Capital gains reserve

When you dispose of capital property, you may realize a capital gain or loss equal to the difference between the proceeds of disposition and the adjusted cost base (ACB) of the property. Normally, you will need to pay tax on the taxable capital gain in the year of disposition. However, you may be able to defer a portion of the capital gain and the associated taxes by claiming a capital gains reserve when you receive the proceeds over a number of years.

When you dispose of capital property, you may realize a capital gain or loss equal to the difference between the proceeds of disposition and the adjusted cost base (ACB) of the property. Normally, you will need to pay tax on the taxable capital gain in the year of disposition. However, you may be able to defer a portion of the capital gain and the associated taxes by claiming a capital gains reserve when you receive the proceeds over a number of years.

Family Office Services

October 14, 2025

Capital Gains Reserve

When you dispose of capital property, you may realize a capital gain or loss equal to the difference between the proceeds of disposition and the adjusted cost base (ACB) of the property. Normally, you will need to pay tax on the taxable capital gain in the year of disposition. However, you may be able to defer a portion of the capital gain and the associated taxes by claiming a capital gains reserve when you receive the proceeds over a number of years. Any reference to spouse in this article also includes a common-law partner.

Who Can Claim a Reserve?

You can claim the reserve when you dispose of capital property and you haven't received all the proceeds of disposition, unless you:

- were not a resident of Canada at the end of the tax year, or at any time in the following year;

- were exempt from paying tax at the end of the tax year, or at any time in the following year; or

- sold the capital property to a corporation that you control in any way.

How Do You Calculate the Reserve?

The capital gains reserve reduces the amount of the capital gain you report as income in a particular year. First you calculate your capital gain, then you reduce the capital gain by the amount of your reserve for the year. You do not have to claim the maximum reserve calculated. The maximum period over which most reserves can be claimed is four years, which allows you to spread the capital gain over a maximum of five years. There is an exception discussed later in the article. In the year after you claimed a reserve, you must add the reserve to your capital gains for the year. You may then claim a recalculated reserve amount.

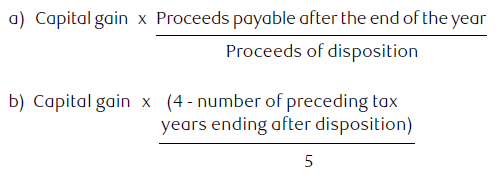

The capital gains reserve in each year cannot be more than the lesser of:

Under this formula, you can't take more than four-fifths of the gain as a reserve in the year you dispose of the capital property. Each year, you repeat the calculation to determine the amount of the reserve. As a result, you can spread the capital gain over a maximum of five years if the proceeds are received over five years or more. If the purchaser pays you the purchase price over a period longer than five years, for example, an eight-year period, you must still recognize the capital gain in full over a period of five years.

You must recognize the capital gain in full by the year in which you receive the final payment. So, if the purchaser pays you 50% of the purchase price in the year of sale and the remaining 50% in the following year, you could recognize up to 50% of the original capital gain in the year of sale and the remaining 50% would have to be recognized in the following year. You will not be able to spread the recognition of the capital gain over more than two years.

Numerical Example

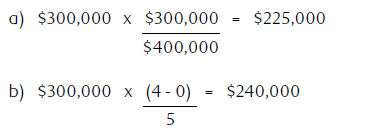

For example, let's assume you sell your cottage to your children at fair market value for $400,000. The ACB of the cottage is $100,000. You would normally declare a capital gain of $300,000 in the year of sale. However, your children can only afford to pay you $100,000 in the year of the sale, so you agree to take back a note for the remaining $300,000. Since you're not receiving all of the proceeds of the sale in the current year, you can claim a capital gains reserve in the year of the sale to defer a portion of the gain to a future tax year. The calculation of the maximum capital gains reserve you can claim in the year of sale is the lesser of:

Therefore, you can defer up to $225,000 of the capital gain to future tax years. You would only have to recognize a capital gain of $75,000 ($300,000 – $225,000), in the year of the sale. In the following year, you would include the $225,000 as a capital gain in your income and you would repeat the capital gains reserve calculation.

