Charitable donations

What you need to know when you make a personal donation. To encourage charitable giving, the government provides you with a tax credit when you make a donation to a registered charity. You can use this donation tax credit to reduce your taxes payable. This article provides an overview of how you can qualify for the donation tax credit and how the tax credit is calculated.

What you need to know when you make a personal donation. To encourage charitable giving, the government provides you with a tax credit when you make a donation to a registered charity. You can use this donation tax credit to reduce your taxes payable. This article provides an overview of how you can qualify for the donation tax credit and how the tax credit is calculated.

Family Office Services

October 14, 2025

Charitable Donations

What you need to know when you make a personal donation

To encourage charitable giving, the government provides you with a tax credit when you make a donation to a registered charity. You can use this donation tax credit to reduce your taxes payable. This article provides an overview of how you can qualify for the donation tax credit and how the tax credit is calculated. Please note that any reference to a spouse in this article also includes a common-law partner.

Qualifying Donations

To qualify for the donation tax credit, you must make a donation to a qualified donee. Qualified donees are generally those organizations which can issue official donation receipts for the gifts they receive. They can be charitable organizations, public foundations or private foundations. Typically, a registered charity is a qualified donee. In this article, the terms qualified donees and registered charities are used interchangeably.

The Canada Revenue Agency (CRA) maintains a list of qualified donees on their website. When you're ready to make a donation, you may wish to check the list to determine if a particular charity is currently registered and can issue official donation receipts.

The CRA considers a gift to be a voluntary transfer of money or property for which you expect and receive no consideration. You can make these gifts in cash or in-kind if the qualified donee accepts non-cash gifts.

Donation receipts are issued for the eligible amount of a gift made to a qualified donee; this is generally the fair market value of the donation. In certain instances, an advantage may be deemed to be received which reduces the amount of the eligible donation. An advantage is generally the total value of any property, service, compensation, use or any other benefit you are entitled to as partial consideration for, or in gratitude for, the gift. An example of this would be if you purchased a table for a charity benefit and it cost $500. The value of the food and party is considered an advantage with a value of $250, therefore the eligible donation amount would be $250 ($500 less the $250 advantage amount).

To receive an eligible donation receipt for a particular tax year, you need to make the donation by December 31 of the tax year.

Mechanics of the Donation Tax Credit

When you make a donation to a registered charity, you may claim a tax credit on your personal tax return. The donation tax credit reduces your income taxes in the year you make the claim.

To receive an eligible donation receipt for a particular tax year, you need to make the donation by December 31 of the tax year.

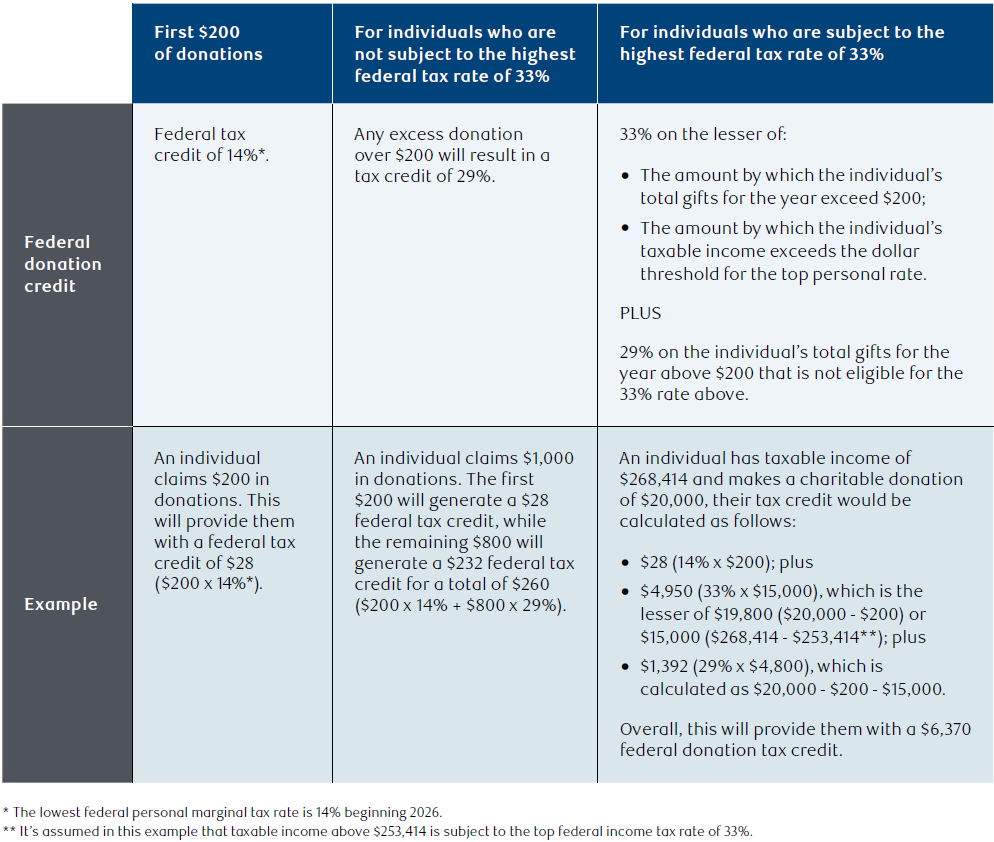

The donation tax credit is non-refundable, which means the tax credit can't reduce the amount of your tax below zero. Federally, there are three levels of tax credits that may be available to you depending on your taxable income and the amount of the donation. The following table illustrates how you calculate your donation tax credit.

