the triggering event. However, this could create risk for the departing shareholder, as there's no guarantee the corporate earnings will be able to support future instalment payments.

- Life Insurance – Life insurance has become one of the preferred funding options for buy-sell agreements, particularly when dealing with a share purchase on the shareholder's death. Life insurance can be a cost-effective funding method and provide an immediate influx of cash. As a result of its unique tax attributes, life insurance may also provide significant tax benefits to the deceased shareholder's estate. Life insurance may not, however, be a viable option where a shareholder is uninsurable or where a triggering event occurs during the lifetime of a shareholder.

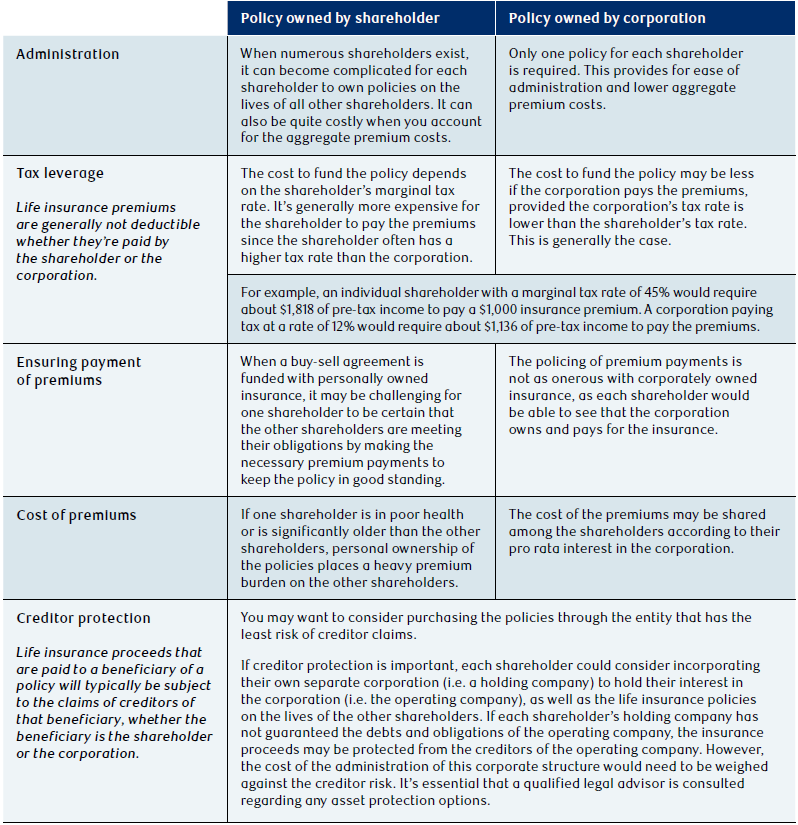

Funding a Buy-sell Agreement with Life Insurance

There are various ways of structuring buy-sell agreements using life insurance. To determine which structure is most appropriate, you need to decide whether to fund the arrangement with corporately owned (corporation pays the premiums) or personally owned (shareholder pays the premiums) life insurance.

The following chart sets out factors to consider when deciding whether the shareholder or the corporation should own and pay for the life insurance policy:

Tax Considerations Relating to Buy-sell Agreements or Provisions

When contemplating the different methods by which shares will be dealt with when a triggering event occurs, it's important to consider the tax implications associated with these methods. For example, if the departing shareholder's shares are redeemed by the corporation, this may result in a deemed dividend and capital gain or loss for the shareholder. A dividend is generally taxed at a higher tax rate than a capital gain. A capital loss can't be used to offset the dividend. (Note that if a corporation has a positive capital dividend account balance as a result of the receipt of insurance proceeds on the death of the shareholder, it may be able to elect to treat this dividend as tax-free.) As well, the shareholder will not be able to utilize their capital gains exemption. On the other hand, if the shares are purchased by the remaining shareholders, the departing shareholder may realize a capital gain. The departing shareholder may be able to use their capital gains exemption to shelter this gain from tax. As well, a capital gain is generally taxed at a lower rate than a dividend.

The tax rules that apply where insurance is used to fund a buy-sell agreement are also generally more complex where the insurance policy is owned by the corporation than when the insurance policy is owned by the individual shareholders.

Tax considerations are also important when drafting the wording of particular buy-sell provisions. For example, when you pass away, you're deemed to dispose of your capital property, including private company shares, at fair market value, unless that property passes to your spouse. If the property "vests indefeasibly" in your spouse within 36 months of your death, a tax-deferred rollover is available. Vested indefeasibly generally refers to the undisputable and enforceable right to ownership of property.

If your Will leaves everything to your spouse, but your buy-sell agreement requires your surviving spouse to sell your shares on your death, it's possible that a rollover may not be available. This is because the Canada Revenue Agency has generally taken a position that if the shares are subject to a compulsory sale by the spouse, the shares will not vest in your spouse. The shares will vest in your spouse, however, if the shares are transferred to your spouse and are merely subject to an option to purchase by the remaining shareholders or corporation.

When structuring a buy-sell agreement or buy-sell provisions in a shareholder's agreement, it's important that you seek advice from a qualified tax advisor.

Conclusion

A buy-sell agreement's validity and value come from properly thought-out and careful drafting. If the triggering events are ambiguous, it may result in confusion and uncertainty between the shareholders. This may require a dispute resolution process, which can be costly and time-consuming. Similarly, it's extremely important to ensure that a valuation method is agreed upon before the triggering event occurs to minimize potential disputes between shareholders, and to ensure the funding options chosen adequately cover the price of the shares. It's equally important to plan for adequate funding of any transfer of shares. Well-drafted buy-sell agreements will provide shareholders with peace of mind and allow them to focus on building a successful business. If you're starting a business with other shareholders or your corporation does not have a buy-sell agreement, you may want to speak with a qualified legal advisor about putting one in place.

If you already have a buy-sell agreement in place, it's important to review it as the business grows and shareholders change. It may be necessary to enter into a new agreement when there's a new shareholder, as the existing agreement may not be binding on the new shareholder. It may also be a good idea to review the buy-sell agreement when one shareholder leaves to determine if all remaining shareholders still agree to the terms or if changes should be made.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.