Nine-Year Reserve Period for Certain Types of Capital Property

You may be able to spread the capital gain you realize over a maximum period of ten years if you are transferring certain types of capital property.

The following qualifies:

- Transfer to your child of a family farm or fishing property (which includes shares of a family farm or fishing corporation, an interest in a family farm or fishing partnership, and land or depreciable property in Canada that you, your spouse, your parent or any of your children used in a farming or fishing business);

- Small business corporation shares;

- Intergenerational business transfer of shares of the capital stock of a family farm or fishing corporation or qualified small business corporation shares to a corporation controlled by one or more of your children and satisfy certain criteria over a 36-month period or within 10 years;

- Qualifying business transfer of the shares of a qualifying business to either an employee ownership trust (EOT) or a Canadian controlled private corporation that is controlled and wholly owned by an EOT.

Your child includes any of the following:

- a person of whom you or your spouse is the legal parent;

- your grandchild or great-grandchild;

- your child's spouse;

- another person who is wholly dependent on you for support and who is, or was immediately before the age of 19, in your custody and under your control;

- for purposes of intergenerational business transfers, a child includes, in addition to this list, a niece or nephew of the transferor, niece or nephew of the transferor's spouse, a spouse of a niece or nephew of the transferor or the transferor's spouse, or a child of a niece or nephew that is a niece or nephew of the transferor or the transferor's spouse.

Lifetime Capital Gains Exemption (LCGE)

A capital gain that you bring into income in the year following the year you claim a reserve may still qualify for the LCGE. To qualify, the original capital gain must qualify for the LCGE. Generally, you qualify for the LCGE if you dispose of shares of a qualifying small business corporation or qualified farm or fishing property.

Reserve for a Gift of Non-Qualifying Securities

If you donate non-qualifying securities, other than an excepted gift, to a qualified donee which results in a capital gain, you may be able to claim a reserve to postpone the inclusion of the capital gain in income.

Examples of a non-qualifying security include (but is not limited to):

- a share of a corporation with which you do not deal at arm's length after the donation is made;

- an obligation of yours, or of any person or partnership, with whom you do not deal at arm's length after the donation is made;

- any other security issued by you or by any person or partnership with whom you do not deal at arm's length after the donation is made.

An excepted gift is a gift of a share you made to a qualified donee with whom you deal at arm's length. The qualified donee cannot be a private foundation. If the donee is a charitable organization or public foundation, it will be an excepted gift if you deal at arm's length with each director, trustee, officer and official of the donee.

Claiming the Reserve Over Different Capital Gains Inclusion Rate Periods

The year the capital gain is taxed determines the capital gains inclusion rate that will apply to the gain and ultimately the tax you will pay. Where you have taken a reserve in one year, you must bring the reserve into income and add it to your capital gains of the current year. The inclusion rate in the current year will be applied in determining the taxable capital gain.

As the capital gains inclusion rate is applied to the reserve, any potential change to this inclusion rate could impact your ultimate tax liability.

Other Considerations

When deciding if you should claim the reserve, you'll want to consider your current and future marginal tax rate. The deferral of the capital gains can be especially advantageous if you expect to be in the same tax bracket or a lower tax bracket over the next four years.

Another benefit of claiming the capital gains reserve is the ability to match the cash flow from the proceeds of sale to the income tax payment.

If you receive certain income-tested benefits, bear in mind that deferring recognition of capital gains can be a potential disadvantage. This is because when you include portions of the capital gain in your income in future years, certain benefits to which you may be entitled (e.g. Old Age Security) may be reduced.

In addition, in the year of death, your executor cannot claim a reserve. Any remaining deferred capital gain must be included in your final return and your estate is responsible for the related tax liability.

Conclusion

If you're selling your property with accrued gains and will not be receiving all of the proceeds in that year, the capital gains reserve may help you defer or reduce taxes. Speak to a qualified tax advisor for more information.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.