In addition to the federal tax credit illustrated in the table, you may also receive a provincial/territorial donation tax credit. The amount of the credit will vary depending on your place of residence. If you currently live in a province that has a surtax (Ontario has a surtax), the donation tax credit will reduce your taxes payable which will reduce your surtax payable.

Donation Timing and Carry-Forward

You're not required to claim the donation tax credit in the year you make the donation. Instead, you may carry it forward for up to five years (or 10 years for a gift of certified ecologically sensitive land). This gives you flexibility with regards to claiming your donations. For instance, it may make sense to save all your donation receipts for a higher income year in order to maximize the credit you receive at the higher federal rate. Further, if you make small annual donations, it may make sense to claim the combined donations to utilize the higher credit for gifts above $200 in a future year. You cannot carry back donations to a previous tax year.

Maximizing the Donation Tax Credit Between Spouses

The CRA allows you and your spouse to combine your donations made in a given tax year and the previous five years (or 10 years for a gift of certified ecologically sensitive land) to the extent you have unclaimed donations for the purposes of the donation tax credit. This enables you and your family to maximize your donation tax credit. If both you and your spouse have made separate donations, consider pooling them and reporting them on the tax return of the spouse who will benefit the most from them. This will generally be the higher income spouse.

Limit on Donation Amount

There is no limit to the amount you can donate in a year. However, for tax purposes, you can generally only claim a charitable donation of up to 75% of your net income in a taxation year. There are exceptions to this limit, for example, where you donate cultural property or ecological land. In some cases, if you donate capital property, the limit is also increased. If you're a resident of Quebec, the limit is 100% of your net taxable income for Quebec tax purposes. This limit is also 100% of net income in the year of death and the preceding year.

For example, assume Jane's net income for the year is $100,000 and she is a resident of Alberta. She received a large inheritance in the same year and decides to make a donation of $200,000 to her favourite charity. Jane will only be able to claim a maximum of $75,000 (75% x $100,000) of donations for tax purposes this year. Jane can carry forward the remainder for a maximum of five years (or 10 years for a gift of certified ecologically sensitive land).

Bequests Under a Will

When a gift is made in your Will (or by beneficiary designation under a registered retirement savings plan (RRSP), registered retirement income fund (RRIF), tax-free savings account (TFSA), tax-free first home savings account (FHSA) or life insurance policy), the donation is deemed to be made by the estate at the time the donation is made to a qualified donee. The donation tax receipt will be based on the fair market value of the gift at the time the property is transferred to the qualified donee.

The executor/liquidator of an individual's estate may have some flexibility in their use of the donation tax credit if at the time the donation is made, the estate is a graduated rate estate (GRE). A GRE is an estate that arises on and as a consequence of the individual's death and satisfies the following conditions:

• The estate is a testamentary trust for tax purposes;

• No more than 36 months have passed since the deceased's date of death;

• The estate designates itself, in its T3 return of income for its first taxation year (or if the estate arose before 2016, for its first taxation year after 2015), as the individual's GRE;

• No other estate is designated as a GRE of the individual (there can only be one GRE); and

• The estate includes the deceased individual's Social Insurance Number in its return of income for each taxation year of the estate that ends after 2015.

If the estate is a GRE at the time the property is transferred to the charity, the executor/liquidator has the flexibility to allocate the donation tax credit among:

• The taxation year of the estate in which the donation is made;

• An earlier taxation year of the estate;

• The last two taxation years of the deceased individual; or

• Any of the five taxation years (or 10 years for a gift of certified ecologically sensitive land) of the estate subsequent to the donation.

If the executor/liquidator makes the donation in the fourth or fifth year of the estate, and the estate continues to meet the requirements of the definition of a GRE, other than the 36-month period, the executor/liquidator may use the donation tax credit in the taxation year of the estate in which the donation is made; any prior year of the GRE, or the last two taxation years of the estate. Donation tax credits that are not used in the GRE context and are carried forward for individuals who are beneficiaries may also be carried forward five years (or 10 years for a gift of certified ecologically sensitive land).

In addition, to benefit from this flexible use of the donation tax credit, the donated property must be properly taxed as an asset in the estate on and as a consequence of the death (or property that was substituted for such property).

Alternative Minimum Tax (AMT)

If you're making a donation to reduce your tax liability, it's very important to consider AMT. This tax aims to ensure that every Canadian individual pays a minimum amount of tax. The calculated AMT is based on the adjusted taxable income, which seeks to remove some of the advantages of certain tax-preferential items such as the donation tax credit. If the AMT calculated is greater than your regular tax liability, the AMT becomes your tax liability for the year. The difference between the AMT you have to pay in a year and your regular tax liability can be carried forward for seven years to reduce your future regular income tax liability when your taxes payable exceed your AMT.

For more information about AMT and charitable giving, ask your RBC advisor for an article on this topic. Be sure to speak with a qualified tax advisor to help you determine how AMT may affect your charitable giving.

Conclusion

Making charitable donations provides you with a chance to make a contribution to your community and receive tax benefits at the same time. This article provides a summary of the basic tax incentives when you donate personally. If you're thinking about donating through your private corporation or donating securities in-kind, speak with your RBC advisor for more information.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide specific advice or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.